SiC Power Devices for New Energy Vehicles Market Overview

This report studies silicon carbide (SiC) power devices for new energy vehicles, including SiC MOSFET Module, SiC MOSFET Discrete and SiC diode. In automotive, currently the silicon carbide (SiC) power devices are mainly used in main drive inverters, On-Board Chargers, and DC/DC converters, etc.

This report provides a deep insight into the global SiC Power Devices for New Energy Vehicles market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global SiC Power Devices for New Energy Vehicles Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the SiC Power Devices for New Energy Vehicles market in any manner.

SiC Power Devices for New Energy Vehicles Market Analysis:

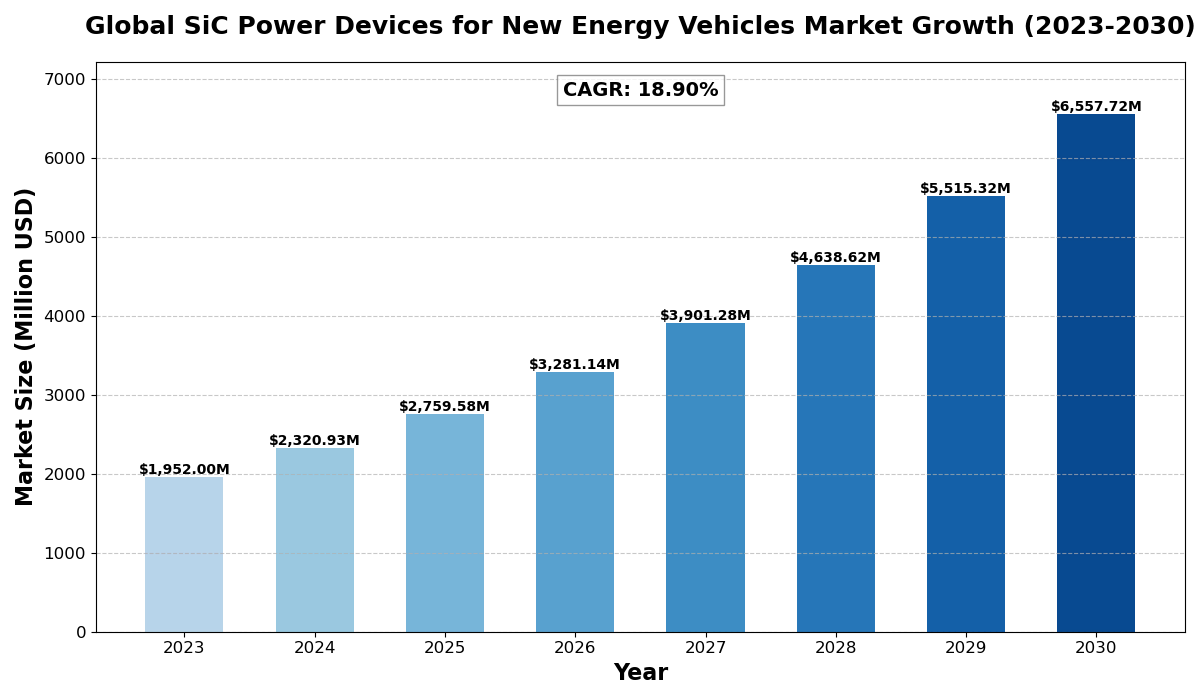

The global SiC Power Devices for New Energy Vehicles market size was estimated at USD 1952 million in 2023 and is projected to reach USD 6557.72 million by 2030, exhibiting a CAGR of 18.90% during the forecast period.

North America SiC Power Devices for New Energy Vehicles market size was USD 508.64 million in 2023, at a CAGR of 16.20% during the forecast period of 2025 through 2030.

SiC Power Devices for New Energy Vehicles Key Market Trends :

Growing Demand for SiC in EV Powertrains

Automakers are increasingly adopting SiC power devices for main inverters, onboard chargers, and DC/DC converters, enhancing efficiency and reducing power losses.Expansion of SiC Manufacturing Facilities

Leading semiconductor manufacturers are investing in new fabrication plants to meet the rising demand for SiC power devices in electric vehicles.Shift Toward High-Voltage EV Architectures

The transition from 400V to 800V systems in EVs is driving demand for SiC power devices, which offer superior efficiency and fast-charging capabilities.Advancements in SiC Module Packaging

New packaging technologies, such as chip-scale packaging and advanced cooling solutions, are improving thermal performance and reliability of SiC power devices.Supportive Government Policies for EV Adoption

Governments worldwide are offering incentives, subsidies, and regulations to accelerate the adoption of electric vehicles, indirectly boosting the demand for SiC power devices.

