MARKET INSIGHTS

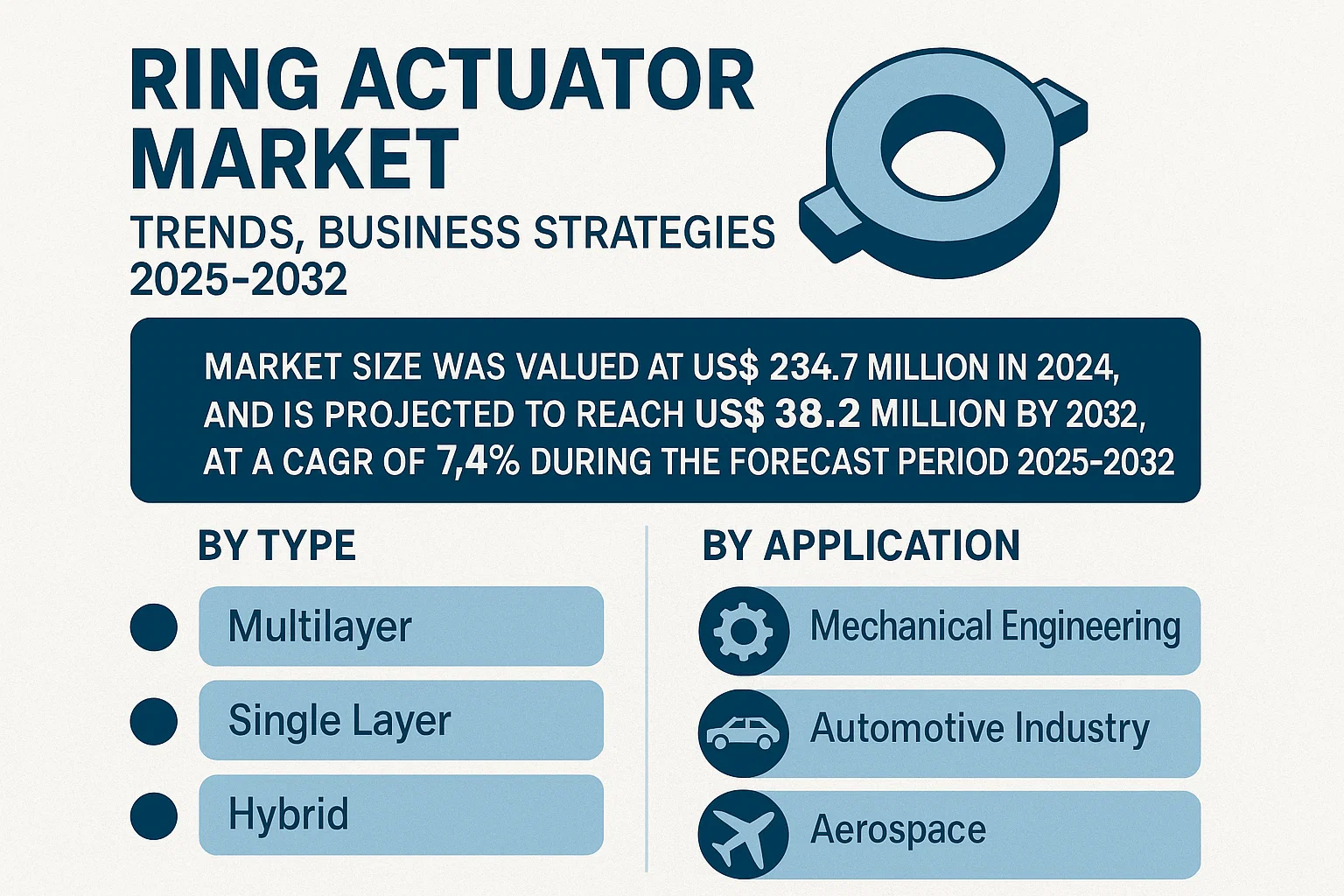

The global Ring Actuator Market size was valued at US$ 234.7 million in 2024 and is projected to reach US$ 389.2 million by 2032, at a CAGR of 7.4% during the forecast period 2025-2032.

Ring actuators are specialized electromechanical devices featuring a central aperture, allowing light or instruments to pass through. Unlike conventional linear actuators, these components are designed for precision applications in fields requiring optical alignment or sample access, particularly in microscopy, laser systems, and photonic instrumentation. The technology enables nanometer-scale positioning while maintaining beam path integrity.

