Quantum Dot Display Market Insights

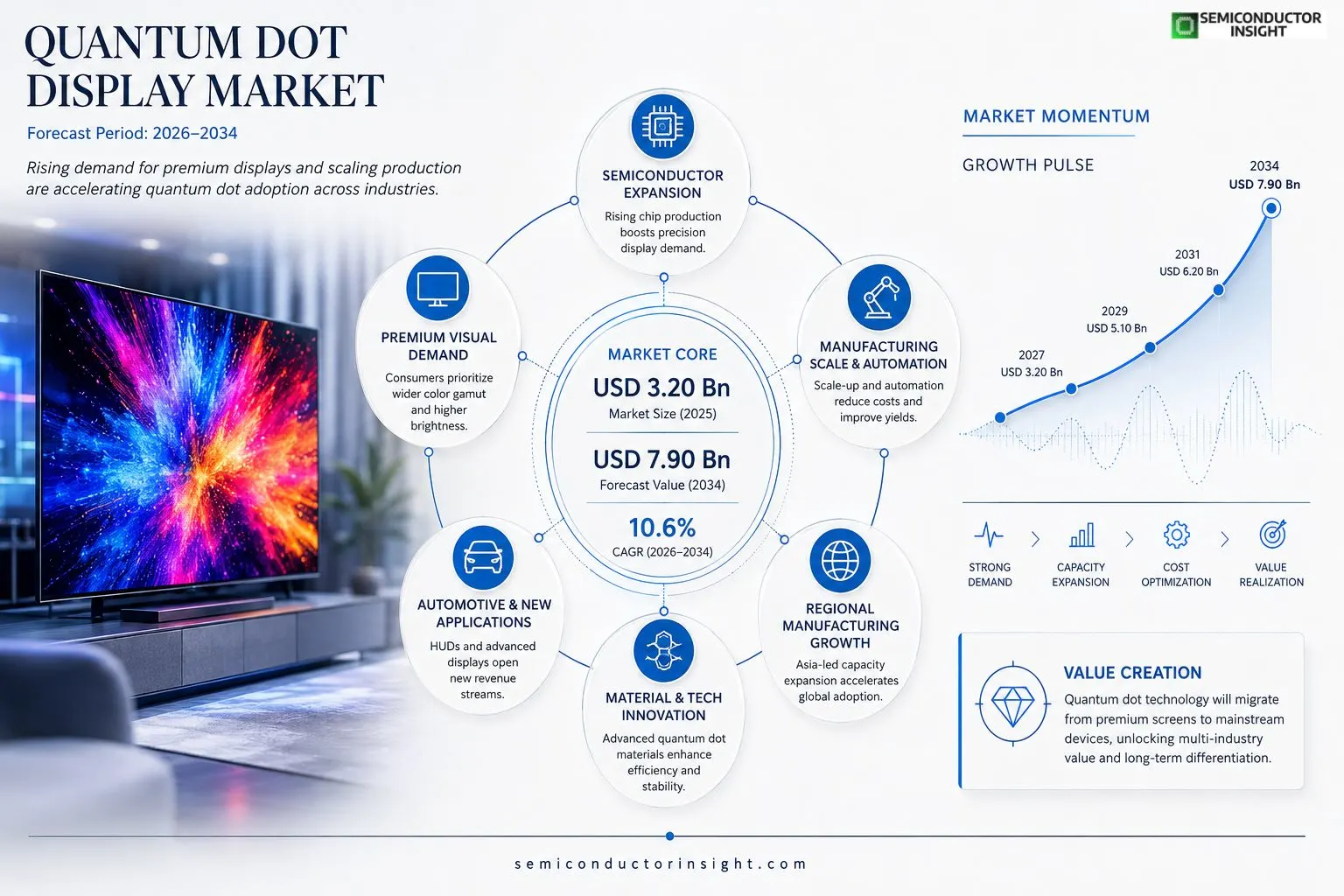

Quantum Dot Display Market was valued at USD 3.20 billion in 2025 and is expected to reach USD 7.90 billion by 2034, exhibiting a CAGR of 10.66% during the forecast period.

