Semiconductor Packaging Cleaning Agents Market Insights

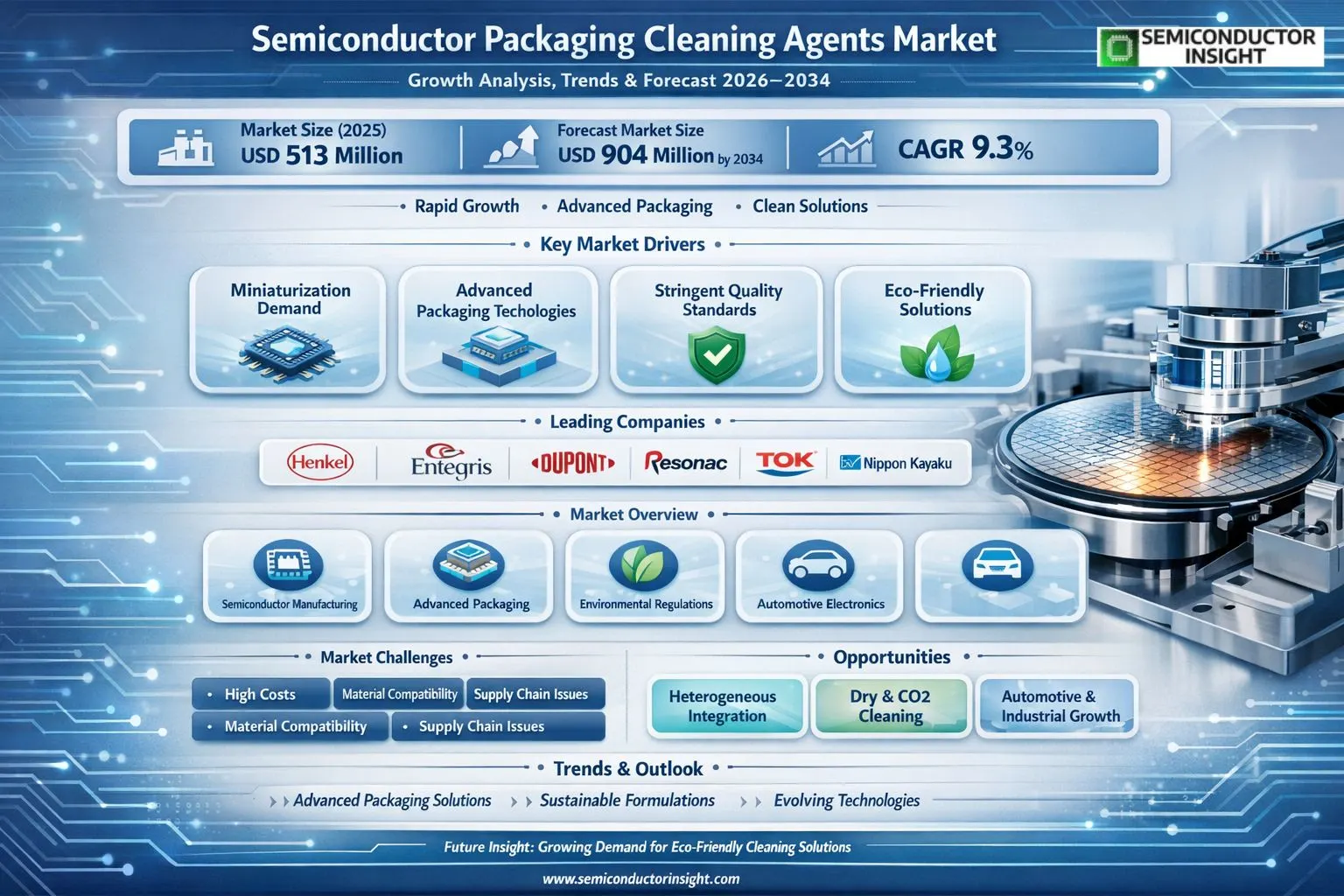

Global Semiconductor Packaging Cleaning Agents market size was valued at USD 513 million in 2025. The market is projected to grow from USD 561 million in 2026 to USD 904 million by 2034, exhibiting a CAGR of 9.3% during the forecast period.

