MARKET INSIGHTS

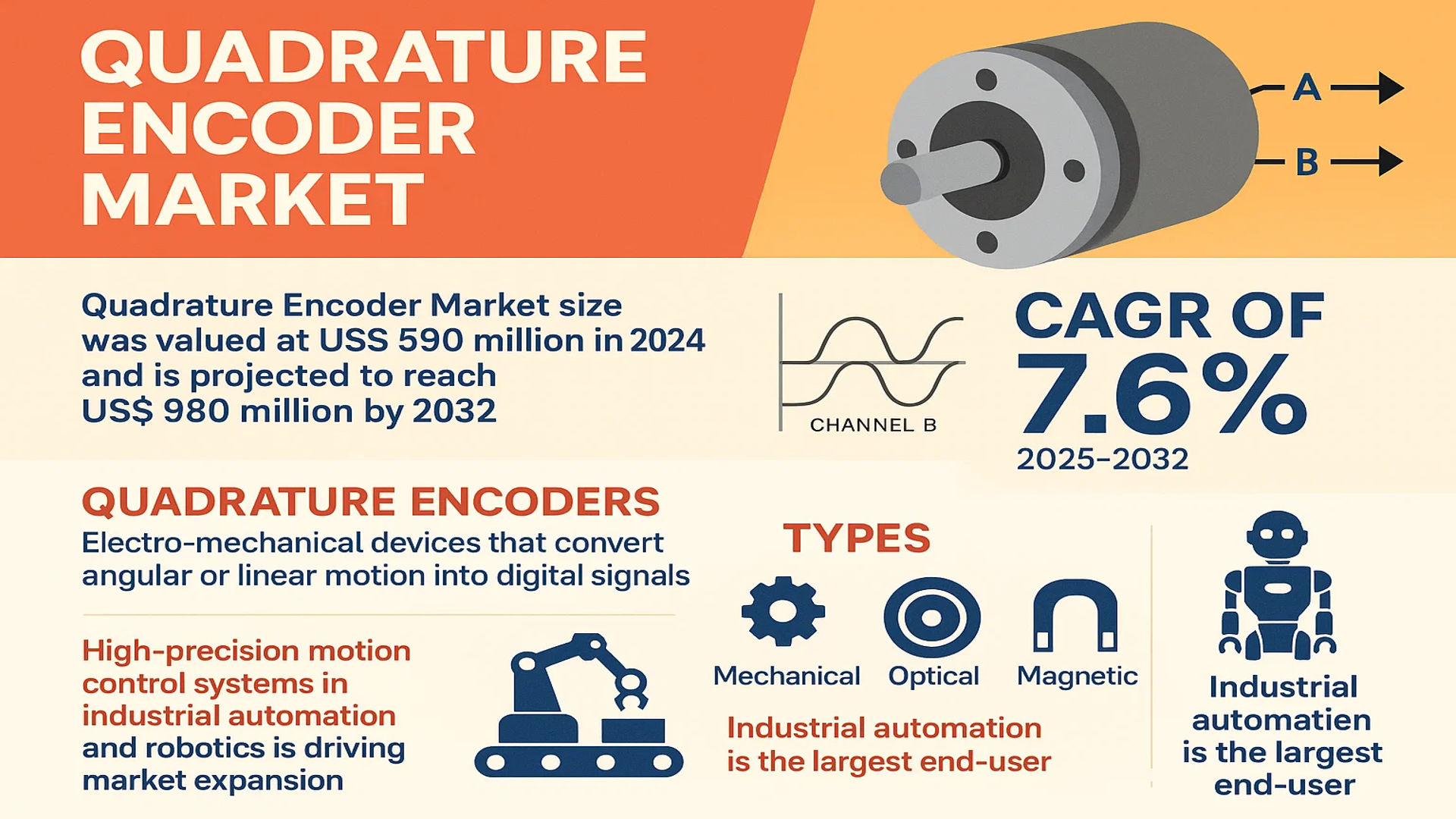

The global Quadrature Encoder Market size was valued at US$ 590 million in 2024 and is projected to reach US$ 980 million by 2032, at a CAGR of 7.6% during the forecast period 2025-2032. The demand for high-precision motion control systems in industrial automation and robotics is driving market expansion.

Quadrature encoders, also known as incremental encoders, are electro-mechanical devices that convert angular or linear motion into digital signals. These encoders utilize two output channels (A and B) to provide position and direction feedback, making them essential for applications like motor control, robotics, and rotating radar systems. They are available in three primary types: mechanical, optical, and magnetic, with optical encoders dominating the market due to their high resolution and reliability.

While the industrial automation sector remains the largest end-user, the robotics segment is growing rapidly because of advancements in collaborative and autonomous robots. Additionally, increasing adoption in aerospace and defense applications is further fueling market growth. Key players such as TE Connectivity, Nidec Avtron, and US Digital are focusing on innovation, including miniaturization and improved signal processing, to maintain competitiveness.

