MARKET INSIGHTS

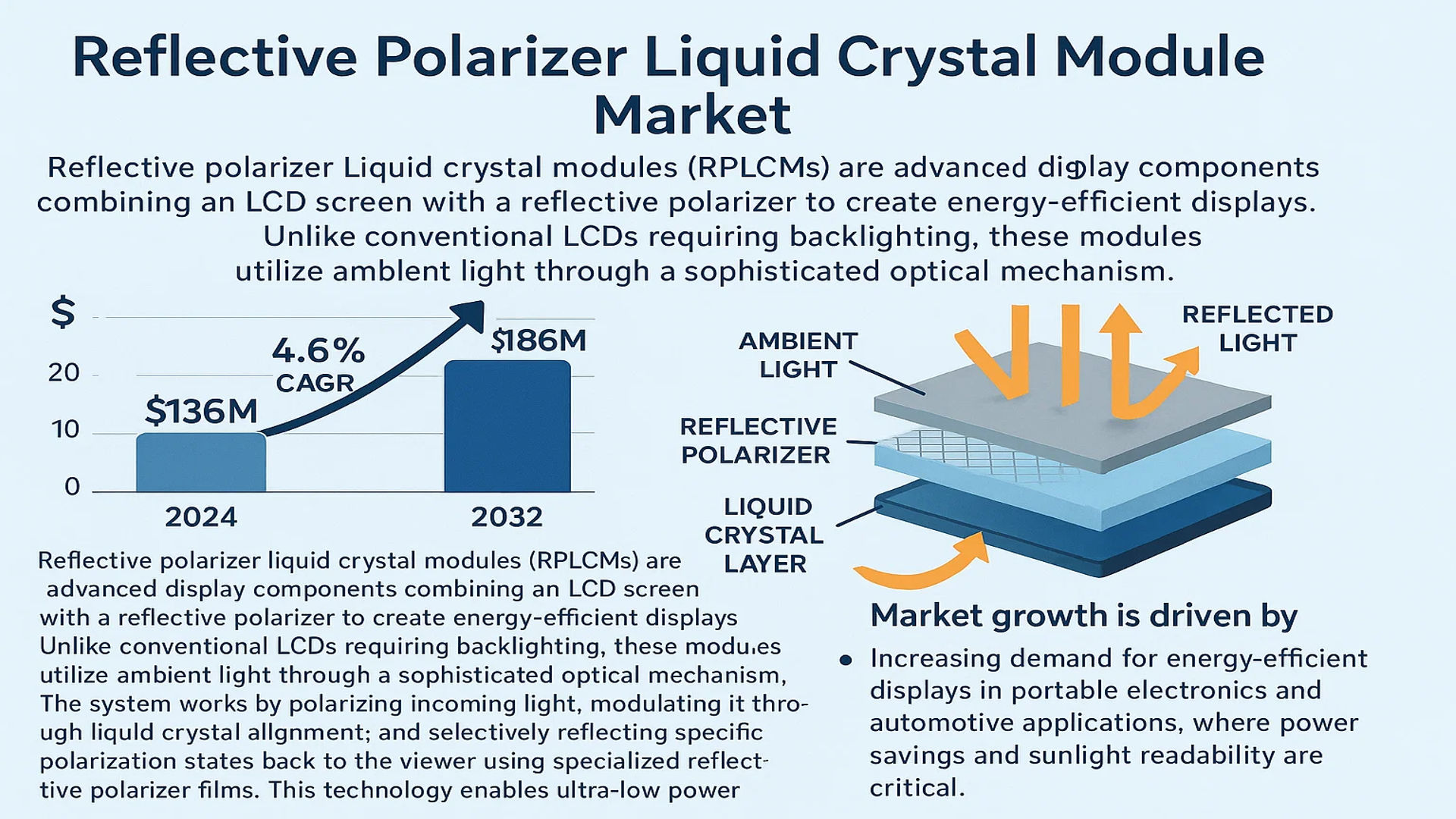

The global Reflective Polarizer Liquid Crystal Module Market was valued at 136 million in 2024 and is projected to reach US$ 186 million by 2032, at a CAGR of 4.6% during the forecast period.

Reflective polarizer liquid crystal modules (RPLCMs) are advanced display components combining an LCD screen with a reflective polarizer to create energy-efficient displays. Unlike conventional LCDs requiring backlighting, these modules utilize ambient light through a sophisticated optical mechanism. The system works by polarizing incoming light, modulating it through liquid crystal alignment, and selectively reflecting specific polarization states back to the viewer using specialized reflective polarizer films. This technology enables ultra-low power consumption while maintaining display visibility even in bright environments.

