MARKET INSIGHTS

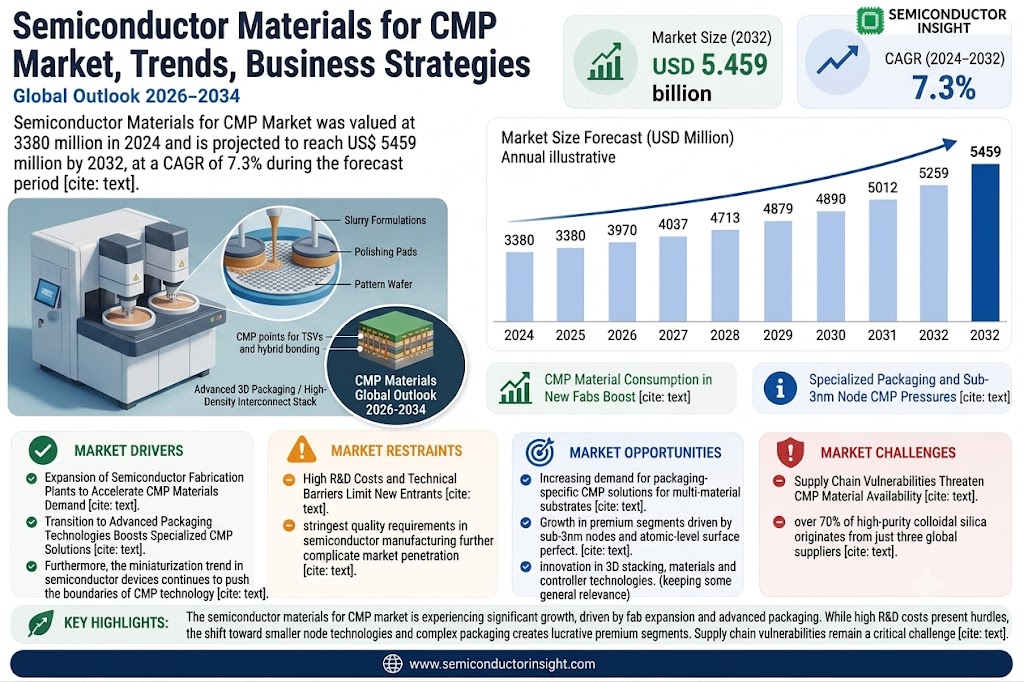

The global Semiconductor Materials for CMP Market was valued at 3380 million in 2024 and is projected to reach US$ 5459 million by 2032, at a CAGR of 7.3% during the forecast period.

Semiconductor materials for CMP are critical components used in wafer fabrication to achieve ultra-flat surfaces through a combination of chemical and mechanical polishing. The market encompasses three primary product categories: CMP slurries (abrasive chemical solutions), CMP pads (polishing surfaces), and CMP ancillaries (including pad conditioners, filters, and retaining rings). These materials enable precise lithography patterning by removing excess material and minimizing defects during chip manufacturing.

Market growth is driven by increasing semiconductor miniaturization demands and the proliferation of advanced nodes (below 7nm). While the CMP slurry segment dominates with 77% market concentration among top eight suppliers, pad conditioners show even higher consolidation with 90% market share held by five manufacturers. Recent strategic moves, like Fujifilm’s acquisition of Entegris’ electronic chemicals business in 2023, are reshaping the competitive landscape alongside established players including DuPont (66% pad market share) and Merck KGaA.

MARKET DYNAMICS

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Semiconductor Fabrication Plants to Accelerate CMP Materials Demand

The global semiconductor industry is witnessing unprecedented growth with the establishment of new fabrication facilities worldwide. Governments and private players are investing heavily in semiconductor manufacturing to reduce dependency on imports and strengthen supply chain resilience. Over 35 new fabs are expected to begin operations between 2024 and 2026, significantly increasing the demand for CMP materials. This expansion is particularly notable in Asia-Pacific regions where semiconductor manufacturing has seen substantial investments. Each advanced semiconductor fab can consume over $50 million annually in CMP materials, making fab expansion the most significant driver for market growth. The industry shift towards smaller node technologies below 7nm further intensifies CMP material requirements as these processes require more polishing steps.

Transition to Advanced Packaging Technologies Boosts Specialized CMP Solutions

Emerging packaging technologies like 3D IC, fan-out wafer-level packaging, and hybrid bonding are driving innovation in the CMP materials segment. Advanced packaging now accounts for nearly 40% of semiconductor manufacturing processes and requires specialized slurries and pads to handle multi-material substrates. The integration of through-silicon vias (TSVs) in 3D packaging demands exceptionally precise planarization, increasing the consumption of copper and barrier slurry formulations. With packaging becoming a critical enabler of performance improvements in cutting-edge chips, manufacturers are investing heavily in developing packaging-specific CMP solutions that can handle delicate interconnect structures while maintaining high removal rate selectivity.

