MARKET INSIGHTS

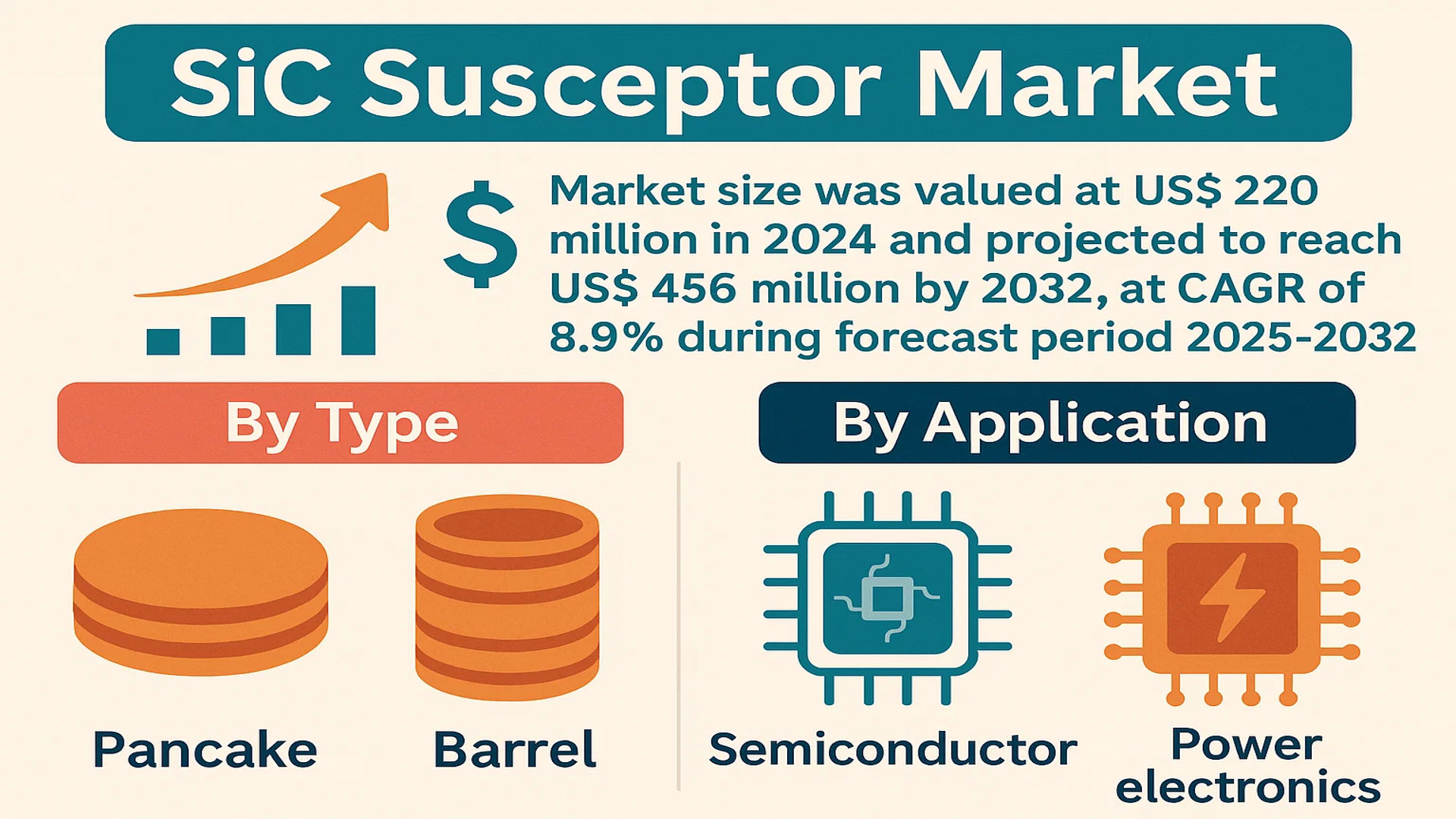

The global SiC Susceptor Market size was valued at US$ 220 million in 2024 and is projected to reach US$ 456 million by 2032, at a CAGR of 8.9% during the forecast period 2025-2032. While North America leads in adoption, Asia-Pacific shows the highest growth potential with China accounting for over 30% of regional demand.

Silicon carbide (SiC) susceptors are critical components in semiconductor manufacturing, particularly in epitaxial growth processes for power electronics and LED production. These high-purity graphite components coated with SiC facilitate uniform heat distribution in chemical vapor deposition (CVD) and metal-organic chemical vapor deposition (MOCVD) systems. The pancake-type segment dominates with 62% market share due to its compatibility with single-wafer processing, though barrel-type susceptors are gaining traction for batch processing efficiency.