Market growth is driven by increasing automation in semiconductor manufacturing, where ring actuators facilitate wafer inspection systems. Furthermore, advancements in biomedical imaging and rising R&D investments in photonics contribute to demand expansion. However, the high precision requirements result in substantial manufacturing costs, creating pricing pressure for suppliers. Leading manufacturers like PI and Thorlabs are addressing this challenge through proprietary piezoelectric ceramic formulations that enhance performance while controlling production expenses.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Precision Optical Systems to Fuel Market Expansion

The ring actuator market is experiencing significant growth due to increasing demand for high-precision optical systems across industries. These specialized actuators enable micron-level positioning adjustments while allowing unobstructed light paths – a critical requirement in advanced microscopy, laser alignment, and photonic applications. The global industrial automation sector, which accounts for nearly 40% of actuator demand, continues to drive adoption as manufacturers seek solutions for delicate material handling and micro-positioning tasks requiring both precision and throughput.

Expansion of Photonics and Semiconductor Industries to Boost Adoption

Semiconductor fabrication and photonic component manufacturing represent key growth areas for ring actuators. As chip geometries shrink below 7nm nodes and photonic integrated circuits become more complex, the need for vibration-isolated, sub-micron positioning has intensified. Front-end semiconductor equipment manufacturers are increasingly specifying ring actuators for wafer inspection systems, where their stable mechanical properties and thermal insensitivity improve yield rates by up to 15% compared to conventional positioning solutions.

Medical Technology Advancements Create New Application Possibilities

The healthcare sector presents substantial growth opportunities, particularly in minimally invasive surgical systems and advanced diagnostic imaging. Modern surgical microscopes and ophthalmic lasers increasingly incorporate multi-axis ring actuator systems for tremor-free instrument positioning. Recent developments in confocal microscopy and optical coherence tomography (OCT) systems have further driven demand, with the global medical actuator market projected to maintain 8% annual growth through 2030.

MARKET RESTRAINTS

High Initial Costs and Complex Integration to Limit Market Penetration

While ring actuators offer superior performance, their adoption faces challenges due to substantial initial investment requirements. Complete positioning systems incorporating high-performance ring actuators can cost 3-5 times more than conventional alternatives, creating barriers for cost-sensitive applications. Additionally, the specialized mounting requirements and control electronics needed for optimal performance often necessitate customized integration solutions, further increasing total system costs and implementation timelines.

Material Science Limitations Constrain Performance Parameters

Current actuator materials face fundamental limitations in simultaneously achieving desired displacement ranges, resolution, and long-term stability. Piezoelectric materials, while offering nanometer-scale resolution, suffer from hysteresis effects and creep that degrade positioning repeatability over extended periods. Advanced composite materials have improved performance but remain costly to manufacture at scale, with production yields below 70% for some critical components. These material challenges particularly impact applications requiring both large displacements and sub-nanometer precision.

Supply Chain Complexities Impact Product Availability

The specialized nature of ring actuator components creates vulnerabilities in global supply chains. Rare earth materials used in high-performance piezoelectric stacks have seen price volatility exceeding 20% annually, while precision-ground ceramic components face manufacturing lead times extending beyond six months in some regions. These supply challenges have led to inventory accumulation strategies that increase working capital requirements for manufacturers and customers alike.

MARKET OPPORTUNITIES

Emerging Space and Defense Applications to Create New Growth Avenues

The aerospace and defense sectors present significant opportunities, particularly for ruggedized ring actuator solutions. Satellite optical communication terminals and space-based telescopes increasingly require actuators that maintain sub-arcsecond pointing accuracy under extreme temperature variations and vibration conditions. Development programs in adaptive optics for directed energy weapons and reconnaissance systems are driving demand for actuators with millisecond response times and micro-radian angular resolution.

Additive Manufacturing Enables Novel Actuator Architectures

Advanced manufacturing techniques are creating opportunities for next-generation actuator designs. Metal additive manufacturing now allows for monolithic ring actuator structures that eliminate assembly tolerances while improving stiffness and thermal stability. Recent developments in multi-material printing enable integrated sensor and actuator configurations that reduce system complexity. Manufacturers employing these techniques report 30-50% reductions in component counts while improving mean time between failures by up to 3x.

Industrial IoT Integration Unlocks Predictive Maintenance Capabilities

The integration of smart sensing and connectivity features creates value-added opportunities in industrial automation. Modern ring actuators increasingly incorporate embedded strain gauges and temperature sensors that enable real-time performance monitoring and predictive maintenance. This smart functionality is particularly valuable in semiconductor fabrication cleanrooms and pharmaceutical production environments, where unplanned downtime can cost over $100,000 per hour.

MARKET CHALLENGES

Competition from Alternative Positioning Technologies

Ring actuators face intensifying competition from emerging positioning technologies. Voice coil actuators have made significant advances in linearity and force density, while magnetic levitation systems now challenge traditional actuators in ultra-high vacuum applications. Perhaps most significantly, the development of MEMS-based mirror arrays threatens to displace conventional optical positioning systems in some scanning and beam steering applications, particularly where size and power efficiency are paramount.

