Semiconductor Pellicle Market Market Insights

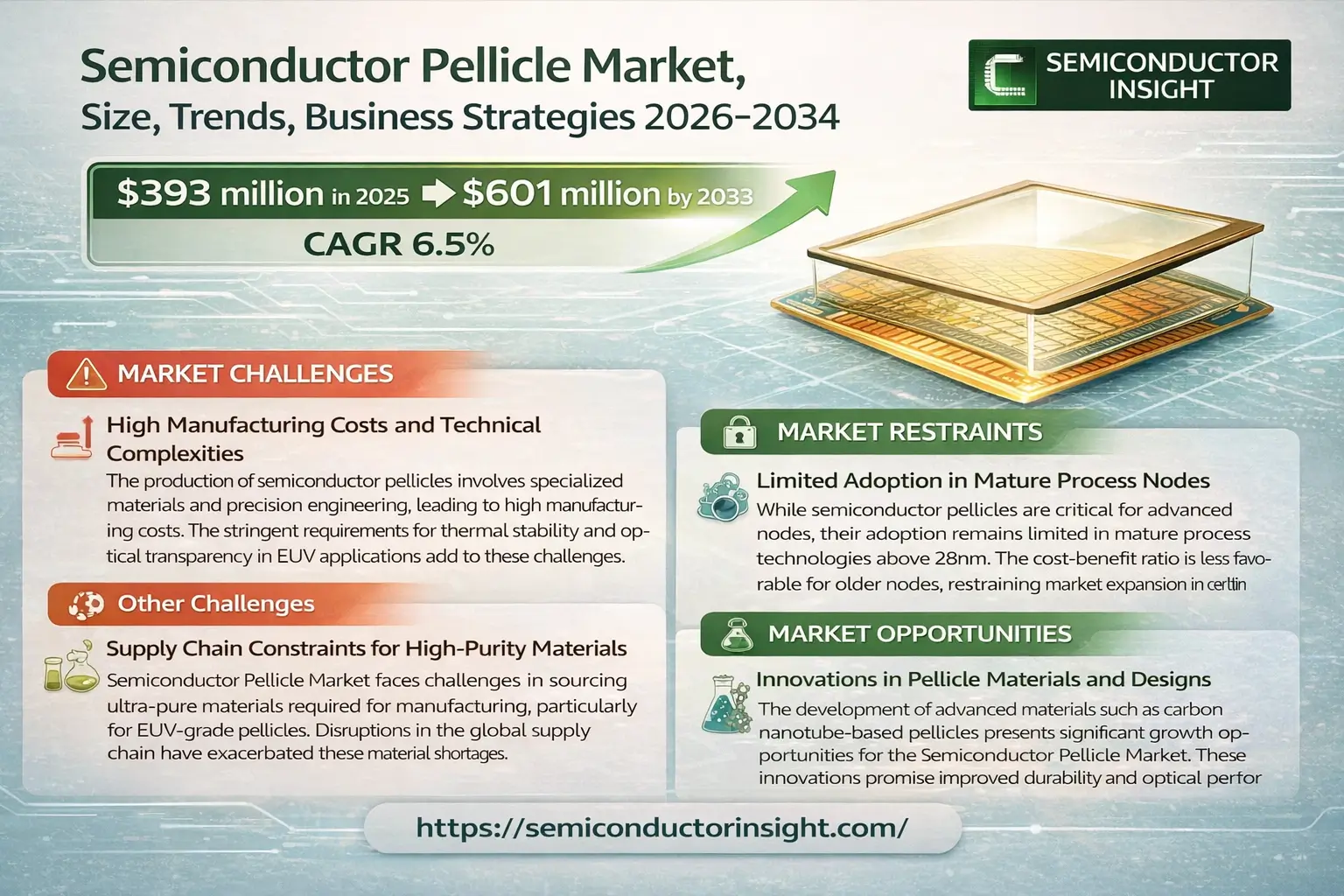

Global Semiconductor Pellicle Market was valued at USD 393 million in 2025 and is projected to reach USD 601 million by 2033, exhibiting a CAGR of 6.5% during the forecast period.

Semiconductor pellicles are thin, transparent films used in photolithography to protect photomasks from contamination during semiconductor manufacturing. These critical components act as a barrier against particles and debris, ensuring high-precision pattern transfer onto silicon wafers. The pellicle’s advanced materials and ultra-thin construction (typically under 1 micrometer) enable minimal light scattering while maintaining durability under extreme conditions.