Market expansion is driven by surging demand for wide-bandgap semiconductors in electric vehicles and renewable energy systems, where SiC devices enable higher efficiency. However, supply chain constraints for high-purity graphite and complex coating processes present challenges. Key players like Toyo Tanso and SGL Carbon are investing in capacity expansions, with Tokai Carbon recently commissioning a new production facility in 2023 to meet growing 200mm wafer demand.

MARKET DYNAMICS

MARKET DRIVERS

Increased Demand for Semiconductor Manufacturing to Accelerate SiC Susceptor Adoption

Silicon Carbide (SiC) susceptors are critical components in semiconductor manufacturing, particularly in epitaxial growth processes. With the global semiconductor market expected to grow at a compound annual growth rate of over 6% through 2030, the demand for high-performance susceptors is rising proportionally. SiC susceptors offer superior thermal conductivity, chemical stability, and longevity compared to traditional graphite alternatives, making them indispensable for producing next-generation power devices. Their ability to maintain consistent temperature distribution in high-temperature environments makes them ideal for manufacturing wide-bandgap semiconductors used in electric vehicles and renewable energy systems.

Expansion of Electric Vehicle Production to Fuel Market Growth

The rapid expansion of electric vehicle manufacturing presents a significant growth opportunity for the SiC susceptor market. Power electronics in modern EVs increasingly rely on SiC-based semiconductors that require high-purity susceptors during production. With EV sales projected to surpass 50 million units annually by 2030, semiconductor foundries are scaling up production capacity, subsequently driving demand for reliable susceptor solutions. Major automotive OEMs are transitioning to 800V architectures, which further increases the need for SiC power devices that depend on quality susceptors during manufacturing.

➤ Recent industry analysis shows that the automotive sector currently accounts for over 40% of total SiC susceptor consumption, with this share expected to grow as EV penetration increases globally.

Furthermore, governments worldwide are implementing policies to support domestic semiconductor production, creating additional demand for critical components like SiC susceptors. These initiatives are expected to maintain steady market growth over the forecast period.

MARKET RESTRAINTS

High Production Costs and Material Scarcity to Limit Market Expansion

Despite strong demand, the SiC susceptor market faces notable constraints, primarily related to production costs and material availability. Silicon carbide raw material prices remain high due to complex manufacturing processes and limited global supply sources. The purification and machining required to produce semiconductor-grade SiC susceptors adds substantial costs throughout the value chain. These factors make the final products significantly more expensive than alternative solutions, potentially restricting adoption in price-sensitive applications.

Other Constraints

Technical Challenges in Manufacturing

Producing defect-free SiC susceptors with consistent properties remains technically demanding. The machining and finishing processes require specialized equipment and skilled operators, leading to manufacturing bottlenecks. Even minor imperfections can negatively impact performance in sensitive semiconductor fabrication environments.

Supply Chain Vulnerabilities

Geopolitical factors and export restrictions on critical materials continue to affect the availability of high-purity SiC. Recent trade tensions have highlighted the market’s exposure to supply disruptions, prompting manufacturers to explore alternative sources and material formulations to mitigate risk.

MARKET CHALLENGES

Material Degradation and Limited Lifespan Pose Operational Challenges

SiC susceptors gradually degrade during high-temperature semiconductor manufacturing processes, developing surface defects that eventually require replacement. This ongoing replacement cycle creates operational challenges for semiconductor manufacturers who require uninterrupted production schedules. The average lifespan of a high-quality SiC susceptor in continuous operation is approximately 6-12 months, depending on process conditions, resulting in significant recurring costs for fabrication facilities.

Additional Industry Challenges

Standardization Issues

The lack of globally standardized specifications for SiC susceptors complicates procurement and quality assurance processes. Manufacturers often need to customize susceptors for specific equipment configurations, hindering economies of scale and increasing lead times.

Technical Support Requirements

The integration of advanced susceptor designs requires substantial technical support and training. As semiconductor fabrication processes become more sophisticated, the knowledge gap between susceptor manufacturers and end-users continues to present implementation challenges.

MARKET OPPORTUNITIES

Emerging Applications in Power Electronics to Create New Growth Avenues

The expansion of 5G infrastructure and renewable energy systems is creating substantial opportunities for SiC susceptor manufacturers. These high-frequency applications demand power electronic components with superior thermal performance that can only be produced using advanced susceptor technology. The renewable energy sector alone is expected to drive significant demand growth as solar inverters and wind power converters increasingly adopt SiC-based solutions.

Innovations in Coating Technologies to Enhance Market Potential

Recent advancements in protective coatings present promising opportunities to extend susceptor lifespans and improve performance. New coating formulations that reduce surface degradation and contamination in high-temperature environments could significantly enhance the value proposition of premium SiC susceptors. These innovations are particularly relevant for next-generation semiconductor nodes where even minor contamination can impact yields.

