Programmable AI Accelerator Market Insights

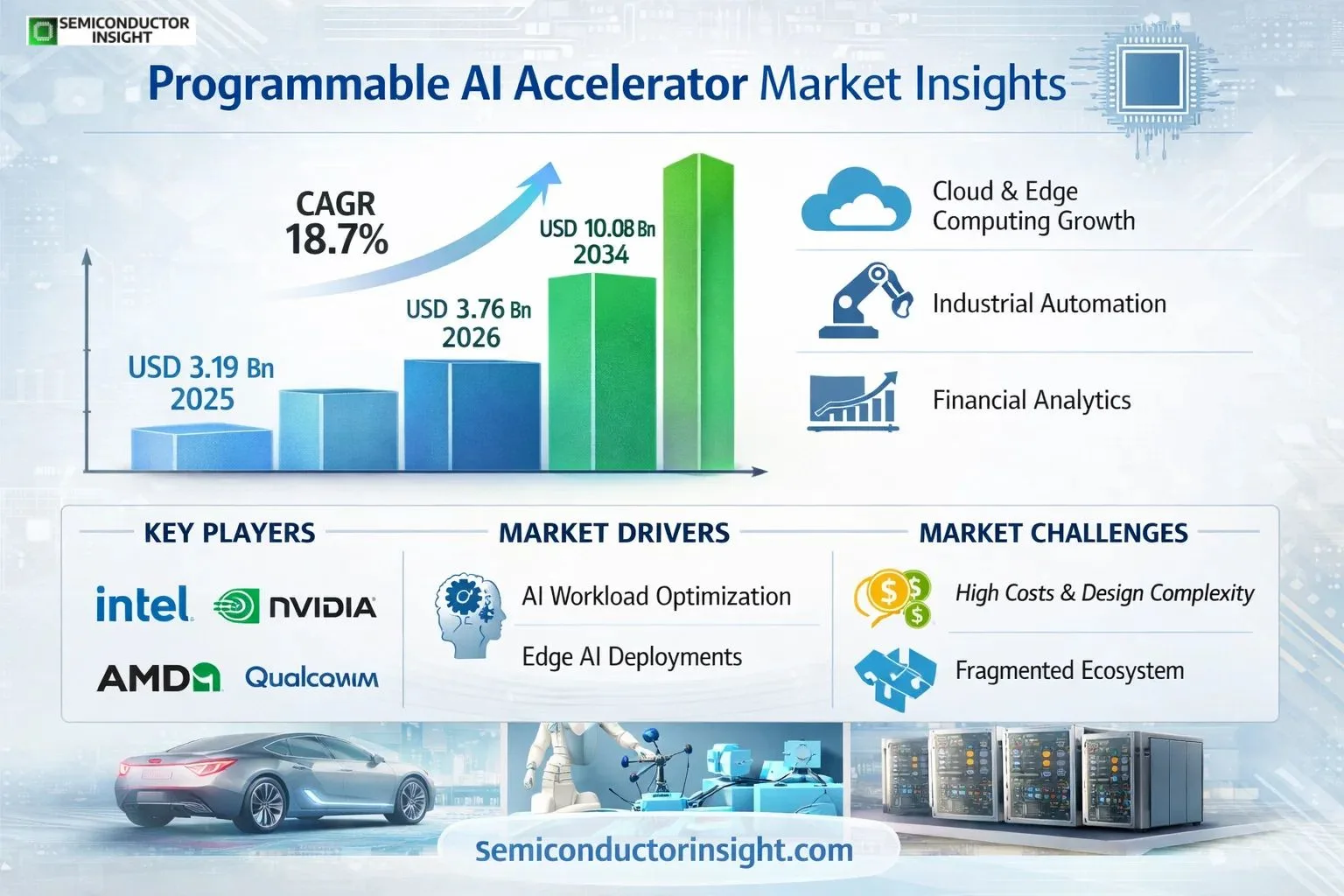

Global Programmable AI Accelerator market size was valued at USD 3.19 billion in 2025. The market is projected to grow from USD 3.76 billion in 2026 to USD 10.48 billion by 2034, exhibiting a CAGR of 18.7% during the forecast period.

Programmable AI Accelerators are specialized hardware solutions designed to enhance artificial intelligence computing efficiency while maintaining flexibility for evolving models and workloads. These include FPGA-based accelerators, reconfigurable compute architectures, and hybrid programmable SoCs deployed across servers, edge devices, and networking infrastructure. Unlike fixed-function ASICs, they enable dynamic adaptation to changing inference pipelines and real-time processing requirements in specialized environments such as industrial automation and financial analytics.

