Rad-hard ceramic capacitor for GEO satellite bus Market Insights

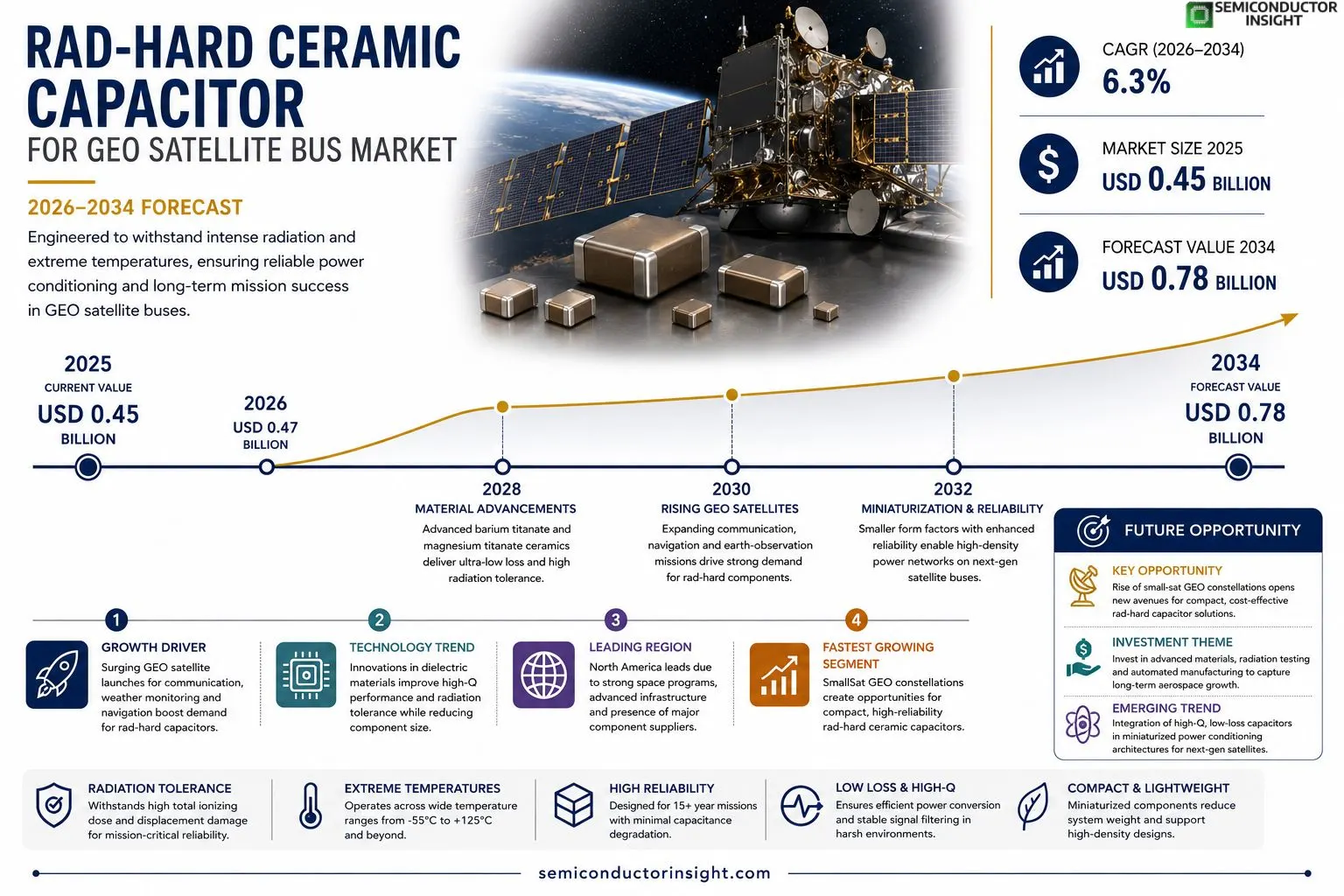

Rad-hard ceramic capacitor for GEO satellite bus market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.45 billion in 2025 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Rad‑hard ceramic capacitors are passive electronic components engineered to retain capacitance performance under intense ionizing radiation and extreme temperature cycles typical of geostationary Earth orbit (GEO) satellite buses. Their dielectric materials,often based on barium titanate or magnesium titanate,provide high‑Q factors and low loss while ensuring long‑term reliability over multi‑year missions.The market is gaining momentum because launch schedules for communication, navigation and earth‑observation satellites are expanding, driving demand for components that guarantee mission‑critical uptime. Furthermore, governmental space initiatives and commercial constellations are pushing manufacturers toward miniaturized yet robust power‑conditioning solutions, which favors rad‑hard ceramics despite their premium cost. Key players such as AVX Corp., KEMET Corporation and Murata Manufacturing continue to invest in process refinements and radiation‑testing facilities, reinforcing supply confidence across the sector.