Standardization Gaps Increase System Integration Costs

The lack of industry-wide standardization for mechanical interfaces and control protocols creates integration challenges. While some manufacturers have adopted common mounting patterns, compatibility issues persist regarding electrical connections, feedback interfaces, and control algorithms. These inconsistencies force system integrators to develop custom interface solutions for nearly 60% of installations, adding complexity and cost to deployment projects.

Intellectual Property Bottlenecks Constrain Innovation

The ring actuator market faces challenges from an increasingly complex IP landscape. Over 200 active patents cover various aspects of piezoelectric actuator designs, control methods, and specialized materials. Navigating this thicket of intellectual property requires significant legal and engineering resources, particularly for smaller manufacturers seeking to develop differentiated products without infringing existing claims. These barriers have led to consolidation in the sector as companies seek to acquire rather than independently develop critical technologies.

RING ACTUATOR MARKET TRENDS

Precision Engineering Demands Drive Advancements in Ring Actuator Technology

The global ring actuator market is witnessing transformative growth due to increasing demand for high-precision motion control in critical applications such as microscopy, laser systems, and photonic instrumentation. Unlike conventional actuators, ring actuators feature a central aperture that allows uninterrupted light or instrument passage while maintaining millimeter-level positioning accuracy. The market is projected to expand at a compound annual growth rate of % through 2032, reaching approximately US$ million, driven by innovations that improve displacement resolution below 1 nanometer. Manufacturers are incorporating advanced piezoelectric materials that offer 30% higher energy efficiency compared to traditional electromagnetic actuators, making them indispensable in space-constrained optical systems.

Other Trends

Medical Technology Integration

The medical technology sector is emerging as a key growth segment for ring actuators, particularly in minimally invasive surgical robots and high-resolution imaging systems. The ability to maintain stability during micron-scale adjustments has led to a % increase in adoption for OCT (Optical Coherence Tomography) devices. Furthermore, the development of sterilizable ceramic-based ring actuators is addressing stringent hygiene requirements in operating theaters, with prototypes demonstrating 500,000+ actuation cycles without performance degradation.

Industrial Automation and Smart Factories Fuel Demand

Industrial automation trends are reshaping the actuator landscape, with ring actuators playing a pivotal role in next-generation manufacturing systems. Their non-magnetic properties and resistance to electromagnetic interference make them ideal for semiconductor fabrication equipment, where they achieve positioning repeatability within ±0.5 microns. Recent developments include the integration of IoT-enabled predictive maintenance capabilities, reducing downtime by anticipating maintenance needs with 92% accuracy. The automotive industry’s shift toward electric vehicles has also created opportunities, with ring actuators being adapted for battery module assembly lines requiring 200+ precise adjustments per minute.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation and Technical Expertise Define Market Leadership

The global Ring Actuator market exhibits a moderately fragmented competitive structure, with established multinational corporations competing alongside specialized regional manufacturers. PI (Physik Instrumente) dominates the market with approximately 18% revenue share in 2024, owing to its extensive piezoelectric actuator portfolio and strong foothold in precision motion control applications across Europe and North America.

Piezosystem Jena and Thorlabs, Inc. collectively account for nearly 25% of global revenues, benefiting from their expertise in photonics integration and microscopy solutions. These companies maintain competitive advantage through continuous R&D investments, with Piezosystem Jena spending over 7% of annual revenues on product development.

Meanwhile, emerging players like Ring Field Company and FindLight are gaining traction in niche industrial segments through cost-competitive solutions and rapid prototyping capabilities. The market witnesses increasing competition in multilayer actuator technology, which is projected to grow at 9.2% CAGR through 2032.

Recent strategic moves include Thorlabs’ acquisition of motorized positioning system manufacturer in Q1 2024 and PI’s expansion of its U.S. production facility to meet growing aerospace and medical technology demand. Such developments indicate manufacturers’ focus on vertical integration and supply chain optimization.

List of Key Ring Actuator Companies Profiled

- PI (Germany)

- Piezosystem Jena (Germany)

- Ring Field Company (U.S.)

- Hilti (Liechtenstein)

- Thorlabs, Inc. (U.S.)

- Rotor Clip Company (U.S.)

- ARIS Stellantriebe GmbH (Germany)

- KSS Co.,Ltd. (South Korea)

- FindLight (U.S.)

