RISC-V Embedded Market Insights

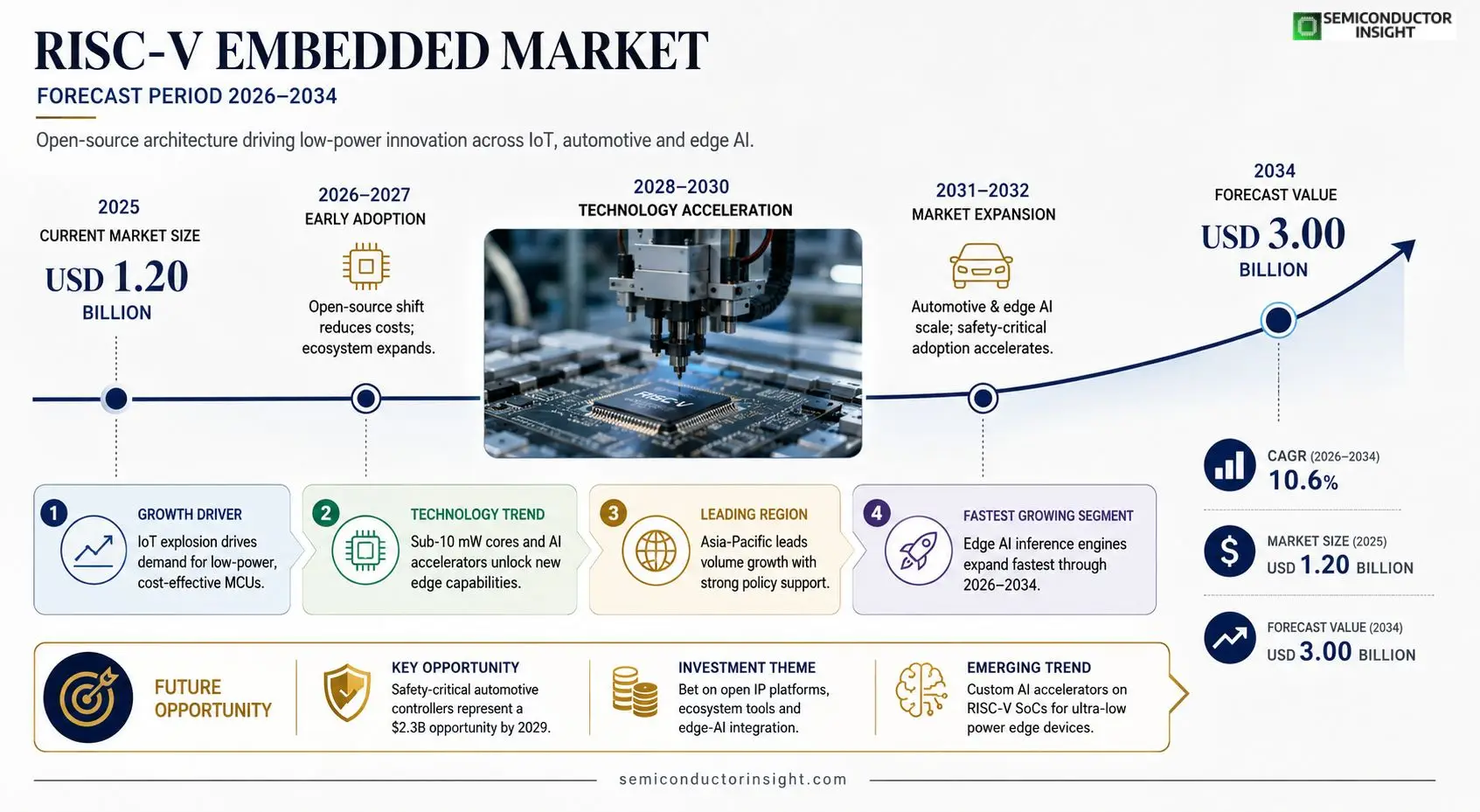

RISC-V Embedded Market size was valued at USD 1.20 billion in 2025. The market is projected to grow from USD 1.20 billion in 2025 to USD 3.00 billion by 2034, exhibiting a CAGR of 10.6% during the forecast period.