MARKET DRIVERS

Increasing GEO Satellite Deployments

The rapid expansion of GEO satellite constellations for communications, weather monitoring, and navigation drives demand for components that can survive prolonged exposure to space radiation. Rad-hard ceramic capacitor for GEO satellite bus Market benefits from this trend as manufacturers seek reliable, high‑performance passive devices that maintain capacitance stability over the satellite’s 15‑year lifespan.

Advances in Ceramic Materials

Recent breakthroughs in doped alumina and magnesium titanate formulations have yielded ceramics with superior dielectric loss and radiation tolerance. These material improvements enable designers to reduce part count while meeting stringent power‑density requirements, strengthening the growth outlook for Rad-hard ceramic capacitor for GEO satellite bus Market.

➤ “Reliability under high radiation is a decisive factor for mission success, making rad‑hard ceramics indispensable.”

Combined, the surge in satellite launches and the availability of more resilient ceramic technologies create a robust foundation for market expansion, encouraging investment from both established aerospace firms and emerging space startups.

MARKET CHALLENGES

Stringent Qualification Requirements

Satellite programs impose rigorous testing protocols,including total ionizing dose (TID), displacement damage, and thermal cycling,to certify component survivability. Meeting these standards often extends development cycles and inflates costs for manufacturers of Rad-hard ceramic capacitor for GEO satellite bus Market products.

Other Challenges

Cost Sensitivity

The specialized processing and low‑volume production associated with rad‑hard ceramics lead to higher unit prices. Satellite operators, facing budget pressures, must balance performance gains against the premium expense of these capacitors.

MARKET RESTRAINTS

Limited Supplier Base

Only a handful of vendors possess the qualified manufacturing lines and radiation‑testing facilities required for rad‑hard ceramic components. This concentration restricts competition, potentially leading to longer lead times and limited design flexibility for satellite developers.

MARKET OPPORTUNITIES

Emerging SmallSat GEO Constellations

While traditional GEO platforms dominate, a new wave of small‑sat constellations seeks cost‑effective yet radiation‑tolerant solutions. These missions create an opening for scaled‑down, high‑reliability rad‑hard ceramic capacitors, allowing suppliers to diversify product lines and capture a growing segment within Rad-hard ceramic capacitor for GEO satellite bus Market.

Rad-hard ceramic capacitor for GEO satellite bus Market Trends

Increasing Demand Driven by Expanded GEO Satellite Launches

Rad-hard ceramic capacitor for GEO satellite bus Market is witnessing steady expansion as the number of communication, navigation and earth‑observation satellites scheduled for geostationary orbit rises. market value reached USD 0.45 billion in 2025 and is projected to climb to approximately USD 0.78 billion by 2034. This trajectory reflects heightened investment in both governmental space programs and commercial constellations, which require power‑conditioning components that can endure intense ionizing radiation and extreme temperature cycles without performance loss. The premium cost of rad‑hard ceramics is offset by their proven reliability over multi‑year missions, making them a preferred choice for mission‑critical bus architectures.

Other Trends

Advancements in Dielectric Materials

Manufacturers are concentrating on barium titanate and magnesium titanate formulations to improve the quality factor (Q) and reduce dielectric loss. Recent process refinements have delivered capacitance stability that exceeds 99 % after exposure to radiation levels typical of GEO environments. These material breakthroughs enable smaller package footprints while maintaining the high‑voltage tolerance required for power‑distribution networks, supporting the trend toward miniaturized yet robust satellite subsystems.

Supply Chain Consolidation and Manufacturing Innovation

Key players such as AVX Corp., KEMET Corporation and Murata Manufacturing are strengthening their supply chains through strategic investments in radiation‑testing facilities and automation of ceramic sintering processes. This focus on manufacturing efficiency reduces lead times and enhances volume capacity, addressing the growing demand while preserving the rigorous quality standards demanded by the space sector. The combined effect of tighter supply chains and ongoing material innovation positions Rad-hard ceramic capacitor for GEO satellite bus Market for sustained growth through the next decade.