MARKET DYNAMICS

MARKET DRIVERS

Rising Automation in Industrial Applications to Fuel Market Expansion

The global surge in industrial automation is driving significant demand for quadrature encoders, which are essential for precise motion control in automated systems. With manufacturing sectors increasingly adopting Industry 4.0 technologies, the need for high-accuracy position feedback devices has grown exponentially. Quadrature encoders play a critical role in closed-loop motor control systems, enabling real-time monitoring and adjustment of robotic arms, conveyor belts, and CNC machines. The industrial automation market is projected to maintain robust growth, subsequently boosting encoder adoption across smart factories and process automation environments.

Expanding Robotics Industry to Accelerate Adoption

The robotics sector’s rapid expansion presents a major growth opportunity for quadrature encoder manufacturers. Modern collaborative robots (cobots) and industrial robotic systems heavily rely on encoder feedback for joint positioning and movement precision. As robot deployments increase across automotive assembly, electronics manufacturing, and logistics automation, encoder integration becomes indispensable. The global robotics market has demonstrated consistent year-over-year growth, with particularly strong adoption in Asia-Pacific manufacturing hubs. This trend directly correlates with increased encoder shipments for robotic servo motor applications.

➤ High-resolution optical encoders are becoming the preferred choice for robotic systems requiring positioning accuracy within ±0.1°, driving innovation in encoder design and performance.

Furthermore, advancements in miniaturized encoder technology align perfectly with the robotics industry’s need for compact, high-performance components. Leading manufacturers are developing specialized encoder solutions for robotic joints and end-effectors, creating new revenue streams in this booming sector.

MARKET RESTRAINTS

High Costs of Precision Encoder Components to Limit Market Penetration

While demand grows, the quadrature encoder market faces constraints from the substantial costs associated with high-precision manufacturing. Optical encoders particularly require expensive components like precision glass discs, high-quality LEDs, and photodetector arrays. These materials account for a significant portion of production costs, making premium encoder models cost-prohibitive for some price-sensitive applications. In developing markets where cost competitiveness is crucial, this pricing barrier slows adoption rates, pushing some users toward lower-quality alternatives.

Additional Constraints

Environmental Sensitivity

Performance limitations in harsh operating conditions present another market restraint. Standard optical encoders can suffer degraded performance when exposed to excessive vibration, temperature extremes, or contamination. While sealed and ruggedized models exist, they command substantial price premiums, creating adoption barriers for applications requiring robust performance in challenging environments.

Installation Complexity

Proper encoder installation requires precise mechanical alignment and often specialized knowledge. Incorrect mounting can lead to signal quality issues or premature failure, increasing total cost of ownership. This technical barrier discourages some potential users from transitioning to encoder-based systems, particularly in maintenance-sensitive environments.

MARKET CHALLENGES

Intense Competition from Alternative Position Sensing Technologies

The quadrature encoder market faces growing competition from emerging position sensing technologies like absolute encoders and magnetic resolvers. While quadrature systems offer cost advantages for many applications, alternative technologies provide benefits in specific use cases. Absolute encoders eliminate the need for homing routines after power cycles, while contactless magnetic sensors offer superior durability in dirty environments. Manufacturers must continually innovate to maintain quadrature encoders’ value proposition against these competing technologies.

Technological Evolution Challenges

The rapid evolution of industrial communication protocols presents integration hurdles. While traditional encoder outputs (A/B/Z signals) remain widely supported, newer industrial networks like EtherCAT and PROFINET demand compatible encoder interfaces. Manufacturers must balance backward compatibility with support for modern industrial networks, increasing development complexity and costs.

MARKET OPPORTUNITIES

Expansion into Emerging Industrial Economies to Open New Growth Frontiers

The ongoing industrialization of emerging markets represents a significant growth opportunity for quadrature encoder providers. As manufacturing sectors in Southeast Asia, India, and Latin America modernize, demand for automation components is accelerating. Localized production facilities and strategic partnerships with regional distributors can help encoder manufacturers capitalize on this growth. Government initiatives promoting smart manufacturing in these regions further enhance market potential.

Integration with IoT Platforms to Create Value-Added Solutions

The convergence of encoder technology with Industrial Internet of Things (IIoT) systems presents compelling opportunities. Smart encoders with built-in condition monitoring capabilities enable predictive maintenance strategies, reducing downtime in critical applications. Manufacturers developing encoder solutions with wireless connectivity and advanced diagnostics can command premium pricing while helping customers optimize equipment performance. Partnerships with industrial automation platform providers can accelerate adoption of these intelligent encoder solutions.

➤ Industry analysis suggests the market for smart, connected encoders could grow at nearly double the rate of conventional encoder products over the next five years.

