MARKET INSIGHTS

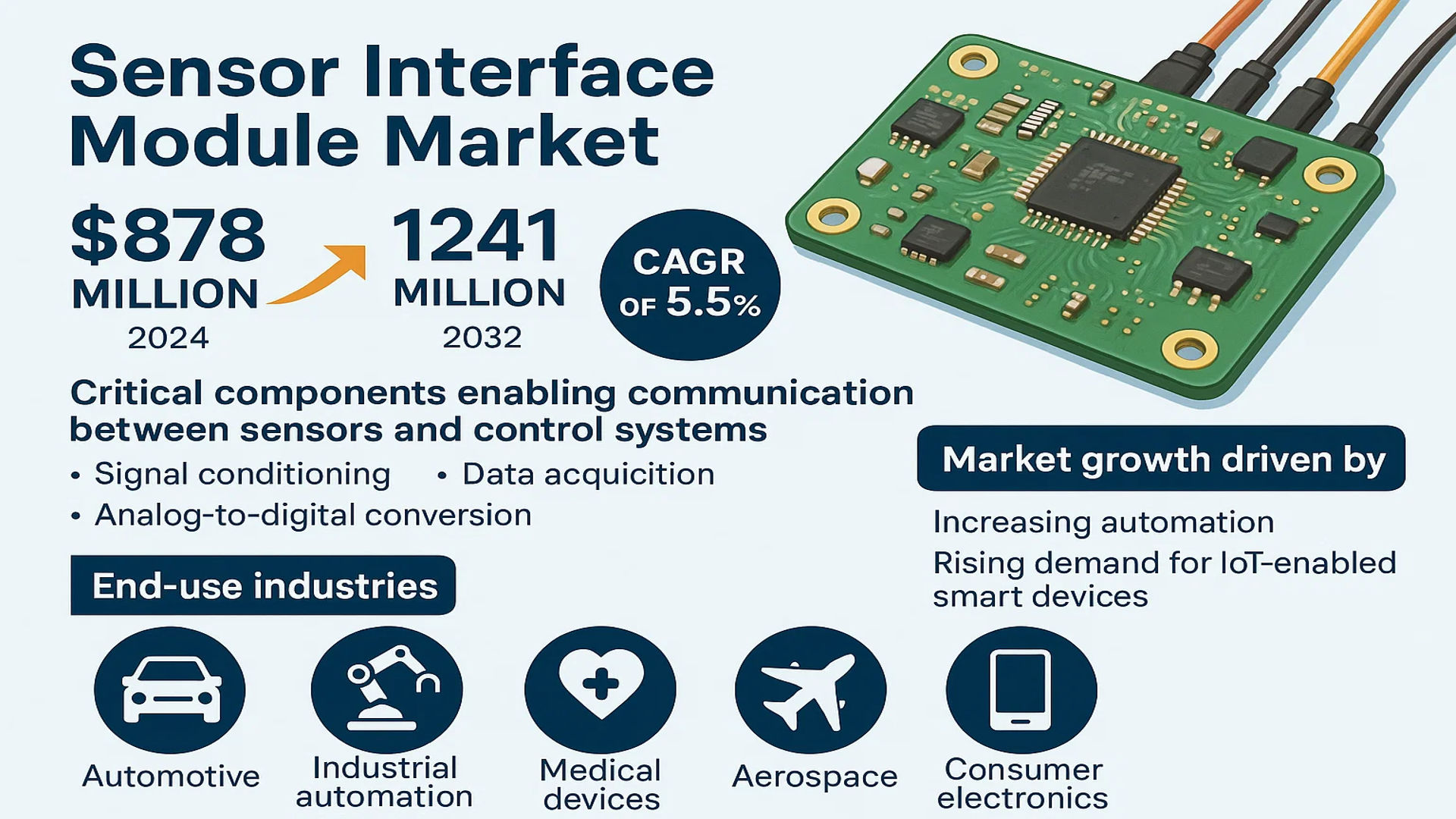

The global Sensor Interface Module market was valued at 878 million in 2024 and is projected to reach US$ 1241 million by 2032, at a CAGR of 5.5% during the forecast period.

Sensor Interface Modules are critical components that enable seamless communication between sensors and control systems. These modules perform essential functions such as signal conditioning, data acquisition, and analog-to-digital conversion, allowing real-time monitoring of environmental and device parameters. They are widely utilized across diverse industries including automotive, industrial automation, medical devices, aerospace, and consumer electronics.