➤ Leading manufacturers are reporting productivity gains of 15-20% from advanced coating solutions, demonstrating the potential for technology-driven market expansion.

Additionally, the development of hybrid susceptor designs combining SiC with other advanced materials may open new application areas while potentially reducing overall system costs through performance optimization.

SIC SUSCEPTOR MARKET TRENDS

Rising Demand for SiC Susceptors in Semiconductor Manufacturing

The global semiconductor industry’s rapid expansion is driving significant growth in the SiC susceptor market, with increasing adoption in epitaxial growth processes for wide-bandgap semiconductors. Silicon carbide susceptors offer superior thermal stability and chemical resistance compared to traditional graphite solutions, making them indispensable for high-temperature applications exceeding 1,600°C. With major foundries expanding production capacity for power electronics and 5G components, demand for high-purity SiC susceptors grew by approximately 18% year-over-year in 2023. The market is further propelled by the automotive sector’s transition to electric vehicles, where SiC-based power modules require precisely controlled epitaxial deposition processes.

Other Trends

Technological Advancements in Susceptor Design

Material science breakthroughs are enabling next-generation susceptor solutions, with manufacturers developing coatings that reduce particle contamination during MOCVD processes. Recent innovations include porous SiC susceptors that improve temperature uniformity to within ±3°C across 200mm wafers – a critical requirement for GaN power device production. Leading Japanese suppliers have introduced susceptor designs with 20% longer operational lifetimes through improved oxidation resistance, directly addressing one of the industry’s key cost concerns. These improvements come as wafer sizes transition to 200mm and 300mm formats in power semiconductor fabrication.

Regional Production Shifts and Supply Chain Diversification

The Asia-Pacific region currently dominates SiC susceptor consumption, accounting for over 65% of global demand, driven by concentrated semiconductor manufacturing in China, Taiwan and South Korea. However, recent government initiatives like the U.S. CHIPS Act and Europe’s semiconductor sovereignty programs are reshaping the landscape. This has led to 35% growth in susceptor procurement by North American fab projects since 2022, with suppliers establishing local production facilities to meet anticipated demand. Meanwhile, Chinese manufacturers are rapidly expanding their share in the mid-market segment, offering cost-competitive alternatives at approximately 20-30% lower price points than premium Japanese products.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Growth in the SiC Susceptor Market

The global SiC susceptor market represents a competitive yet concentrated landscape, dominated by established material science and semiconductor equipment manufacturers. Toyo Tanso and SGL Carbon collectively hold a significant market share, driven by their expertise in high-temperature graphite solutions and strong foothold in Asia-Pacific and European markets. These leaders continue to invest in advanced manufacturing techniques to meet the rising demand from semiconductor fabrication plants.

Tokai Carbon has emerged as another key player, leveraging its vertically integrated production capabilities to offer cost-competitive SiC susceptors. Their recent capacity expansion in Japan positions them strongly for the 300mm wafer fabrication boom. Meanwhile, Mersen has been focusing on proprietary coating technologies that extend susceptor lifespan – a critical factor for semiconductor manufacturers aiming to reduce tool downtime.

The market also sees dynamic competition from specialized players like Top Seiko and Schunk Xycarb Technology, who differentiate through application-specific susceptor designs. These nimble competitors are gaining traction in emerging semiconductor hubs like Taiwan and South Korea, where custom solutions for advanced packaging applications are in high demand.

Recent industry movements show established players increasingly adopting two-pronged strategies: forming strategic alliances with equipment OEMs while simultaneously diversifying into adjacent markets like SiC epitaxy. For instance, CoorsTek recently partnered with a major semiconductor tool manufacturer to co-develop next-generation susceptors capable of withstanding higher process temperatures required for GaN-on-SiC devices.

List of Key SiC Susceptor Manufacturers

- Toyo Tanso Co., Ltd. (Japan)

- Top Seiko Co., Ltd. (Japan)

- SGL Carbon (Germany)

- Tokai Carbon Co., Ltd. (Japan)

- Mersen (France)

- CoorsTek, Inc. (U.S.)

