MARKET INSIGHTS

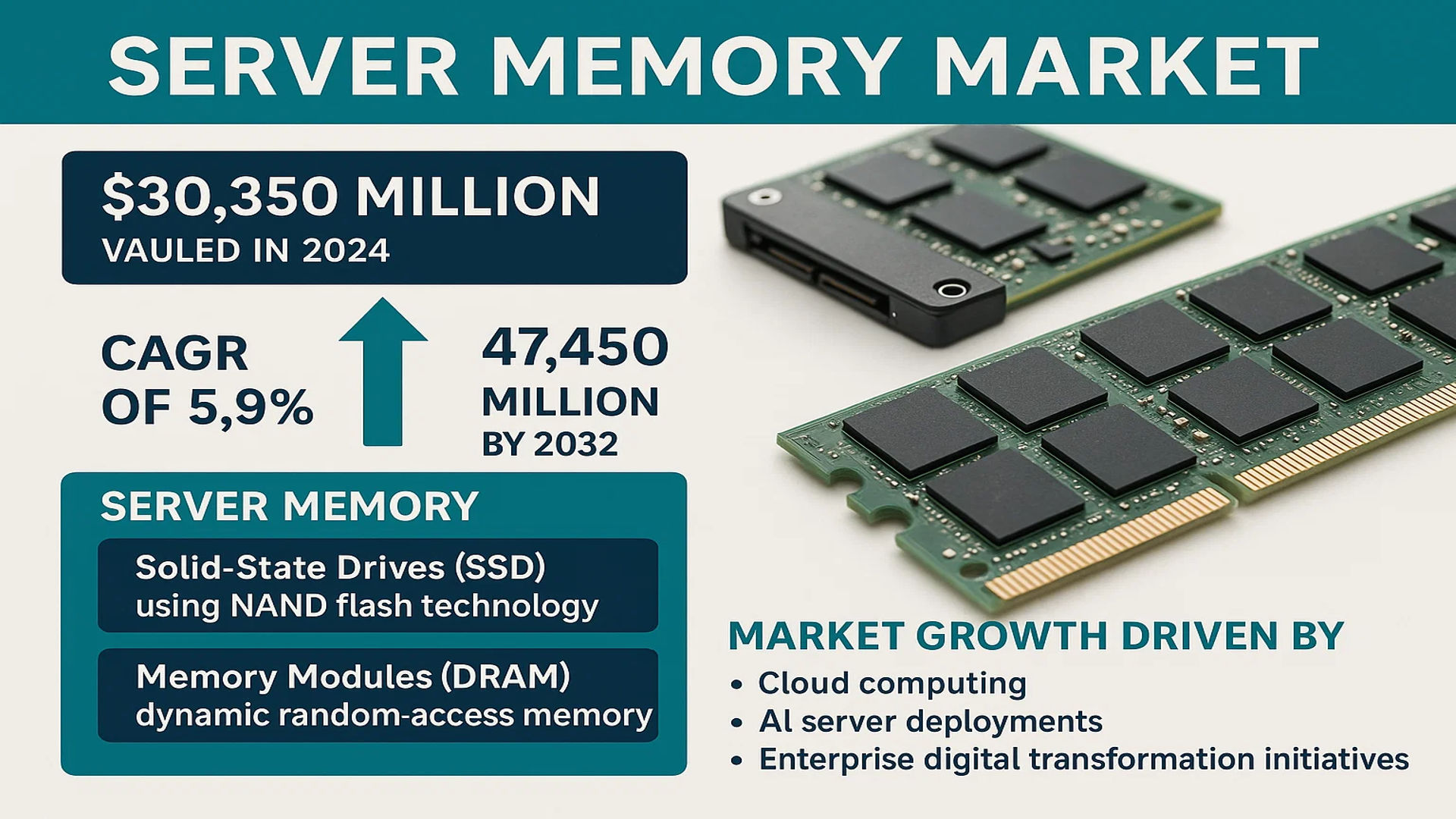

The global Server Memory Market was valued at 30350 million in 2024 and is projected to reach US$ 47450 million by 2032, at a CAGR of 5.9% during the forecast period.

Server memory comprises critical components that enable high-performance computing in data centers and enterprise IT environments. The market primarily includes Solid-State Drives (SSD) using NAND flash technology and Memory Modules (DRAM). SSDs provide non-volatile storage with superior speed and reliability compared to traditional HDDs, while DRAM modules facilitate rapid data processing through dynamic random-access memory technology.

