Self-illuminated Display Panel Market Insights

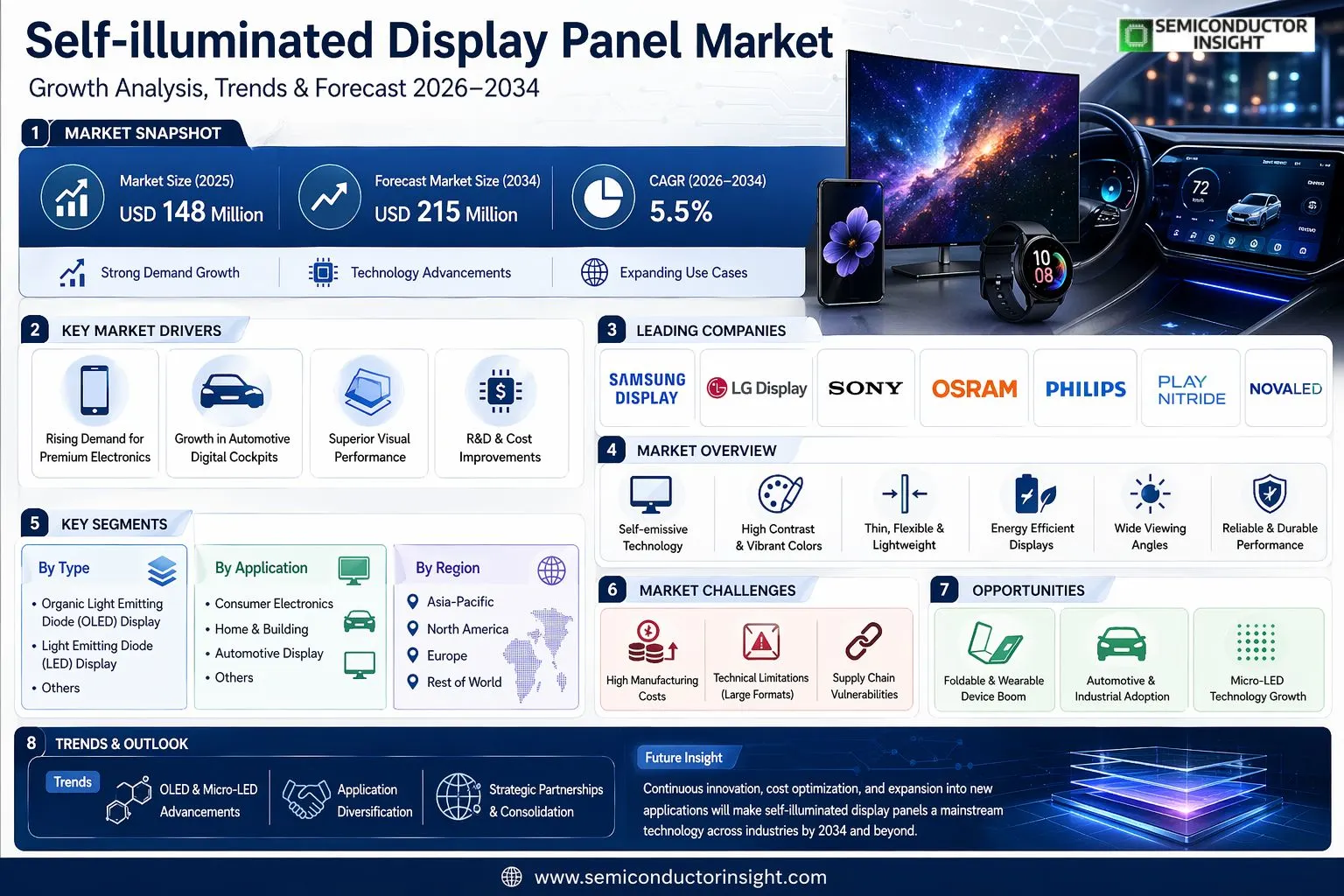

Global Self-illuminated Display Panel market size was valued at USD 148 million in 2025. The market is projected to grow from USD 156 million in 2026 to USD 215 million by 2034, exhibiting a CAGR of 5.5% during the forecast period.

Self-illuminated display panels are a display technology that does not require a backlight and is able to display images or text by emitting its own light. Unlike traditional liquid crystal display (LCD) panels, which require a backlight to illuminate the screen, self-luminous panels emit light directly through self-luminous materials such as organic light-emitting diodes (OLEDs) or quantum dots. This technology enables superior contrast ratios, wider viewing angles, and thinner form factors.