Semiconductor Packaging Cleaning Agents are specialized chemical formulations designed for cleaning semiconductor devices and their packaging during manufacturing processes. These agents are crucial for removing residues, contaminants, and impurities such as flux, particles, and ionic compounds that can compromise device performance and reliability. Their application spans various packaging types including DIP, SOP, QFP, QFN, BGA, LGA, and PGA.

The market is experiencing robust growth due to several factors, including the relentless miniaturization of semiconductor devices and the increasing complexity of advanced packaging architectures like Fan-Out Wafer-Level Packaging (FOWLP) and 3D ICs. Furthermore, stringent quality requirements for high-reliability applications in automotive electronics and data centers are driving demand for superior cleaning solutions. Initiatives by key players are also expected to fuel market growth. For instance, leading suppliers continuously innovate to develop environmentally sustainable water-based formulations with high efficacy while complying with evolving regulations like REACH. Henkel AG & Co. KGaA, Entegris Inc., DuPont de Nemours Inc., Resonac Holdings Corporation (formerly Showa Denko), and Tokyo Ohka Kogyo Co., Ltd. (TOK) are some of the key players that operate in the market with a wide range of portfolios.

MARKET DRIVERS

Advancements in Semiconductor Packaging Complexity

The relentless drive for miniaturization and performance in electronics, particularly for high-performance computing and artificial intelligence applications, is a primary catalyst. Advanced packaging technologies like 2.5D/3D IC integration and fan-out wafer-level packaging feature extremely dense interconnects and require impeccable cleanliness. Contaminants as small as a few nanometers can cause catastrophic failure, directly increasing the demand for high-purity Semiconductor Packaging Cleaning Agents Market solutions capable of removing ionic residues, organic flux, and particles from these intricate structures.

Stringent Yield and Reliability Imperatives

In semiconductor manufacturing, yield is paramount. Post-assembly contaminants are a leading cause of electrical shorts, corrosion, and delamination, impacting device reliability and longevity. As package dimensions shrink, the tolerance for any residue diminishes to near zero. This has compelled packaging foundries and OSAT providers to adopt more aggressive and specialized cleaning processes, fueling innovation and adoption of advanced cleaning chemistries within the semiconductor packaging cleaning agents market to protect multi-billion-dollar wafer investments.

➤ Global shift towards electric vehicles and 5G infrastructure is creating sustained demand for power semiconductors and RF modules, which rely on robust packaging that must withstand harsh operating conditions, further emphasizing the need for flawless cleaning.

Concurrently, the industry’s sustainability goals are driving development of newer, environmentally compliant Semiconductor Packaging Cleaning Agents. Regulations phasing out hazardous substances are pushing manufacturers to replace traditional solvents with safer, yet equally effective, aqueous or semi-aqueous cleaning chemistries, opening a new front for market growth and R&D.

MARKET CHALLENGES

Technical Hurdles in Cleaning Advanced Materials

As packaging evolves, so do the material sets. The introduction of novel substrates, low-k dielectrics, and delicate copper pillar bumps presents significant challenges. Many advanced materials are chemically sensitive and can be damaged by traditional aggressive cleaning agents. Developing formulations for the Semiconductor Packaging Cleaning Agents Market that effectively remove stubborn contamination without etching, swelling, or degrading these new materials requires substantial and costly R&D, creating a high barrier for chemical suppliers.

Other Challenges

Process Integration and Cost Pressure

Integrating a new cleaning chemistry into an established high-volume manufacturing line is complex and risky. It requires extensive qualification, compatibility testing with photoresists and adhesives, and potential retooling of equipment. Furthermore, relentless cost pressure from semiconductor manufacturers forces cleaning agent suppliers to deliver superior performance without significant price increases, squeezing profit margins.