The market growth is driven by escalating demand for cloud-based AI services, edge computing deployments in telecommunications (vRAN), and mission-critical applications requiring deterministic performance. In 2025, approximately 920k units were produced globally at an average price of USD 3,800 per unit. Key industry players like NVIDIA (holding ~35% market share), Intel (through its Altera FPGA division), and AMD are investing heavily in software ecosystems to differentiate their offerings amid intensifying competition from custom ASIC solutions.

MARKET DRIVERS

Growing Demand for AI Workload Optimization

The Programmable AI Accelerator Market is witnessing significant growth due to the rising demand for efficient AI workload processing across industries. As deep learning models become more complex, programmable accelerators offer the flexibility required for diverse AI applications. Enterprises are prioritizing custom hardware solutions to enhance performance while reducing power consumption.

Advancements in Edge Computing

Programmable AI accelerators are becoming essential for edge devices, where low latency and real-time processing are critical. The market is projected to grow at 28.7% CAGR as industries adopt AI-powered edge solutions for autonomous systems and IoT applications. These accelerators enable efficient deployment of machine learning models in resource-constrained environments.

➤ “The global Programmable AI Accelerator Market is expected to reach $42.6 billion by 2028, driven by increased adoption in cloud and edge computing.”

Cloud service providers are also accelerating demand, deploying programmable accelerators to offer AI-as-a-service with improved cost efficiency and scalability compared to fixed-function hardware.

MARKET CHALLENGES

Complexity in Design and Implementation

Developing programmable AI accelerators requires specialized expertise in both hardware architecture and AI algorithms. The high development costs and lengthy design cycles pose significant barriers for smaller players in the Programmable AI Accelerator Market. Integration with existing infrastructure remains a key technical challenge for many organizations.

Other Challenges

Fragmented Ecosystem

The lack of standardized programming frameworks across different accelerator architectures creates compatibility issues, slowing down widespread adoption.

MARKET RESTRAINTS

High Development and Deployment Costs

The substantial R&D investment required for programmable AI accelerator development limits market entry for many companies. Current solutions often carry premium pricing, making them inaccessible to small and medium enterprises. Additionally, the specialized knowledge required for optimal deployment creates a skills gap that hinders market growth.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Systems

The Programmable AI Accelerator Market is poised for expansion into autonomous vehicles, drones, and robotics, where flexible acceleration is crucial. These applications require real-time decision-making capabilities that programmable accelerators can efficiently provide. The healthcare sector also presents significant growth potential for AI acceleration in medical imaging and diagnostics.

Programmable AI Accelerator Market Trends

Adoption of Reconfigurable Architectures for AI Workload Diversity

The Programmable AI Accelerator market is experiencing growing demand for FPGA-based solutions and hybrid SoCs that adapt to evolving AI models. Industries ranging from telecom edge deployments to industrial automation require hardware capable of handling diverse inference tasks while maintaining deterministic performance. This trend is driving innovation in runtime reconfiguration and specialized compute architectures optimized for real-time processing.

Other Trends

Cloud-to-Edge Deployment Expansion

Major cloud providers are increasingly deploying programmable accelerators in both data center and edge environments to optimize AI service delivery. Telecom operators leverage these solutions for virtualized RAN workloads, while industrial applications utilize them for adaptive machine vision systems. The flexibility of programmable architectures reduces total cost of ownership by supporting multiple AI pipelines on shared hardware.

Software Ecosystem Development

Vendors are investing heavily in compiler technologies and optimized kernel libraries to improve the usability of programmable AI accelerators. Advanced toolchains that automatically map neural networks to reconfigurable hardware are becoming crucial competitive differentiators. The market is seeing increased integration with mainstream frameworks like TensorFlow and PyTorch to streamline deployment workflows for enterprise customers.

Energy Efficiency Focus

With rising compute demands in AI applications, programmable accelerators are being optimized for power efficiency through architectural innovations like fine-grained clock gating and dynamic voltage scaling. Recent designs demonstrate 30-50% better performance-per-watt compared to previous generations, making them viable for battery-powered edge devices and sustainable data center operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Programmable AI Accelerator Market Leaders Driving Innovation Through Reconfigurable Architectures

The programmable AI accelerator market is dominated by semiconductor giants and specialized AI hardware innovators, with Intel (through its Altera subsidiary) and NVIDIA holding significant shares due to their FPGA and GPU-based solutions respectively. Qualcomm and AMD have strengthened positions through heterogeneous compute architectures optimized for edge AI workloads, while IBM leverages its research expertise in neuromorphic computing. The market exhibits a mix of vertical integration strategies, with cloud providers like Amazon AWS and Meta developing custom accelerators alongside ecosystem partnerships.

Niche players are gaining traction in specific segments – Cerebras Systems and Graphcore lead in wafer-scale and IPU architectures for training acceleration, while Groq and Tenstorrent focus on deterministic latency for inference workloads. SambaNova Systems differentiates through full-stack solutions combining reconfigurable dataflow with memory optimization. Broadcom and Marvell address networking-adjacent acceleration, with Architek emerging in industrial machine vision applications. This diverse landscape reflects the technology’s application across cloud, edge, and specialized vertical deployments.