The market is experiencing steady growth due to several factors, including increasing adoption in premium consumer electronics like smartphones and televisions, where OLED displays are now standard for high-end models. Furthermore, the expansion into automotive displays for digital dashboards and infotainment systems is a significant driver because of the technology’s flexibility and durability. However, challenges such as higher production costs compared to LCDs and concerns regarding long-term burn-in for static images persist. Initiatives by key players are also expected to fuel market growth. For instance, major manufacturers like Samsung Display and LG Display continue to invest heavily in next-generation OLED and micro-LED technologies to improve efficiency and reduce costs. Samsung Electronics Co., Ltd., Sony Corporation, LG Display Co., Ltd., and Osram Licht AG are some of the key players that operate in the market with a wide range of portfolios.

MARKET DRIVERS

Proliferation of High-End Consumer Electronics

The primary growth engine for Self-illuminated Display Panel Market is the relentless demand for superior visual experiences in smartphones, tablets, and laptops. As consumers prioritize vibrant colors, deep blacks, and energy efficiency, manufacturers are rapidly adopting OLED and Micro-LED technologies. These panels, which emit their own light, are critical for enabling the sleek, flexible form factors and always-on display features now expected in premium devices.

Automotive Industry’s Shift to Digital Cockpits

The transformation of vehicle interiors into digital experiences creates substantial demand. Self-illuminated display panels are essential for advanced infotainment systems, digital instrument clusters, and head-up displays due to their high contrast, wide viewing angles, and fast response times. The trend towards electric and autonomous vehicles, which emphasize futuristic, integrated interiors, further accelerates this adoption.

➤ Analyst Perspective: The market is being reshaped by the convergence of superior performance and novel form factors, pushing self-illuminated technology beyond niche applications into mass-market consumer and automotive domains.

Furthermore, rising investments in next-generation display R&D are lowering production costs and improving yields for technologies like QD-OLED, making them more competitive against traditional LCDs and driving market expansion.

MARKET CHALLENGES

High Manufacturing Cost and Complexity

Despite technological advances, the production of self-illuminated display panels, particularly for larger formats and cutting-edge Micro-LEDs, remains expensive and complex. The precision required for depositing organic materials or assembling millions of microscopic LEDs leads to lower yields compared to mature LCD manufacturing, directly impacting final product pricing and market penetration.

Other Challenges

Technical Limitations for Large Formats

Scaling up production for large-area applications, such as televisions and public signage, presents significant hurdles. Issues like pixel uniformity, luminance degradation over time for OLEDs, and the monumental transfer processes for Micro-LEDs act as bottlenecks for widespread adoption in these segments.

Intense Competition and Rapid Technological Obsolescence

The market is characterized by fierce competition and rapid innovation cycles. Manufacturers face constant pressure to invest in new fabrication lines and R&D to keep pace. This environment creates financial strain and risks of inventory becoming obsolete quickly, challenging the profitability of market players.

MARKET RESTRAINTS

Durability Concerns and Product Lifespan

A key restraint for Self-illuminated Display Panel Market is the potential for burn-in and luminance decay over time, especially in OLED displays. This phenomenon, where static images leave a permanent ghost trace, undermines consumer confidence for certain professional and high-static-content applications. While improvements are ongoing, this perception issue slows adoption in markets where long-term reliability and screen integrity are paramount.

Supply Chain Vulnerabilities

Global supply chain for advanced materials and precision manufacturing equipment is concentrated and susceptible to disruptions. Dependencies on specific chemical compounds, rare earth elements, and specialized machinery from a limited number of suppliers can lead to production delays and cost volatility, restraining steady market growth.

MARKET OPPORTUNITIES

Explosion in Wearable and Foldable Devices

burgeoning market for wearables like smartwatches and AR/VR headsets, alongside the innovation in foldable and rollable smartphones, presents a major opportunity. Self-illuminated display panels are uniquely suited for these applications due to their flexibility, thinness, and ability to be manufactured on plastic substrates, enabling entirely new product designs and user experiences.

Adoption in Industrial and Medical Sectors

Beyond consumer electronics, there is significant growth potential in specialized sectors. The high contrast, readability in various lighting conditions, and design flexibility of self-illuminated panels make them ideal for medical monitoring equipment, industrial control interfaces, and professional aviation displays, where performance and reliability are critical.

Advancements in Micro-LED Technology

The ongoing commercialization of Micro-LED technology represents a transformative opportunity. By combining the best attributes of OLED and traditional LED, Micro-LEDs offer superior brightness, longevity, and energy efficiency. Breakthroughs in mass transfer and repair techniques could unlock cost-effective production, propelling the next major growth wave for Self-illuminated Display Panel Market.