SiC Power Devices for New Energy Vehicles Market Regional Analysis :

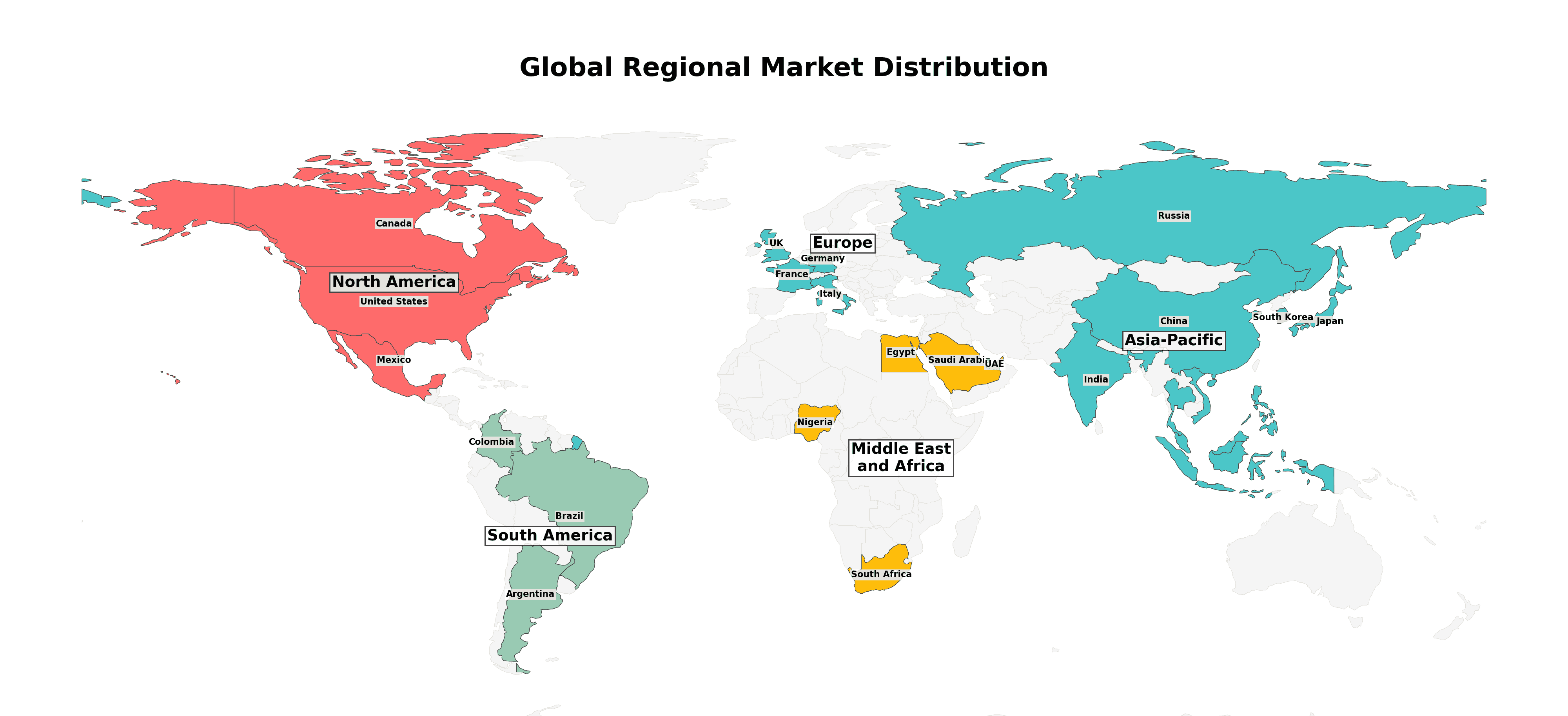

- North America:Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

- Europe:Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

- Asia-Pacific:Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

- South America:Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

- Middle East & Africa:Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

SiC Power Devices for New Energy Vehicles Market Segmentation

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- Kyocera

- Maruwa

- NGK Spark Plug

- SCHOTT Electronic Packaging

- AdTech Ceramics

- Ametek

- Murata

- Yokowo

- Hitachi Metals

- NIKKO

- Taiyo Yuden

- Adamant Namiki

- MST

- API Technologies (CMAC)

- NeoCM

- ACX Corp

- Elit Fine Ceramics

- SoarTech

- ECRI Microelectronics

- Jiangsu Yixing Electronics

- Chaozhou Three-Circle (Group)

- Hebei Sinopack Electronic Tech

- Beijing BDStar Navigation

Market Segmentation (by Type)

