Satellite Communication Market Insights

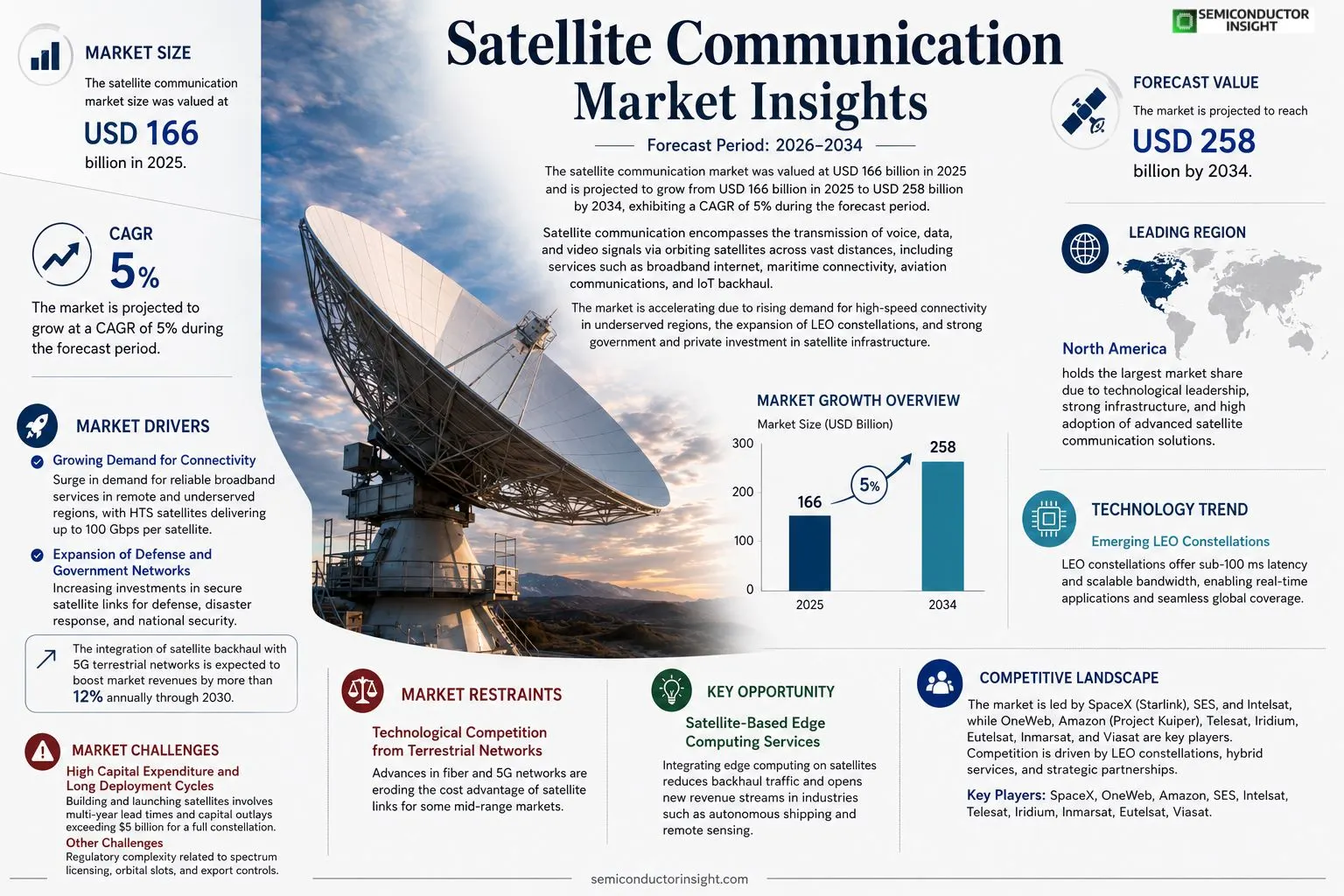

Satellite communication market size was valued at USD 166 billion in 2025. The market is projected to grow from USD 166 billion in 2025 to USD 258 billion by 2034, exhibiting a CAGR of 5 % during the forecast period.

Satellite communication encompasses the transmission of voice, data, and video signals via orbiting satellites that relay information between ground stations across vast distances. It includes services such as broadband internet, maritime connectivity, aviation communications, and IoT backhaul, leveraging geostationary (GEO), medium Earth orbit (MEO), and low Earth orbit (LEO) platforms.The market is accelerating because demand for high‑speed connectivity in underserved regions is rising, while LEO constellations expand capacity and reduce latency; meanwhile, government initiatives and private investments are fueling infrastructure upgrades.

MARKET DRIVERS

Growing Demand for Connectivity

Satellite Communication Market is being propelled by the surge in demand for reliable broadband services in remote and underserved regions. Operators are deploying high‑throughput satellites (HTS) that can deliver up to 100 Gbps per satellite, enabling cost‑effective internet access for maritime, aviation, and rural land sectors.