Furthermore, the miniaturization trend in semiconductor devices continues to push the boundaries of CMP technology. Nodes below 3nm require atomic-level surface perfection, driving the development of ultra-pure slurries with particle sizes below 50nm and specialized conditioning systems. These technological advancements are creating premium segments within the CMP market where manufacturers can command higher prices for cutting-edge solutions.

MARKET RESTRAINTS

High R&D Costs and Technical Barriers Limit New Entrants

The semiconductor CMP materials market presents substantial barriers to entry due to the complex chemistry and physics involved in slurry and pad development. Creating formulations that meet the exacting standards of advanced node manufacturing requires investments exceeding $50 million in research facilities and testing equipment. New slurry formulations can take 3-5 years to develop from concept to commercial viability, with particle size distribution control often proving particularly challenging. This extended development cycle, combined with the need to validate materials in customer production environments, creates significant roadblocks for companies attempting to enter the high-end segment of the market.

The stringent quality requirements in semiconductor manufacturing further complicate market penetration. Slurry contamination at parts-per-billion levels can render an entire wafer lot unusable, forcing manufacturers to maintain ultra-clean production environments. The cost of establishing Class 1 cleanrooms for slurry production alone can exceed $100 million for medium-scale operations. These financial and technical hurdles preserve the market dominance of established players while limiting competition that could drive price reductions.

MARKET CHALLENGES

Supply Chain Vulnerabilities Threaten CMP Material Availability

The semiconductor CMP materials industry faces significant supply chain risks stemming from concentration in raw material sourcing. Over 70% of high-purity colloidal silica, a key slurry component, originates from just three global suppliers. Similarly, polyurethane pad materials depend on specialized isocyanate formulations available from limited chemical producers. This concentration creates single points of failure where disruptions can ripple through the semiconductor manufacturing pipeline. The 2021 global supply chain crisis demonstrated how regional production halts could create months-long shortages of critical CMP materials, forcing fabs to reduce output despite strong demand.

Other Challenges

Environmental Regulations

Increasing environmental regulations governing chemical handling and disposal present ongoing challenges for CMP material manufacturers. Many slurry formulations contain metals like copper and tungsten that face strict wastewater discharge limits, requiring expensive treatment systems. The transition to greener chemistries involves complex reformulations that must maintain performance characteristics while reducing environmental impact.

Process Integration Complexities

The interdependence between CMP materials and other process steps creates significant integration challenges. Each new device generation requires coordinated development between slurry manufacturers, pad producers, and tool makers to ensure compatibility across the entire polishing system. These integration challenges lengthen development cycles and increase the risk of performance mismatches in high-volume manufacturing.

MARKET OPPORTUNITIES

Emerging Memory Technologies Create New CMP Material Requirements

Next-generation memory technologies including 3D NAND, MRAM, and FeRAM present significant growth opportunities for specialized CMP solutions. 3D NAND fabrication in particular requires innovative slurry formulations to handle the unique challenges of high-aspect-ratio structures and multi-material stacks. With 3D NAND layers exceeding 200 in cutting-edge devices, manufacturers demand slurries that can planarize complex oxide-nitride stacks while maintaining critical dimension control. The memory segment now accounts for over 25% of total CMP material consumption, with this share expected to grow as layer counts increase and new memory types enter volume production.

Additionally, the integration of novel materials into semiconductor manufacturing opens new avenues for CMP innovation. The introduction of ruthenium, cobalt, and 2D materials like graphene in advanced interconnects requires corresponding developments in CMP technology. Manufacturers that can rapidly develop compatible slurries and pads for these emerging materials will gain first-mover advantages in specialized market segments. The commercialization of materials previously limited to R&D settings creates a pipeline of opportunities for CMP material developers throughout the semiconductor technology roadmap.

SEMICONDUCTOR MATERIALS FOR CMP MARKET TRENDS

Transition to Advanced Nodes and Emerging Materials Driving CMP Innovation

The semiconductor industry’s relentless pursuit of smaller transistors and higher performance has created exponential demand for precision Chemical Mechanical Planarization (CMP) materials. As foundries transition to 3nm and 2nm process nodes, CMP slurry formulations require increasingly sophisticated abrasives with particle sizes below 50nm to achieve atomic-level surface uniformity. Simultaneously, the introduction of novel chip architectures like gate-all-around (GAA) transistors and complex interconnect stacks with low-k dielectrics necessitates customized CMP solutions that can handle delicate materials without inducing defects.

