MARKET INSIGHTS

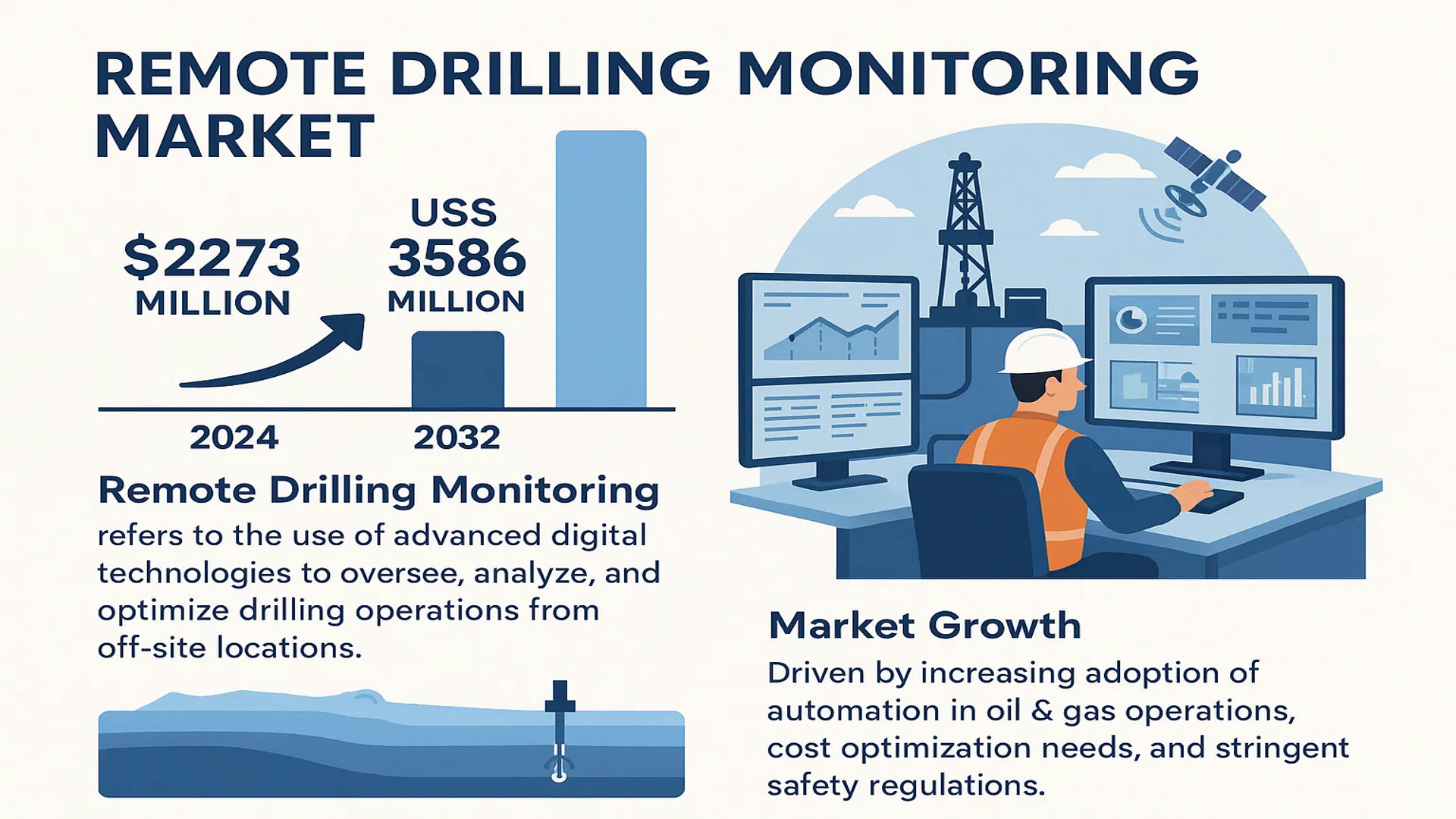

The global Remote Drilling Monitoring Market was valued at 2273 million in 2024 and is projected to reach US$ 3586 million by 2032, at a CAGR of 7.8% during the forecast period.