The market growth is driven by increasing automation across industries and the rising demand for IoT-enabled smart devices. However, challenges such as high development costs and compatibility issues with legacy systems may restrain market expansion. Key players like Bosch, Siemens, and Pepperl+Fuchs are investing in advanced interface solutions to capitalize on emerging opportunities in Industry 4.0 and smart manufacturing applications.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation to Fuel Sensor Interface Module Adoption

The rapid growth of Industry 4.0 and smart manufacturing is significantly driving demand for sensor interface modules globally. These components serve as critical bridges between sensors and control systems in automated production lines, enabling real-time data acquisition and process optimization. The industrial automation market has shown consistent annual growth rates above 8% in recent years, necessitating more sophisticated sensor interfacing solutions. Modern manufacturing facilities increasingly rely on distributed sensor networks for predictive maintenance and quality control, creating sustained demand for reliable interface modules with high sampling rates and noise immunity.

Advances in Automotive Electronics to Accelerate Market Penetration

The automotive sector’s transition toward electric and autonomous vehicles represents a major growth opportunity for sensor interface modules. Modern vehicles now incorporate over 100 sensors for various functions including advanced driver assistance systems (ADAS), battery management, and emissions control. The automotive sensor market is projected to exceed $40 billion by 2026, creating complementary demand for high-performance interface solutions. Vehicle electrification trends particularly favor modules with capabilities for current monitoring and thermal sensing, with major OEMs increasingly specifying integrated interface solutions to reduce wiring complexity and improve reliability.

➤ A recent industry analysis indicates that autonomous vehicle platforms require 3-5 times more sensor interfaces compared to conventional vehicles, creating substantial growth potential for module manufacturers.

Healthcare Digitization to Expand Medical Applications

The global healthcare sector’s digital transformation is generating new opportunities for medical-grade sensor interface modules. Patient monitoring equipment, diagnostic devices, and portable medical instruments increasingly incorporate advanced sensing capabilities requiring specialized interfacing solutions. The medical sensors market has consistently grown at 7-9% annually, with particular demand for modules meeting stringent safety and EMC standards. Wireless sensor interfaces capable of reliable operation in clinical environments have emerged as particularly promising segment, enabled by recent developments in low-power embedded designs.

MARKET RESTRAINTS

Interoperability Challenges to Limit Adoption Rates

The absence of universal standards for sensor interfaces creates integration challenges across different system architectures. Many industrial environments utilize sensors from multiple vendors with varying communication protocols, requiring customized interface solutions that increase deployment costs and complexity. This fragmentation particularly affects brownfield installations where legacy equipment must interface with modern control systems, often necessitating costly gateway solutions.

Component Shortages and Supply Chain Constraints to Impact Market Growth

The semiconductor supply chain disruptions that began in 2020 continue to affect sensor interface module production, particularly for designs utilizing advanced mixed-signal ICs. Lead times for certain microcontroller and signal conditioning components have extended to over 40 weeks in some cases, forcing manufacturers to redesign products or accept lower production volumes. These constraints have been particularly challenging for automotive-grade modules requiring qualified components with extended temperature ranges.

Other Constraints

Price Sensitivity in Cost-Driven Applications

Certain market segments like consumer electronics exhibit extreme price sensitivity, limiting the adoption of premium interface solutions. Competition from integrated sensor modules that combine sensing and interfacing functions presents additional pricing pressures for standalone interface products.

MARKET CHALLENGES

Technical Complexity of Next-Generation Designs to Strain Development Resources

Emerging applications demand interface modules with higher channel counts, faster sampling rates, and improved noise performance, significantly increasing design complexity. The need to support multiple sensor types (analog, digital, smart sensors) within single platforms requires sophisticated signal conditioning architectures and advanced power management. Developing these solutions while maintaining competitive pricing and rapid time-to-market presents ongoing challenges for manufacturers.

Other Challenges

Cybersecurity Concerns in Networked Applications

Industrial IoT deployments require interface modules with robust security features to prevent unauthorized access to sensor networks. Implementing effective security protocols without compromising real-time performance remains an ongoing technical and cost challenge.

Regulatory Compliance Across Industries

Modules for medical, automotive, and aerospace applications must meet increasingly stringent regulatory requirements. The certification process for safety-critical applications can add significant time and cost to product development cycles.

MARKET OPPORTUNITIES

AI-Enabled Smart Sensing to Create New Market Segments

The integration of edge computing capabilities into sensor interface modules presents significant growth opportunities. Next-generation designs incorporating basic AI functions for on-board signal processing and analytics are gaining traction in predictive maintenance applications. This evolution requires interface modules with additional computational resources and specialized firmware, creating opportunities for value-added solutions.

Renewable Energy Sector to Drive Specialty Interface Demand

The rapid expansion of solar and wind power generation is creating demand for ruggedized interface modules capable of operating in harsh environments while maintaining precision measurements. Applications such as solar panel monitoring and wind turbine condition monitoring require specialized solutions combining high accuracy with robust environmental protection.

➤ A recent survey of energy sector operators indicates that over 60% plan to upgrade their sensor interface infrastructure within the next three years to support renewable integration.