The market growth is driven by escalating demand for cloud computing, AI server deployments, and enterprise digital transformation initiatives. Recent technological advancements like DDR5 memory, PCIe Gen5 interfaces, and 3D NAND architectures are reshaping performance benchmarks. Key players including Samsung, SK Hynix, and Micron Technology dominate the competitive landscape, collectively holding over 60% market share through continuous innovation in memory density and power efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Data Growth Fueling Demand for High-Performance Server Memory

The global datasphere is projected to grow from 64 zettabytes in 2020 to over 180 zettabytes by 2025, creating unprecedented demand for server memory solutions. This data explosion, driven by IoT deployments, 5G networks, and AI applications, requires memory systems that can process and store vast amounts of information with minimal latency. Enterprise SSDs alone are expected to account for over 35% of total SSD shipments by 2025 as data centers upgrade their infrastructure. The shift towards memory-intensive workloads in cloud computing and virtualization is particularly accelerating adoption of high-capacity DDR5 modules and NVMe SSDs in server environments.

AI and Machine Learning Workloads Driving Memory Innovation

The artificial intelligence server market, which grew at over 35% CAGR between 2020-2024, is fundamentally changing memory requirements for data centers. Training complex neural networks requires server memory solutions with bandwidth exceeding 500GB/s and capacities over 1TB per system. This has led to rapid adoption of High Bandwidth Memory (HBM) and computational storage solutions. Leading cloud providers are now deploying servers with specialized memory configurations optimized for AI, with some systems incorporating up to 32TB of DRAM alongside GPU-accelerated memory architectures.

Cloud Computing Expansion Creating Sustained Demand

Public cloud services spending is forecast to grow at nearly 22% annually through 2026, driving continuous investment in hyperscale data center infrastructure. Each new generation of cloud servers requires more advanced memory solutions, with current deployments frequently using 256GB DDR4 modules and 15.36TB SSDs as standard configurations. Memory now accounts for over 25% of total server BOM costs in cloud environments, up from just 15% five years ago. The transition to memory-dense architectures like CXL (Compute Express Link) is further expanding opportunities for high-performance server memory solutions.

MARKET RESTRAINTS

Memory Pricing Volatility Creating Cost Pressures

The server memory market experiences cyclical price fluctuations that can impact adoption rates. DRAM prices declined nearly 40% year-over-year in 2023 before stabilizing, creating challenging conditions for memory manufacturers. While beneficial to buyers in the short term, such volatility makes long-term capacity planning difficult for both suppliers and customers. Enterprise SSD prices also remain approximately 2-3 times higher per gigabyte than HDDs, limiting broader adoption in budget-constrained environments despite their performance advantages.

Complex Supply Chains and Geopolitical Factors Impacting Availability

The concentrated nature of memory production – with over 85% of DRAM and NAND flash manufactured in just three countries – creates supply chain vulnerabilities. Trade restrictions and regional conflicts have periodically disrupted memory shipments, causing allocation shortages. In 2022, supply chain constraints led to lead times exceeding 30 weeks for some enterprise SSD models, forcing server OEMs to revise product roadmaps. The capital-intensive nature of memory fabrication, requiring investments exceeding $15 billion per fab, further complicates supply-demand balancing.

MARKET CHALLENGES

Thermal and Power Constraints in High-Density Memory Systems

As memory densities increase, power consumption and thermal management become critical challenges. A fully-populated 8-channel DDR5 server can consume over 500W just for memory subsystems, approaching the thermal limits of standard 1U server designs. New cooling solutions such as liquid immersion and direct-to-chip cooling add significant cost and complexity to server deployments. Memory reliability also becomes challenging at higher temperatures, with error rates increasing exponentially above 85°C, necessitating advanced ECC and error mitigation technologies.

Security Vulnerabilities in Modern Memory Architectures

Memory-related security threats like Rowhammer attacks and cold boot vulnerabilities continue to evolve, requiring ongoing countermeasures. The complexity of modern memory systems, often combining DRAM, NAND flash, and emerging persistent memory technologies, creates multiple potential attack surfaces. Encryption implementations for data-at-rest in SSDs and data-in-use in DRAM add latency and reduce effective bandwidth, forcing difficult tradeoffs between security and performance in enterprise environments.

MARKET OPPORTUNITIES

CXL and Memory Pooling Creating New Architectural Possibilities

The Compute Express Link (CXL) standard is enabling revolutionary memory architectures where capacity can be dynamically allocated across multiple processors and accelerators. Early CXL-based memory pooling implementations are showing 30-40% better utilization compared to traditional fixed-memory configurations. This technology allows data centers to implement true disaggregated memory architectures, potentially reducing total memory requirements while improving performance for memory-intensive workloads.

Emerging Memory Technologies Opening New Markets

Next-generation memory technologies like MRAM, ReRAM, and phase-change memory are reaching commercialization stages suitable for specialized server applications. These non-volatile memory solutions offer persistence characteristics combined with near-DRAM performance, enabling new types of memory hierarchies. Persistent Memory Modules (PMEM), already being deployed in cloud databases and analytics platforms, demonstrate hybrid memory’s potential to reduce storage bottlenecks while maintaining data durability.

