MARKET INSIGHTS

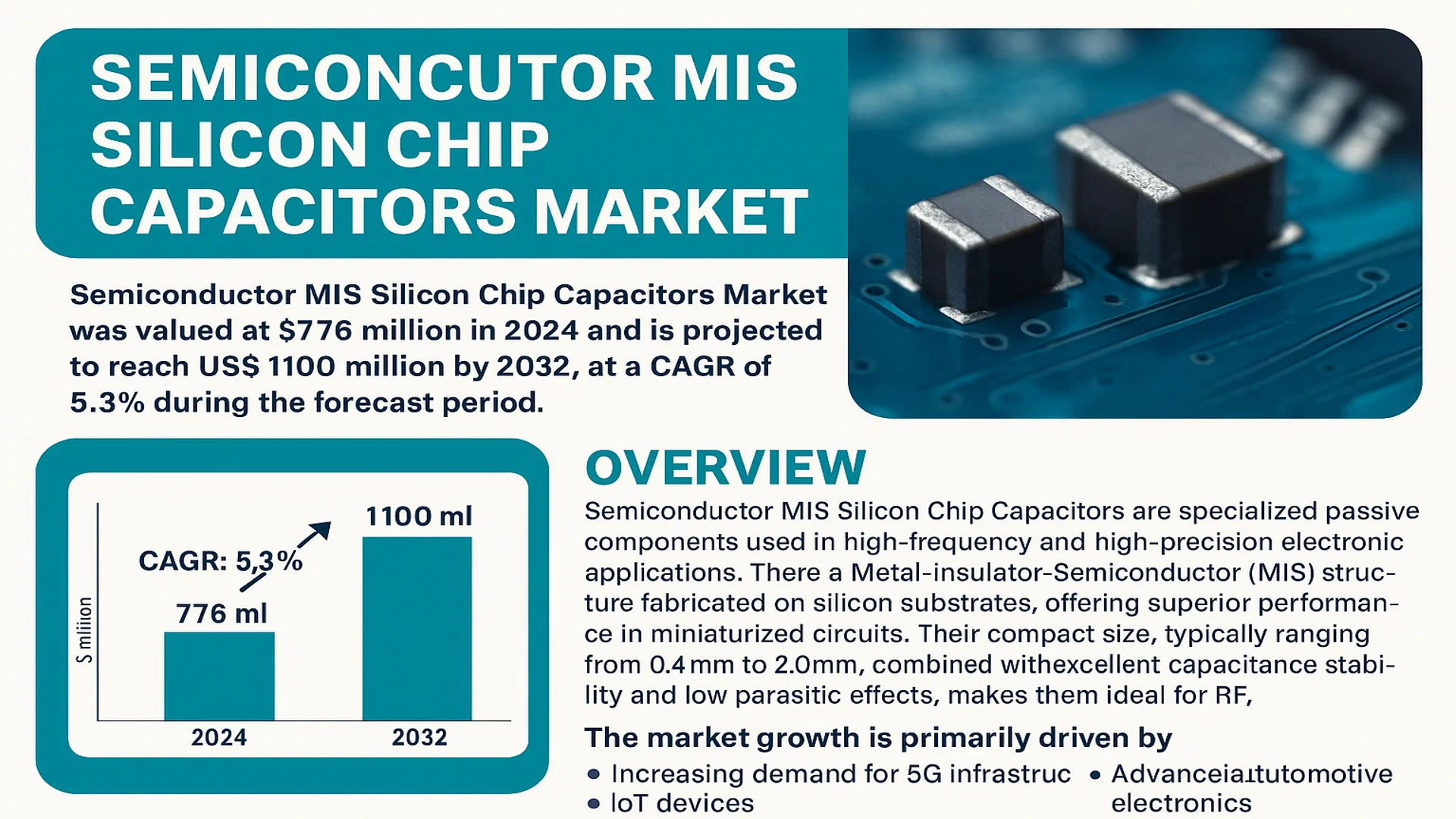

The global Semiconductor MIS Silicon Chip Capacitors Market was valued at 776 million in 2024 and is projected to reach US$ 1100 million by 2032, at a CAGR of 5.3% during the forecast period.