COMPETITIVE LANDSCAPEKey Industry Players

Rad‑hard Ceramic Capacitors for GEO Satellite Bus – Competitive Overview

The GEO satellite bus segment is dominated by a few multinational firms that have integrated rad‑hard ceramic capacitor production into dedicated aerospace lines. AVX Corp., KEMET Corporation and Murata Manufacturing collectively account for the bulk of annual shipments, leveraging deep expertise in barium‑titanate dielectrics and investing heavily in radiation‑testing facilities to meet stringent NASA and ESA qualification standards. Their scale enables cost‑effective volume production while maintaining the premium reliability required for multi‑year missions, positioning them as the primary suppliers for large commercial and government satellite programs.Beyond the market leaders, several niche manufacturers contribute specialized offerings that address emerging miniaturization and high‑frequency demands. TDK Corporation, Vishay Intertechnology, Taiyo Yuden, Kyocera Corporation and Samsung Electro‑Mechanics focus on compact, high‑Q components for next‑generation small‑sat constellations. NXP Semiconductors, Qorvo and Skyworks provide hybrid solutions that combine rad‑hard capacitors with advanced RF front‑end modules. Cobham (formerly STC) and Analog Devices target defense‑grade platforms, emphasizing extended temperature ranges and ultra‑low leakage. Texas Instruments and Intel, while not primary capacitor producers, engage in strategic partnerships to source rad‑hard parts for their space‑qualified ASICs.

List of Key Rad‑hard Ceramic Capacitor Companies Profiled

- AVX Corp.

- KEMET Corporation

- Murata Manufacturing

- TDK Corporation

- Vishay Intertechnology

- Taiyo Yuden

- Kyocera Corporation

- Samsung Electro‑Mechanics

- NXP Semiconductors

- Qorvo

- Skyworks Solutions

- Cobham (formerly STC)

- Analog Devices

- Texas Instruments

- Intel

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High‑Q ceramic capacitors dominate due to their superior dielectric stability in radiation‑rich environments.

|

| By Application |

|

Power regulation modules emerge as the leading application because mission‑critical bus power systems demand unwavering capacitance under radiation stress.

|

| By End User |

|

Commercial satellite manufacturers lead the demand trajectory, driven by expanding broadband constellations and earth‑observation platforms.

|

| By Radiation Tolerance |

|

High‑dose tolerance is the most sought after characteristic because GEO missions expose hardware to prolonged ionizing radiation.

|

| By Form Factor |

|

Surface‑mount devices (SMD) dominate the packaging landscape as satellite bus designs favor compact, high‑density board layouts.

|

Regional Analysis: Rad-hard ceramic capacitor for GEO satellite bus Market

North America

Sustained demand stems from the need to replace aging GEO satellites, the launch of new high‑capacity communication payloads, and heightened mission‑critical reliability requirements imposed by defense agencies.

A concentrated supplier base of specialty ceramic firms, combined with advanced testing labs, provides a reliable flow of radiation‑hard components, though lead times remain sensitive to raw material availability.

FCC licensing and ITU coordination encourage compliance with stringent radiation tolerance standards, fostering a market that rewards high‑reliability design approaches.

Ongoing R&D focuses on ultra‑low loss ceramics and novel sealing techniques that extend capacitor lifespan under intense radiation, supporting next‑gen GEO bus architectures.

Europe

European space agencies, notably ESA, drive regional interest through collaborative satellite programs that prioritize radiation‑hardened components. Local manufacturers benefit from a policy environment that supports EU‑wide research funding, fostering innovation in ceramic material purity and test‑bed facilities across Germany, France, and the UK. While the market size is smaller than North America, strong regulatory alignment with international standards sustains steady demand.

Asia-Pacific

Rapid growth in the Asia‑Pacific space sector, propelled by China, India, and Japan, is creating new opportunities for Rad-hard ceramic capacitors. Emerging GEO satellite constellations for broadband services are prompting domestic manufacturers to upscale capabilities, though supply chain maturity lags behind the West. Partnerships with established Western firms are expected to accelerate technology transfer and market penetration.

South America

South America’s satellite market remains nascent, with a few national programs focusing on communications and earth observation. The region relies heavily on imported radiation‑hard components, primarily sourced from North America and Europe. Growing interest in regional GEO payloads could stimulate modest demand, but infrastructure constraints limit rapid expansion.

Middle East & Africa

Investment in GEO satellite capacity by Gulf Cooperation Council (GCC) nations is driving a cautious uptick in demand for radiation‑tolerant capacitors. While local manufacturing is limited, strategic procurement agreements with suppliers ensure access to high‑reliability components. Africa’s market remains largely dependent on external vendors, with potential growth linked to regional connectivity initiatives.

Report Scope

This market research report provides a comprehensive analysis of the Rad-hard ceramic capacitor for GEO satellite bus Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Rad-hard ceramic capacitor for GEO satellite bus Market?

-> Rad-hard ceramic capacitor for GEO satellite bus Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 0.78 billion by 2034.

Which key companies operate in Rad-hard ceramic capacitor for GEO satellite bus Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...