Quantum dot displays are advanced thin‑film devices that incorporate semiconductor nanocrystals to emit pure‑color light when excited electrically or optically; this enables significantly wider color gamuts and higher brightness compared with conventional LCDs.The market is experiencing rapid growth due to rising consumer demand for premium‑quality televisions and mobile screens, expanding adoption of quantum‑dot technology in automotive heads‑up displays, and ongoing cost reductions driven by scale‑up manufacturing at firms such as Samsung Display, LG Display, BOE Technology Group and TCL Corporation.

MARKET DRIVERS

Rising Consumer Demand for High‑Performance Visuals

The surge in premium‑grade televisions and ultrawide monitors is pushing manufacturers to adopt quantum‑dot technology for its superior color gamut and brightness. Consumers increasingly prioritize vivid, lifelike images, which directly fuels growth in Quantum Dot Display Market.

Adoption by Leading Electronics OEMs

Major OEMs such as Samsung, LG, and TCL have integrated quantum‑dot panels across flagship product lines, citing reduced power consumption and improved efficiency. Their commitment accelerates scale economies and validates the technology’s commercial viability.

➤ “Quantum‑dot panels are now the preferred choice for premium displays, delivering up to 30 % higher luminance while maintaining color accuracy.”

As pricing pressures ease and production yields improve, the technology is expected to migrate from high‑end models to mid‑range devices, expanding the addressable market base.

MARKET CHALLENGES

Manufacturing Complexity and Yield Issues

Quantum‑dot layer deposition requires precise control of particle size and uniformity. Small variations can cause color shift, leading to lower yields and higher per‑unit costs, which constrain price‑sensitive segments.

Other Challenges

Supply Chain Constraints

The reliance on rare‑earth materials and specialized inks creates bottlenecks, especially when global logistics face disruptions. These constraints limit the ability to quickly upscale production volumes.

MARKET RESTRAINTS

High Production Costs

Initial capital investment for quantum‑dot fabs remains substantial. Even with incremental cost reductions, price premiums over conventional LCD panels restrict adoption in cost‑conscious markets.Environmental regulations surrounding the disposal of cadmium‑based quantum dots add compliance expenses, prompting some manufacturers to explore cadmium‑free alternatives.Competing technologies such as Mini‑LED and OLED continue to improve in efficiency and cost, posing a restraint on market share gains for quantum‑dot solutions.

MARKET OPPORTUNITIES

Expansion into Automotive Displays

Automotive infotainment systems demand high brightness and wide color range for both daytime and nighttime visibility. Quantum‑dot panels meet these criteria, opening a sizable new revenue stream.Large‑format signage and digital out‑of‑home installations benefit from the technology’s durability and low power draw, presenting opportunities in urban advertising networks.Emerging handheld devices and augmented‑reality headsets are exploring quantum‑dot micro‑displays to achieve richer color reproduction without compromising form factor, further diversifying the market’s application base.

Quantum Dot Display Market Trends

Premium Television Adoption Accelerates Growth

Quantum Dot Display Market is being propelled by a marked increase in consumer preference for high‑end televisions that deliver wider color gamuts and higher peak brightness than conventional LCD panels. Manufacturers integrate semiconductor nanocrystals that emit pure‑color light, allowing displays to achieve near‑perfect color accuracy that appeals to cinephiles and early‑technology adopters alike. Retail data show that premium‑size models equipped with quantum‑dot technology are now commanding a larger share of total TV shipments, driven by streaming services that showcase HDR content. This shift is encouraging OEMs to prioritize quantum‑dot panels across their flagship product lines, reinforcing the market’s upward trajectory.

Other Trends

Automotive Heads‑Up Displays Expand Opportunities

In parallel, Quantum Dot Display Market is witnessing rapid integration of quantum‑dot panels into automotive heads‑up displays (HUDs). These displays benefit from the technology’s high brightness and narrow viewing angle, which are essential for clear visibility under varying ambient light conditions within vehicle cabins. Major automotive suppliers are collaborating with display manufacturers to embed quantum‑dot HUDs that can render critical navigation and safety information in vivid, easily distinguishable colors. Early‑stage deployments in luxury vehicle models have demonstrated reduced driver distraction and improved situational awareness, prompting broader adoption across mid‑range segments as production volumes increase.

