MARKET INSIGHTS

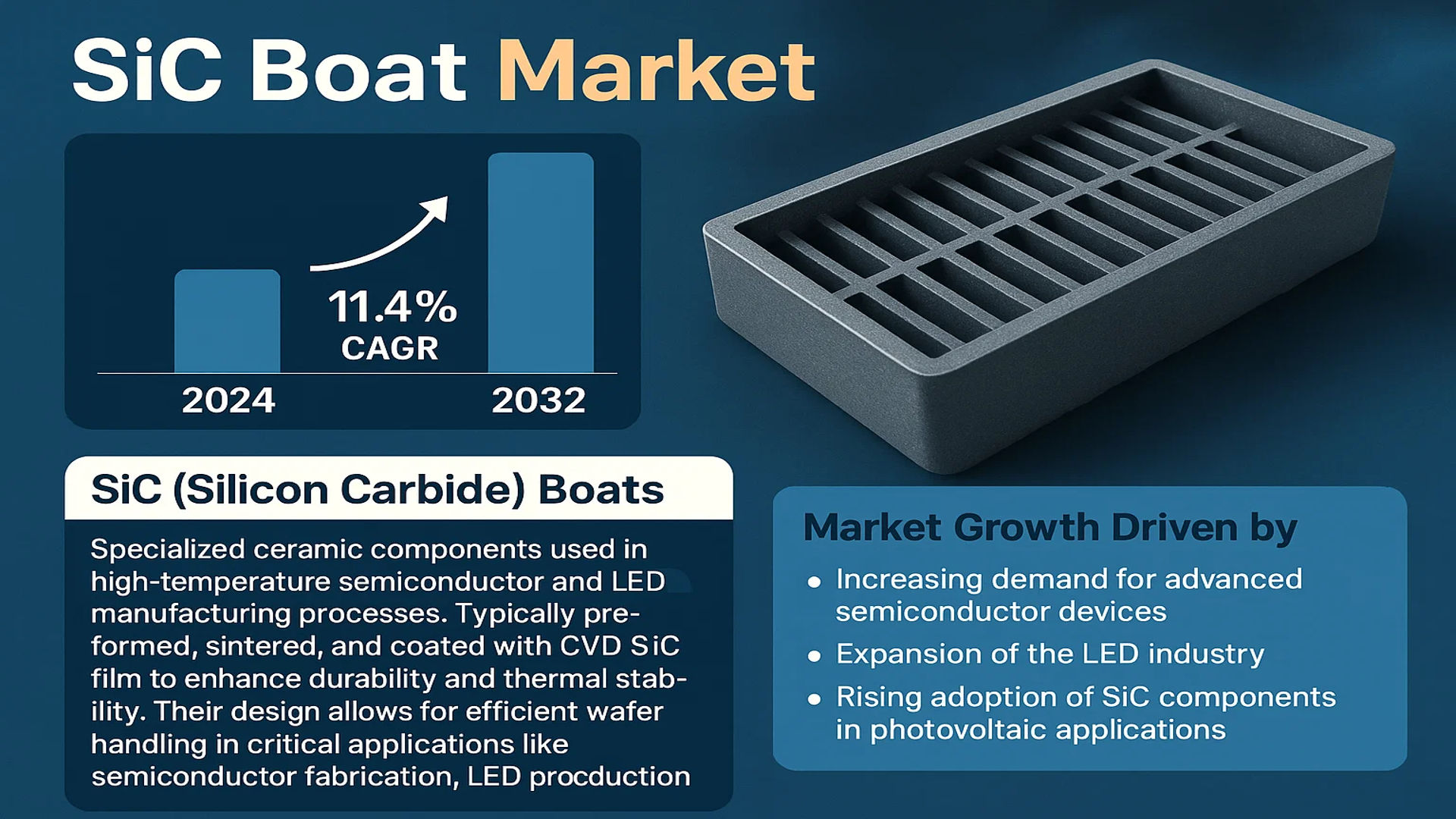

The global SiC Boat Market was valued at 114 million in 2024 and is projected to reach US$ 238 million by 2032, at a CAGR of 11.4% during the forecast period.

SiC (Silicon Carbide) Boats are specialized ceramic components used in high-temperature semiconductor and LED manufacturing processes. These boats are typically preformed, sintered, and coated with a CVD (Chemical Vapor Deposition) SiC film to enhance durability and thermal stability. Their design allows for efficient wafer handling in critical applications like semiconductor fabrication, LED production, and photovoltaic manufacturing.