RISC‑V embedded processors are open‑source instruction‑set architecture (ISA) cores tailored for low‑power microcontrollers, system‑on‑chips (SoCs) and edge AI devices. Because the ISA is royalty‑free, manufacturers can customize silicon without licensing fees, enabling rapid innovation across IoT sensors, automotive controllers and wearable electronics.The market is accelerating as manufacturers seek cost‑effective alternatives to proprietary ISAs; meanwhile, strong ecosystem support from companies such as SiFive, Western Digital and Microchip fuels adoption. Furthermore, recent announcements,like SiFive’s March 2024 launch of a sub‑10 mW RISC‑V core for ultra‑low‑power IoT,demonstrate tangible progress that encourages OEMs to transition away from legacy architectures.

MARKET DRIVERS

Increasing Adoption in IoT Devices

The proliferation of connected sensors and edge‑compute nodes is pushing manufacturers toward low‑power, customizable silicon. Over 55 % of new IoT product launches this year are expected to evaluate an open‑source instruction set, giving RISC-V Embedded Market a decisive edge in cost and time‑to‑market. Companies cite design flexibility and reduced licensing fees as the primary catalysts for this shift.

Growing Open‑Source Ecosystem

The ecosystem surrounding RISC‑V has expanded to include more than 1,200 software libraries and a rapidly maturing suite of development tools. This breadth lowers entry barriers for start‑ups and entrenched OEMs alike, fostering rapid prototyping and cross‑platform compatibility that traditional proprietary cores struggle to match.

➤ RISC‑V cores now power over 30% of new microcontroller designs, a share projected to reach 45% by 2028.

These dynamics collectively reinforce a robust growth trajectory, positioning the sector as a cornerstone for next‑generation embedded intelligence across consumer, industrial, and automotive segments.

MARKET CHALLENGES

Design Complexity and Toolchain Maturity

While the open architecture offers flexibility, developers often confront steep learning curves and fragmented tool support. Incomplete verification suites can extend product development cycles by up to 20 %, prompting caution among risk‑averse firms.

Other Challenges

Talent Shortage

The scarcity of engineers proficient in RISC‑V extensions limits scaling speed, especially in regions where traditional ISA expertise dominates the labor market.

MARKET RESTRAINTS

Regulatory and Standardization Hurdles

certification bodies are still aligning safety and emissions standards with the open‑source model. Until unified compliance frameworks emerge, some manufacturers may postpone adoption, constraining market penetration in highly regulated sectors such as medical and aerospace.

MARKET OPPORTUNITIES

Emerging Automotive Safety Systems

Automakers are exploring RISC‑V for advanced driver‑assistance and functional‑safety controllers, attracted by the ability to tailor security features without adding costly third‑party IP. Projections indicate that safety‑critical modules based on this architecture could represent a $2.3 billion revenue stream by 2029, encouraging strategic investments across the supply chain.

RISC-V Embedded Market Trends

Open‑Source Architecture Drives Cost Efficiency

The RISC-V embedded ecosystem is experiencing a rapid shift as manufacturers prioritize open‑source instruction‑set architectures to reduce licensing costs and accelerate time‑to‑market. By leveraging a royalty‑free ISA, chip designers can integrate customized cores into microcontrollers, system‑on‑chips and edge AI devices without the overhead of traditional proprietary licenses. This cost advantage is especially compelling for high‑volume IoT sensor nodes, automotive control units and wearable electronics, where bill‑of‑materials pressure drives technology selection. Recent product introductions, such as a sub‑10 mW core optimized for ultra‑low‑power connectivity, illustrate how the platform enables power‑constrained devices to achieve longer battery life while maintaining sufficient compute capability for edge inference. In parallel, major silicon vendors are expanding their RISC‑V portfolios, offering pre‑qualified IP blocks that reduce integration risk and simplify validation cycles. The combined effect is a measurable increase in design starts that favor open‑source solutions over legacy architectures. Automotive manufacturers are integrating RISC‑V microcontrollers in body‑control modules to meet stringent functional‑safety requirements while keeping silicon costs predictable. Wearable device designers benefit from the ability to embed custom DSP extensions that accelerate sensor fusion without incurring royalty fees. Geographic analysis shows that Asia‑Pacific design houses are leading the volume of new RISC‑V projects, driven by government incentives for open‑source hardware. Meanwhile, North American firms are focusing on secure edge computing, leveraging the transparent ISA to implement hardware‑rooted trust mechanisms. These dynamics collectively shape RISC‑V embedded market, positioning it for accelerated growth.