Supply Chain and Raw Material Volatility

The production of high-purity specialty chemicals depends on a stable supply of raw materials. Geopolitical tensions and trade policies can disrupt this supply, leading to price volatility and availability issues for key ingredients used in Semiconductor Packaging Cleaning Agents. This insecurity complicates long-term planning and stable pricing for market participants.

MARKET RESTRAINTS

High Development and Validation Costs

The path from laboratory formulation to qualified production-grade cleaning agent is capital-intensive. Each new chemistry must undergo rigorous testing for efficacy, material compatibility, and long-term reliability, often over thousands of hours. The stringent validation protocols required by leading semiconductor fabs and OSATs mean that only well-funded, established chemical companies can typically compete, limiting new entrants and potentially slowing the pace of innovation in the Semiconductor Packaging Cleaning Agents Market.

Maturity and Optimization of Legacy Processes

For many established, mainstream packaging applications, cleaning processes are highly optimized and entrenched. Manufacturers are often hesitant to switch chemistries or methods due to the perceived risk of introducing new variables that could impact yield. This inertia towards adopting new Semiconductor Packaging Cleaning Agents, especially for legacy nodes and packages, restrains market expansion, as suppliers must demonstrate a clear and compelling return on investment to overcome this resistance.

MARKET OPPORTUNITIES

Emergence of Heterogeneous Integration and Chiplets

The paradigm shift towards chiplet-based designs and heterogeneous integration represents a major growth vector. This architecture involves assembling multiple dies with different functions into a single package, drastically increasing the number of bonds and interfaces that must be perfectly clean. This creates a specialized need for cleaning agents that can handle mixed material surfaces and clean deep within complex, multi-die stacks, opening a premium segment within the Semiconductor Packaging Cleaning Agents Market.

Adoption of Dry Cleaning and Supercritical CO2 Technologies

While wet chemistry dominates, environmental and technical limitations are fostering interest in alternative methods. Dry cleaning techniques using plasma or cryogenic aerosols, and supercritical CO2 cleaning, offer residue-free drying and excellent penetration for high-aspect-ratio features. The development and commercialization of compatible chemistries and processes for these platforms present a significant opportunity for forward-looking companies in the semiconductor packaging cleaning agents sector to establish early leadership in a nascent field.

Expansion in Automotive and Industrial Semiconductor Demand

The automotive industry’s transition to electric and autonomous vehicles requires a massive increase in semiconductor content, particularly in power modules and sensors that demand extremely reliable packaging. Similarly, growth in industrial IoT and automation drives demand for robust chips. These sectors have zero-tolerance for failure, mandating the use of the highest-performance cleaning processes and agents, thereby providing a stable, high-growth end-market for advanced Semiconductor Packaging Cleaning Agents.

Semiconductor Packaging Cleaning Agents Market Trends

Accelerated Demand for Advanced Packaging Solutions

The Semiconductor Packaging Cleaning Agents Market is experiencing a clear trend driven by the industry-wide transition to advanced packaging architectures like Fan-Out Wafer-Level Packaging (FOWLP) and 2.5D/3D integration. These high-density packaging methods create intricate geometries and tighter spaces that are more susceptible to contamination from fluxes, residues, and particles. This necessitates the development and adoption of more sophisticated cleaning chemistries capable of precise, residue-free cleaning without damaging delicate interconnects or substrates. Manufacturers are consequently shifting towards specialized formulations within the Semiconductor Packaging Cleaning Agents Market to ensure yield and long-term device reliability in these demanding applications.

Other Trends

Shift Towards Safer and Sustainable Formulations

A prominent operational trend is the growing preference for water-based and semi-aqueous cleaning agents over traditional solvent-based systems. This shift is propelled by stringent global environmental regulations, such as those limiting volatile organic compound (VOC) emissions, and by corporate sustainability goals. While effective, newer water-based agents in the Semiconductor Packaging Cleaning Agents Market must achieve the same high-performance cleaning benchmarks for ionic contamination and organic residue removal, pushing innovation in surfactant technology and rinse processes.