Other Trends

Consolidation Among Materials Suppliers

The $3.38 billion CMP materials market is witnessing strategic mergers as manufacturers seek to offer integrated solutions. Recent acquisitions, such as Fujifilm’s purchase of Entegris’ electronic chemicals business, have created vertically integrated suppliers capable of providing both slurries and pads. Meanwhile, established players like DuPont continue to dominate the CMP pad segment with 66% market share, leveraging their proprietary polyurethane formulations. This consolidation enables better compatibility between consumables, potentially reducing defect rates by up to 30% in advanced node manufacturing.

Sustainability Initiatives Reshaping Material Development

Environmental regulations and cost pressures are accelerating the development of green CMP solutions. Manufacturers now prioritize slurries with lower heavy metal content and pads with extended lifespans – some next-generation products achieve 20-25% longer service life through advanced conditioning technologies. The industry is also adopting closed-loop recycling systems that recover and repurpose up to 90% of used slurry, significantly reducing wastewater treatment costs. These sustainability measures are becoming key differentiators as fabs aim to meet stringent ESG targets while maintaining profitability.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Consolidate Positions Through Technological Innovation and Strategic Alliances

The semiconductor materials for CMP market features a highly concentrated competitive environment dominated by specialized chemical and materials science companies. Fujifilm has emerged as the undisputed leader in CMP slurries following its strategic acquisition of Entegris’ electronic chemicals business, controlling approximately 23% of the global slurry market share in 2023. This positions the company ahead of traditional competitors like Resonac and Fujimi Incorporated, both of whom maintain strong positions in the copper and tungsten slurry segments respectively.

In the CMP pads segment, DuPont maintains market leadership with over 66% share, leveraging its proprietary polyurethane formulations and extensive R&D capabilities. Their dominance is increasingly challenged by Asian players such as Fujibo Group and Hubei Dinglong, who are gaining traction through cost-competitive offerings tailored for 300mm wafer applications.

The ancillary equipment market presents a different dynamic, with 3M and Kinik Company controlling nearly half of the global CMP pad conditioner market. Their diamond-disc conditioning technologies have become industry standards for maintaining pad performance. Meanwhile, Entegris and Pall Corporation effectively monopolize the critical slurry filtration segment through patented membrane technologies that reduce defect counts in advanced node manufacturing.

Recent market developments highlight intense R&D focus on novel abrasive formulations for next-generation materials like cobalt and ruthenium. Merck KGaA has notably expanded its Versum Materials portfolio with low-defect slurries for 3D NAND applications, while JSR Corporation is pioneering colloidal silica solutions for gate-all-around transistor architectures. Such innovations are critical as the industry transitions to sub-3nm process nodes requiring unprecedented planarization precision.

List of Key Semiconductor CMP Materials Companies Profiled

- Fujifilm Holdings (Japan)

- Resonac Corporation (Japan)

- Fujimi Incorporated (Japan)

- DuPont de Nemours, Inc. (U.S.)

- Merck KGaA (Germany)

- AGC Inc. (Japan)

- KC Tech (South Korea)

- JSR Corporation (Japan)

- Anjimirco Shanghai (China)

- 3M Company (U.S.)

- Entegris, Inc. (U.S.)

- Pall Corporation (U.S.)

- Kinik Company (Taiwan)

- Fujibo Holdings (Japan)

- Hubei Dinglong (China)

Segment Analysis:

By Type

CMP Slurry Segment Dominates Due to Critical Role in Wafer Planarization

The market is segmented based on type into:

- CMP Slurry

- CMP Pads

- CMP Pad Conditioners

- CMP POU Slurry Filters

- CMP PVA Brushes

- CMP Retaining Rings

By Application

300mm Wafers Application Leads Due to Industry Shift Towards Larger Diameter Wafers

The market is segmented based on application into:

- 300mm Wafers

- 200mm Wafers

- Others

By End User

Foundries Segment Dominates Due to High Volume Semiconductor Manufacturing

The market is segmented based on end user into:

- Foundries

- IDMs (Integrated Device Manufacturers)

- OSAT (Outsourced Semiconductor Assembly and Test)

- Research Institutes

By Technology Node

Advanced Nodes Below 10nm Drive Demand for Precision CMP Materials

The market is segmented based on technology node into:

- Below 10nm

- 10-20nm

- 20-45nm

- Above 45nm

Regional Analysis: Semiconductor Materials for CMP Market

North America

The North American semiconductor materials for CMP market benefits from robust investment in advanced semiconductor manufacturing and strong R&D capabilities. The U.S. leads the region due to its dominant position in chip fabrication, with key players such as DuPont and Entegris headquartered here. The CHIPS and Science Act, allocating $52 billion for semiconductor research and production, is accelerating demand for high-performance CMP slurries and pads. Technological advancements in wafer fabrication processes, particularly for 300mm wafers, drive the need for precision polishing materials. However, stringent environmental regulations on chemical usage create both challenges and opportunities for sustainable material innovation.