Semiconductor MIS Silicon Chip Capacitors are specialized passive components used in high-frequency and high-precision electronic applications. These capacitors feature a Metal-Insulator-Semiconductor (MIS) structure fabricated on silicon substrates, offering superior performance in miniaturized circuits. Their compact size, typically ranging from 0.4mm to 2.0mm, combined with excellent capacitance stability and low parasitic effects, makes them ideal for RF, microwave, and high-speed digital applications.

The market growth is primarily driven by increasing demand for 5G infrastructure, IoT devices, and advanced automotive electronics. While North America currently holds the largest market share, Asia-Pacific is expected to witness the highest growth rate due to expanding semiconductor manufacturing capabilities in China, Taiwan, and South Korea. Key players like Murata, TDK, and AVX dominate the market, collectively holding over 60% of global revenue share in 2024, as they continue to innovate in high-density capacitor technologies for next-generation electronics.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 5G and IoT Technologies Accelerating Market Expansion

The rapid deployment of 5G networks and Internet of Things (IoT) devices is significantly driving demand for semiconductor MIS silicon chip capacitors. These components are essential for high-frequency signal processing in 5G base stations, smartphones, and IoT endpoints. The global 5G infrastructure market is projected to grow at over 40% CAGR through 2030, requiring millions of high-performance capacitors for RF filtering and power management. Major telecom equipment manufacturers are increasingly adopting MIS silicon capacitors due to their superior performance in millimeter-wave frequencies and compact form factor. For instance, recent network infrastructure upgrades in North America and Asia-Pacific regions are utilizing these components in massive MIMO antenna systems.

Automotive Electronics Revolution Creating New Growth Avenues

The automotive industry’s transition toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is fueling significant demand for reliable capacitor solutions. Modern vehicles contain over 3,000 semiconductor components on average, with MIS silicon chip capacitors playing critical roles in powertrain control units, infotainment systems, and autonomous driving modules. The shift to 48V architectures in EVs particularly benefits from these capacitors’ high voltage tolerance and temperature stability. Leading automakers are now specifying MIS silicon capacitors for safety-critical applications where component failure isn’t an option, creating sustained demand growth across the automotive supply chain.

Miniaturization Trend in Consumer Electronics Driving Adoption

Consumer electronics manufacturers continue pushing the boundaries of device miniaturization while increasing functionality. This paradox creates immense demand for passive components that offer maximum capacitance in minimum footprint. Semiconductor MIS silicon chip capacitors are gaining traction in smartphones, wearables, and hearables where PCB real estate is at premium. Recent flagship smartphones now incorporate over 1,000 passive components with space constraints driving 60% of designs toward chip-scale packaging solutions. The ability of MIS silicon capacitors to deliver stable performance in sub-millimeter packages makes them ideal for next-generation portable electronics.

➤ High-performance computing applications are adopting MIS silicon capacitors at 2.5x the rate of traditional MLCCs due to superior high-frequency characteristics and reliability.

MARKET RESTRAINTS

Supply Chain Vulnerabilities Constraining Market Growth

The semiconductor MIS silicon chip capacitor market faces significant challenges from global supply chain disruptions. The industry’s reliance on specialized silicon wafers and rare earth materials creates bottlenecks when geopolitical tensions or natural disasters impact production. Recent trade restrictions have caused lead times for certain capacitor types to extend beyond 40 weeks, forcing manufacturers to maintain excessive inventory levels. Smaller electronics firms in particular struggle with these supply chain challenges, often delaying product launches or redesigning circuits to accommodate available components.

High Production Costs Limiting Market Penetration

While performance advantages are clear, semiconductor MIS silicon chip capacitors carry significant cost premiums over traditional ceramic alternatives. Production requires expensive semiconductor fabrication equipment and cleanroom facilities, with yield optimization remaining an ongoing challenge. Current manufacturing costs for silicon capacitors range 3-5x higher than equivalent MLCCs, making price-sensitive applications hesitant to adopt the technology. While economies of scale are gradually reducing this gap, the cost differential remains a substantial barrier for mass-market electronics.