Emerging Wireless Standards to Enable New Applications

Advancements in low-power wireless technologies are creating opportunities for battery-operated sensor interface modules in building automation, agriculture, and environmental monitoring. Emerging standards specifically designed for industrial sensor networks are reducing power consumption while improving reliability, enabling previously impractical deployment scenarios for wireless sensing solutions.

SENSOR INTERFACE MODULE MARKET TRENDS

Industrial Automation Boost Driving Demand for Sensor Interface Modules

The global sensor interface module market is experiencing significant growth, with a valuation of US$ 878 million in 2024 and an expected reach of US$ 1,241 million by 2032, growing at a CAGR of 5.5%. A key driver behind this expansion is the increasing adoption of automation across industrial sectors. Sensor interface modules play a vital role in optimizing real-time data acquisition and signal conditioning, crucial for automated manufacturing processes. These modules are integral to ensuring seamless communication between sensors and control systems, enhancing operational efficiency in industries such as automotive, aerospace, and electronics. Over 45% of sensor interface modules are currently deployed in industrial automation, with demand projected to grow steadily as smart factories and Industry 4.0 initiatives gain traction.

Other Trends

IoT Integration Enhancing Sensor Connectivity

The proliferation of Internet of Things (IoT)-enabled devices has elevated the importance of advanced sensor interface modules. These modules facilitate secure and efficient data transmission between edge devices and cloud-based platforms, improving predictive maintenance and remote monitoring applications. Industries such as healthcare and consumer electronics are leveraging IoT-integrated sensor modules to enhance connectivity and interoperability. As IoT ecosystems expand, demand for high-performance, low-power sensor interface solutions is expected to rise significantly, particularly in regions where smart infrastructure investments are accelerating.

Shift Toward Miniaturization and Wireless Capabilities

Technological advancements are leading to the development of compact, energy-efficient sensor interface modules with wireless communication capabilities. The demand for lightweight, space-saving solutions in applications like wearable medical devices and automotive sensors is pushing manufacturers to innovate in miniaturization. Companies such as Siemens and Bosch are investing in chip-level integration to reduce power consumption while maintaining high data accuracy. Meanwhile, wireless sensor interface modules, which eliminate wiring complexities, are gaining preference in large-scale industrial and smart city deployments, further fueling market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define the Competitive Dynamics

The global sensor interface module market features a competitive yet fragmented landscape, with established conglomerates coexisting alongside specialized manufacturers. Bosch and Siemens currently dominate market share, leveraging their industrial automation expertise and extensive distribution networks across Europe and North America. These giants benefit from vertical integration—producing sensors, control systems, and interface modules under one roof—which grants them cost and technical advantages.

Meanwhile, mid-sized players like Pepperl+Fuchs and Omega Engineering are carving niches through application-specific solutions. Pepperl+Fuchs, for instance, strengthened its industrial safety-focused interface modules after acquiring a majority stake in ecom instruments GmbH in 2022, demonstrating how targeted acquisitions can bolster market positioning. Similarly, Omega’s 2023 launch of the SI-1000 series with enhanced IoT connectivity shows how product differentiation drives competitiveness.

Regional players also influence market dynamics. Japan’s Kyowa Electronic Instruments maintains stronghold in Asia-Pacific’s research sector, while Germany’s Beckhoff Automation excels in high-speed industrial interfaces. However, Chinese manufacturers like Adlink Technology are rapidly gaining traction by offering cost-competitive alternatives, particularly in emerging markets where price sensitivity is high.

The competitive intensity is further amplified by evolving industry standards. With Industry 4.0 adoption accelerating, companies investing in wireless protocols (like IO-Link Wireless) and edge-computing capabilities—as seen in Siemens’ SIMATIC IMX32-6 module—are outpacing competitors still reliant on legacy wired interfaces. This technological shift is reshaping market hierarchies in real-time.

List of Key Sensor Interface Module Companies Profiled

- Bosch (Germany)

- Siemens (Germany)

- Omega Engineering (U.S.)

- Pepperl+Fuchs (Germany)

- Kyowa Electronic Instruments (Japan)

- Beckhoff Automation (Germany)

- Hydronix (UK)

- Lorenz Messtechnik GmbH (Germany)

- Adlink Technology (Taiwan)

- Encelium Technologies (U.S.)

- Contemporary Control Systems (U.S.)