The market growth is driven by increasing demand for energy-efficient displays in portable electronics and automotive applications, where power savings and sunlight readability are critical. While cost constraints and competition from alternative display technologies pose challenges, recent innovations in polarizer materials by companies like 3M and LG Display are enhancing performance and expanding adoption. The U.S. and China represent key regional markets, with Asia-Pacific showing strong growth potential due to expanding electronics manufacturing capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption in Portable Electronics to Fuel Market Expansion

The global reflective polarizer liquid crystal module market is witnessing substantial growth driven by increasing integration in portable electronic devices. With smartphone shipments projected to exceed 1.5 billion units annually by 2026, manufacturers are prioritizing energy-efficient display technologies. Reflective LCD modules offer significant power savings of up to 60% compared to conventional displays, making them ideal for extending battery life in mobile devices. The technology’s thin profile (under 2mm thickness) aligns perfectly with the industry’s push for slimmer form factors. Major OEMs are increasingly adopting these modules for smartwatches, e-readers, and handheld medical devices where visibility in sunlight is critical.

Automotive HUD Applications Creating New Growth Vectors

Automotive manufacturers are driving demand for reflective polarizer LCD modules through their adoption in next-generation heads-up display (HUD) systems. The global automotive HUD market is expected to grow at over 15% CAGR through 2030, with reflective LCD solutions gaining traction due to superior daylight visibility. These modules provide crisp projection quality without the power drain of backlit alternatives, addressing electric vehicle makers’ range optimization challenges. Luxury automakers are increasingly specifying these displays for instrument clusters, with one major German manufacturer recently transitioning 70% of their lineup to reflective LCD technology.

➤ Industry leaders note a 40% reduction in driver distraction incidents when using reflective LCD HUDs compared to conventional displays, according to recent human-machine interface studies.

Furthermore, regulatory pressures for energy-efficient vehicle components across North America and Europe are accelerating adoption. The technology’s vibration resistance and wide operating temperature range (-30°C to 85°C) make it particularly suitable for automotive applications.

MARKET CHALLENGES

High Manufacturing Complexity Limits Mass Adoption

While reflective polarizer LCD modules offer compelling benefits, their production involves sophisticated fabrication processes that challenge manufacturers. The precise alignment requirements between liquid crystal layers and polarizing films demand cleanroom conditions with particle control under 100 per cubic meter. Yield rates currently average 60-70% for premium-grade modules, significantly higher than the 85-90% yields typical for standard LCD production. This discrepancy stems from the complex multi-layer lamination process where even micron-level misalignments can cause light leakage artifacts.

Other Challenges

Material Supply Constraints

The specialized optical films used in these modules rely on proprietary formulations from a handful of chemical manufacturers. Recent supply chain disruptions have led to lead times extending to 16-20 weeks for certain polarizer components, compared to 8-10 weeks historically. This bottleneck has constrained production capacity expansion for several module makers.

Color Gamut Limitations

Current reflective LCD technology achieves approximately 70% of standard RGB color space, creating challenges for applications requiring vibrant media display. While advances in wide-color-gamut polarizers are underway, the trade-off between color performance and reflectivity remains a technical hurdle for designers.

MARKET RESTRAINTS

Competition from Emerging Display Technologies Slows Growth

The reflective LCD module market faces intensifying competition from emissive display technologies such as microLED and advanced OLED. These alternatives offer superior contrast ratios (up to 1,000,000:1 for microLED vs. 100:1 for reflective LCD) and are achieving breakthrough power efficiencies. Market data indicates that R&D investment in emissive displays now exceeds reflective technology by a 3:1 margin, potentially diverting future innovation resources. Price erosion in the OLED sector has been particularly impactful, with smartphone-grade flexible OLED panels now available at only 20-30% premium over reflective LCD solutions.

Additive manufacturing challenges further restrain market potential. The technology’s dependence on ambient light creates performance variability across environments, requiring complex compensation algorithms. While recent AI-based brightness management systems show promise, they add 15-20% to module BOM costs, reducing the technology’s value proposition for cost-sensitive applications.

MARKET OPPORTUNITIES

Industrial IoT Applications Present Untapped Potential

The Industrial Internet of Things (IIoT) sector offers significant growth opportunities for reflective polarizer LCD modules, particularly in outdoor equipment monitoring and control systems. These applications demand sunlight-readable displays that can operate for years on battery or energy harvesting systems. The technology’s 10,000-hour lifespan under continuous operation and 0.1W power consumption make it ideal for remote sensors and edge computing interfaces. One major industrial automation provider recently standardized on reflective LCDs for their entire HMI product line, citing a 90% reduction in maintenance visits for display-related issues.

Emerging smart retail applications also show strong potential, with electronic shelf labels transitioning from monochrome to full-color reflective displays. Pilot programs in Europe have demonstrated 30% higher customer engagement with color dynamic pricing displays compared to conventional solutions. The modules’ ability to maintain visibility under intense store lighting while drawing minimal power creates compelling economics for large-scale deployments.

