Pseudo-capacitive electrode materials for micro-supercapacitor Market Insights

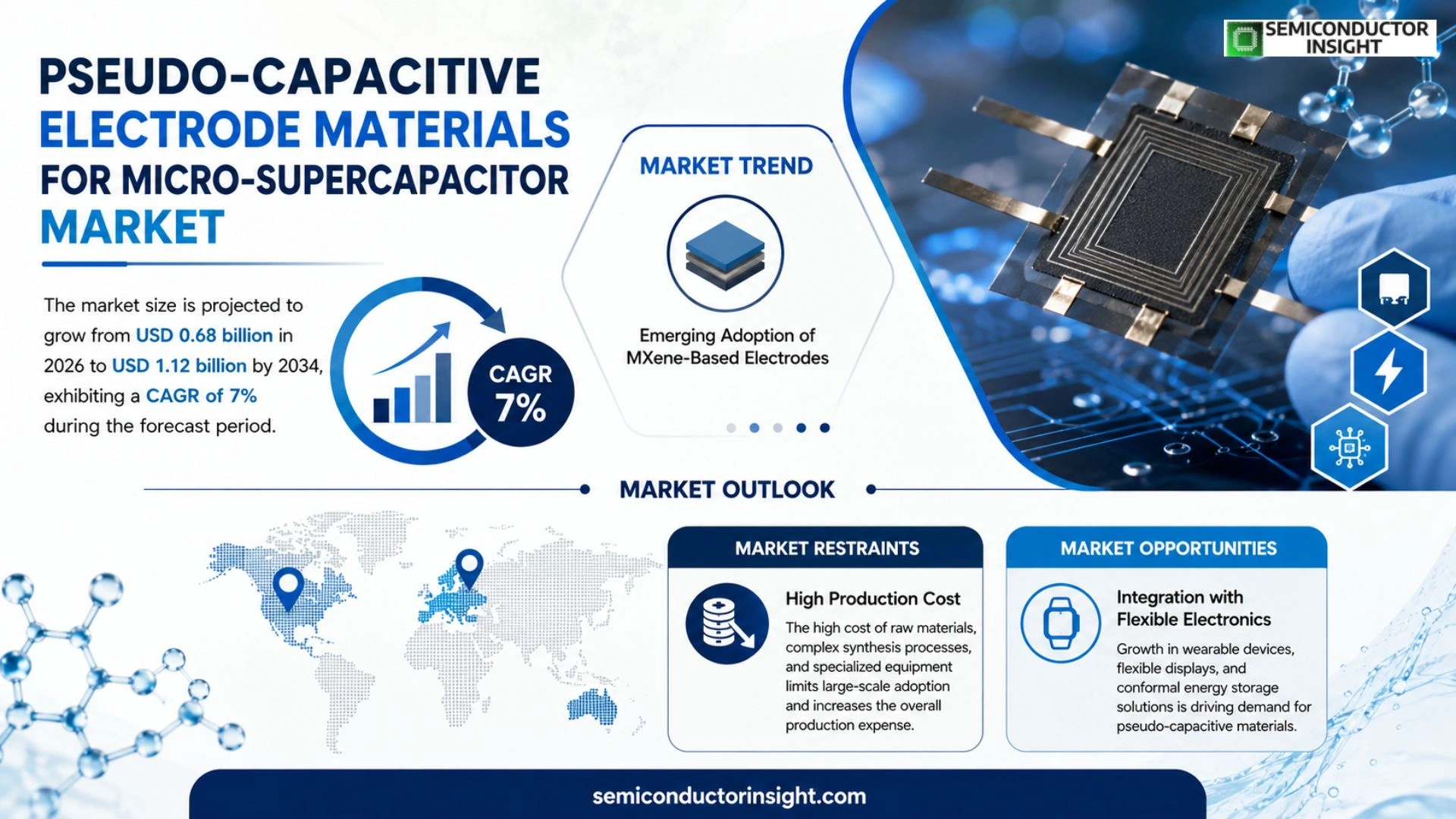

Global Pseudo-Capacitive electrode materials for micro-supercapacitor market size was valued at USD 0.62 billion in 2025. The market is projected to grow from USD 0.68 billion in 2026 to USD 1.12 billion by 2034, exhibiting a CAGR of 7 % during the forecast period.