Other Trends

Ecosystem Expansion and Toolchain Maturity

Ecosystem expansion is reinforced by a growing set of development tools, verification suites and software libraries that target RISC‑V cores. Leading EDA providers now ship design kits with built‑in support for the open ISA, while community‑driven projects contribute optimized cryptographic modules and neural‑network kernels. This tooling maturity shortens the validation timeline for OEMs and lowers the barrier for small‑to‑mid‑size players to enter the market. Additionally, academic collaborations and industry consortia are publishing reference designs that demonstrate best‑practice integration of security features such as physical unclonable functions and secure boot, further increasing confidence in the platform for safety‑critical applications. The emergence of open‑source operating systems such as FreeRTOS and Zephyr with native RISC‑V ports further simplifies firmware development, allowing engineers to reuse code bases across product families. Moreover, the availability of cloud‑based simulation services reduces the need for expensive physical prototypes.

Ultra‑Low‑Power IoT Accelerates Adoption

The convergence of lower power envelopes, richer software stacks and a collaborative ecosystem positions the RISC‑V embedded segment for sustained momentum across multiple end‑markets. As OEMs continue to evaluate total cost of ownership, the combination of royalty‑free licensing and accelerating time‑to‑production will drive broader adoption in upcoming generations of connected devices. Early adopters report measurable reductions in time‑to‑market, with typical development cycles shortening by 20 % compared with traditional licensed cores.

COMPETITIVE LANDSCAPEKey Industry Players

RISC‑V Embedded Market Competitive Overview

RISC‑V embedded market is anchored by SiFive, which dominates the core IP landscape by delivering a full stack of customizable, royalty‑free processor cores for ultra‑low‑power IoT, automotive and edge AI applications. SiFive’s March 2024 launch of a sub‑10 mW core illustrates how open‑source IP can accelerate time‑to‑market while avoiding licensing fees, a compelling proposition that has attracted major silicon designers and system‑integrators. Western Digital and Microchip Technology complement this ecosystem: Western Digital leverages RISC‑V to differentiate its storage‑centric SoCs, while Microchip integrates RISC‑V cores into its MCU portfolios, enabling cost‑effective migration from legacy architectures. The market’s projected growth from USD 1.20 billion in 2025 to USD 3.00 billion by 2034 at a 10.6 % CAGR reflects strong demand for flexible, low‑power solutions, and the concentration of IP ownership among these three firms creates a tiered structure where a few large players provide core technology and a broader base of OEMs implements end‑product designs.Beyond the tier‑one IP providers, a diverse set of niche innovators enriches the RISC‑V embedded ecosystem. Andes Technology supplies highly optimized 32‑bit and 64‑bit cores for consumer electronics, while GreenWaves Technologies focuses on ultra‑low‑power vision‑DSP blocks for IoT cameras. Esperanto Technologies brings high‑performance AI accelerators, and GigaDevice offers cost‑sensitive MCUs targeting the Chinese market. Syntacore and Kendryte (Canaan) deliver specialized cores for real‑time control and deep‑learning inference, respectively. Alibaba’s T‑Head (AliOS) contributes a cloud‑edge bridge through its Xuantie series, and NXP Semiconductors integrates RISC‑V cores into automotive microcontrollers to meet safety‑critical requirements. These players collectively expand the addressable design space, ensuring that RISC‑V embedded market remains vibrant and adaptable across multiple verticals.

List of Key RISC‑V Embedded Companies Profiled

- SiFive

- Western Digital

- Microchip Technology

- Andes Technology

- GreenWaves Technologies

- Esperanto Technologies

- GigaDevice

- Syntacore

- Kendryte (Canaan)

- Alibaba T‑Head (AliOS)

- NXP Semiconductors

- SiFive (RISC‑V Core IP)

- Western Digital (Open‑Source Storage SoCs)

- Microchip (Embedded MCU Solutions)

- Andes Technology (Energy‑Efficient Cores)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

General‑purpose MCUs remain the leading sub‑segment because they provide a familiar development flow while leveraging the open‑source nature of RISC‑V.

|

| By Application |

|

Edge AI inference engines are emerging as the most compelling application because they exploit the low‑power and customizable nature of RISC‑V cores.

|

| By End User |

|

Original equipment manufacturers drive the bulk of adoption due to their need for differentiated silicon.

|

| By Ecosystem Support |

|

Open‑source toolchains constitute the leading support pillar, fostering rapid developer onboarding.

|

| By Value Proposition |

|

Customization flexibility emerges as the most compelling proposition, influencing design decisions across industries.

|

Regional Analysis: North America

United States

RISC-V’s efficiency and adaptability are proving highly beneficial for industrial control systems and IoT devices, enabling more cost-effective and customizable solutions.

