MARKET INSIGHTS

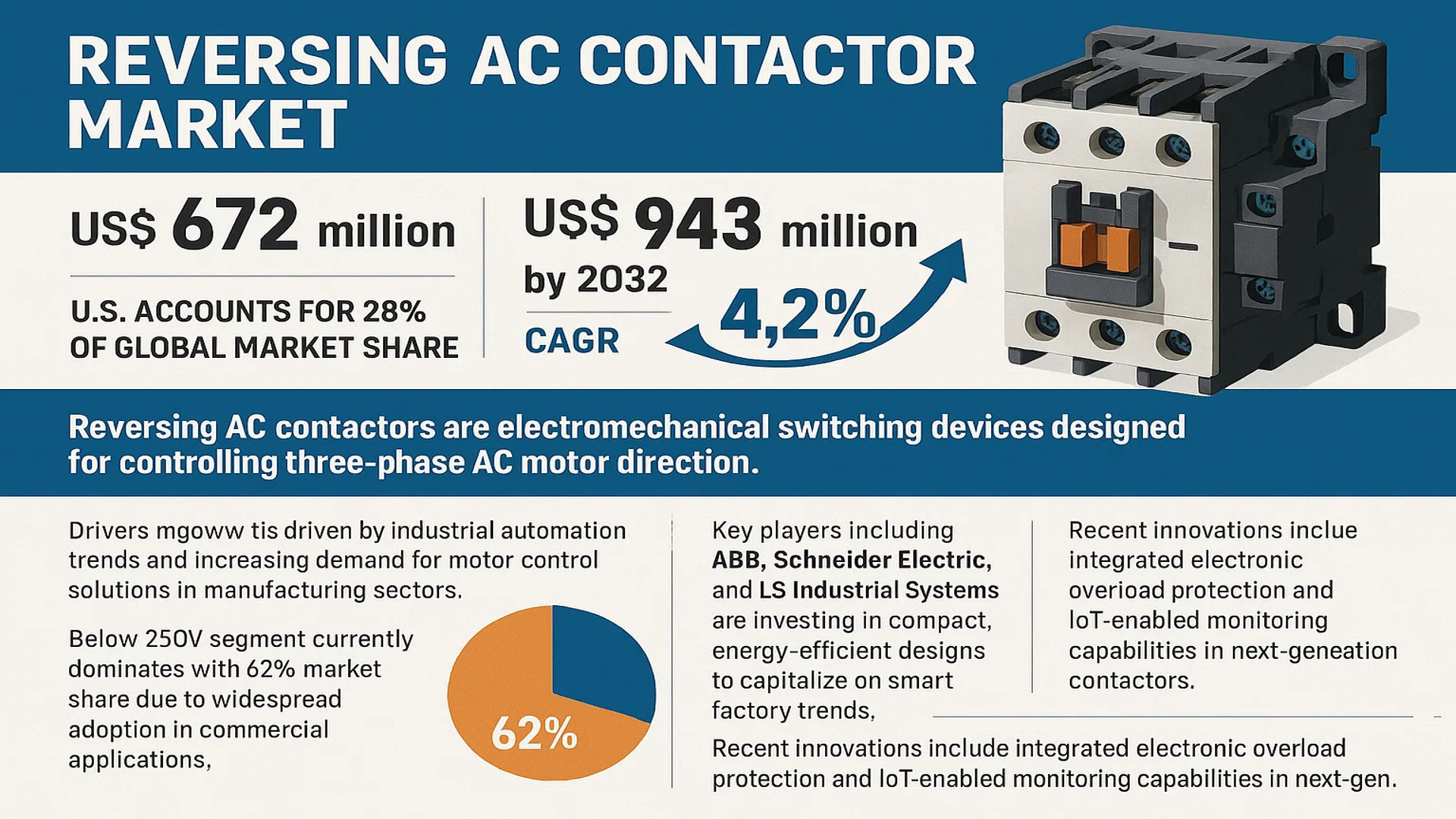

The global Reversing AC Contactor Market size was valued at US$ 672 million in 2024 and is projected to reach US$ 943 million by 2032, at a CAGR of 4.2% during the forecast period 2025-2032. The U.S. accounts for 28% of global market share, while China’s market is expected to grow at 6.2% CAGR through 2032.