Additionally, the renewable energy sector’s expansion offers new application avenues. Wind turbine pitch control systems and solar tracking mechanisms increasingly incorporate high-reliability encoders, creating specialized market segments with strong growth potential.

QUADRATURE ENCODER MARKET TRENDS

Increasing Automation and Precision Demand Accelerate Quadrature Encoder Adoption

The global quadrature encoder market is experiencing robust growth due to the rising demand for high-precision motion control systems in industrial automation. With an anticipated CAGR of over 7.5% between 2024 and 2032, these critical components are becoming essential for applications requiring precise positional feedback such as robotics and CNC machinery. Optical quadrature encoders currently dominate the market with nearly 60% share, driven by their superior resolution capabilities in clean environments. However, magnetic encoders are gaining traction in harsh industrial settings where durability matters more than extreme precision.

Other Trends

Miniaturization in Robotics and Medical Devices

The push for smaller, more efficient motion control systems has driven innovation in encoder miniaturization. Robotic surgical systems and compact automation equipment increasingly require encoders with footprints under 15mm while maintaining resolutions exceeding 5000 pulses per revolution. This trend aligns with the projected 23% growth in collaborative robot shipments through 2030, creating parallel demand for lightweight, high-performance encoders that don’t compromise on accuracy in confined spaces.

Integration with Smart Manufacturing Ecosystems

Quadrature encoders are evolving beyond standalone components into networked Industry 4.0 assets. Modern variants now incorporate predictive maintenance capabilities through embedded diagnostics, with some advanced models transmitting real-time performance data via IO-Link connections. This integration supports the estimated 28% of manufacturers currently implementing smart factory initiatives, where encoder feedback contributes to overall equipment effectiveness (OEE) calculations and condition monitoring systems. The ability to detect subtle vibration changes or wear patterns before failure occurs represents a significant value-add in capital-intensive production environments.

Material and Coating Innovations Enhance Reliability

Leading encoder manufacturers are responding to extreme environment challenges with advanced material solutions. New hermetically sealed optical encoders utilizing corrosion-resistant alloys maintain accuracy in marine applications, while magnetic variants with graphene-enhanced coatings demonstrate 40% better wear resistance in high-particulate manufacturing settings. These developments address critical pain points in industries like oil & gas and mining equipment, where encoder failure can lead to costly downtime. The automotive sector’s shift toward electric vehicles is also driving encoder innovation, with temperature-resistant designs capable of operating in EV motor environments exceeding 150°C.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Expansion Drive Market Leadership in Quadrature Encoder Segment

The global quadrature encoder market features a moderately fragmented competitive landscape, characterized by a blend of established multinational corporations and agile niche players. TE Connectivity and Nidec Avtron have emerged as dominant forces, collectively holding over 25% of the market share in 2024. Their leadership stems from comprehensive product portfolios spanning optical, magnetic, and mechanical encoder technologies, coupled with extensive distribution networks across North America and Europe.

While legacy players maintain strong positions, emerging competitors like US Digital and Pololu are gaining traction through specialized solutions for robotics and industrial automation applications. These smaller firms compete effectively by offering customization capabilities and rapid prototyping services that larger manufacturers often struggle to match. Notably, US Digital reported a 12% year-over-year revenue growth in Q1 2024, underscoring the demand for application-specific encoder solutions.

Recent strategic movements have intensified competition, with Mouser Electronics expanding its encoder distribution agreements with three new Asian manufacturers in March 2024. Meanwhile, SparkFun Electronics continues to capitalize on the maker community’s growth, offering affordable development kits that serve as entry points to more sophisticated industrial applications.

Looking forward, the competitive dynamics will likely shift as companies invest in smart encoder technologies. ELAP recently unveiled its IoT-enabled encoder prototype at Hannover Messe 2024, signaling the industry’s move toward connected industrial components. Such innovations, combined with strategic partnerships in emerging markets, are expected to reshape market share distribution through the forecast period.

List of Key Quadrature Encoder Companies Profiled

- TE Connectivity (Switzerland)

- Mouser Electronics (U.S.)

- ELAP S.r.l. (Italy)

- SparkFun Electronics (U.S.)

- US Digital (U.S.)

- Pololu Corporation (U.S.)

- Nidec Avtron Automation (U.S.)

- Laurel Electronics, Inc. (U.S.)