Pseudo‑capacitive electrode materials are engineered nanostructures,such as transition‑metal oxides, MXenes, conductive polymers and hybrid composites,that store charge through fast surface redox reactions while maintaining the high power density of traditional electrostatic capacitors.

The market is accelerating because the proliferation of Internet‑of‑Things devices, wearable electronics and autonomous sensors demands ultra‑compact energy storage with rapid charge‑discharge cycles. Furthermore, breakthroughs in scalable printing techniques and government funding for flexible electronics are expanding adoption. Recent collaborations,for example, a March 2024 joint development between Bosch and the University of Cambridge on MXene‑based electrodes,illustrate how key players are driving commercialization.

MARKET DRIVERS

Growing Demand for High‑Energy Density Devices

Wearable electronics, autonomous sensors, and compact medical implants are pushing manufacturers to seek higher energy storage in ever‑smaller footprints. Pseudo-Capacitive electrode materials for micro-supercapacitor Market is benefitting from this trend, as pseudo‑capacitive mechanisms deliver energy densities up to three times those of conventional electric double‑layer capacitors while retaining rapid charge‑discharge capabilities.

Advancements in Nanostructured Materials

Recent breakthroughs in MXenes, transition‑metal oxides, and conductive polymers enable tailored ion pathways and enhanced surface redox activity. Laboratory reports indicate that engineered nanolayered electrodes can achieve power densities exceeding 20 kW kg⁻¹, making them attractive for next‑generation micro‑energy modules.

➤ “Scaling nano‑architectures while preserving pseudo‑capacitive performance is the keystone for mainstream adoption.”

Combined, these drivers are accelerating investment in pilot production lines and attracting partnerships between semiconductor foundries and advanced materials firms, setting the stage for rapid market expansion.

MARKET CHALLENGES

Scalability of Synthesis Processes

Laboratory‑scale hydrothermal and chemical‑vapor‑deposition routes often involve precise temperature control and hazardous reagents, which inflate capital expenditures when transferred to volume manufacturing. As a result, many startups face prolonged time‑to‑market, limiting early‑stage adoption.

Other Challenges

Material Stability Issues

Pseudo‑capacitive electrodes can undergo faradaic degradation under repeated cycling, especially in humid environments. Recent stress‑tests reveal capacity loss rates of up to 15 % after 10,000 cycles for certain transition‑metal oxides, prompting concerns over long‑term reliability.

Addressing these challenges requires robust encapsulation technologies and process optimizations that maintain electrochemical performance without sacrificing scalability.

MARKET RESTRAINTS

High Production Cost

Precursors such as high‑purity titanium carbide or graphene oxide demand premium pricing, and multi‑step functionalization adds further expense. Consequently, the unit cost of pseudo‑capacitive micro‑supercapacitors remains 2–3 times higher than that of traditional carbon‑based counterparts.

Additionally, the need for specialized equipment,including inert‑atmosphere furnaces and atomic‑layer‑deposition systems,creates a financial barrier for small‑to‑mid‑size manufacturers, restraining broader market penetration.

Without cost‑reduction pathways, many OEMs may defer integration of these advanced components until economies of scale become evident.

MARKET OPPORTUNITIES

Integration with Flexible Electronics

Flexible substrates, such as polyimide and stretchable polymers, are compatible with pseudo‑capacitive inks, enabling conformal energy storage that conforms to complex device geometries. Forecasts suggest that flexible micro‑supercapacitors could capture a 12 % share of the wearable market by 2030, driven by this integration capability.

Emerging Applications in IoT Edge Devices

Edge computing nodes require burst power for data processing and radio transmission. Pseudo‑capacitive materials deliver rapid discharge spikes while maintaining a low standby leakage, positioning them as a strategic power source for autonomous IoT sensors deployed in remote locations.