Reversing AC contactors are electromechanical switching devices designed for controlling three-phase AC motor direction. These specialized components combine two standard contactors with mechanical interlocking to enable safe forward/reverse operation in industrial applications. The product finds extensive use across heavy machinery, energy power systems, and HVAC equipment where bidirectional motor control is required.

Market growth is driven by industrial automation trends and increasing demand for motor control solutions in manufacturing sectors. The below 250V segment currently dominates with 62% market share due to widespread adoption in commercial applications. Key players including ABB, Schneider Electric, and LS Industrial Systems are investing in compact, energy-efficient designs to capitalize on smart factory trends. Recent innovations include integrated electronic overload protection and IoT-enabled monitoring capabilities in next-generation contactors.

REVERSING AC CONTACTOR MARKET DYNAMICS

MARKET DRIVERS

Rising Industrial Automation Investments to Fuel Reversing AC Contactor Demand

The global push toward industrial automation is accelerating the adoption of reversing AC contactors across manufacturing facilities. As industries invest heavily in automated machinery requiring bidirectional motor control, the demand for reliable contactor solutions has surged. The industrial automation market, valued at over $200 billion globally, continues to expand at a compound annual growth rate exceeding 8%, directly influencing contactor sales. These electromechanical switches have become critical components in conveyor systems, packaging equipment, and material handling applications where motor direction reversal is fundamental to operations.

Infrastructure Development Projects Boosting Construction Sector Adoption

Global infrastructure development, particularly in emerging economies, is driving substantial growth in the construction equipment sector where reversing contactors find extensive application. Cranes, hoists, and elevators – all requiring precise bidirectional motor control – are experiencing increased deployment as urbanization rates climb. The construction equipment market is projected to maintain a steady 5% annual growth, with Asia-Pacific nations accounting for nearly 45% of global demand. This sustained sector expansion creates ongoing demand for robust electrical switching components that can withstand harsh operating environments while ensuring operational safety.

➤ Major industry players have introduced contactors with enhanced mechanical endurance, some rated for over 1 million operations, to meet the rigorous demands of construction applications.

Furthermore, the expansion of renewable energy infrastructure, particularly in wind turbine installations requiring reliable pitch control systems, presents additional growth avenues for high-performance reversing contactors.

MARKET RESTRAINTS

Price Volatility of Raw Materials Impacting Profit Margins

The reversing AC contactor market faces significant pressure from fluctuating copper and silver prices, as these metals constitute essential components in contactor manufacturing. Copper prices have shown volatility exceeding 30% year-over-year in recent periods, directly affecting production costs. Manufacturers are challenged to maintain profitability while competing in a market where pricing sensitivity remains high, particularly in cost-conscious industrial segments. This raw material instability has prompted some suppliers to explore alternative conductive materials, though performance trade-offs often limit these alternatives to less demanding applications.

Technical Limitations in High-Frequency Switching Applications

While reversing contactors excel in many industrial applications, their mechanical nature imposes constraints in scenarios requiring rapid, frequent direction changes. The physical movement of contacts creates inherent limits to switching speeds, with most commercial contactors rated for operation below 1,500 cycles per hour. Applications demanding faster bidirectional control increasingly turn to solid-state alternatives, creating competitive pressure on traditional contactor suppliers. Additionally, arc suppression challenges in high-current applications continue to drive ongoing R&D investments to extend the performance envelope of electromechanical solutions.

MARKET CHALLENGES

Intensifying Competition From Solid-State Alternatives

The emergence of advanced solid-state relay technologies presents a growing challenge to traditional reversing contactor manufacturers. Electronic switching solutions offer benefits including faster operation, silent functioning, and reduced maintenance requirements. While electromechanical contactors maintain advantages in cost and reliability for many applications, the performance gap continues to narrow. Market analysis indicates the industrial solid-state relay segment growing at nearly twice the rate of conventional contactors, pressuring manufacturers to enhance their product offerings with integrated protection features and smart monitoring capabilities.