Europe

Europe’s CMP materials market maintains steady growth through specialized chemical expertise and precision engineering capabilities. Germany and France are key manufacturing hubs, with companies like Merck KGaA developing advanced slurries for cutting-edge nodes. The region’s focus on environmental sustainability promotes water-based and low-defect slurry formulations. EU semiconductor sovereignty initiatives, including the European Chips Act’s €43 billion investment, are expected to boost local demand. However, higher production costs compared to Asian competitors and dependence on imported raw materials present ongoing challenges for regional suppliers.

Asia-Pacific

Asia-Pacific dominates the global CMP materials market, accounting for over 60% of consumption, driven by concentrated semiconductor fabrication in Taiwan, South Korea, and China. Taiwan’s TSMC and South Korea’s Samsung create massive demand for advanced slurry and pad solutions, particularly for sub-7nm processes. China’s aggressive semiconductor self-sufficiency push has spurred domestic material development, though quality gaps remain versus international competitors. Japan maintains strong positions in high-end slurries through companies like Fujimi and AGC. The region benefits from established supply chain ecosystems but faces increasing pressure to develop environmentally sustainable solutions amid tightening regulations.

South America

South America represents a developing market with limited but growing semiconductor manufacturing presence, primarily in Brazil. The region currently depends heavily on imported CMP materials due to limited local production capabilities. Emerging technology parks in São Paulo and tax incentives for electronics manufacturing create potential demand growth. However, infrastructure limitations, inconsistent regulatory frameworks, and economic instability have slowed widespread adoption of advanced CMP solutions. Most regional demand comes from secondary applications rather than leading-edge node production.

Middle East & Africa

The MEA region shows nascent but promising growth potential in semiconductor materials, particularly through strategic diversification efforts in the Gulf states. Saudi Arabia’s Vision 2030 includes plans for tech manufacturing expansion, while Israel’s strong tech sector creates specialized demand. Partnerships with global CMP material suppliers are increasing as the region builds its semiconductor ecosystem. Currently, the market remains limited by small-scale production facilities and lack of domestic material suppliers, requiring nearly all advanced CMP products to be imported. Long-term growth will depend on sustained infrastructure investment and workforce development.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor Materials for CMP (Chemical Mechanical Planarization) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Semiconductor Materials for CMP market was valued at USD 3,380 million in 2024 and is projected to reach USD 5,459 million by 2032, growing at a CAGR of 7.3% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (CMP Slurry, CMP Pads, Pad Conditioners, Filters, Brushes, Retaining Rings), wafer size (300mm, 200mm, others), and end-use applications to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with particular focus on semiconductor manufacturing hubs like Taiwan, South Korea, Japan, and China.

- Competitive Landscape: Profiles of leading market participants including Fujifilm, DuPont, Merck KGaA, Entegris, 3M, and Pall, covering their product portfolios, market shares, R&D investments, and strategic moves like Fujifilm’s acquisition of Entegris’ electronic chemicals business.

- Technology Trends & Innovation: Assessment of advanced CMP slurry formulations, next-generation pad materials, and the integration of Industry 4.0 technologies in CMP processes to improve yield and reduce defects.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing semiconductor demand, advanced node transitions) along with challenges (material costs, supply chain complexities, and geopolitical factors).

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, material suppliers, equipment vendors, and investors regarding technology roadmaps and emerging opportunities in the CMP ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from semiconductor industry associations, and analysis of financial reports from key market players to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Materials for CMP Market?

-> Semiconductor Materials for CMP Market was valued at 3380 million in 2024 and is projected to reach US$ 5459 million by 2032, at a CAGR of 7.3% during the forecast period.

Which key companies operate in Global Semiconductor Materials for CMP Market?

-> Key players include Fujifilm, DuPont, Merck KGaA, Entegris, 3M, Pall, Resonac, Fujimi Incorporated, and AGC, among others. The top 8 slurry suppliers control about 77% of the market.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor production, transition to advanced nodes (below 7nm), and rising demand for 300mm wafers.

Which region dominates the market?

-> Asia-Pacific dominates the market due to concentration of semiconductor fabs in Taiwan, South Korea, and China, accounting for over 60% of global demand.

What are the emerging trends?

-> Emerging trends include development of cobalt and ruthenium CMP slurries for advanced nodes, eco-friendly formulations, and smart conditioning technologies to improve process control.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...