MARKET CHALLENGES

Technical Complexity in High-Volume Manufacturing

Scaling production of semiconductor MIS silicon chip capacitors presents unique engineering challenges. The intricate MIS structures require atomic-level precision during deposition and etching processes, with even minor variations causing significant yield losses. Current production lines achieve approximately 75-85% yields for complex multilayer designs, forcing manufacturers to either absorb these losses or pass costs to customers. Developing more robust manufacturing processes without compromising performance characteristics remains an ongoing challenge across the industry.

Other Challenges

Thermal Management Issues

As operating frequencies increase, power dissipation becomes a critical concern. The small form factor of MIS silicon capacitors makes heat dissipation challenging, particularly in densely packed circuit designs. Thermal cycling can accelerate aging effects, potentially impacting long-term reliability in harsh environments.

Standardization Gaps

The relatively new technology lacks unified industry standards for critical parameters like lifetime expectations or failure modes. This creates uncertainty for design engineers when qualifying components for mission-critical applications.

MARKET OPPORTUNITIES

Emerging Applications in Medical Electronics Creating New Potential

The medical device industry represents a high-growth opportunity for semiconductor MIS silicon chip capacitors. Implantable devices, diagnostic equipment, and portable medical monitors increasingly require capacitors that combine miniature size with absolute reliability. Recent advancements in wireless body area networks and ingestible sensors are driving demand for biocompatible passive components. The global medical electronics market is projected to exceed $8 billion by 2027, with capacitor requirements growing at an even faster rate due to increasing functionality in wearable health monitors.

AI and Edge Computing Driving Next-Generation Requirements

Artificial intelligence applications at the edge are creating demand for capacitors with unprecedented performance characteristics. AI processors require ultra-stable power delivery with minimal latency, making MIS silicon capacitors ideal for power rail decoupling in neural network accelerators. The proliferation of edge AI chips, projected to grow at 25% CAGR through 2030, will drive innovation in capacitor technology to meet these specialized requirements. Leading chipset manufacturers are already collaborating with capacitor suppliers to develop solutions optimized for AI workloads.

Military and Aerospace Modernization Programs Offering Stability

Government investments in defense electronics modernization provide stable long-term opportunities for high-reliability capacitor manufacturers. Next-generation radar systems, satellite communications, and avionics demand components that withstand extreme environments while maintaining precise electrical characteristics. Military applications typically prioritize performance over cost, making them ideal for premium MIS silicon capacitor solutions. Recent defense budget increases across major economies are expected to sustain this segment’s growth despite broader economic uncertainties.

SEMICONDUCTOR MIS SILICON CHIP CAPACITORS MARKET TRENDS

Miniaturization and High-Frequency Applications Driving Market Growth

The global Semiconductor MIS Silicon Chip Capacitors Market is experiencing significant growth due to the increasing demand for miniaturized components in high-frequency electronic applications. These capacitors, known for their compact size and superior performance in radio frequency (RF) environments, are critical in telecommunications, 5G infrastructure, and IoT devices. As of 2024, the market is valued at $776 million, with projections indicating a rise to $1100 million by 2032 at a CAGR of 5.3%. This expansion is largely fueled by the rapid development of 5G networks, which require high-performance capacitors for signal filtering and power management. Additionally, the rise in electric vehicle (EV) production is contributing to market demand, as these capacitors are essential in automotive electronic systems for their thermal stability and reliability.

Other Trends

Demand Surge in Consumer Electronics

Consumer electronics remain a dominant application segment, driven by the growing adoption of smartphones, wearables, and smart home devices. The shift toward higher frequency operations in these gadgets necessitates components like MIS silicon chip capacitors that offer low parasitic inductance and high capacitance density. While the U.S. leads in market share, China is rapidly catching up with substantial investments in semiconductor manufacturing infrastructure. The increasing integration of AI and IoT within consumer electronics further intensifies demand, as these technologies require robust and efficient capacitive components for seamless operation.