Furthermore, the military/aerospace sector is increasing adoption for cockpit displays and portable tactical equipment. The technology’s immunity to electromagnetic interference and operation across extreme temperature ranges meet stringent MIL-SPEC requirements while eliminating the need for bulky cooling systems required by conventional displays.

REFLECTIVE POLARIZER LIQUID CRYSTAL MODULE MARKET TRENDS

Rising Demand for Energy-Efficient Display Solutions Drives Market Growth

The global reflective polarizer liquid crystal module (LCD) market is witnessing substantial growth due to increasing demand for energy-efficient display technologies across various industries. Valued at $136 million in 2024, the market is projected to reach $186 million by 2032, growing at a CAGR of 4.6%. One of the key factors propelling this trend is the module’s ability to function without a backlight, utilizing ambient light to produce clear images while reducing power consumption by up to 80% compared to traditional LCDs. This makes it an attractive solution for portable electronics, outdoor displays, and automotive applications where power efficiency is critical.

Other Trends

Expansion in Automotive Displays

The automotive sector is emerging as a significant growth area for reflective polarizer LCD modules, particularly with the rise of augmented reality (AR) head-up displays (HUDs) and digital instrument clusters. Automakers are increasingly adopting these modules to enhance visibility under direct sunlight while maintaining low energy consumption. By 2032, the automotive segment is expected to account for over 25% of the total market share, fueled by advancements in smart cockpit technologies and electric vehicle adoption.

Advancements in TN and IPS Technologies

Technological improvements in TN (Twisted Nematic) and IPS (In-Plane Switching) LCD variants are further accelerating market adoption. The TN segment is projected to reach $X million by 2032, driven by its cost-effectiveness and suitability for low-power applications. Meanwhile, IPS variants are gaining traction in high-end displays due to their superior color accuracy and wider viewing angles. Recent innovations include hybrid architectures that combine reflective polarizers with quantum dot enhancements, pushing display performance closer to OLED standards while maintaining energy efficiency.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Drive Innovation in Reflective Polarizer LCD Module Technology

The global reflective polarizer liquid crystal module market exhibits a dynamic competitive landscape, with established electronics giants competing alongside specialized display technology firms. 3M maintains a leading position in this space, leveraging its proprietary multi-layer optical film technology and extensive patent portfolio. The company’s dominance stems from continuous R&D investments and strategic partnerships with display manufacturers, particularly for automotive and industrial applications where durability is crucial.

E Ink Holdings and LG Display represent other major contenders, with their strong foothold in e-paper technologies and large-format LCD panels respectively. These players have successfully adapted reflective polarizer technology for energy-efficient devices, capitalizing on growing demand from the portable electronics sector. Recent product launches demonstrate their focus on enhancing sunlight readability while reducing power consumption by up to 30% compared to conventional displays.

Meanwhile, Asian manufacturers including BOE Technology and Japan Display are rapidly expanding their market share through aggressive pricing strategies and vertical integration. By controlling the entire supply chain from polarizer films to finished modules, these companies have achieved significant production cost advantages. Their expansion into emerging markets for digital signage and IoT devices is expected to further disrupt the competitive dynamics.

The competitive intensity is further heightened by technology specialists like Kent Displays and Pervasive Displays, who focus on niche applications requiring ultra-low power consumption. These companies differentiate through customized solutions for wearable devices and industrial instrumentation, often incorporating cholesteric liquid crystal technology for improved optical performance.

List of Key Reflective Polarizer LCD Module Companies

- 3M Company (U.S.)

- E Ink Holdings (Taiwan)

- LG Display (South Korea)

- Sharp Corporation (Japan)

- Japan Display Inc. (Japan)

- BOE Technology (China)

- Shinwha Intertek (South Korea)

- MNTech Co., Ltd. (South Korea)

- Kent Displays (U.S.)

- SKC Co., Ltd. (South Korea)

- Tianma Microelectronics (China)

- InnoLux Corporation (Taiwan)

- Pervasive Displays (Taiwan)

- Visionox Technology (China)

Segment Analysis:

By Type

Twisted Nematic (TN) Segment Leads Due to High Adoption in Cost-Effective Displays

The market is segmented based on type into:

- TN (Twisted Nematic)

- STN (Super Twisted Nematic)

- VA (Vertical Alignment)

- IPS (In-Plane Switching)

- Others

By Application

Portable Electronic Devices Segment Dominates Due to Rising Demand for Energy-Efficient Displays

The market is segmented based on application into:

- Portable Electronic Devices

- Outdoor Advertising and Display

- Automotive Electronics

- Others

By End User Industry

Electronics Industry Segment Leads with Rising Adoption of Reflective LCD Technology