The market growth is driven by increasing demand for advanced semiconductor nodes (7nm and below), where contamination control becomes more stringent. Furthermore, the transition to extreme ultraviolet (EUV) lithography requires specialized pellicles capable of withstanding higher energy exposure without degradation. Key players like Mitsui Chemicals, Shin-Etsu, and FINE SEMITECH dominate the market, collectively holding nearly 80% revenue share in 2025 through continuous innovation in material science and coating technologies.

Semiconductor Pellicle Market MARKET DRIVERS

Increasing Demand for Advanced Semiconductor Nodes

Semiconductor Pellicle Market is experiencing significant growth due to the rising demand for advanced semiconductor nodes below 10nm. As chipmakers push toward smaller process nodes, the need for defect-free lithography processes has intensified, directly boosting pellicle adoption.

Expansion of EUV Lithography Technology

Extreme Ultraviolet (EUV) lithography adoption has become a key driver for the Semiconductor Pellicle Market, with leading foundries increasingly adopting this technology for high-volume manufacturing. EUV systems require specialized pellicles to maintain mask integrity during exposure.

Additionally, the expansion of 5G infrastructure and AI chip fabrication is further accelerating demand for high-performance semiconductor components that rely on defect-free lithography processes.

Semiconductor Pellicle Market MARKET CHALLENGES

High Manufacturing Costs and Technical Complexities

The production of semiconductor pellicles involves specialized materials and precision engineering, leading to high manufacturing costs. The stringent requirements for thermal stability and optical transparency in EUV applications add to these challenges.

Other Challenges

Supply Chain Constraints for High-Purity Materials

Semiconductor Pellicle Market faces challenges in sourcing ultra-pure materials required for manufacturing, particularly for EUV-grade pellicles. Disruptions in the global supply chain have exacerbated these material shortages.

Semiconductor Pellicle Market MARKET RESTRAINTS

Limited Adoption in Mature Process Nodes

While semiconductor pellicles are critical for advanced nodes, their adoption remains limited in mature process technologies above 28nm. The cost-benefit ratio is less favorable for older nodes, restraining market expansion in certain segments.

Semiconductor Pellicle Market MARKET OPPORTUNITIES

Innovations in Pellicle Materials and Designs

The development of advanced materials such as carbon nanotube-based pellicles presents significant growth opportunities for the Semiconductor Pellicle Market. These innovations promise improved durability and optical performance for next-generation lithography systems.

Semiconductor Pellicle Market Trends

Robust Market Growth Driven by Advanced Semiconductor Nodes

Global Semiconductor Pellicle Market was valued at USD 393 million in 2025 and is projected to reach USD 601 million by 2033, growing at a CAGR of 6.5%. This growth is primarily driven by the increasing complexity of semiconductor manufacturing processes, particularly at 7nm nodes and below. The advancement to extreme ultraviolet lithography (EUVL) technology has significantly elevated demand for specialized pellicles due to their critical role in protecting photomasks from contamination during the lithography process.

Other Trends

Technological Advancements in Pellicle Manufacturing

Leading manufacturers are adopting precise vacuum coating technologies like physical vapor deposition (PVD) and chemical vapor deposition (CVD) to create uniform, defect-free films. The process requires exacting control of temperature, pressure, and gas flow parameters to meet stringent quality standards. As EUV lithography becomes more prevalent, the requirements for pellicle uniformity and defect control have become more rigorous, with pattern sizes shrinking below 50nm in advanced nodes.

Consolidated Competitive Landscape

Semiconductor Pellicle Market is highly concentrated, with the top three companies – Mitsui Chemicals, Shin-Etsu, and FINE SEMITECH – accounting for nearly 80% of global revenue in 2025. These industry leaders continue to invest in R&D to develop next-generation pellicles for emerging lithography technologies, while smaller players focus on niche applications in IC bumping, MEMS, and LED packaging.

Regional Market Dynamics

Asia dominates the Semiconductor Pellicle Market with over 60% share, driven by major semiconductor foundries in South Korea, Taiwan, and China. North America and Europe maintain strong positions in R&D for advanced pellicle technologies, particularly for EUV applications. The market remains sensitive to global supply chain dynamics and trade policies affecting semiconductor manufacturing inputs.

COMPETITIVE LANDSCAPE

Key Industry Players

Oligopolistic Market Dominated by Three Asian Suppliers

Global Semiconductor Pellicle Market exhibits a concentrated competitive landscape, with Mitsui Chemicals, Shin-Etsu, and FINE SEMITECH collectively controlling approximately 80% of market revenue as of 2025. These industry leaders have established strong technological barriers through patented vacuum deposition techniques and strategic partnerships with major foundries. Their dominance is particularly evident in advanced EUV pellicle solutions, where technical requirements for 7nm and below process nodes create high entry barriers.