Manufacturing Scale Reduces Costs and Broadens Reach

Scaling production capacity remains a pivotal factor for Quantum Dot Display Market. Companies such as Samsung Display, LG Display, BOE Technology Group, and TCL Corporation have expanded their quantum‑dot manufacturing lines, achieving economies of scale that lower unit costs. This cost moderation enables mid‑tier consumer electronics, including smartphones and tablets, to incorporate quantum‑dot panels without a prohibitive price premium. As supply chains stabilize and yield rates improve, the technology is expected to transition from premium niches to mainstream devices, further diversifying the market landscape and supporting sustained demand growth.

COMPETITIVE LANDSCAPEKey Industry Players

Quantum Dot Display Market – Competitive Overview

The quantum‑dot display segment is presently dominated by a handful of vertically integrated manufacturers that control both the nanocrystal supply chain and high‑volume panel production. Samsung Display and LG Display lead the market with extensive R&D pipelines, large‑scale fabs, and deep relationships with premium TV OEMs. Their ability to achieve economies of scale has driven cost reductions, allowing quantum‑dot technology to migrate from niche premium sets into mainstream product lines. BOE Technology Group and TCL Corporation have rapidly expanded capacity in China, leveraging governmental incentives and aggressive pricing strategies to capture a growing share of the mid‑range and automotive heads‑up display markets. This concentration creates a tiered market structure: a top tier of global foundries setting technology standards, a second tier of regional players scaling volume, and an emerging tier of specialist innovators.Beyond the dominant tier, several niche and specialist firms contribute critical differentiation through proprietary quantum‑dot chemistries, flexible substrates, or vertical integration of supply chains. Companies such as Visionox, Nanosys, and JD Science focus on next‑generation QD‑LED and micro‑LED solutions for smartphones and wearables. Traditional LCD manufacturers like Sharp, AU Optronics, and Japan Display Inc. are pivoting to quantum‑dot backplanes to extend the life of their LCD portfolios. Additional players—including Sony, Hisense, and Vizio—lever on licensed QD technology to offer differentiated TV models, while emerging Chinese firms like Tianma and EverDisplay bring cost‑focused alternatives to the market. This diverse ecosystem sustains innovation pressure, ensuring continuous performance gains and price erosion across the quantum‑dot display value chain.

List of Key Quantum Dot Display Companies Profiled

- Samsung Display

- LG Display

- BOE Technology Group

- TCL Corporation

- Visionox

- Nanosys

- Sharp

- AU Optronics

- Japan Display Inc.

- Sony

- Hisense

- Vizio

- Tianma

- EverDisplay

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

LCD‑Quantum Dot is the dominant type because it integrates seamlessly with existing panel manufacturing lines, offering a cost‑effective pathway to richer colours. • It leverages mature LCD supply chains while delivering quantum‑dot‑enhanced colour fidelity. • Manufacturers can upgrade legacy fabs with minimal re‑tooling. • Consumers appreciate the familiar form factor combined with superior visual experience. |

| By Application |

|

Televisions lead the application landscape as premium‑size screens demand the widest colour gamut and highest brightness. • Quantum‑dot panels differentiate flagship models through vivid, lifelike imagery. • Content creators value the expanded colour space for cinema‑grade production. • Retail environments showcase the technology’s impact, driving brand perception and consumer willingness to upgrade. |

| By End User |

|

Consumer Electronics dominate end‑user demand, driven by home entertainment and personal device aspirations. • Home viewers seek immersive experiences that replicate theatrical colour depth. • Mobile device makers integrate quantum‑dot layers to differentiate flagship phones. • The combination of visual performance and evolving design aesthetics reinforces consumer preference for quantum‑dot enabled products. |

| By Technology |

|

Photoluminescent Quantum Dots remain the primary technological choice because they provide reliable colour conversion with established blue‑LED excitation. • Their manufacturing process aligns with current back‑light assembly lines. • They offer a balance of efficiency and longevity that appeals to OEMs. • The technology’s stability supports diverse form‑factors from large‑screen TVs to automotive HUDs. |

| By Form Factor |

|

Flat‑Panel continues to dominate because it aligns with mainstream manufacturing infrastructure and consumer expectations. • Design simplicity facilitates large‑area deployment in living rooms and public venues. • Production yields are higher, reducing risk for manufacturers. • The flat‑panel format serves as a platform for future innovations such as rollable or bendable displays. |