Remote drilling monitoring refers to the use of advanced digital technologies to oversee, analyze, and optimize drilling operations from off-site locations. This system leverages real-time data transmission via satellite or cloud-based networks, enabling engineers to monitor key metrics such as drill bit performance, pressure levels, and geological formations without being physically present at the rig site. Major components include sensors, data analytics platforms, and communication infrastructure.

The market growth is driven by increasing adoption of automation in oil & gas operations, cost optimization needs, and stringent safety regulations. Additionally, rising investments in offshore and unconventional drilling projects are accelerating demand. Key players like Schlumberger, Halliburton, and Baker Hughes are expanding their remote monitoring capabilities through AI integration and predictive analytics, further propelling industry expansion. The U.S. dominates market share due to shale gas activities, while Asia-Pacific shows rapid growth potential with new deepwater projects.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Operational Efficiency in Oil & Gas to Drive Market Growth

The global energy sector’s growing emphasis on cost optimization and operational efficiency is a key driver for remote drilling monitoring systems. With oilfield operators under pressure to maximize production while minimizing downtime, real-time monitoring solutions have become indispensable. These systems reduce non-productive time by 15-25% while improving drilling accuracy through predictive analytics, making them highly attractive for modern oilfield operations. The technology enables proactive decision-making by detecting potential equipment failures or formation challenges before they escalate into costly incidents.

Expansion of Unconventional Resource Exploration Accelerates Adoption

The boom in shale gas and tight oil exploration has created significant demand for advanced monitoring solutions. Horizontal drilling and hydraulic fracturing operations in unconventional reservoirs require precise monitoring of multiple parameters simultaneously. Remote systems provide crucial oversight of complex multi-well pad operations, with shale gas regions showing 30-40% higher adoption rates than conventional fields. As global shale resources continue to be developed, particularly in North America and China, this specialized application is expected to drive sustained market growth.

Technological Advancements in IoT and Cloud Computing Fuel Innovation

Integration of IoT sensors with cloud-based analytics platforms is revolutionizing remote monitoring capabilities. Modern systems now incorporate artificial intelligence for automated anomaly detection, reducing human error in data interpretation. The development of low-latency satellite communications has enabled real-time monitoring even in offshore and remote locations, with data transmission delays reduced to under 5 seconds in most cases. Leading service providers are continuously enhancing their software platforms with machine learning algorithms that can predict drilling dysfunctions with over 90% accuracy based on historical patterns.

MARKET RESTRAINTS

High Implementation Costs Restrain SME Adoption

While large oilfield operators are rapidly adopting remote monitoring solutions, the high initial investment remains a significant barrier for smaller companies. A comprehensive remote drilling monitoring system requires substantial capital expenditure in sensors, communication infrastructure, and software licenses – typically ranging from $500,000-$2 million per installation depending on complexity. Additionally, the ongoing costs for data transmission and cloud services can add 15-20% to operational budgets. This pricing structure makes the technology prohibitive for many independent operators and service companies.

Other Restraints

Data Security Concerns Hinder Widespread Implementation

The oil and gas industry’s cautious approach to data security significantly impacts remote monitoring adoption. With drilling data containing sensitive operational information and proprietary formation details, companies remain wary of cloud-based solutions despite advanced encryption standards. Recent incidents of cyberattacks targeting energy infrastructure have amplified these concerns, causing some operators to maintain manual monitoring processes for critical wells.

Resistance to Cultural Change in Traditional Operations

The transition from on-site to remote monitoring faces pushback from crews accustomed to conventional practices. Many veteran drilling professionals question the reliability of digital systems and prefer hands-on oversight. This cultural resistance slows implementation times, with typical workforce adaptation periods spanning 6-12 months even after system deployment.