Expansion of Defense and Government Networks

Governments worldwide are increasing budget allocations for secure satellite links to support defense communications, disaster response, and national security. This investment drives the development of resilient, low‑latency constellations that can operate in contested environments.

➤ The integration of satellite backhaul with 5G terrestrial networks is expected to boost market revenues by more than 12% annually through 2030.

Additionally, the rise of IoT devices requiring ubiquitous coverage is encouraging satellite operators to launch next‑generation constellations, further strengthening the market trajectory.

MARKET CHALLENGES

High Capital Expenditure and Long Deployment Cycles

Building and launching satellites involves multi‑year lead times and capital outlays that can exceed $5 billion for a full constellation, creating financial pressure on manufacturers and service providers.

Other Challenges

Regulatory Complexity

Spectrum licensing, orbital slot allocation, and export‑control restrictions vary across jurisdictions, complicating rollout strategies and increasing compliance costs.

MARKET RESTRAINTS

Technological Competition from Terrestrial Networks

Advances in fiber‑optic infrastructure and the rapid expansion of 5G networks are eroding the cost advantage of satellite links for some mid‑range markets. While satellites excel in coverage, the lower latency of terrestrial solutions can limit adoption for latency‑sensitive applications.

MARKET OPPORTUNITIES

Emerging Low‑Earth Orbit (LEO) Constellations

The deployment of LEO constellations presents a significant growth avenue, offering sub‑100 ms latency and scalable bandwidth. Companies launching hundreds of small satellites are positioning themselves to capture enterprise and consumer segments that demand near‑real‑time connectivity.

Satellite‑Based Edge Computing Services

Integrating edge computing capabilities on satellite platforms enables data processing closer to the source, reducing backhaul traffic and opening new revenue streams in data‑intensive industries such as autonomous shipping and remote sensing.

Satellite Communication Market Trends

Growing Demand for High‑Speed Connectivity

Satellite Communication Market is experiencing a notable shift as enterprises and consumers alike seek reliable broadband in remote and underserved locations. Network operators are leveraging both geostationary and non‑geostationary platforms to extend coverage into rural areas where terrestrial fiber is cost‑prohibitive. This expansion is driven by increased adoption of cloud‑based services, remote work requirements, and the rising importance of real‑time data for agricultural and mining operations. As a result, service providers are prioritizing scalable architectures that can deliver consistent latency while supporting higher throughput demands.

Other Trends

Expansion of LEO Constellations

Low‑Earth‑Orbit satellites are reshaping Satellite Communication Market by delivering lower latency and broader capacity compared with traditional geostationary systems. Operators are deploying dense constellations that enable seamless hand‑off between satellites, creating a more continuous user experience for mobile and IoT applications. This architecture supports emerging use cases such as autonomous vessel tracking, in‑flight entertainment, and edge computing for disaster response. The modular nature of LEO platforms also allows rapid iteration, encouraging private investment and encouraging partnerships with regional regulators to secure spectrum allocations.

Integration of Satellite Services with 5G Networks

A parallel trend sees satellite backhaul becoming a cornerstone of 5G rollout strategies. By complementing terrestrial base stations, satellite links provide redundancy and extend coverage to densely populated urban zones where underground infrastructure limits fiber deployment. This synergy enhances network resilience, enables new business models for mobile virtual network operators, and supports massive machine‑type communications essential for smart city initiatives. Government programs are further incentivizing the joint deployment of satellite and 5G assets, positioning Satellite Communication Market as a critical enabler of next‑generation connectivity.

COMPETITIVE LANDSCAPEKey Industry Players

Satellite Communication Market Competitive Landscape

Satellite Communication Market is anchored by a handful of vertically integrated operators that own extensive GEO and emerging LEO fleets. SpaceX’s Starlink constellation, with several thousand LEO satellites, dominates the high‑throughput broadband segment and forces traditional GEO providers such as SES and Intelsat to accelerate constellation development and hybrid service offerings. These incumbents command the majority of enterprise and governmental traffic, while also leveraging strategic partnerships to broaden coverage across maritime, aviation and IoT backhaul. The overall market structure reflects a dual‑track dynamic: entrenched GEO operators sustain legacy services, whereas agile LEO entrants capture rapid‑deployment demand, together driving the projected growth from US$166 billion in 2025 to US$258 billion by 2034.Beyond the dominant trio, a diverse set of niche players enriches the competitive fabric. OneWeb and Amazon’s Project Kuiper are rapidly expanding LEO constellations aimed at underserved regions. Telesat’s Lightspeed and Iridium’s LEO network target specialized verticals such as aerospace and critical communications. European operators Eutelsat and Inmarsat remain strong in maritime and aeronautical services, while Viasat focuses on fiber‑backed satellite broadband for residential markets. Aerospace manufacturers including Thales Alenia Space, Boeing, and Lockheed Martin supply next‑generation payloads, reinforcing an ecosystem where hardware, service, and network design intersect to shape market differentiation.