Investors are increasingly targeting venture‑backed startups that combine scalable printing techniques with high‑performance pseudo‑capacitive chemistries, presenting a fertile landscape for early‑stage capital and strategic collaborations.

Pseudo-capacitive electrode materials for micro-supercapacitor Market Trends

Emerging Adoption of MXene‑Based Electrodes

The micro‑supercapacitor segment is increasingly anchored by MXene‑based pseudo‑capacitive electrodes, which combine metallic conductivity with abundant surface functional groups. The March 2024 joint development between Bosch and the University of Cambridge highlighted the practical scalability of MXene inks for roll‑to‑roll printing, enabling the production of flexible micro‑supercapacitor arrays that can be integrated directly onto sensor substrates. Analysts observe that this collaboration reflects a broader shift toward printable energy storage solutions that meet the ultra‑compact form factors demanded by emerging Internet‑of‑Things (IoT) devices and wearable electronics. By leveraging the rapid surface redox reactions of MXenes, manufacturers achieve high power density while preserving the thin‑film architecture essential for autonomous sensor networks.

Other Trends

Transition‑Metal Oxide Nanostructures

Transition‑metal oxides such as nickel oxide, manganese dioxide and cobalt oxide remain foundational to pseudo‑capacitive electrode design. Recent advances in nanostructuring,particularly hydrothermal and solvothermal synthesis,have improved the uniformity of active particles, thereby enhancing charge transfer pathways and extending cycle life. These improvements are critical for applications that require long‑term reliability, such as remote environmental monitors that must operate for years without maintenance. In addition, the intrinsic chemical stability of metal oxides supports operation across a wide temperature range, aligning with the needs of outdoor IoT deployments.

Growth of Conductive Polymer Hybrids

Conductive polymers, especially poly(3,4‑ethylenedioxythiophene) polystyrene sulfonate (PEDOT:PSS), are gaining prominence when combined with carbon‑based nanomaterials. The hybrid approach exploits the mechanical flexibility of polymers together with the high electrical conductivity of graphene or carbon nanotubes. Pilot production lines in East Asia have demonstrated that solution‑processed polymer hybrids can be deposited by inkjet and aerosol‑jet printing, delivering uniform electrode films that conform to curved surfaces. Government incentives for flexible electronics have accelerated the adoption of these hybrid systems, encouraging both established manufacturers and start‑ups to invest in scalable manufacturing footprints.

COMPETITIVE LANDSCAPE

Key Industry Players

Emerging Leaders in Pseudo‑Capacitive Electrode Materials for Micro‑Supercapacitors

micro‑supercapacitor market, valued at USD 0.62 billion in 2025 and projected to reach USD 1.12 billion by 2034, is increasingly shaped by a handful of large‑scale OEMs that integrate pseudo‑capacitive electrodes into IoT and wearable platforms. Bosch leads the segment through its joint MXene‑based development with the University of Cambridge, leveraging extensive automotive and sensor portfolios to accelerate volume production. Samsung Electro‑Mechanics and Panasonic complement this leadership by deploying transition‑metal‑oxide nanostructures in their flexible printed circuitry lines, while TDK supplies high‑purity MXene powders that underpin fast‑charge architectures. These incumbents benefit from deep R&D budgets, established supply chains, and strategic collaborations that lock in early‑stage market share, creating a tiered structure where a few global players dominate bulk supply and technology standardization.

Beyond the tier‑one manufacturers, a vibrant ecosystem of specialist firms and academic spin‑outs fuels niche innovation. Guangzhou Research Institute of Nano Materials, Ningbo Jony Materials, and NanoTech Energy focus on hybrid composite chemistries that enhance energy density without compromising power delivery. Spin‑outs such as Cambridge Graphene, Axiom Materials (MIT), and Graphenea provide proprietary MXene and conductive‑polymer platforms targeting ultra‑compact sensor modules. Regional players like SK Innovation, LG Chem, and KEMET Corporation expand the portfolio with scalable electrode printing processes, while companies such as 3M and Xiaomi explore integrated device solutions that embed pseudo‑capacitive modules directly into consumer electronics. Together, these entities enrich the competitive landscape, ensuring a pipeline of differentiated technologies that address diverse application requirements across the micro‑supercapacitor value chain.