- HTCC Alumina Ceramic Substrates

- LTCC Alumina Ceramic Substrates

Market Segmentation (by Application)

- Industrial & Consumer Electronics

- Aerospace & Military

- Optical Communication Package

- Automobile Electronics

Drivers

Increasing EV Production and Adoption

The rising demand for electric vehicles, driven by environmental concerns and government regulations, is fueling the need for efficient SiC power devices.Higher Efficiency and Performance of SiC Power Devices

Compared to silicon-based components, SiC devices provide lower energy losses, higher switching speeds, and improved thermal stability, making them ideal for EV applications.Growing Investments in Semiconductor R&D

Semiconductor manufacturers are heavily investing in research and development to improve SiC wafer quality, reduce production costs, and enhance device performance.

Restraints

High Cost of SiC Materials and Manufacturing

The complex manufacturing process and limited availability of high-quality SiC wafers result in higher costs compared to traditional silicon-based power devices.Challenges in Large-Scale SiC Production

Expanding SiC wafer production to meet growing demand requires significant investment in fabrication facilities and specialized equipment.Reliability and Design Complexity

Integrating SiC power devices into existing automotive powertrains requires redesigning components and ensuring compatibility with other vehicle systems.

Opportunities

Advancements in SiC Wafer Processing

Innovations in wafer thinning, defect reduction, and epitaxial growth techniques are expected to improve SiC device performance and reduce costs.Expansion of EV Charging Infrastructure

The development of fast-charging networks globally is increasing the demand for SiC power devices, which enhance power conversion efficiency.Strategic Partnerships Among Automakers and Chipmakers

Collaborations between automotive OEMs and semiconductor companies are accelerating the adoption of SiC power devices in next-generation electric vehicles.

Challenges

Competition from Silicon-Based Alternatives

While SiC offers superior efficiency, traditional silicon-based power devices still dominate in cost-sensitive automotive applications.Scalability and Supply Chain Constraints

The limited supply of SiC wafers and dependence on specialized manufacturing processes pose challenges for large-scale production.Need for Standardization and Certification

Establishing industry-wide standards for SiC power devices is crucial to ensuring reliability, safety, and seamless integration into EV systems.

SiC Power Devices for New Energy Vehicles Market News :

U.S. Investment in SiC Semiconductor Manufacturing

Date: December 13, 2024

Overview: The U.S. Commerce Department reached a preliminary agreement with Bosch to provide up to $225 million in subsidies for producing SiC power semiconductors in Roseville, California. This funding supports Bosch’s $1.9 billion investment to transform its manufacturing facility, with production expected to commence in 2026. SiC chips are essential for electric vehicles due to their energy efficiency.

Stellantis and Infineon’s Collaboration on Next-Generation Vehicles

Date: November 7, 2024

Overview: Stellantis and Infineon announced a strategic collaboration to develop power architectures for Stellantis’ next-generation vehicles. This partnership includes the integration of Infineon’s SiC semiconductors, aiming to enhance the performance and efficiency of electric vehicles

China’s Push for Domestic SiC Chip Production

Date: January 2025

Overview: China is increasing the use of domestically produced semiconductor chips in electric vehicles, with homegrown chips now comprising around 15% of the total used—a figure expected to grow. This push for self-sufficiency is part of a broader industrial policy to control key technologies.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the CMP Consumable Parts Market

- Overview of the regional outlook of the CMP Consumable Parts Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

What are the key driving factors and opportunities in the SiC Power Devices for New Energy Vehicles market?

The market is driven by the increasing production of electric vehicles, the superior efficiency of SiC power devices, and growing investments in semiconductor R&D. Opportunities include advancements in wafer processing, expansion of EV charging infrastructure, and strategic industry partnerships.

Which region is projected to have the largest market share?

Asia-Pacific is expected to dominate the market due to its strong EV manufacturing base, government incentives for electric mobility, and increasing investments in SiC semiconductor production.

Who are the top players in the global SiC Power Devices for New Energy Vehicles market?

Leading companies include STMicroelectronics, Infineon, Wolfspeed, Rohm, onsemi, BYD Semiconductor, Mitsubishi Electric, Semikron Danfoss, Fuji Electric, and Qorvo (UnitedSiC).

What are the latest technological advancements in the industry?

Recent advancements include high-efficiency SiC MOSFETs, improved SiC module packaging, advanced thermal management solutions, and the development of 800V EV architectures for faster charging.

What is the current size of the global SiC Power Devices for New Energy Vehicles market?

The market was valued at USD 1,952 million in 2023 and is projected to reach USD 6,557.72 million by 2030, growing at a CAGR of 18.90% during the forecast period

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...