Self-illuminated Display Panel Market Trends

Advancements in OLED Technology Accelerate Market Maturation

Self-illuminated Display Panel Market is witnessing a pivotal phase dominated by rapid technological refinement, primarily within the Organic Light Emitting Diode (OLED) segment. This core technology’s ability to deliver superior contrast ratios, deeper blacks, and more vibrant colors without a backlight aligns perfectly with consumer demand for high-fidelity visual experiences. Continuous improvements in the longevity of organic materials and manufacturing yield efficiencies are directly reducing production costs, making these panels more viable for a broader range of applications. The market trend is characterized by manufacturers investing heavily in next-generation production lines to scale capacity for larger panel sizes and more complex form factors.

Other Trends

Application Diversification Beyond Consumer Electronics

While consumer electronics remain the dominant application, a significant trend in Self-illuminated Display Panel Market is its expansion into new sectors. Automotive display systems are integrating these panels for digital dashboards and entertainment consoles, valuing their flexibility and superior readability. Similarly, the home and building segment is adopting them for ambient lighting solutions and architectural displays where thinness and design integration are key. This diversification reduces market reliance on the volatile consumer electronics cycle and creates stable, long-term revenue channels for key manufacturers.

Consolidation and Strategic Alliances Among Key Players

The competitive landscape is trending towards strategic consolidation and partnerships. Leading companies in Self-illuminated Display Panel Market, including Samsung, LG Display, and Sony, are forming technology alliances and engaging in vertical integration to secure supply chains for critical materials. Simultaneously, the rise of specialized manufacturers focusing on micro-LED and quantum dot enhancements is fostering a more segmented ecosystem. This activity is driven by the need to share the immense capital burden of R&D and production facility upgrades, shaping a market where collaboration is as crucial as competition.

Regional Production Hubs and Supply Chain Realignment

A clear trend involves the geographical shifting of manufacturing and supply networks. Asia-Pacific, led by South Korea, China, and Japan, continues to be the epicenter of production for Self-illuminated Display Panel Market. However, recent global supply chain assessments are prompting some companies to establish auxiliary production or advanced assembly facilities in North America and Europe. This realignment aims to mitigate logistical risks and cater to regional demand more responsively, particularly for the automotive and specialized industrial sectors, indicating a move towards more resilient and regionally focused supply strategies.

COMPETITIVE LANDSCAPE

Key Industry Players

A Concentrated Market Led by Display and Lighting Giants

Self-illuminated Display Panel Market is characterized by a high degree of concentration, with the top five global manufacturers by revenue holding a significant collective share. Market leadership is firmly anchored by established electronics and semiconductor titans, with Samsung and LG Display representing dominant forces, particularly in the high-volume Organic Light Emitting Diode (OLED) segment for consumer electronics and automotive displays. These leaders leverage immense scale, vertical integration, and continual R&D investment in next-generation display technologies to maintain their competitive edge. Their strategic focus extends across smartphones, televisions, and increasingly, large-format digital signage, setting the technological and pricing benchmarks for the industry.

Beyond the dominant players, the competitive landscape includes several significant niche and specialized manufacturers that drive innovation in specific applications and emerging technologies. Companies like Osram and Philips bring deep expertise in advanced lighting solutions to the market, influencing the home & building and specialized industrial display segments. Meanwhile, technology innovators such as Play Nitride (focusing on micro-LED), Novaled (specializing in OLED materials and technology), and Aledia (developing nanowire LED technology) are critical to the long-term evolution of the market, pushing the boundaries of efficiency, resolution, and form factors. These players often engage in strategic partnerships or serve as key suppliers to the larger integrators.

List of Key Self-illuminated Display Panel Companies Profiled

- Samsung

- LG Display

- Sony

- Osram

- Philips

- Acuity Brands

- Play Nitride

- eLUX

- Novaled

- Aledia

- Panasonic

- Newhaven Display International

- Shenzhen TCL

- Taiwan AUO Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Organic Light Emitting Diode (OLED) Display is the leading technology segment, defined by its premium performance characteristics and broad applicability.

|

| By Application |

|

Consumer Electronics remains the dominant and most dynamic application segment, serving as the primary driver for technological advancements.

|

| By End User |

|

Individual Consumers represent the core end-user group, driving market trends through purchasing preferences and demand for enhanced visual media.

|

| By Technology Maturity |

|

Growth/Emerging technologies represent the most strategic and active segment, characterized by rapid evolution and significant future potential.

|

| By Display Performance Tier |

|

Premium/Flagship tier is the critical segment for establishing brand leadership and driving overall market innovation forward.

|

Regional Analysis: Self-illuminated Display Panel Market

Asia-Pacific

South Korea is the undisputed technology powerhouse, home to global giants that dominate OLED intellectual property and mass production. These firms drive Self-illuminated Display Panel Market forward with substantial R&D focused on foldable, transparent, and ultra-high-resolution panels, setting global performance benchmarks.