List of Key Pseudo‑Capacitive Electrode Materials Companies Profiled

- Bosch

- Samsung Electro‑Mechanics

- Panasonic

- TDK

- Guangzhou Research Institute of Nano Materials

- Ningbo Jony Materials

- NanoTech Energy

- Graphenea

- Cambridge Graphene

- Axiom Materials

- SK Innovation

- LG Chem

- KEMET Corporation

- 3M

- Xiaomi

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Transition‑metal oxides

|

| By Application |

|

IoT sensors

|

| By End User |

|

Consumer electronics

|

| By Maturity Level |

|

Pilot production

|

| By Integration Approach |

|

Printed thin‑film

|

Regional Analysis: Pseudo-capacitive electrode materials for micro-supercapacitor Market

Asia‑Pacific

China and South Korea host the majority of production facilities, capitalizing on mature silicon processing lines and emerging roll‑to‑roll manufacturing. These hubs benefit from economies of scale and a skilled labor pool, enabling cost‑effective fabrication of nano‑structured electrode films.

The region is witnessing a surge in demand for micro‑supercapacitors within wearable health monitors, portable robotics, and miniaturized power modules for IoT devices, driving the need for high‑performance pseudo‑capacitive materials.

Integrated supply chains connect raw material providers of graphene and metal oxides with downstream component assemblers, reducing lead times and supporting rapid prototyping cycles across the value chain.

Favorable environmental regulations and standards for energy storage devices encourage the adoption of greener electrode chemistries, fostering market confidence among manufacturers and end‑users alike.

North America

North America remains a strong contributor to the Pseudo‑capacitive electrode materials for micro‑supercapacitor Market, with the United States leading in research funding and collaborative ventures between universities and start‑ups. The emphasis on high‑performance computing and autonomous vehicle technologies fuels demand for compact, fast‑charging energy storage. While production capacity is comparatively lower than Asia‑Pacific, the region excels in advanced material characterization and intellectual property generation, ensuring a steady pipeline of innovation.

Europe

European countries, particularly Germany, France, and the United Kingdom, focus on sustainable manufacturing practices and the integration of pseudo‑capacitive materials into renewable energy systems. Strong policy frameworks supporting green technology transitions incentivize the development of micro‑supercapacitors for grid‑balancing and smart‑city applications. Collaborative research across the EU drives the creation of hybrid electrode formulations that aim to enhance cycle life while maintaining high power density.

South America

South America is gradually building its capabilities in the micro‑supercapacitor sector, with Brazil and Argentina pioneering pilot projects that combine local mineral resources with emerging electrode technologies. The region’s growing emphasis on renewable energy integration, particularly solar and wind, creates opportunities for decentralized storage solutions where pseudo‑capacitive materials can provide rapid response to fluctuating generation.

Middle East & Africa

In the Middle East & Africa, strategic investments in research hubs and partnerships with Asian manufacturers are expanding market awareness of pseudo‑capacitive electrode materials. Countries such as the United Arab Emirates and South Africa are exploring micro‑supercapacitors for aerospace and telecommunications infrastructure, leveraging the region’s high solar irradiance to develop resilient, fast‑charging storage components.

Report Scope

This market research report provides a comprehensive analysis of the Pseudo-capacitive electrode materials for micro-supercapacitor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Pseudo-capacitive electrode materials for micro-supercapacitor Market?

-> Pseudo-Capacitive electrode materials for micro-supercapacitor market is projected to grow from USD 0.68 billion in 2026 to USD 1.12 billion by 2034

Which key companies operate in Pseudo-capacitive electrode materials for micro-supercapacitor Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...