Smaller players like S&S Tech and INKO have carved out specialized niches in KrF and ArF pellicle segments, catering to mature node applications. Emerging manufacturers from South Korea and China are gradually increasing their market presence, focusing on cost-competitive solutions for mid-tier semiconductor applications. The market remains highly technical, favoring companies with expertise in atomic-level thin film deposition and defect control capabilities.

List of Key Semiconductor Pellicle Companies Profiled

- Mitsui Chemicals

- Shin-Etsu Chemical

- FINE SEMITECH

- Micro Lithography, Inc.

- S&S Tech

- INKO

- NEPCO

- Canatu

- Applied Materials

- Entegris

- Toppan Photomasks

- Photronics

- AGC Inc.

- Zeon Corporation

- Tokyo Ohka Kogyo

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

EUV Pellicle dominates with critical technology advantages:

|

| By Application |

|

IC Foundry represents the most demanding application:

|

| By End User |

|

Foundries drive specialized requirements:

|

| By Technology Node |

|

7nm and below presents unique challenges:

|

| By Deposition Method |

|

CVD Methods gaining prominence:

|

Regional Analysis: Semiconductor Pellicle Market

Asia-Pacific

Taiwan leads in semiconductor pellicle integration with its advanced foundry ecosystem. TSMC’s pellicle requirements drive continuous improvements in durability and transmittance characteristics. Local R&D focuses on solving pellicle-induced imaging errors for sub-5nm nodes.

South Korean manufacturers require specialized pellicle solutions for high-volume memory production. The market sees growing demand for pellicles compatible with extreme patterning techniques used in DRAM and NAND flash manufacturing processes.

Japanese firms contribute advanced pellicle membrane materials and frame technologies. The market benefits from Japan’s expertise in ultra-thin film fabrication and contamination control solutions tailored for EUV lithography applications.

China’s Semiconductor Pellicle Market grows as domestic foundries scale up production. Local manufacturers are developing pellicle solutions to reduce import dependency, though still facing challenges in EUV pellicle technology adoption.

North America

North America maintains strong Semiconductor Pellicle Market presence through equipment leadership and R&D centers. The region hosts key pellicle technology developers and benefits from close collaborations between foundries and material scientists. US-based semiconductor manufacturers emphasize pellicle performance optimization for advanced packaging applications. The market sees increased investment in pellicle solutions for both EUV and multi-patterning applications, with research institutions exploring next-generation membrane materials.

Europe

Europe’s Semiconductor Pellicle Market shows steady growth supported by automotive and industrial semiconductor demand. The region’s strength lies in specialty IC manufacturing requiring customized pellicle solutions. ASML’s EUV technology development in the Netherlands influences pellicle specifications for global markets. European research initiatives focus on improving pellicle lifetime and thermal stability characteristics for high-volume manufacturing environments.

Middle East & Africa

The Middle East shows emerging interest in semiconductor pellicle technologies as part of regional technology diversification strategies. While currently a smaller market, planned semiconductor projects in the Gulf region could create future demand. Africa’s market remains nascent but shows potential growth with increasing electronics manufacturing activities in North African countries.

South America

South America’s Semiconductor Pellicle Market is developing, primarily serving regional electronics manufacturing needs. Brazil and Mexico show the most activity, with demand driven by consumer electronics production. The market remains dependent on imports but shows growing technical capabilities in semiconductor packaging that may drive future pellicle adoption.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Pellicle Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Pellicle Market?

-> Semiconductor Pellicle Market was valued at USD 393 million in 2025 and is projected to reach USD 601 million by 2033, exhibiting a CAGR of 6.5% during the forecast period.

Which key companies operate in Semiconductor Pellicle Market?

-> Key players include Mitsui Chemicals, Shin-Etsu, FINE SEMITECH, Micro Lithography, Inc., S&S Tech, and INKO, with the top 3 companies holding nearly 80% market share in 2025.

What are the key growth drivers?

-> Key growth drivers include advancements in photolithography technology, increasing demand for semiconductor manufacturing, and stringent requirements for defect control in advanced chip processes (7nm and below).

Which region dominates the market?

-> Asia dominates the market, particularly countries like China, Japan, and South Korea, due to their strong semiconductor manufacturing base.

What are the emerging trends?

-> Emerging trends include adoption of EUV lithography technology, development of advanced pellicles for reflective masks, and precision coating technologies like PVD/CVD.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...