MARKET CHALLENGES

Integration with Legacy Systems Presents Technical Hurdles

Many drilling contractors operate mixed fleets with equipment spanning multiple generations, creating integration challenges for modern monitoring solutions. Older rigs often lack standardized data output formats or compatible sensor interfaces, requiring expensive retrofits. Approximately 35-40% of current rig fleets need significant hardware upgrades to fully support advanced remote monitoring capabilities, representing a substantial obstacle to universal adoption.

Other Challenges

Regulatory Compliance Across Jurisdictions

The absence of uniform global standards for remote drilling operations complicates multinational implementation. Different countries impose varying requirements for data retention, well control procedures, and personnel certifications in remote operations. Navigating these regulatory landscapes increases compliance costs by 10-15% for service providers operating across multiple regions.

Reliability in Extreme Operating Conditions

Maintaining consistent data transmission and sensor accuracy in harsh environments remains challenging. High-temperature high-pressure wells, Arctic drilling, and deepwater operations push monitoring equipment beyond standard operating parameters, increasing failure rates. Sensor malfunction frequencies can double in extreme conditions compared to conventional operations, potentially compromising monitoring continuity.

MARKET OPPORTUNITIES

Digital Twin Technology Opens New Frontiers for Predictive Maintenance

The emerging integration of remote monitoring with digital twin technology presents significant growth opportunities. By creating virtual replicas of drilling systems that update in real-time, operators can simulate scenarios and predict equipment failures before they occur. Early adopters have reported 30-50% reductions in unplanned downtime through this technology. The digital twin segment within remote drilling monitoring is projected to grow significantly as computational power and modeling accuracy continue to improve.

5G Networks Enable Next-Generation Monitoring Capabilities

The rollout of 5G networks in oilfield regions is set to transform remote monitoring capabilities. With latency reduced to milliseconds and bandwidth increased tenfold compared to 4G, 5G enables real-time high-definition video monitoring, augmented reality interfaces, and instantaneous control adjustments. Several major oil companies have already initiated 5G pilot programs at their fields, with initial results showing 40% improvements in response times to drilling anomalies detected remotely.

Increasing Focus on ESG Drives Demand for Emission Monitoring Features

Growing environmental, social, and governance (ESG) pressures are creating opportunities for specialized monitoring functions. New systems incorporating methane detection, carbon footprint tracking, and environmental parameter monitoring are gaining traction. Regulations mandating real-time emission reporting in several jurisdictions have made these features increasingly essential, with the environmental monitoring component expected to account for 25-30% of new system revenues by 2030.

REMOTE DRILLING MONITORING MARKET TRENDS

Adoption of AI and IoT Drives Growth in Remote Drilling Monitoring

The integration of Artificial Intelligence (AI) and Internet of Things (IoT) technologies has fundamentally transformed remote drilling monitoring, enabling predictive maintenance, real-time decision-making, and enhanced operational efficiency. AI-driven analytics help identify potential equipment failures before they occur, reducing downtime by as much as 30% in some operations. Similarly, IoT-enabled sensors provide continuous data streams, allowing for precise adjustments to drilling parameters like torque and pressure. Companies are increasingly investing in cloud-based platforms to store and analyze this data, facilitating remote collaboration among geographically dispersed teams. The global market for remote drilling monitoring is projected to grow at a CAGR of 7.8% from 2024 to 2032, reaching US$ 3.59 billion, largely driven by these technological advancements.

Other Trends

Expansion in Offshore and Unconventional Resources

The rise in deepwater drilling and shale gas exploration has significantly increased demand for remote monitoring solutions. Offshore drilling operations, particularly in regions like the Gulf of Mexico and West Africa, rely on real-time data to navigate complex geological conditions. Similarly, shale gas extraction requires constant monitoring of horizontal wellbores to optimize hydraulic fracturing efficiency. The Wellsite-Level Monitoring segment, valued at a substantial market share, is particularly crucial for these applications, ensuring safer and more cost-effective operations. As unconventional energy resources gain traction, remote drilling monitoring systems are becoming indispensable for risk mitigation and regulatory compliance.