The market growth is primarily driven by increasing demand for advanced semiconductor devices, expansion of the LED industry, and rising adoption of SiC components in photovoltaic applications. While the semiconductor segment currently dominates demand, the PV sector is showing strong growth potential due to global renewable energy initiatives. Key manufacturers such as Kallex, CoorsTek, and Ferrotec are investing in production capacity expansion to meet this growing demand, particularly in Asia-Pacific regions where semiconductor manufacturing is concentrated.

MARKET DYNAMICS

MARKET DRIVERS

Booming Semiconductor Industry Accelerates Demand for SiC Boats

The global semiconductor industry’s rapid expansion is a fundamental driver for the SiC boat market. With semiconductor sales projected to exceed $700 billion by 2030, manufacturers increasingly require advanced ceramic components like SiC boats for wafer processing. Silicon carbide’s unique properties—including exceptional thermal conductivity, chemical inertness, and mechanical strength—make it indispensable for high-temperature semiconductor fabrication processes. The transition to larger 300mm wafer sizes further amplifies this demand, as SiC boats must maintain structural integrity under extreme conditions while minimizing particulate contamination.

Renewable Energy Push Fuels PV Applications

Global commitments to renewable energy are creating substantial opportunities for SiC boat manufacturers. The photovoltaic sector, projected to install over 400GW of new capacity annually by 2030, relies heavily on silicon carbide components for crystal growth and wafer handling. SiC boats’ ability to withstand repeated thermal cycling in PV manufacturing processes significantly reduces downtime compared to traditional quartz alternatives. Countries implementing aggressive solar initiatives, particularly in Asia-Pacific and North America, are driving this segment’s growth, with China alone accounting for approximately 40% of global PV production capacity.

➤ Recent industry analysis indicates that SiC boat adoption in LED manufacturing has grown by 22% since 2022, driven by demand for more energy-efficient lighting solutions worldwide.

Furthermore, the increasing miniaturization of electronic components has necessitated more precise manufacturing environments, where SiC boats’ dimensional stability provides critical advantages in maintaining process consistency across production batches.

MARKET RESTRAINTS

High Production Costs Limit Market Penetration

While SiC boats offer superior performance characteristics, their manufacturing complexity presents a significant market restraint. The specialized CVD coating process alone can account for 35-45% of total production costs, creating pricing pressures in cost-sensitive markets. Small and medium-sized manufacturers often face challenging ROI calculations when considering SiC boat adoption, particularly when competing with lower-cost alternatives like graphite or quartz components. This cost barrier is most pronounced in developing regions where manufacturing budgets are tightly constrained.

Other Critical Restraints

Fragile Nature During Handling

Despite their high-temperature durability, SiC boats remain brittle at room temperature, leading to handling challenges. Industry studies suggest that approximately 15% of operational costs in SiC boat applications stem from careful transportation and installation procedures required to prevent microfractures that compromise performance.

Long Lead Times for Custom Solutions

The specialized nature of SiC boat production results in lead times averaging 12-16 weeks for custom configurations, creating supply chain bottlenecks for manufacturers requiring rapid equipment changes to meet evolving process requirements.

MARKET CHALLENGES

Technical Complexities in Large-Scale Manufacturing

Scaling SiC boat production while maintaining consistent quality presents ongoing challenges for manufacturers. The sintering process requires precise temperature controls within ±5°C across large furnaces—a technical hurdle that becomes magnified as demand increases. Recent industry benchmarks indicate that yield rates for premium-grade SiC boats currently average 65-75%, with rejections primarily occurring during final inspection due to microscopic defects. This quality variance creates uncertainty for end-users requiring absolute consistency in high-value semiconductor and PV production environments.

Intellectual Property Barriers in Advanced Coatings

Proprietary CVD coating technologies developed by market leaders create barriers to entry for new competitors. The R&D investment required to match the performance characteristics of established players’ coatings—some protected by patents extending through 2030—effectively segments the market. This technological stratification limits customer options while potentially slowing innovation as smaller firms struggle to compete with dominant players’ established solutions.

MARKET OPPORTUNITIES

Emerging Wide Bandgap Semiconductor Technologies Open New Applications

The rapid development of GaN and SiC power electronics represents a significant growth avenue for SiC boat manufacturers. As these next-generation semiconductors require even higher processing temperatures—often exceeding 1600°C—the limitations of traditional materials become apparent. Early adoption metrics suggest that demand for specialized SiC boats in wide bandgap semiconductor fabrication could grow at a 28% CAGR through 2030. This segment’s requirements for ultra-high purity and thermal shock resistance align precisely with advanced SiC boat capabilities.