Material Innovation for Heterogeneous Integration

The rise of heterogeneous integration, which combines different die types and materials within a single package, presents a unique challenge for the Semiconductor Packaging Cleaning Agents Market. Cleaning processes must be compatible with a diverse set of materials, including various solder alloys, organic substrates, metals, and polymers, without causing corrosion or delamination. This trend is driving the customization of cleaning agents for specific material sets and the development of multi-functional chemistries that can safely remove a broader spectrum of contaminants.

Supply Chain Diversification and Regional Manufacturing Growth

Geopolitical factors and supply chain resilience initiatives are influencing the Semiconductor Packaging Cleaning Agents Market, with increased semiconductor fabrication capacity being built in regions like North America, Europe, and Southeast Asia. This geographic diversification of packaging and assembly operations is creating parallel demand for localized supply and technical support for cleaning agents. Key suppliers are adapting by strengthening regional distribution networks and application engineering teams to serve these new manufacturing hubs effectively and responsively.

COMPETITIVE LANDSCAPE

Key Industry Players

A High-Growth Market Defined by Specialty Chemical and Materials Science Expertise

Global Semiconductor Packaging Cleaning Agents market is moderately consolidated, with the top five players accounting for a significant revenue share. Leading the market are multinational specialty chemical and materials science corporations such as Henkel, Entegris, and DuPont. These established giants leverage their deep R&D capabilities, global supply chains, and comprehensive product portfolios tailored for advanced semiconductor fabrication. Their solutions are critical for removing residues and contaminants from packages like BGAs, LGAs, and QFNs, ensuring device performance and reliability. Competition centers on developing high-purity, environmentally compliant agents,including both solvent-based and water-based formulations,that meet the stringent requirements of next-generation packaging technologies and increasing miniaturization.

The competitive field extends to prominent Japanese chemical suppliers like Resonac, Tokyo Ohka Kogyo (TOK), Nippon Kayaku, and Kao Corporation, which hold strong positions, particularly in the Asia-Pacific region. These players compete on advanced formulation technology and close collaboration with regional semiconductor manufacturers. Furthermore, specialized niche players, including Zestron and several agile Chinese suppliers, are gaining traction by offering cost-effective solutions and rapid technical support for specific applications and emerging regional packaging hubs. This creates a dynamic landscape where partnership with OEMs and continuous innovation in green chemistry are key competitive differentiators.

List of Key Semiconductor Packaging Cleaning Agents Companies Profiled

- Henkel AG & Co. KGaA

- Entegris, Inc.

- DuPont de Nemours, Inc.

- Resonac Holdings Corporation

- Tokyo Ohka Kogyo Co., Ltd. (TOK)

- Nippon Kayaku Co., Ltd.

- Syensqo SA

- LCY Chemical Corp.

- KISCO Ltd.

- Kao Corporation

- Zestron GmbH

- Enviro Tech International, Inc.

- Shenzhen Capchem Technology Co., Ltd.

- Guangdong Shuangke New Materials Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Solvent-based cleaning agents are the dominant category due to their superior efficacy in dissolving tough organic residues and ionic contaminants without damaging delicate packaging components. The segment benefits from established formulations offering high vapor pressure for rapid drying and compatibility with a wide array of packaging materials. However, evolving environmental, health, and safety regulations are prompting significant R&D efforts to enhance the sustainability profile of these solutions while maintaining their critical cleaning performance, creating a dynamic competitive landscape for manufacturers. |

| By Application |

|

BGA/LGA/PGA Packaging represents the leading and most demanding application segment, driven by the proliferation of high-performance computing, servers, and advanced consumer electronics. The complex, high-density interconnect structures and fine-pitch solder balls in these packages are exceptionally vulnerable to flux residues and micro-contaminants that can cause electrical failures, necessitating highly precise and effective cleaning chemistries. This segment commands specialized agent formulations that ensure complete residue removal from under the package without compromising solder joint integrity or substrate materials, making it a key focus area for innovation. |