Regulatory and Cost Efficiency Demands Accelerate Adoption

Stringent safety and environmental regulations are compelling oil and gas companies to adopt remote monitoring technologies to minimize spill risks and workplace accidents. Governments worldwide are mandating stricter reporting requirements, pushing operators to deploy advanced monitoring systems. At the same time, the need for cost optimization in volatile energy markets is driving adoption. Remote monitoring reduces the need for on-site personnel, cutting operational expenses by up to 20% in some cases. Leading industry players like Schlumberger and Halliburton are innovating modular monitoring systems that offer scalability and affordability, further fueling market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Invest in Digitalization to Enhance Remote Drilling Capabilities

The global remote drilling monitoring market features a moderately consolidated structure with dominant multinational players and emerging regional competitors vying for market share. Schlumberger leads the segment through its digital division, which includes the DrillOps® advisory solution enabling real-time optimization of drilling parameters from remote centers.

Halliburton and Baker Hughes follow closely, collectively holding over 30% of the market share in 2024 thanks to their established expertise in offshore and shale drilling monitoring systems. Both companies have recently expanded their cloud-based monitoring platforms, a strategic move to reduce latency in deepwater operations.

Meanwhile, National Oilwell Varco maintains its position through continued innovation in downhole sensor technologies and data visualization tools. Their RigSense™ platform demonstrates how traditional equipment manufacturers are adapting to the digital transformation of drilling operations.

Chinese players like China Oilfield Services Limited and Shaanxi Baihao are rapidly expanding their regional footprint, leveraging government support for domestic oilfield technology development. These companies are particularly focusing on cost-effective monitoring solutions tailored for Asian shale formations.

The competitive intensity is further heightened by specialty providers such as Weatherford and Shenzhen Fluid Science & Technology, who are gaining traction with modular monitoring systems that can be retrofitted to existing rigs at lower capital expenditure.

List of Key Remote Drilling Monitoring Companies Profiled

- Schlumberger Limited (U.S.)

- Halliburton Company (U.S.)

- Baker Hughes Company (U.S.)

- National Oilwell Varco (U.S.)

- Weatherford International (Switzerland)

- Shaanxi Baihao Electronic Technology Co., Ltd. (China)

- Shenzhen Fluid Science & Technology Co., Ltd. (China)

- China Oilfield Services Limited (China)

Segment Analysis:

By Type

Wellsite-Level Monitoring Dominates the Market Due to Real-Time Data Transmission and Operational Efficiency

The market is segmented based on type into:

- Wellsite-Level Monitoring

- Subtypes: Data Acquisition Systems, Sensor Networks, and others

- Regional-Level Monitoring

- Subtypes: Cloud-Based Monitoring, Integrated Control Centers, and others

By Application

Offshore Deepwater Drilling Segment Leads Due to High Adoption in Complex Drilling Environments

The market is segmented based on application into:

- Offshore Deepwater Drilling

- Shale Gas Horizontal Wells

- Others

By Technology

IoT-Based Solutions Surge Due to Enhanced Connectivity and Predictive Analytics

The market is segmented based on technology into:

- IoT-Based Monitoring

- AI-Powered Analytics

- Satellite Communication

- Others

By End User

Oil & Gas Companies Hold Largest Share Due to Operational Optimization Needs

The market is segmented based on end user into:

- Oil & Gas Companies

- Drilling Service Providers

- EPC Contractors

- Others

Regional Analysis: Remote Drilling Monitoring Market

North America

The North American region dominates the Remote Drilling Monitoring Market, driven by advanced technological adoption in the U.S. and Canada. Major oil and gas players, including Schlumberger, Halliburton, and National Oilwell Varco, are investing heavily in digital drilling solutions to optimize operations and reduce costs. The U.S. shale boom, particularly in the Permian Basin, has accelerated demand for real-time monitoring systems. Regulatory pressures for safer drilling practices and emission reductions further support market growth. While the U.S. remains the largest market, Canada is seeing increased adoption due to oil sands and offshore drilling projects in Newfoundland. However, fluctuating oil prices and operational disruptions in the Gulf of Mexico pose challenges.