SERVER MEMORY MARKET TRENDS

Growing Adoption of DDR5 and High-Performance SSDs in Data Centers

The server memory market is experiencing a significant shift toward DDR5 and high-performance SSDs, driven by escalating demand from hyperscale data centers and cloud computing providers. DDR5 technology, which offers double the bandwidth and improved power efficiency compared to DDR4, is becoming a critical enabler for AI, machine learning, and high-performance computing applications. The SSD segment is also witnessing rapid advancements, with NVMe-based drives delivering up to 7,000 MB/s read speeds, reducing latency and improving data center operational efficiency. This transition is supported by the increasing deployment of 5G networks and edge computing, which require faster, more reliable memory solutions to handle massive data workloads.

Other Trends

Rising Demand in AI and Hyperscale Data Centers

The explosive growth in AI and hyperscale computing is fueling demand for high-capacity, low-latency memory solutions. With AI server shipments projected to grow at a compound annual growth rate (CAGR) of over 25% between 2024 and 2030, server memory manufacturers are focusing on high-bandwidth solutions such as HBM (High Bandwidth Memory) and DRAM modules optimized for AI training and inference workloads. Additionally, the expansion of cloud service providers like AWS, Microsoft Azure, and Google Cloud is accelerating investment in next-generation memory technologies to enhance data center efficiency and scalability.

Focus on Energy-Efficient and Sustainable Memory Solutions

Sustainability is becoming a key driver in the server memory market, with enterprises prioritizing energy-efficient solutions to meet corporate ESG (Environmental, Social, and Governance) goals. Energy-optimized DRAM modules and SSDs with advanced power management features are gaining traction, particularly in Europe and North America, where data center operators face stringent carbon footprint regulations. Furthermore, innovations like 3D NAND flash technology enable higher storage densities with lower energy consumption, aligning with the industry’s push for greener IT infrastructure. This trend is further reinforced by increasing investments in renewable energy-powered data centers, which require memory components that minimize power consumption without compromising performance.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Scalability to Meet Data Center Demands

The global server memory market exhibits a highly dynamic competitive structure, dominated by established semiconductor giants while witnessing increased participation from emerging regional players. Samsung Electronics continues to lead the industry, holding approximately 30% of the DRAM market share in 2024 according to industry analyses. The company’s dominance stems from its vertically integrated supply chain and continuous advancements in DDR5 server memory technology.

SK Hynix and Micron Technology collectively account for nearly 50% of server memory shipments globally, leveraging their expertise in high-performance computing solutions. These manufacturers are aggressively investing in next-gen technologies like CXL (Compute Express Link) memory and 3D-stacked DRAM to address AI server requirements. Meanwhile, Kioxia and Western Digital maintain strong positions in the enterprise SSD segment, particularly with their PCIe Gen5 offerings that deliver 14GB/s throughput.

Chinese competitors such as Changxin Memory Technologies (CXMT) are rapidly expanding their production capacity, supported by government initiatives to localize semiconductor supply chains. The company recently announced plans to mass-produce DDR5 modules for the domestic server market by late 2024, challenging the entrenched leadership of Korean and American manufacturers.

Specialist providers including SMART Modular Technologies and Innodisk are carving out niches in ruggedized and industrial server memory solutions. These companies differentiate through customization capabilities and extended product lifecycles, catering to aerospace, defense, and telecom infrastructure applications where reliability outweighs pure performance metrics.

List of Key Server Memory Manufacturers Profiled

- Samsung Electronics (South Korea)

- SK Hynix (South Korea)

- Micron Technology (U.S.)

- Kioxia Corporation (Japan)

- Western Digital (U.S.)

- Changxin Memory Technologies (China)

- Kingston Technology (U.S.)

- SMART Modular Technologies (U.S.)

- ADATA Technology (Taiwan)

- Rambus (U.S.)