| By End User |

|

Outsourced Semiconductor Assembly and Test (OSAT) providers constitute the largest end-user segment due to the industry’s heavy reliance on external packaging and testing services. OSATs operate at high volumes across diverse packaging technologies, creating substantial, consistent demand for reliable, high-throughput cleaning agents. Their procurement strategies emphasize supply chain stability, technical support for process optimization, and cost-effectiveness. Furthermore, as OSATs are at the forefront of adopting new, complex packaging architectures like 2.5D/3D ICs, they drive the co-development of next-generation cleaning solutions with chemical suppliers to address novel contamination challenges. |

| By Cleaning Process |

|

Post-Solder Flux Removal is the most critical and widespread cleaning process, essential for ensuring long-term device reliability after solder reflow operations. The shift towards lead-free and low-residue “no-clean” fluxes has not eliminated the need for cleaning, as even minimal residues can cause corrosion or dendritic growth in humid environments. This process segment demands agents with excellent solvency power for specific flux chemistries, combined with low surface tension to penetrate dense component arrays. The effectiveness of this step directly impacts yield and is a major determinant in the selection and qualification of cleaning agents by manufacturers. |

| By Technology Focus |

|

Advanced & Heterogeneous Integration is the leading high-growth technology focus, encompassing 2.5D/3D ICs, chiplets, and fan-out wafer-level packaging. These architectures introduce unique cleaning challenges such as removing residues from deep, high-aspect-ratio through-silicon vias (TSVs), cleaning delicate microbumps, and preventing damage to low-k dielectrics and novel underfill materials. Agents for this segment are characterized by ultra-high purity, tailored chemical selectivity, and compatibility with new material sets. Success in this area requires close collaboration between cleaning agent suppliers and packaging pioneers to develop customized, precision cleaning protocols that enable next-generation performance. |

Regional Analysis: Semiconductor Packaging Cleaning Agents Market

Asia-Pacific

Taiwan and South Korea represent the technological vanguard, home to the world’s leading foundries and memory manufacturers. The relentless drive for node shrinks and the adoption of complex packaging schemes in these countries necessitates the most advanced, low-residue cleaning formulations. Suppliers must meet extreme purity standards demanded by these flagship fabs, making this sub-region a critical testing ground for next-generation agents targeting post-etch and post-CMP cleaning challenges.

China’s aggressive push to develop an indigenous semiconductor industry is a primary growth engine for the packaging cleaning agents market. The establishment of numerous new OSAT (Outsourced Semiconductor Assembly and Test) facilities and integrated device manufacturers (IDMs) is generating significant demand for reliable, cost-effective cleaning solutions. This expansion focuses on mid-range to advanced packaging, creating opportunities for both established global suppliers and emerging local chemical manufacturers.

Japan remains a key center for high-purity chemical innovation and manufacturing, supplying critical ingredients for cleaning formulations globally. Concurrently, Southeast Asian nations like Malaysia, Singapore, and Vietnam are growing as vital hubs for back-end packaging and testing operations. This dual role strengthens the regional supply chain, with Japan providing material expertise and Southeast Asia offering high-volume manufacturing demand for established cleaning processes.

Across Asia-Pacific, regulatory pressures concerning chemical safety, wastewater discharge, and environmental impact are intensifying. This is catalyzing a shift towards greener, more sustainable semiconductor packaging cleaning agents, including aqueous-based systems and chemistries with lower global warming potential. Manufacturers and chemical suppliers are increasingly collaborating to develop compliant, effective solutions that meet both performance and emerging environmental, social, and governance (ESG) criteria.