Collaborations and Technological Innovations

Key industry players, including Murata, TDK, and AVX, are investing in R&D to enhance capacitor performance, particularly in multilayer designs, which accounted for a significant portion of revenue in 2024. The development of new dielectric materials and thin-film technologies has improved capacitance stability under extreme conditions, expanding applications in medical devices and industrial automation. Furthermore, partnerships between semiconductor manufacturers and automotive companies are fostering innovations tailored for autonomous vehicles, where these capacitors play a critical role in LiDAR and ADAS systems. The shift toward greener manufacturing processes is also influencing production techniques, with companies increasingly adopting lead-free materials to comply with global environmental regulations.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Expand Capacitor Innovations to Meet Rising Demand

The global Semiconductor MIS Silicon Chip Capacitors market is characterized by intense competition among established players and emerging innovators, with the top five companies collectively holding a significant market share as of 2024. Murata Manufacturing and TDK Corporation dominate the space, leveraging their decades of experience in passive components and strong relationships with semiconductor foundries. These Japanese titans have maintained leadership through continuous R&D investments, exemplified by Murata’s recent development of ultra-thin 01005-size capacitors for 5G applications.

Skyworks Solutions has emerged as a formidable competitor in RF-oriented capacitor solutions, capitalizing on its vertical integration capabilities. Meanwhile, Vishay Intertechnology strengthens its position through strategic acquisitions and a diversified product portfolio spanning both single-layer and multilayer configurations. The company’s recent expansion of its silicon capacitor production capacity in Israel underscores this growth strategy.

While established players maintain dominance, smaller specialized firms like Johanson Technology and Massachusetts Bay Technologies are gaining traction by focusing on niche applications. Their ability to deliver customized solutions for aerospace and medical applications has allowed them to carve out profitable market segments despite the competitive pressures.

Recent industry developments highlight the dynamic nature of this competition: AVX Corporation’s 2023 breakthrough in high-temperature silicon capacitors for automotive applications and Taiyo Yuden’s partnership with a major Taiwanese semiconductor manufacturer demonstrate how companies are differentiating themselves. Further consolidation appears likely as firms seek to bolster their technological capabilities and geographic reach.

List of Key Semiconductor MIS Silicon Chip Capacitor Manufacturers

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- Skyworks Solutions, Inc. (U.S.)

- Vishay Intertechnology, Inc. (U.S.)

- Johanson Technology, Inc. (U.S.)

- Massachusetts Bay Technologies (U.S.)

- SemiGen, Inc. (U.S.)

- Taiyo Yuden Co., Ltd. (Japan)

- KEMET Corporation (U.S.)

- AVX Corporation (U.S.)

- Yageo Corporation (Taiwan)

- Kyocera Corporation (Japan)

Segment Analysis:

By Type

Multilayer Segment Leads Due to Superior Performance in High-Frequency Applications

The market is segmented based on type into:

- Singlelayer

- Multilayer

- Subtypes: Stacked MIS, Trench MIS, and others

By Application

Telecommunication Segment Dominates Owing to Growing Demand for High-Speed Data Processing

The market is segmented based on application into:

- Telecommunication

- Consumer Electronics

- Automotive

- Industrial

- Medical

- Others

By Capacitance Range

Medium Capacitance Range (1nF-10nF) Preferred for Balanced Performance in Most Applications

The market is segmented based on capacitance range into:

- Low capacitance (below 1nF)

- Medium capacitance (1nF-10nF)

- High capacitance (above 10nF)

By End-User Industry

Semiconductor Manufacturing Sector Dominates Due to Critical Role in IC Production

The market is segmented based on end-user industry into:

- Semiconductor manufacturing

- Electronics component manufacturers

- Research and development institutions

- Defense and aerospace

Regional Analysis: Semiconductor MIS Silicon Chip Capacitors Market

Asia-Pacific

The Asia-Pacific region dominates the global Semiconductor MIS Silicon Chip Capacitors market, driven by strong demand from China, Japan, and South Korea. These countries house major semiconductor manufacturers and electronics OEMs, fueling the need for high-performance chip capacitors. China’s semiconductor industry, supported by government initiatives like the “Made in China 2025” policy, is rapidly expanding its domestic production capabilities. Japan and South Korea maintain technological leadership with companies like Murata and Samsung driving innovation in miniaturized components. The region benefits from robust supply chains and cost-competitive manufacturing, though recent geopolitical tensions have caused some supply chain adjustments.