- THK CO., LTD (Japan)

- ACTUATECH S.p.A. (Italy)

- Zhejiang Jiechang Linear Drive Technology Co. (China)

Segment Analysis:

By Type

Multilayer Segment Dominates Due to High Precision and Stability in Photonic Applications

The market is segmented based on type into:

- Multilayer

- Subtypes: Piezoelectric, Electromagnetic, and others

- Single Layer

- Hybrid

By Application

High Demand from the Medical Technology Sector for Laser and Microscopy Applications

The market is segmented based on application into:

- Mechanical Engineering

- Automotive Industry

- Aerospace

- Medical Technology

- Subtypes: Surgical equipment, Diagnostic imaging devices

- Electrical Industry

By Material

Piezoelectric Materials Lead Owing to Superior Performance in Precision Actuation Systems

The market is segmented based on material into:

- Piezoelectric

- Shape Memory Alloys

- Ferromagnetic

- Electroactive Polymers

By End User

Industrial Manufacturers Drive Adoption for Automation and Control Applications

The market is segmented based on end user into:

- Industrial Manufacturers

- Research Institutions

- Healthcare Providers

- Defense Organizations

Regional Analysis: Ring Actuator Market

North America

The North American ring actuator market is characterized by high technological adoption, particularly in photonics, microscopy, and aerospace applications. The U.S. holds a dominant position with substantial investments in medical technology and semiconductor industries, where precision motion control is critical. For instance, the growing semiconductor manufacturing sector, driven by the CHIPS and Science Act, is expected to fuel demand for high-performance actuators in optical alignment applications. Additionally, the presence of key players like PI and Thorlabs, Inc. strengthens the region’s market position. While Canada’s market is smaller, it shows steady growth in industrial automation. Mexico, however, faces slower adoption due to limited R&D infrastructure.

Europe

Europe maintains a strong foothold in the ring actuator market, thanks to its thriving photonics and laser technology industries. Germany leads in manufacturing precision actuators, supported by companies like Piezosystem Jena and ARIS Stellantriebe GmbH. The EU’s emphasis on automation and Industry 4.0 further stimulates demand for advanced actuator solutions. However, strict environmental regulations—particularly around material usage in actuators—pose challenges for manufacturers. Countries like France and the U.K. see steady demand from aerospace and defense sectors, while Nordic countries focus on medical and renewable energy applications. Despite economic uncertainties, innovation remains a key driver.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for ring actuators, fueled by China’s dominance in manufacturing and industrial automation. China accounts for the highest consumption, particularly in semiconductor and laser processing applications, aided by government initiatives like “Made in China 2025.” Japan and South Korea follow, leveraging their strong electronics and automotive industries. While cost-sensitive markets like India initially favored conventional actuators, growing technological investments are shifting preferences toward multilayer actuators. Southeast Asia is emerging as a manufacturing hub, though infrastructure gaps slow adoption. Nevertheless, urbanization and industrial expansion ensure long-term growth.

South America

South America presents nascent opportunities in the ring actuator market, primarily driven by Brazil and Argentina’s industrial and oil & gas sectors. Brazil’s expanding aerospace sector has created demand for actuators in navigation and instrumentation systems. However, economic instability and currency fluctuations restrict investment in high-end actuator technologies. Argentina’s market remains limited but shows potential in medical device manufacturing. The lack of local production facilities forces reliance on imports, increasing costs. While industrial automation is growing, political and financial hurdles delay widespread adoption.

Middle East & Africa

The Middle East & Africa region is in the early stages of adopting ring actuator technologies. The UAE and Saudi Arabia lead with investments in smart infrastructure and oilfield automation, where actuators are used in optical sensing and valve control. Israel’s advanced medical and defense sectors also contribute to demand. However, limited technical expertise and inconsistent regulatory frameworks slow market growth. Africa’s actuator market remains underdeveloped, though South Africa shows gradual uptake in mining and industrial applications. Despite current challenges, diversification efforts in Gulf economies could unlock future potential.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Ring Actuator markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Ring Actuator market was valued at US$ 234.7 million in 2024 and is projected to reach US$ 389.2 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Multilayer, Single Layer), application (Mechanical Engineering, Automotive, Aerospace, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading players including PI, Piezosystem Jena, Thorlabs, Inc., and Hilti, covering their market share (top five held approximately % in 2024), product portfolios, and strategic developments.

- Technology Trends: Assessment of emerging actuator technologies, integration with photonic systems, and precision engineering advancements for microscopy and laser applications.

- Market Drivers & Restraints: Evaluation of factors driving growth in photonics and precision engineering sectors along with supply chain and regulatory challenges.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, and investors in the precision actuator ecosystem.

The research employs primary interviews with industry experts and validated secondary data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ring Actuator Market?

-> Ring Actuator Market size was valued at US$ 234.7 million in 2024 and is projected to reach US$ 389.2 million by 2032, at a CAGR of 7.4% during the forecast period 2025-2032.

Which key companies operate in Global Ring Actuator Market?

-> Key players include PI, Piezosystem Jena, Thorlabs, Inc., Hilti, ARIS Stellantriebe GmbH, and KSS Co.,Ltd., among others.

What are the key growth drivers?

-> Key growth drivers include advancements in photonics technology, increasing demand for precision microscopy, and growth in laser applications.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to show the highest growth rate.

What are the emerging trends?

-> Emerging trends include miniaturization of actuators, integration with smart systems, and development of high-precision multilayer designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...