North America

North America maintains a strong position in the semiconductor packaging cleaning agents market, characterized by high-value, innovation-led demand. The region is a powerhouse for R&D in next-generation packaging architectures, such as heterogeneous integration and chiplets, often pioneered by leading fabless design companies and integrated device manufacturers (IDMs). This emphasis on cutting-edge research creates a premium market for highly specialized, application-specific cleaning chemistries used in pilot lines and low-volume, high-mix production. Furthermore, major initiatives like the U.S. CHIPS and Science Act are catalyzing significant domestic reinvestment in semiconductor manufacturing, including advanced packaging facilities. This is expected to boost onshore demand for high-performance cleaning agents, with a strong focus on supply chain security, intellectual property protection, and collaboration between material science firms and national research consortia.

Europe

The European market for semiconductor packaging cleaning agents is defined by a focus on specialized, high-reliability applications, particularly within the automotive, industrial, and aerospace sectors. This drives demand for robust cleaning solutions that ensure extreme longevity and performance under harsh conditions, supporting technologies like power electronics and MEMS packaging. The region’s strong environmental regulations, including stringent REACH compliance, heavily influence market dynamics, pushing chemical suppliers to pioneer sustainable and safe formulations. While Europe’s manufacturing footprint in volume packaging is smaller than Asia’s, its strategic focus on packaging research,supported by programs like the European Chips Act,aims to foster innovation in key niches. This creates a stable, quality-oriented market for cleaning agents that meet both advanced technical specifications and rigorous regulatory standards.

South America

The South American market for semiconductor packaging cleaning agents is presently niche but exhibits potential for gradual growth. Current demand is primarily linked to the servicing and maintenance of existing electronics assembly and limited semiconductor packaging operations, which are often focused on consumer electronics and industrial applications. The region lacks a significant domestic semiconductor fabrication base, so the cleaning agent market is largely import-dependent, served by global distributors and chemical suppliers. Growth is tied to broader economic development and potential future investments in regional electronics manufacturing. However, any expansion would require parallel development of technical support infrastructure and supply chains to meet the specific needs of semiconductor-grade chemical handling and application.

Middle East & Africa

The Middle East & Africa region represents an emerging market with strategic initiatives that could influence long-term demand for semiconductor packaging cleaning agents. Certain Gulf nations are making substantial sovereign investments in technology diversification, which includes ambitions to develop downstream electronics manufacturing and potentially attract packaging and assembly operations. While a large-scale, established market for these specialized chemicals does not currently exist, these long-term vision projects could create future demand. Present activities are confined to academic research collaborations, pilot projects, and the supply of agents for maintenance in existing industrial and telecommunications infrastructure. Market development is contingent on the successful realization of these high-tech economic diversification plans and the concurrent build-out of necessary technical ecosystems.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Packaging Cleaning Agents Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Packaging Cleaning Agents Market?

-> Global Semiconductor Packaging Cleaning Agents Market was valued at USD 513 million in 2025 and is projected to reach USD 904 million by 2034, at a CAGR of 9.3% during the forecast period.

Which key companies operate in Semiconductor Packaging Cleaning Agents Market?

-> Key players include Henkel, Entegris, DuPont, Resonac, Tokyo Ohka Kogyo (TOK), Nippon Kayaku, Syensqo, LCY, KISCO, and Kao Corporation, among others.

What are the key growth drivers?

-> The market is driven by the critical need to remove residues, contaminants, and impurities during semiconductor manufacturing to ensure device performance, reliability, and miniaturization trends across various advanced packaging applications.

Which region dominates the market?

-> The Asia region is a dominant and rapidly growing market, led by major semiconductor manufacturing hubs such as China, Japan, South Korea, and Southeast Asia. The U.S. market also represents a significant share within North America.

What are the emerging trends?

-> Emerging trends include advancements in specialized cleaning agent formulations, increasing demand for water-based and environmentally sustainable solutions, and stringent cleaning requirements for advanced packaging types like BGA, QFN, and Fan-Out Wafer Level Packaging (FOWLP).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...