- Applied Measurements (UK)

Segment Analysis:

By Type

Automatic Type Segment Leads Due to Advanced Signal Processing and Integration Capabilities

The market is segmented based on type into:

- Automatic Type

- Manual Type

By Application

Industrial Automation Segment Dominates Owing to Increasing Adoption in Smart Manufacturing

The market is segmented based on application into:

- Automotives

- Industrial Automation

- Medical Devices

- Electronics and Consumer Products

- Aerospace

- Research and Education

- Others

By Interface Standard

CAN Bus Interface Holds Major Share Due to Its Robustness in Automotive Applications

The market is segmented based on interface standard into:

- I2C

- SPI

- UART

- CAN Bus

- Ethernet

- Others

By Sensor Type

Temperature Sensors Maintain Strong Position Across Multiple Industries

The market is segmented based on sensor type into:

- Temperature Sensors

- Pressure Sensors

- Proximity Sensors

- Motion Sensors

- Optical Sensors

- Others

Regional Analysis: Sensor Interface Module Market

Asia-Pacific

The Asia-Pacific region dominates the global sensor interface module market, accounting for over 38% of global revenue share in 2024. Rapid industrialization and the strong presence of automotive and electronics manufacturing hubs in China, Japan, and South Korea are primary growth drivers. China leads regional demand due to extensive Industry 4.0 adoption, with smart manufacturing investments exceeding $20 billion annually. While cost-sensitive markets still prefer manual interface modules, demand for advanced automatic variants is growing in precision-dependent sectors like semiconductor manufacturing and medical devices. However, intellectual property concerns and fragmented supplier networks create quality control challenges for some buyers.

North America

North America maintains technological leadership in high-end sensor interface solutions, particularly for aerospace and medical applications. Stringent FDA and FAA regulations compel manufacturers to adopt precision modules with advanced signal conditioning capabilities. The U.S. market benefits from strong R&D ecosystems around IoT and Industry 4.0, with companies like TE Connectivity and Texas Instruments driving innovation. A notable trend includes growing integration of AI-powered diagnostic features in interface modules for predictive maintenance. While labor costs impact price competitiveness, the region excels in low-volume, high-complexity applications where reliability outweighs cost considerations.

Europe

European demand emphasizes energy efficiency and interoperability, with strict EU regulations governing electromagnetic compatibility and industrial safety standards. Germany’s Mittelstand manufacturers lead in adopting modular interface solutions for flexible production lines, while Nordic countries show strong uptake in environmental monitoring applications. The region faces challenges from slower industrial growth compared to Asia, but maintains strength in specialized segments like automotive test systems and pharmaceutical manufacturing equipment. Recent developments include increased standardization efforts through IEC and DIN specifications to simplify multi-vendor system integration.

South America

The market remains nascent but shows potential in mining and agricultural automation applications. Brazil accounts for nearly 60% of regional demand, driven by expanding automotive production and oil/gas operations. Economic volatility sometimes delays capital expenditure on automation equipment, leading to preference for refurbished or lower-specification modules. However, growing awareness of predictive maintenance benefits and gradual infrastructure modernization are creating opportunities. Local distributors are increasingly partnering with global suppliers to improve technical support capabilities, addressing a key barrier to adoption in the region.

Middle East & Africa

Growth focuses on oil/gas infrastructure and smart city projects, particularly in GCC countries. The UAE and Saudi Arabia lead investments in industrial automation, with special economic zones offering tax incentives for smart manufacturing setups. While the market remains relatively small, it demonstrates above-average growth rates around 7-9% as operators upgrade legacy systems. Challenges include limited local technical expertise and dependence on imports, though regional offices of major brands like Siemens and Bosch are expanding service networks. Renewable energy projects also present emerging opportunities for specialized environmental sensing applications.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Sensor Interface Module markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Sensor Interface Module market was valued at USD 878 million in 2024 and is projected to reach USD 1,241 million by 2032, growing at a CAGR of 5.5% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Automatic and Manual), application (Automotives, Industrial Automation, Medical Devices, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Encelium, Omega, Bosch, Siemens, and Pepperl Fuchs, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies including AI/IoT integration, advanced signal processing, and miniaturization trends in sensor interface modules.

- Market Drivers & Restraints: Evaluation of factors such as increasing automation across industries, growing demand for smart sensors, and challenges related to standardization and interoperability.

- Stakeholder Analysis: Strategic insights for component manufacturers, system integrators, OEMs, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and secondary data from verified sources to ensure accuracy and reliability of market insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Sensor Interface Module Market?

-> Sensor Interface Module market was valued at 878 million in 2024 and is projected to reach US$ 1241 million by 2032, at a CAGR of 5.5% during the forecast period.

Which key companies operate in Global Sensor Interface Module Market?

-> Key players include Encelium, Omega, Bosch, Siemens, Pepperl Fuchs, Helvar, Lorenz Messtechnik GmbH, and Hydronix, among others.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, rising adoption of IoT devices, and growing demand for smart sensors across multiple industries.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by industrial expansion in China and India, while North America remains a technological leader.

What are the emerging trends?

-> Emerging trends include AI-powered sensor interfaces, wireless sensor networks, and miniaturization of interface modules for compact applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...