China leverages immense state-backed investment and scale to become a manufacturing juggernaut. The country is rapidly closing the technology gap, building vast production capacity for both OLED and next-generation microLED panels to supply its domestic device manufacturers and export markets competitively.

Japan maintains a critical role through its mastery of advanced materials, precision manufacturing equipment, and key component supply. Japanese firms are pivotal in developing the materials science behind high-efficiency, long-life OLED emitters and the sophisticated machinery required for microLED assembly.

This sub-region represents the high-growth frontier for Self-illuminated Display Panel Market, driven by rapidly expanding consumer electronics demand and increasing local assembly of devices. It is becoming a vital consumption hub and an emerging location for secondary manufacturing and supply chain operations.

North America

North America is a primary driver of innovation and premium demand within Self-illuminated Display Panel Market. The region’s influence stems from its concentration of leading technology firms that design and market flagship smartphones, laptops, and wearables, which are major adoption channels for advanced OLED displays. Furthermore, North American automotive manufacturers and Silicon Valley tech companies are at the forefront of integrating these panels into next-generation vehicle dashboards, AR/VR headsets, and smart retail solutions. High consumer purchasing power and a culture of early technology adoption ensure strong market pull for the latest display innovations, making it a critical region for high-margin, cutting-edge product launches.

Europe

Europe holds a significant position characterized by strong demand in automotive and high-end consumer applications. German and French automakers are leading integrators of sophisticated self-illuminated displays for digital cockpits and infotainment systems, emphasizing quality and design excellence. The region also has a robust market for premium televisions and monitors, where OLED technology is highly valued. European research institutes and companies contribute notably to materials research and niche applications in healthcare and professional signage. Stringent regulatory standards around energy efficiency also influence product development, pushing for more sustainable and power-efficient display panel solutions in the market.

South America

The South American market for self-illuminated display panels is in a growth phase, primarily fueled by the expanding consumer electronics segment. Increasing smartphone penetration and a growing middle class are creating demand for devices featuring newer display technologies, though adoption often lags behind global leaders due to economic volatility and price sensitivity. The aftermarket automotive sector also presents opportunities for display upgrades. Market growth is uneven, with Brazil being the most significant national market. Overall, the region represents an emerging opportunity where affordability and localized supply chains will be key to deeper market penetration for display panel technologies.

Middle East & Africa

This diverse region shows varied adoption patterns for self-illuminated display panels. Wealthier Gulf nations exhibit strong demand for luxury goods, including high-end OLED televisions and premium vehicles with advanced digital displays, driven by high disposable incomes. In contrast, broader African markets are price-sensitive, with growth centered on affordable smartphones and basic consumer electronics, which gradually incorporates more modern display technology. The commercial sector, including retail and hospitality in urban centers, is adopting digital signage solutions. The region’s overall market dynamics are shaped by economic disparity, making it a landscape of niche high-end demand alongside volume-driven, entry-level growth.

Report Scope

This market research report provides a comprehensive analysis of the Self-illuminated Display Panel Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

-

Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Self-illuminated Display Panel Market?

-> Global Self-illuminated Display Panel Market was valued at USD 148 million in 2025 and is projected to reach USD 215 million by 2034, growing at a CAGR of 5.5% during the forecast period.

Which key companies operate in Self-illuminated Display Panel Market?

-> Key players include Osram, Samsung, Sony, Philips, Acuity Brands, LG Display, Play Nitride, eLUX, Novaled, and Aledia, among others.

What are the key growth drivers?

-> Key growth drivers include demand for high-quality displays in consumer electronics, automotive displays, and the superior visual performance of self-illuminated technologies like OLED.

Which region dominates the market?

-> While specific regional market sizes are estimated, key markets include the U.S. and China, with Asia being a significant region in terms of manufacturing, consumption, and growth potential.

What are the emerging trends?

-> Emerging trends include advancements in Organic Light Emitting Diode (OLED) and quantum dot display technologies, integration into flexible and foldable devices, and increasing adoption in automotive and home & building applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...