North America

North America represents a high-value market for advanced Semiconductor MIS Silicon Chip Capacitors, particularly in defense, aerospace, and telecommunications applications. The U.S. leads in R&D investments, with companies like Skyworks and Vishay developing cutting-edge capacitor technologies. Recent CHIPS Act funding has accelerated domestic semiconductor production, creating new opportunities for component suppliers. Stringent quality requirements and the shift toward 5G infrastructure are key market drivers. However, higher production costs compared to Asia remain a challenge for regional manufacturers competing on price-sensitive applications.

Europe

Europe maintains a strong position in specialized segments of the Semiconductor MIS Silicon Chip Capacitors market, particularly for automotive and industrial applications. Germany’s automotive electronics sector and the Netherlands’ semiconductor equipment industry drive steady demand. EU regulations on electronic waste and hazardous substances influence product development trends toward more sustainable materials. While the region lacks the scale of Asian production, European companies like TDK and NXP focus on high-reliability components for mission-critical systems. The ongoing energy crisis and economic uncertainties have temporarily slowed some industrial investments in the region.

Middle East & Africa

This emerging market shows gradual growth in Semiconductor MIS Silicon Chip Capacitor adoption, primarily for telecommunications infrastructure and oil/gas industry applications. Israel has developed a niche in defense electronics requiring specialized components. The UAE and Saudi Arabia are investing in smart city projects that will increase demand over time. However, the market remains constrained by limited local manufacturing and reliance on imports. Technological adoption varies significantly across countries, with more advanced economies showing stronger growth potential in the long term.

South America

South America represents the smallest but growing market for Semiconductor MIS Silicon Chip Capacitors. Brazil accounts for the majority of regional demand, driven by consumer electronics production and automotive manufacturing. Economic instability and currency fluctuations have historically limited market growth, though increasing digital transformation initiatives are creating new opportunities. Local content requirements in some countries promote regional manufacturing, but most components continue to be imported. The market shows potential for gradual expansion as industrial automation increases across the region.

Report Scope

This market research report provides a comprehensive analysis of the Global Semiconductor MIS Silicon Chip Capacitors Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 776 million in 2024 and is projected to reach USD 1,100 million by 2032 at a CAGR of 5.3%.

- Segmentation Analysis: Detailed breakdown by product type (Singlelayer, Multilayer), application (Telecommunication, Consumer Electronics, Automotive, Industrial, Medical, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Skyworks, Vishay, Murata, TDK, and AVX.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards impacting MIS Silicon Chip Capacitors.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers in the semiconductor industry.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the semiconductor capacitor market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor MIS Silicon Chip Capacitors Market?

-> Semiconductor MIS Silicon Chip Capacitors Market was valued at 776 million in 2024 and is projected to reach US$ 1100 million by 2032, at a CAGR of 5.3% during the forecast period.

Which key companies operate in Global Semiconductor MIS Silicon Chip Capacitors Market?

-> Key players include Skyworks, Vishay, Murata, TDK, Taiyo Yuden, KEMET, AVX, and Johanson Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for miniaturized electronic components, growth in 5G infrastructure, automotive electronics expansion, and rising adoption in medical devices.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing region, driven by semiconductor manufacturing hubs in China, Japan, and South Korea, while North America remains a key innovation center.

What are the emerging trends?

-> Emerging trends include development of high-density capacitors, integration with advanced packaging technologies, and increasing use in RF applications for 5G and IoT devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...