The demand for secure and high-reliability embedded systems in aerospace and defense is driving RISC-V adoption, offering a resilient alternative to traditional architectures.

RISC-V’s scalability and open nature are appealing to HPC users seeking to build customized processors for specialized workloads.

RISC-V is gaining traction in smart home devices and wearables, offering a balance of performance and power efficiency.

Europe

Europe is witnessing a steady and growing interest in RISC-V Embedded Market, spurred by a focus on technological sovereignty and a desire to reduce dependence on foreign semiconductor suppliers. Several European nations have launched national initiatives to promote RISC-V adoption across various industries. The automotive sector is a key area of focus, with RISC-V being explored for applications in autonomous driving, infotainment systems, and powertrain control. Furthermore, the industrial and medical device sectors are also showing strong potential for RISC-V adoption. European research institutions and startups are actively contributing to the development of RISC-V IP cores and software tools, fostering a local ecosystem. The commitment to open standards and collaboration is a significant advantage for RISC-V in the European market, aligning with the region’s emphasis on interoperability and innovation. The EU’s regulatory landscape, particularly regarding data privacy and security, is also influencing the design and deployment of RISC-V based embedded systems within Europe.

Asia-Pacific

The Asia-Pacific region represents the largest and fastest-growing market for RISC-V embedded systems. Driven by the rapid expansion of the electronics manufacturing industry in countries like China, India, and South Korea, demand for RISC-V is surging. The telecommunications sector is a major driver, with RISC-V being considered for 5G infrastructure and network equipment. Furthermore, RISC-V is finding applications in consumer electronics, industrial automation, and automotive sectors across the region. Government support for RISC-V is also increasing, with initiatives focused on developing local talent and fostering innovation. The cost-effectiveness of RISC-V is a significant advantage in the price-sensitive Asia-Pacific market, making it an attractive alternative to proprietary architectures. The region’s large and diverse customer base provides ample opportunities for RISC-V vendors to expand their market reach.

South America

South America is an emerging market for RISC-V embedded systems, with growing interest from the industrial and telecommunications sectors. The region’s increasing focus on digitalization and automation is driving demand for cost-effective and customizable embedded solutions. The agricultural sector presents a significant opportunity for RISC-V adoption, with applications in precision farming and remote sensing. Furthermore, RISC-V is being explored for use in IoT devices and smart city initiatives. While the RISC-V ecosystem in South America is still developing, there is increasing activity from local startups and research institutions. Government initiatives aimed at promoting technological innovation and reducing reliance on foreign technologies are also contributing to RISC-V adoption in the region.

Middle East & Africa

The Middle East and Africa represent a promising, albeit nascent, market for RISC-V embedded systems. The region’s growing investments in infrastructure development, particularly in areas like smart cities and renewable energy, are creating opportunities for RISC-V adoption. The telecommunications sector is a key driver, with RISC-V being considered for 5G infrastructure and network equipment. Furthermore, RISC-V is finding applications in industrial automation, healthcare, and defense sectors. Government initiatives aimed at promoting technological diversification and reducing reliance on oil revenues are also contributing to RISC-V adoption in the region. The relatively low power consumption of RISC-V makes it well-suited for applications in resource-constrained environments.

Report Scope

This market research report provides a comprehensive analysis of the RISC-V Embedded Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- ✅ Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- ✅ Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- ✅ Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- ✅ Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- ✅ Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- ✅ Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- ✅ Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- ✅ Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RISC-V Embedded Market?

-> RISC-V Embedded Market was valued at USD 1.20 billion in 2025 and is expected to reach USD 3.00 billion by 2034.

Which key companies operate in RISC-V Embedded Market?

-> Key players include SiFive, Western Digital, Microchip, Andes Technology, and Nuvoton, among others.

What are the key growth drivers?

-> Key growth drivers include cost‑effective royalty‑free ISA, expanding IoT and edge‑AI applications, and strong ecosystem support from silicon vendors and open‑source communities.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while North America remains a dominant market due to high R&D activity.

What are the emerging trends?

-> Emerging trends include ultra‑low‑power RISC‑V cores for sub‑10 mW IoT devices, integration of AI accelerators on RISC‑V SoCs, and increasing adoption of open‑source development toolchains.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...