- Testview Measurement Systems (Italy)

- REVOTICS (Germany)

Segment Analysis:

By Type

Optical Encoder Segment Holds the Largest Market Share Due to High Precision and Durability

The market is segmented based on type into:

- Mechanical

- Subtypes: Contact-based, Non-contact-based

- Optical

- Subtypes: Absolute, Incremental

- Magnetic

- Subtypes: Hall-effect, Magneto-resistive

By Application

Industrial Segment Leads Due to Widespread Use in Automation and Motion Control Systems

The market is segmented based on application into:

- Industrial

- Robotics

- Rotating Radar

- Automotive

- Aerospace & Defense

- Others

By End User

Manufacturing Sector Dominates Due to High Demand for Process Automation

The market is segmented based on end user into:

- Manufacturing

- Healthcare

- Automotive

- Aerospace & Defense

- Energy & Power

Regional Analysis: Quadrature Encoder Market

Asia-Pacific

The Asia-Pacific region dominates the global quadrature encoder market, accounting for over 42% of market revenue in 2024. China’s booming automation sector, with industrial robot installations projected to reach 290,000 units annually by 2026, fuels substantial demand for precision motion control components. Japan’s well-established robotics industry maintains strict quality standards, pushing innovation in high-resolution optical encoders. Meanwhile, India’s growing manufacturing sector, particularly in automotive and electronics, creates opportunities for cost-effective encoder solutions. While price sensitivity remains a factor in emerging markets, the region benefits from robust local supply chains and increasing adoption of Industry 4.0 technologies.

North America

North America represents the second-largest quadrature encoder market, driven by advanced manufacturing and defense applications. The U.S. aerospace sector, valued at $250 billion annually, relies heavily on precision encoders for guidance systems and servo controls. Canada’s focus on industrial automation in mining and energy sectors contributes to steady demand. Strict certification requirements and emphasis on reliability push manufacturers toward high-end magnetic and optical encoder solutions. The region also benefits from strong R&D investments, particularly in medical robotics and autonomous vehicle technologies.

Europe

Europe maintains a technologically advanced encoder market centered around Germany’s industrial automation sector, which accounts for 30% of regional demand. Stringent EU machinery safety directives prompt manufacturers to integrate encoders with advanced diagnostic features. Italy’s thriving packaging machinery industry and France’s aerospace sector create specialized demand. The region shows particular interest in environmentally robust encoders capable of operating in harsh industrial environments. While growth remains steady, higher costs compared to Asian imports present ongoing competitive challenges.

Middle East & Africa

This emerging market shows increasing encoder demand across oil/gas automation and infrastructure projects. The UAE’s industrial automation investments, projected to reach $1.8 billion by 2027, drive adoption in conveyor systems and processing equipment. Israel’s high-tech sector creates niche demand for specialized encoders in medical and defense applications. However, limited local manufacturing capability results in heavy reliance on imports, with price competition significantly influencing purchasing decisions. The market shows strong potential but faces infrastructure and skilled labor constraints.

South America

Brazil and Argentina lead regional demand, primarily serving food processing, mining, and automotive sectors. Brazil’s industrial automation market is growing at 6.5% annually, creating opportunities for encoder suppliers. Economic volatility and currency fluctuations heavily impact purchasing patterns, with many buyers favoring mid-range mechanical encoders over premium solutions. Local assembly operations are gradually emerging, though most high-end components remain imported. The market shows promise but requires stabilization to achieve its full potential.

Report Scope

This market research report provides a comprehensive analysis of the Global Quadrature Encoder market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Quadrature Encoder market was valued at US$ 590 million in 2024 and is projected to reach US$ 980 million by 2032, growing at a CAGR of 7.6%.

- Segmentation Analysis: Detailed breakdown by product type (Mechanical, Optical, Magnetic), application (Industry, Robot, Rotating Radar, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific accounted for 42% market share in 2024.

- Competitive Landscape: Profiles of 15+ leading market participants including TE Connectivity, US Digital, Nidec Avtron, and their product offerings, market share (top 5 players held 35% share in 2024), and recent developments.

- Technology Trends: Assessment of emerging encoder technologies, integration with Industry 4.0, smart manufacturing applications, and precision improvements.

- Market Drivers & Restraints: Evaluation of automation growth, robotics adoption, and industrial IoT expansion versus high costs and technical complexity challenges.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators and investors in the motion control ecosystem.

Primary research included interviews with 25+ industry experts, while secondary research utilized verified data from industry reports, company filings, and trade associations to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Quadrature Encoder Market?

-> Quadrature Encoder Market size was valued at US$ 590 million in 2024 and is projected to reach US$ 980 million by 2032, at a CAGR of 7.6% during the forecast period 2025-2032.

Which key companies operate in Global Quadrature Encoder Market?

-> Key players include TE Connectivity, US Digital, Nidec Avtron, Mouser Electronics, Sparkfun, and Pololu, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation expansion, robotics adoption, demand for precision motion control, and Industry 4.0 implementation.

Which region dominates the market?

-> Asia-Pacific is the largest market (42% share in 2024), driven by manufacturing growth in China and Japan, while North America leads in technology innovation.

What are the emerging trends?

-> Emerging trends include miniaturization of encoders, higher resolution models, wireless encoder solutions, and integration with AI-driven predictive maintenance systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...