List of Key Satellite Communication Companies Profiled

- SpaceX

- OneWeb

- Amazon (Project Kuiper)

- SES

- Intelsat

- Telesat

- Iridium Communications

- Inmarsat

- Eutelsat

- Viasat

- Thales Alenia Space

- Boeing

- Lockheed Martin

- ViaSat

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Low Earth Orbit (LEO) is emerging as the leading segment because it delivers markedly lower latency and higher bandwidth density.

|

| By Application |

|

Broadband Internet drives the market narrative as the primary service channel, shaping network architecture and investment focus.

|

| By End User |

|

Enterprise/Industrial stands out as the leading end‑user segment, reflecting the strategic role of satellite connectivity in mission‑critical operations.

|

| By Service Type |

|

Data Services dominate the service landscape, underpinning the growth of high‑throughput satellite applications.

|

| By Deployment Model |

|

Hybrid Solutions are increasingly recognized as the leading deployment model, merging the stability of fixed stations with the flexibility of mobile terminals.

|

Regional Analysis: North America

United States

The government and defense sectors represent a substantial portion of Satellite Communication Market in the United States. This segment focuses on secure communications, intelligence gathering, and military operations. The demand for resilient and high-bandwidth satellite networks for critical infrastructure protection and national security initiatives continues to drive innovation and investment.

The expansion of broadband access, particularly in rural and remote areas, is a key growth driver for Satellite Communication Market in the US. Satellite internet services offer a viable alternative to traditional terrestrial broadband, bridging the digital divide and enabling connectivity for underserved populations. The increasing demand for high-speed internet for both residential and commercial users fuels the adoption of satellite broadband solutions.

The proliferation of IoT devices and Machine-to-Machine (M2M) communication is creating significant demand for satellite connectivity. Applications range from asset tracking and monitoring to remote environmental sensing and industrial automation. Secure and reliable satellite networks are crucial for enabling data transmission from remote locations where terrestrial connectivity is unavailable.

Businesses across various sectors are leveraging satellite communication for a range of applications, including data backup and disaster recovery, remote office connectivity, and maritime and aviation communications. The need for reliable and secure communication solutions in challenging environments drives demand for satellite services among enterprises.

Europe

Europe presents a mature and diversified satellite communication market, with a strong emphasis on technological innovation and regulatory harmonization. The region benefits from a well-established infrastructure and a high level of technological expertise. Key applications driving growth include broadband access, maritime communications, and government services. The development of high-throughput satellites (HTS) is enabling increased bandwidth and improved service quality. Europe’s focus on sustainability and environmental regulations is also influencing the development of more energy-efficient satellite technologies. The increasing demand for secure communications across various sectors, including defense and critical infrastructure, further contributes to market growth. The region is actively exploring opportunities in areas such as satellite-based IoT and precision agriculture.

Asia-Pacific

The Asia-Pacific region is emerging as the fastest-growing market for satellite communication, driven by rapid economic development and increasing demand for connectivity. The growth is particularly strong in countries like India, China, and Southeast Asia. Key applications include broadband access, mobile backhaul, and government services. The increasing adoption of 5G technology is creating new opportunities for satellite backhaul solutions. Government initiatives promoting digital inclusion and infrastructure development are also fueling market growth. The proliferation of IoT devices and the growth of e-commerce are further driving demand for satellite connectivity. Geopolitical factors and regional collaborations are also influencing the development of Satellite Communication Market in the Asia-Pacific region.

South America

South America presents a promising market for satellite communication, with significant potential for growth in broadband access and rural connectivity. The region’s vast geographical size and challenging terrain make satellite communication a viable option for providing connectivity to underserved areas. The demand for satellite-based IoT solutions is also increasing, driven by applications in agriculture, mining, and logistics. Government initiatives aimed at expanding broadband access and promoting digital inclusion are supporting market growth. The increasing adoption of satellite imagery for applications such as environmental monitoring and disaster management is also contributing to market demand.

Middle East & Africa

The Middle East and Africa represent dynamic markets for satellite communication, with growing demand for broadband access, mobile backhaul, and government services. The region is witnessing significant investments in satellite infrastructure to address the digital divide and support economic development. The increasing adoption of 5G technology and the growth of IoT applications are driving market growth. Government initiatives promoting digital transformation and infrastructure development are also fueling demand for satellite services. The region’s strategic location and growing connectivity needs make it an attractive market for satellite operators.

Report Scope

This market research report provides a comprehensive analysis of the Satellite Communication Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Satellite Communication Market?

-> Satellite Communication Market was valued at USD 166 billion in 2025 and is expected to reach USD 258 billion by 2034.

Which key companies operate in Satellite Communication Market?

-> Key players include SpaceX, OneWeb, SES, Eutelsat, Iridium, Inmarsat, Telesat, and Viasat.

What are the key growth drivers?

-> Key growth drivers include rising demand for high‑speed connectivity in underserved regions, deployment of LEO satellite constellations, and increasing government and private investment in satellite infrastructure.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia‑Pacific is the fastest‑growing region.

What are the emerging trends?

-> Emerging trends include LEO mega‑constellations, satellite‑based broadband for 5G backhaul, and integration of IoT and AI for network optimization.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...