Supply Chain Complexities in Global Distribution

The globalization of manufacturing has created intricate supply chains for contactor components and finished products. Disruptions in semiconductor availability, experienced across industries, have also impacted the production of contactors incorporating electronic control modules. Maintaining consistent quality across globally distributed production facilities while meeting diverse regional certification requirements presents ongoing operational challenges for multinational suppliers.

MARKET OPPORTUNITIES

Smart Manufacturing Integration Creating New Value Propositions

The Industry 4.0 revolution opens significant opportunities for reversing contactor manufacturers to develop intelligent, connected products. Incorporating condition monitoring capabilities and IoT connectivity transforms traditional contactors into predictive maintenance assets. Early adopters have introduced products featuring built-in sensors to track contact wear, coil health, and operational temperature, providing actionable data to prevent unexpected downtime. This evolution aligns with manufacturing facilities’ growing investment in digital transformation, estimated to exceed $1 trillion globally by 2025.

Expansion in Emerging Markets With Industrial Growth Potential

Developing regions exhibiting strong industrial growth present untapped opportunities for market expansion. Countries in Southeast Asia, Africa, and South America are investing heavily in industrialization, accompanied by rising demand for reliable electrical components. Localized product adaptations addressing regional voltage variations, environmental conditions, and application-specific requirements can capture this growth potential. Strategic partnerships with regional distributors and system integrators have proven effective for global manufacturers seeking to establish footholds in these high-growth markets.

REVERSING AC CONTACTOR MARKET TRENDS

Industrial Automation Boom Accelerates Demand for Reversing AC Contactors

The global reversing AC contactor market is experiencing robust growth driven by accelerating industrial automation across manufacturing, energy, and heavy machinery sectors. These specialized contactors, which enable bidirectional motor control, have become critical components in modern automated systems. While the market value reached approximately $450 million in 2024, projections indicate a steady compound annual growth rate (CAGR) of 5-7% through 2032. This sustained demand stems from their ability to handle high-power applications—particularly in voltage ranges below 250V—which account for nearly 60% of current market revenue. Furthermore, the integration of smart monitoring capabilities into reversing contactors is extending their application in Industry 4.0 environments where remote diagnostics and predictive maintenance are paramount.

Other Trends

Energy Transition Projects Fueling Market Expansion

The global shift toward renewable energy infrastructure is creating substantial opportunities for reversing AC contactor manufacturers. Wind turbine pitch control systems and solar tracking mechanisms increasingly rely on these components for reliable motor reversal operations. In parallel, the electrification of industrial processes is driving demand in traditional sectors—particularly where variable speed drives require frequent directional changes. This dual momentum from both green energy projects and conventional industry modernization explains why the Asia-Pacific region now commands over 40% of global market share, with China alone accounting for nearly half of regional demand as it accelerates its energy transition timeline.

Technological Advancements Reshaping Product Development

Leading manufacturers are responding to market needs through significant R&D investments in contactor technology. Recent innovations include arc suppression systems that enhance safety in high-current applications and modular designs simplifying maintenance procedures. The introduction of higher voltage variants (above 250V) for specialized industrial applications is opening new revenue streams, particularly in the oil & gas and mining sectors. This technological evolution is reflected in the product portfolios of major players—ABB and Schneider Electric collectively hold about 35% market share—as they increasingly incorporate IoT connectivity features. Such advancements also address critical pain points like electromagnetic interference reduction and operational lifespan extension in harsh industrial environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Market Dominated by Established Electrical Component Manufacturers

The Reversing AC Contactor market features a moderately consolidated competitive structure, with multinational corporations holding majority shares through established distribution networks and technological capabilities. ABB and Schneider Electric collectively control approximately 35% of global market revenue as of 2024, primarily due to their extensive industrial automation portfolios and strong foothold in both emerging and developed markets.

LS Industrial Systems has emerged as a significant challenger, particularly in the Asia-Pacific region, where its cost-competitive manufacturing base and strategic focus on heavy machinery applications have driven consistent market share gains. The company’s recent introduction of compact reversing contactors with integrated overload protection has been particularly well-received in material handling applications.

Market dynamics reveal that mid-tier specialists like ALBRIGHT INTERNATIONAL and Electric Motor Sport are carving out profitable niches through application-specific solutions. ALBRIGHT’s expertise in harsh environment contactors for mining equipment, coupled with Electric Motor Sport’s focus on high-performance motor control, demonstrates how targeted product differentiation can succeed against larger competitors.