Advanced Manufacturing Technologies Enable Performance Breakthroughs

Innovations in additive manufacturing and AI-driven process control are revolutionizing SiC boat production. Recent trials indicate that 3D-printed SiC boat prototypes demonstrate 40% better thermal stress resistance compared to conventional manufacturing methods, while reducing material waste by up to 60%. As these technologies mature, they promise to address current challenges around production costs and lead times while enabling design innovations that were previously impossible with traditional fabrication techniques.

SIC BOAT MARKET TRENDS

Rising Demand from Semiconductor Industry Fuels Growth in SiC Boat Market

The global SiC (Silicon Carbide) boat market, valued at $114 million in 2024, is witnessing significant growth, primarily driven by the expanding semiconductor industry. Silicon carbide boats are critical components used in high-temperature processing environments, such as wafer manufacturing and epitaxial growth, due to their superior thermal and chemical stability. With an expected CAGR of 11.4%, the market is projected to reach $238 million by 2032, with Asia-Pacific leading in consumption due to rapid semiconductor fabrication expansions in China, South Korea, and Taiwan.

Other Trends

Technological Advancements in Material and Manufacturing Processes

The demand for high-precision SiC boats has intensified with the increasing complexity of semiconductor devices. Manufacturers are investing in CVD (Chemical Vapor Deposition) coating enhancements to improve durability and reduce contamination risks during high-temperature use. Vertical integration strategies, where companies streamline production from raw material sourcing to finishing, have contributed to better cost efficiency and product reliability. Horizontal SiC boats, expected to experience strong growth, are particularly favored in large-scale semiconductor manufacturing due to their ease of assembly and robustness.

Expansion into LED and Photovoltaic Applications

The LED and photovoltaic (PV) sectors are emerging as key adopters of SiC boats, driven by the need for high-temperature resistant components in crystal growth processes. Compared to traditional quartz or graphite alternatives, SiC boats offer superior performance in MOCVD (Metal-Organic Chemical Vapor Deposition) applications. Additionally, growing investments in renewable energy technologies have spurred demand for efficient, long-lasting components, further propelling SiC boat adoption. While semiconductors retain over 60% market share, the LED segment is anticipated to grow rapidly due to its expanding use in smart lighting and display technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Manufacturers Focus on Technological Advancements to Gain Market Share

The global SiC boat market exhibits a fragmented competitive landscape with established ceramic manufacturers competing alongside specialized semiconductor component suppliers. CoorsTek emerges as a dominant player owing to its extensive expertise in advanced ceramics and global manufacturing footprint across North America, Europe, and Asia-Pacific. The company’s continuous innovation in high-performance ceramic solutions positions it favorably in the growing semiconductor and LED markets.

Ferrotec Taiwan Co and Kallex have secured significant market positions through their focus on customized SiC boat solutions and strong relationships with semiconductor fabrication plants. These companies benefit from their ability to meet stringent purity requirements while maintaining cost competitiveness in the price-sensitive Asian markets.

The competitive intensity is further heightened by Chinese manufacturers like FCT(Tangshan) and Xi’an Zhongwei New Materials, who are rapidly expanding their production capacities. While these domestic players currently focus on serving local demand, their improving technological capabilities pose a growing challenge to established international suppliers.

Market leaders are actively pursuing several strategic initiatives to maintain their positions. Product portfolio expansion, particularly for large-diameter boats used in next-generation semiconductor manufacturing, remains a key focus area. Many competitors are also investing in proprietary coating technologies to enhance the thermal and chemical resistance properties of their SiC boats.

List of Key SiC Boat Manufacturers Profiled

- CoorsTek (U.S.)

- Kallex (Japan)

- 3X Ceramic Parts (Germany)

- Ferrotec Taiwan Co (Taiwan)

- FCT(Tangshan) (China)

- Xi’an Zhongwei New Materials (China)

- Zhejiang Dongxin New Material (China)

- Shandong Huamei New Material (China)

Segment Analysis:

By Type

Horizontal Segment Leads Due to High Adoption in Semiconductor Manufacturing

The market is segmented based on type into:

- Horizontal

- Subtypes: Standard horizontal, Customized horizontal

- Vertical

By Application

Semiconductor Segment Dominates Owing to Widespread Use in Wafer Processing

The market is segmented based on application into:

- Semiconductor

- LED

- PV

By Material Grade

High-Purity SiC Boats Gain Traction in Critical Industrial Applications

The market is segmented based on material grade into:

- Standard grade

- High purity grade

- Ultra high purity grade

By End-Use Industry

Electronics Manufacturing Sector Accounts for Significant Market Share

The market is segmented based on end-use industry into:

- Electronics

- Energy

- Research & Development

- Aerospace & Defense

Regional Analysis: SiC Boat Market

Asia-Pacific

The Asia-Pacific region dominates the global SiC boat market, driven by China’s strong semiconductor manufacturing sector and rapid expansion of LED and photovoltaic industries. China alone accounts for over 40% of global semiconductor production capacity, creating substantial demand for high-performance SiC boats used in crystal growth and wafer processing. Major manufacturers such as Xi’an Zhongwei New Materials and Zhejiang Dongxin New Material have expanded production capacities to meet domestic and international demand. While Japan and South Korea maintain advanced technological capabilities in semiconductor equipment, cost competitiveness favors Chinese suppliers. Challenges include fluctuating raw material costs and the need for precision engineering in next-generation applications.