Regional Analysis: North America

United States

The consumer electronics segment is the primary driver for Quantum Dot Display adoption in the US, with televisions and mobile devices leading the way.

The automotive industry is increasingly exploring Quantum Dot Displays for in-vehicle infotainment systems and instrument clusters, prioritizing vibrant and clear visuals.

High-performance Quantum Dot Displays are finding applications in industrial control panels and medical imaging equipment due to their high color gamut and brightness.

The growth of augmented and virtual reality is creating demand for Quantum Dot Displays that deliver accurate colors and high refresh rates for immersive experiences.

Europe

Europe presents a mature and sophisticated market for Quantum Dot Display technology. Driven by stringent quality standards and a strong emphasis on energy efficiency, the adoption of these displays is steadily increasing. The television market remains a key driver, with consumers seeking enhanced picture quality and wider color gamuts. Beyond televisions, applications in professional displays, automotive infotainment, and industrial control systems are gaining traction. Business strategies in Europe often focus on compliance with European regulations and collaborations with leading technology companies. The region’s commitment to sustainability further encourages the adoption of energy-efficient Quantum Dot Display solutions, aligning with the growing demand for environmentally responsible products.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing market for Quantum Dot Display technology. Fueled by the rapid expansion of the consumer electronics industry in countries like China and India, the demand for vibrant and high-quality displays is soaring. The smartphone and television sectors are particularly strong contributors to this growth. Moreover, the region’s robust manufacturing ecosystem provides a competitive advantage for Quantum Dot Display manufacturers. Business strategies in Asia-Pacific often involve localized production and partnerships with regional players to cater to specific market needs and preferences. The increasing disposable incomes and growing digital penetration further contribute to the expanding market for Quantum Dot Displays across the Asia-Pacific region.

South America

The South American market for Quantum Dot Display technology is characterized by steady growth potential. The increasing affordability of consumer electronics and a rising demand for premium viewing experiences are driving adoption. The television and mobile device segments are the primary consumers of these displays. While the market is still relatively nascent compared to North America and Asia-Pacific, there are opportunities for growth in the coming years. Business strategies in South America often focus on cost-effective solutions and building brand awareness.

Middle East & Africa

The Middle East and Africa represent a growing market for Quantum Dot Display technology, with increasing investments in consumer electronics and infrastructure development. The demand for large-screen televisions and high-performance displays is rising, particularly in key markets like the United Arab Emirates and South Africa. The automotive sector is also showing potential for Quantum Dot Display integration. Business strategies in this region often involve partnerships with local distributors and retailers to penetrate the market effectively.

Quantum Dot Display Market Trends, Business Strategies 2026-2034

Quantum Dot Display Market is poised for substantial growth between 2026 and 2034. Key trends include further advancements in Quantum Dot materials and manufacturing processes, leading to improved efficiency and cost-effectiveness. Increased integration of Quantum Dots into OLED and LCD technologies will drive widespread adoption. Business strategies will increasingly focus on sustainability, with manufacturers prioritizing environmentally friendly production methods. The demand for wider color gamuts and higher brightness levels will continue to fuel innovation in Quantum Dot Display technologies.

Report Scope

This market research report provides a comprehensive analysis of the Quantum Dot Display Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Quantum Dot Display Market?

-> Quantum Dot Display Market was valued at USD 3.20 billion in 2025 and is expected to reach USD 7.90 billion by 2034, exhibiting a CAGR of 10.66% during the forecast period.

Which key companies operate in Quantum Dot Display Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...