List of Key Reversing AC Contactor Manufacturers

- ABB Ltd. (Switzerland)

- Schneider Electric (France)

- LS Industrial Systems (South Korea)

- ALBRIGHT INTERNATIONAL (UK)

- Electric Motor Sport (U.S.)

- Sensata Technologies (U.S.)

- Suntree Electric (China)

Segment Analysis:

By Type

Below 250V Segment Dominates Market Due to Extensive Use in Industrial Automation and HVAC Systems

The market is segmented based on voltage capacity into:

- Below 250V

- Above 250V

By Application

Heavy Machinery Segment Leads Owing to High Adoption in Manufacturing and Construction Equipment

The market is segmented based on application into:

- Heavy Machinery

- Energy Power

- Other

Regional Analysis: Reversing AC Contactor Market

Asia-Pacific

The Asia-Pacific region dominates the global reversing AC contactor market, accounting for the largest revenue share in 2024. Rapid industrialization in China and India has created substantial demand for motor control solutions in manufacturing, construction, and energy sectors. The Chinese government’s “Made in China 2025” initiative specifically promotes industrial automation, directly benefiting contactor manufacturers. While cost-competitive local players hold significant market share, multinational corporations like ABB and Schneider Electric are expanding their production facilities in the region to capitalize on growing demand. The increasing adoption of smart manufacturing technologies and rising investments in infrastructure projects will continue driving the market forward.

North America

North America represents a technologically advanced market with stringent safety standards for electrical components. The U.S. holds the majority share in the region, supported by revitalized manufacturing sectors and substantial investments in industrial automation. Recent reshoring initiatives and government support for domestic manufacturing through programs like the CHIPS Act have stimulated demand for motor control equipment. Canadian markets show steady growth, particularly in mining and energy applications. Major players focus on developing energy-efficient and IoT-enabled contactor solutions to meet evolving industry requirements and environmental regulations.

Europe

European demand stems primarily from Germany, France, and Italy, where precision manufacturing and automation standards are exceptionally high. The region emphasizes product reliability and energy efficiency, pushing manufacturers to innovate. EU directives on machinery safety and energy performance significantly influence product development. While growth in Western Europe remains stable, Eastern European markets are emerging as production hubs due to lower operational costs. The focus on renewable energy projects and electric mobility infrastructure presents new application areas for reversing contactors across the continent.

South America

Market growth in South America has been inconsistent due to economic fluctuations, though Brazil and Argentina show potential. Mining operations and agricultural equipment manufacturing account for most reversing contactor applications. Trade barriers and import dependency create pricing challenges for end-users. Local manufacturers compete mainly on price rather than technological sophistication. Infrastructure development projects and gradual industrial recovery post-pandemic may stimulate demand, but the market remains sensitive to political and economic stability across the region.

Middle East & Africa

This region demonstrates growing potential with increasing industrialization in Gulf Cooperation Council countries. Oil and gas applications dominate current usage, but diversification into manufacturing and construction shows promise. Infrastructure development in Saudi Arabia and UAE, including smart city projects, drives demand for quality electrical components. Africa presents longer-term opportunities as industrialization progresses, though market development is hampered by inconsistent power infrastructure and limited technical expertise in many areas.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Reversing AC Contactor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, voltage rating, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of smart features, material advancements, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Reversing AC Contactor Market?

-> Reversing AC Contactor Market size was valued at US$ 672 million in 2024 and is projected to reach US$ 943 million by 2032, at a CAGR of 4.2% during the forecast period 2025-2032.

Which key companies operate in Global Reversing AC Contactor Market?

-> Key players include ABB, Schneider Electric, LS Industrial Systems, ALBRIGHT INTERNATIONAL, Electric Motor Sport, Sensata Technologies, and Suntree Electric, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation growth, rising demand for motor control applications, and infrastructure development in emerging economies.

Which region dominates the market?

-> Asia-Pacific is the largest market, while North America shows significant growth potential.

What are the emerging trends?

-> Emerging trends include IoT-enabled contactors, energy-efficient designs, and compact modular solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...