- Kimtigo (China)

- Transcend (Taiwan)

- Innodisk (Taiwan)

Segment Analysis:

By Type

Solid-State Drive (SSD) Segment Gains Momentum Due to High-Speed Data Processing in Modern Data Centers

The market is segmented based on type into:

- Solid-State Drive (SSD)

- Subtypes: SATA SSD, SAS SSD, NVMe SSD

- Memory Modules

- Subtypes: DDR4, DDR5, LPDDR, NVDIMM

By Application

AI Server Segment Shows Strong Growth Potential Fueled by Increasing AI Workloads

The market is segmented based on application into:

- AI Server

- General Purpose Server

- Cloud Computing Infrastructure

- High Performance Computing

- Others

By Technology

DDR5 Technology Emerges as Key Growth Driver for Next-Generation Server Infrastructure

The market is segmented based on technology into:

- DRAM

- NAND Flash

- 3D XPoint

- Others

By Capacity

High-Capacity Modules in Demand for Enterprise Data Center Applications

The market is segmented based on capacity into:

- Below 512GB

- 512GB-1TB

- 1TB-2TB

- Above 2TB

Regional Analysis: Server Memory Market

Asia-Pacific

The Asia-Pacific region dominates the global server memory market, accounting for the largest revenue share in 2024, primarily driven by China, Japan, and South Korea. The region benefits from robust semiconductor manufacturing ecosystems, with key players like Samsung, SK Hynix, and Kioxia headquartered here. China’s aggressive data center expansion and government-backed semiconductor self-sufficiency initiatives are accelerating demand. Artificial intelligence (AI) server deployment across enterprises and hyperscalers is fueling high-bandwidth memory (HBM) and DDR5 adoption. However, geopolitical tensions and export controls on advanced memory technologies create supply chain uncertainties in certain markets.

North America

North America represents the most technologically advanced server memory market, characterized by early adoption of DDR5, PCIe Gen5 SSDs, and CXL-based memory solutions. The U.S. hosts major cloud service providers and hyperscale data centers that drive innovation in storage-class memory and high-endurance SSDs. Domestic manufacturers like Micron and Western Digital collaborate closely with server OEMs to optimize memory architectures for AI/ML workloads. Regulatory pressures for data sovereignty and security are prompting localized memory supply chains, while the CHIPS Act investments strengthen domestic production capabilities in advanced memory technologies.

Europe

Europe’s server memory market is shaped by stringent data protection regulations and sustainability directives that influence memory product specifications. The region shows increasing preference for energy-efficient DDR5 modules and low-power SSDs compliant with EU energy standards. Automotive and industrial server applications drive demand for ruggedized memory solutions with extended temperature ranges. While Europe lacks major memory manufacturers, it maintains strong design expertise through companies like Infineon and STMicroelectronics. The market faces challenges from higher costs of compliant memory solutions compared to global alternatives.

South America

South America’s server memory market is emerging, with Brazil and Argentina showing moderate growth in data center infrastructure. Price sensitivity leads to higher adoption of legacy DDR4 memory and SATA SSDs rather than cutting-edge technologies. Limited local manufacturing results in reliance on imports, creating supply chain vulnerabilities. However, increasing digital transformation initiatives in banking and telecommunications sectors are driving gradual modernization of server memory infrastructures. The region presents opportunities for value-oriented memory providers as cloud service providers expand their regional footprints.

Middle East & Africa

The MEA server memory market is in early growth stages, with Gulf Cooperation Council countries leading in data center investments. Government-led smart city projects and financial sector modernization create demand for reliable server memory solutions. The region shows preference for high-temperature tolerant memory products suitable for harsh environments. While adoption of advanced memory technologies lags behind other regions, increasing hyperscale data center deployments suggest future growth potential. Challenges include limited technical expertise in memory subsystem optimization and dependence on international suppliers for high-performance solutions.

Report Scope

This market research report provides a comprehensive analysis of the Global Server Memory Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Server Memory market was valued at USD 30,350 million in 2024 and is projected to reach USD 47,450 million by 2032, growing at a CAGR of 5.9% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Solid-State Drives (SSD) and Memory Modules (DRAM)), application (AI Servers and General Purpose Servers), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific is the fastest-growing region, driven by increasing data center investments.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Samsung, SK Hynix, Micron Technology, Kioxia, and Western Digital (WD).

- Technology Trends & Innovation: Assessment of emerging technologies, including advancements in DDR technology, NAND flash memory, persistent memory solutions, and energy-efficient designs for data centers.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as increasing demand for cloud computing and AI applications, along with challenges like supply chain constraints and semiconductor shortages.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the server memory market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Server Memory Market?

->Server Memory Market was valued at 30350 million in 2024 and is projected to reach US$ 47450 million by 2032, at a CAGR of 5.9% during the forecast period.

Which key companies operate in Global Server Memory Market?

-> Key players include Samsung, SK Hynix, Micron Technology, Kioxia, Western Digital (WD), Changxin Memory Technologies (CXMT), and Kingston Technology Company, Inc., among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for cloud computing, expansion of data centers, increasing AI server deployments, and advancements in memory technology.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by significant data center investments in China, Japan, and South Korea, while North America maintains a strong market position.

What are the emerging trends?

-> Emerging trends include higher capacity DDR5 adoption, PCIe 5.0 SSDs, persistent memory solutions, and energy-efficient memory designs for sustainable data centers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...