North America

The U.S. market is characterized by high-value semiconductor production and innovation in compound semiconductors, particularly silicon carbide (SiC) for electric vehicle power electronics. Major fabs and research institutions prioritize thermal stability and purity, driving demand for premium SiC boats. Key players like CoorsTek and Kallex focus on R&D partnerships with semiconductor equipment makers to enhance product longevity and deposition uniformity. While the market is smaller in volume compared to Asia-Pacific, per-unit pricing remains higher due to stringent quality requirements. Government initiatives like the CHIPS Act are expected to bolster domestic semiconductor manufacturing, indirectly supporting the SiC boat market.

Europe

European demand stems from niche applications in aerospace, automotive sensors, and renewable energy systems, where SiC boats enable high-temperature processing of advanced materials. Germany and France lead in adopting vertical integration strategies, with manufacturers collaborating with CVD equipment suppliers to optimize boat designs. Environmental regulations on chemical usage in semiconductor processes influence material selection, favoring suppliers compliant with REACH standards. However, limited local semiconductor fab capacity compared to Asia restrains market growth, pushing European players toward specialized high-margin segments.

South America

The region presents nascent opportunities as Brazil and Argentina develop local electronics manufacturing capabilities. Most SiC boat demand is met through imports, primarily from China and the U.S., due to limited domestic production infrastructure. Economic instability and currency fluctuations hinder long-term investments in semiconductor materials, though photovoltaic applications show gradual uptake. Local suppliers focus on servicing maintenance, repair, and operations (MRO) needs rather than volume production.

Middle East & Africa

This emerging market is constrained by minimal semiconductor fabrication activity but shows potential in PV manufacturing clusters in the UAE and Saudi Arabia. Investments in renewable energy infrastructure could drive demand for SiC boats in solar cell production lines. Currently, the market relies entirely on imports, with logistical challenges and limited technical expertise slowing adoption. Long-term growth depends on regional industrial diversification policies and partnerships with Asian or European technology providers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional SiC Boat markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global SiC Boat market was valued at USD 114 million in 2024 and is projected to reach USD 238 million by 2032, at a CAGR of 11.4% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Horizontal, Vertical), application (Semiconductor, LED, PV), and end-user industry to identify high-growth segments and investment opportunities. The Horizontal segment is expected to dominate the market, with significant growth in semiconductor applications.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy, Russia), Asia-Pacific (China, Japan, South Korea, India), Latin America, and the Middle East & Africa. China and the U.S. are key markets driving demand.

- Competitive Landscape: Profiles of leading market participants, including Kallex, 3X Ceramic Parts, CoorsTek, Ferrotec Taiwan Co, FCT(Tangshan), Xi’an Zhongwei New Materials, Zhejiang Dongxin New Material, and Shandong Huamei New Material, among others. The top five players accounted for a significant market share in 2024.

- Technology Trends & Innovation: Assessment of emerging fabrication techniques, CVD coating advancements, and material innovations enhancing the performance and durability of SiC boats in high-temperature semiconductor applications.

- Market Drivers & Restraints: Evaluation of factors such as the growing semiconductor industry, demand for energy-efficient LED and PV applications, and challenges like high manufacturing costs and supply chain complexities.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the SiC Boat market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SiC Boat Market?

-> SiC Boat Market was valued at 114 million in 2024 and is projected to reach US$ 238 million by 2032, at a CAGR of 11.4% during the forecast period.

Which key companies operate in Global SiC Boat Market?

-> Key players include Kallex, 3X Ceramic Parts, CoorsTek, Ferrotec Taiwan Co, FCT(Tangshan), Xi’an Zhongwei New Materials, Zhejiang Dongxin New Material, and Shandong Huamei New Material, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand in semiconductor manufacturing, expansion of LED and PV industries, and technological advancements in SiC material applications.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing region, driven by semiconductor production in China, Japan, and South Korea, while North America remains a significant market.

What are the emerging trends?

-> Emerging trends include development of high-purity SiC boats, integration of advanced CVD coating technologies, and increasing adoption in next-generation semiconductor fabrication.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...