Europe

Europe’s market is shaped by stringent environmental regulations, particularly in offshore drilling operations in the North Sea. Countries like Norway and the UK lead in adopting IoT-enabled remote monitoring technologies to enhance operational efficiency and comply with EU sustainability mandates. Digital twin technology is gaining traction among operators such as Equinor and BP to simulate drilling scenarios. Despite steady growth, the region faces constraints due to declining hydrocarbon investments and increased focus on renewable energy transitions. Nonetheless, technological advancements in deepwater drilling and mature field rejuvenation present opportunities for market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region, propelled by China’s shale gas exploration and India’s expanding offshore projects. China Oilfield Services Limited (COSL) and other domestic players are integrating AI-driven monitoring to improve drilling accuracy. Indonesia and Australia also contribute significantly due to offshore gas field developments. While cost sensitivity limits the adoption of high-end systems in some markets, the push for energy security is driving investments in remote monitoring solutions. However, geopolitical tensions and infrastructure disparities in Southeast Asia create uneven growth patterns across the region.

South America

Brazil dominates South America’s market, with Petrobras leveraging remote monitoring for pre-salt offshore fields. Argentina’s Vaca Muerta shale play is another key growth area, though economic instability and policy uncertainties hinder large-scale deployments. The lack of skilled personnel and limited digital infrastructure in smaller markets like Colombia and Venezuela restrict broader adoption. Nevertheless, partnerships with global technology providers and rising foreign investments are gradually improving market prospects.

Middle East & Africa

The Middle East, led by Saudi Arabia and the UAE, is rapidly adopting automation to maximize output from aging oil fields. Saudi Aramco’s digitization initiatives and ADNOC’s focus on AI-based predictive analytics underscore the region’s shift toward smart drilling. In Africa, countries like Angola and Nigeria are implementing monitoring systems to enhance offshore operations, though political instability and underdeveloped digital ecosystems slow progress. Long-term growth potential remains strong, supported by untapped reserves and increasing FDI in oil and gas infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the Global Remote Drilling Monitoring Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Remote Drilling Monitoring market was valued at USD 2.27 billion in 2024 and is projected to reach USD 3.59 billion by 2032, growing at a CAGR of 7.8% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Wellsite-Level Monitoring, Regional-Level Monitoring), application (Offshore Deepwater Drilling, Shale Gas Horizontal Wells, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key markets driving growth.

- Competitive Landscape: Profiles of leading market participants including National Oilwell Varco, Halliburton, Schlumberger, Baker Hughes, and Weatherford, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies including IoT integration, AI-driven analytics, and advanced data transmission systems for real-time monitoring.

- Market Drivers & Restraints: Evaluation of factors such as increasing deepwater exploration activities, shale gas development, and operational efficiency demands versus challenges like high implementation costs.

- Stakeholder Analysis: Strategic insights for oilfield service providers, technology vendors, investors, and policymakers regarding market opportunities and challenges.

The research employs both primary and secondary methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Remote Drilling Monitoring Market?

-> Remote Drilling Monitoring Market was valued at 2273 million in 2024 and is projected to reach US$ 3586 million by 2032, at a CAGR of 7.8% during the forecast period.

Which key companies operate in this market?

-> Major players include National Oilwell Varco, Halliburton, Schlumberger, Baker Hughes, Weatherford, Shaanxi Baihao, Shenzhen Fluid Science & Technology, and China Oilfield Services Limited.

What are the key growth drivers?

-> Key drivers include increasing offshore drilling activities, demand for operational efficiency, safety regulations, and technological advancements in real-time monitoring systems.

Which region dominates the market?

-> North America currently leads the market due to shale gas activities, while Asia-Pacific is expected to show the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include AI-powered predictive analytics, cloud-based monitoring platforms, integration of 5G networks, and autonomous drilling systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...