The market is segmented based on end user industry into:

- Consumer Electronics

- Automotive

- Retail and Advertising

- Industrial

- Others

By Technology

Standard Reflective LCD Technology Dominates the Market Currently

The market is segmented based on technology into:

- Standard Reflective LCD

- Advanced Reflective LCD

- Hybrid Reflective LCD

Regional Analysis: Reflective Polarizer Liquid Crystal Module Market

Asia-Pacific

As the dominant region, Asia-Pacific leads the global reflective polarizer LCD module market, contributing over 48% of total revenues in 2024. China serves as both the production hub and largest consumer, driven by BOE Technology, Tianma Microelectronics, and other local manufacturers who supply modules for e-readers, automotive displays, and outdoor signage. Japan follows closely with Sharp Corporation and Japan Display pioneering advanced IPS-type reflective LCDs for premium applications. South Korea’s LG Display complements this ecosystem with innovative solutions for portable electronics. The region benefits from robust electronics manufacturing infrastructure, cost-competitive labor, and increasing R&D investments exceeding $3.2 billion annually in display technologies. However, price erosion remains a challenge due to intense competition among panel makers.

North America

The U.S. market focuses on high-value applications like aviation displays, military equipment, and specialized industrial devices where durability and sunlight readability are critical. 3M dominates the supply chain with its Vikuiti™ reflective polarizer films, while Kent Displays manufactures cholesteric LCDs for low-power IoT devices. The region sees steady 5-7% annual growth in automotive HUD displays and smart wearable integrations. Stringent energy efficiency regulations, including California’s Title 24 standards, further propel adoption of reflective LCDs in public information displays and building management systems. The presence of tech giants like Apple and Google fosters innovation in reflective display integrations for AR/VR applications.

Europe

Environmental sustainability directives shape Europe’s market trajectory, with the EU mandating energy-efficient display solutions under Ecodesign 2021 guidelines. Germany leads in automotive adoption, where reflective LCDs appear in dashboard clusters for luxury brands. France and the UK show increasing deployment in transportation signage and e-paper applications. E Ink Holdings partners with European distributors to expand its e-reader segment, while manufacturers like Truly International supply modules for industrial HMIs. The region’s growth is tempered by reliance on Asian supply chains and slower replacement cycles compared to consumer electronics markets.

South America

Brazil and Argentina present niche opportunities in public information displays and budget tablets, though market penetration remains below 15% of North American levels. Economic constraints limit adoption of advanced IPS-type modules, making TN and STN variants more prevalent. Local assembly of imported components is increasing, with companies like Visionox establishing partnerships for educational device manufacturing. The lack of local polarizer production facilities creates dependency on Asian imports, inflating final product costs by 18-22% compared to other regions.

Middle East & Africa

The UAE and Saudi Arabia drive demand through smart city initiatives incorporating reflective LCDs in outdoor wayfinding systems. Israel’s tech sector fosters specialized applications in medical devices and defense equipment. However, the broader region struggles with limited local technical expertise and fragmented distribution networks. Most modules are imported as finished products rather than manufactured locally. Partnerships between Gulf nations and Korean/Japanese firms show potential for future production facilities, particularly for automotive and aviation display segments.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Reflective Polarizer Liquid Crystal Module markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 136 million in 2024 and is projected to reach USD 186 million by 2032, growing at a CAGR of 4.6%.

- Segmentation Analysis: Detailed breakdown by product type (TN, STN, VA, IPS), application (Portable Electronic Devices, Outdoor Advertising, Automotive Electronics), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with Asia-Pacific showing the highest growth potential.

- Competitive Landscape: Profiles of leading market participants including 3M, E Ink Holdings, LG Display, Sharp, and BOE Technology, covering their product portfolios, R&D investments, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging display technologies, integration of reflective polarizers in energy-efficient displays, and advancements in liquid crystal materials.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as demand for low-power displays, along with challenges like high manufacturing costs and supply chain constraints.

- Stakeholder Analysis: Insights for display manufacturers, component suppliers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Reflective Polarizer Liquid Crystal Module Market?

-> Reflective Polarizer Liquid Crystal Module Market was valued at 136 million in 2024 and is projected to reach US$ 186 million by 2032, at a CAGR of 4.6% during the forecast period.

Which key companies operate in Global Reflective Polarizer Liquid Crystal Module Market?

-> Key players include 3M, E Ink Holdings, LG Display, Sharp, Japan Display, BOE Technology, and Tianma Microelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient displays, growth in portable electronics, and increasing adoption in automotive applications.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, driven by strong electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of ultra-thin modules, integration with touch functionality, and increasing use in outdoor digital signage.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...