- Schunk Xycarb Technology (Netherlands)

Segment Analysis:

By Type

Pancake SiC Susceptors Lead the Market Due to High Thermal Stability in Semiconductor Manufacturing

The market is segmented based on type into:

- Pancake

- Barrel

- Cylindrical

- Custom configurations

- Others

By Application

Semiconductor Segment Dominates Owing to Increased Demand for Wafer Processing Applications

The market is segmented based on application into:

- Semiconductor

- Power electronics

- LED manufacturing

- Wireless communication devices

- Others

By Material Grade

High-Purity SiC Segment Holds Major Share for Critical Semiconductor Applications

The market is segmented based on material grade into:

- High-purity SiC

- Industrial grade SiC

- Coated SiC

- Others

By End-User

Foundries Lead Consumption Due to Large-Scale Semiconductor Production Requirements

The market is segmented based on end-user into:

- Semiconductor foundries

- IDMs (Integrated Device Manufacturers)

- Research institutions

- Wafer manufacturers

- Others

Regional Analysis: SiC Susceptor Market

North America

The North American SiC susceptor market is driven by robust semiconductor manufacturing and research investments, particularly in the U.S. With the CHIPS and Science Act injecting $52.7 billion into domestic semiconductor production, demand for high-purity SiC susceptors used in epitaxial growth processes is accelerating. Leading manufacturers like CoorsTek and Mersen dominate the regional supply chain, specializing in large-diameter pancake susceptors for 5G and electric vehicle (EV) power electronics. However, stringent export controls on advanced semiconductor technologies have created supply chain complexities, pushing local players to develop vertically integrated production capabilities.

Europe

Europe’s market prioritizes sustainability, with SGL Carbon and Tokai Carbon leading the adoption of recyclable SiC susceptor solutions. The EU’s €43 billion Chips Act is fueling demand for susceptors in compound semiconductor fabs, particularly in Germany and France. A notable trend is the shift from graphite-coated to pure SiC susceptors, driven by stricter contamination control requirements in silicon carbide wafer production. While innovation is strong, dependence on Asian raw material suppliers and energy-intensive manufacturing processes present cost challenges. Collaborative R&D initiatives between universities and corporations aim to improve susceptor lifespans beyond 1,500 deposition cycles.

Asia-Pacific

Accounting for over 60% of global SiC susceptor consumption, the APAC region is powered by China’s booming third-generation semiconductor industry. Local players like Toyo Tanso and Top Seiko aggressively compete on price, offering susceptors 20-30% cheaper than Western counterparts. Japan leads in technical sophistication, with susceptors tailored for ultrahigh-temperature (up to 2,000°C) MOCVD applications. India is emerging as a growth hotspot, with new SiC wafer plants driving 15% YoY demand increases. The region’s main challenge is quality consistency, as rapid production scaling sometimes compromises dimensional tolerances critical for uniform thermal distribution.

South America

The South American market remains niche but shows potential, with Brazil investing in local assembly of power electronics modules. Most susceptors are imported from China or the U.S., creating 6-8 week lead times that hinder just-in-time manufacturing. Argentina’s developing rare earth mining sector could enable future raw material localization, though current susceptor adoption focuses mainly on research institutions rather than volume production. Currency volatility and 35-40% import duties on advanced ceramics significantly inflate end-user costs, limiting market expansion.

Middle East & Africa

This region is in the early adoption phase, with Saudi Arabia and UAE leading demand through investments in semiconductor test and packaging facilities. The lack of local manufacturing means nearly 90% of susceptors are imported, primarily from Europe. High-growth potential exists in RF device production for telecommunications infrastructure projects, though market education about SiC susceptor benefits versus traditional graphite remains a barrier. Political instability in some areas creates supply chain uncertainties, while desert environmental conditions require specialized coatings to prevent particulate contamination during susceptor use.

Report Scope

This market research report provides a comprehensive analysis of the global and regional SiC Susceptor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Pancake, Barrel), application (Semiconductor, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Toyo Tanso, SGL Carbon, Tokai Carbon, and others, covering their product portfolios, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor manufacturing technologies, material advancements, and evolving industry standards for SiC susceptors.

- Market Drivers & Restraints: Evaluation of factors driving market growth including semiconductor industry expansion, along with challenges such as material costs and supply chain constraints.

- Stakeholder Analysis: Insights for material suppliers, semiconductor equipment manufacturers, investors, and policymakers regarding market opportunities and challenges.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SiC Susceptor Market?

-> SiC Susceptor Market size was valued at US$ 220 million in 2024 and is projected to reach US$ 456 million by 2032, at a CAGR of 8.9% during the forecast period 2025-2032.

Which key companies operate in Global SiC Susceptor Market?

-> Key players include Toyo Tanso, SGL Carbon, Tokai Carbon, Mersen, CoorsTek, and Schunk Xycarb Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising semiconductor production, increasing adoption of SiC wafers, and demand for advanced semiconductor manufacturing equipment.

Which region dominates the market?

-> Asia-Pacific dominates the market due to semiconductor manufacturing concentration, while North America shows significant growth potential.

What are the emerging trends?

-> Emerging trends include development of large-diameter susceptors, advanced coating technologies, and integration with next-gen semiconductor fabrication processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...