List of Key Programmable AI Accelerator Companies Profiled

- Qualcomm Technologies

- IBM Research

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices (AMD)

- Marvell Technology

- Broadcom Inc.

- Altera (Intel PSG)

- Cerebras Systems

- Groq Inc.

- SambaNova Systems

- Graphcore

- Tenstorrent

- Meta Platforms

- Amazon Web Services

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

FPGA-based Accelerators dominate due to:

|

| By Application |

|

Cloud Inference Acceleration leads with:

|

| By End User |

|

Cloud Service Providers are primary adopters because:

|

| By Deployment Form |

|

PCIe Accelerator Cards remain preferred due to:

|

| By Workload Type |

|

Inference Acceleration dominates because:

|

Regional Analysis: North America Programmable AI Accelerator Market

United States

Cloud Infrastructure Dominance

Automotive AI Integration

Detroit and Silicon Valley auto manufacturers are implementing Programmable AI Accelerators in next-gen ADAS systems. The flexibility of FPGA solutions allows for over-the-air updates to accommodate evolving autonomous driving algorithms and sensor fusion requirements.

Pentagon contracts are accelerating military adoption of radiation-hardened Programmable AI Accelerators for space and battlefield applications. The technology enables real-time sensor processing and EW systems that can be reprogrammed for mission-specific AI workloads.

Healthcare Innovation

Leading medical research institutions are deploying Programmable AI Accelerators for genomics and medical imaging analysis. The reconfigurable nature of these systems allows healthcare providers to adapt AI models for specialized diagnostic applications without hardware replacements.

Canada

Canada’s Programmable AI Accelerator Market benefits from strong government support through the Pan-Canadian AI Strategy, particularly in Toronto-Waterloo and Montreal tech corridors. The country specializes in edge AI applications for smart cities and industrial IoT, with programmable accelerators enabling adaptable solutions for harsh climate conditions. Financial technology firms in Toronto leverage these solutions for AI-powered risk analysis, while oil/gas operations in Alberta deploy ruggedized versions for predictive maintenance. Academic partnerships between universities and chip manufacturers drive innovation in energy-efficient AI acceleration architectures.

Mexico

Mexico’s growing automotive manufacturing sector adopts Programmable AI Accelerators for smart factory applications and quality control systems. The proximity to U.S. tech firms facilitates knowledge transfer, with maquiladoras implementing programmable solutions for flexible production line configurations. Telecommunications companies are deploying edge AI accelerators for 5G network optimization, while financial institutions use them for fraud detection in digital payment systems. Challenges include limited domestic R&D capabilities and reliance on imported semiconductor components.

Western Europe

Germany leads in industrial Programmable AI Accelerator adoption for Industry 4.0 applications, particularly in automotive and precision manufacturing. The UK’s financial sector utilizes these solutions for algorithmic trading, while France focuses on healthcare and defense applications. Nordic countries emphasize energy-efficient designs for datacenters, with Sweden’s climate pledge driving innovations in low-power AI acceleration. The EU Chips Act is boosting regional semiconductor capabilities, though adoption trails North America in cloud deployment scale.

Asia-Pacific

China dominates regional Programmable AI Accelerator deployment through government-backed tech giants and semiconductor initiatives. Japan specializes in edge AI for robotics and automotive applications, while South Korea’s memory chip leaders integrate programmable accelerators. India shows rapid growth in startup-driven AI solutions, particularly for financial inclusion and agriculture. Australia’s mining sector employs ruggedized accelerators for autonomous equipment. Trade restrictions create regional semiconductor ecosystem fragmentation impacting supply chains.

Report Scope

This market research report provides a comprehensive analysis of the Programmable AI Accelerator Market , covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of programmable AI accelerators in powering advancements across industries such as cloud computing, telecommunications, industrial automation, and financial analytics.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, target workload, deployment form factor, and application to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/ML, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Programmable AI Accelerator Market?

-> The Programmable AI Accelerator Market was valued at USD 3192 million in 2025 and is projected to reach USD 10475 million by 2034, growing at a CAGR of 18.7% during the forecast period.

Which key companies operate in Programmable AI Accelerator Market?

-> Key players include Qualcomm, IBM, Nvidia, Intel, AMD, Architek, Broadcom, Marvell, Altera (Intel), Cerebras Systems, Groq, SambaNova Systems, Graphcore, Tenstorrent, Meta, and Amazon AWS, among others.

What are the key growth drivers?

-> Key growth drivers include cloud and enterprise inference acceleration, telecom edge/vRAN deployments, industrial machine vision, cybersecurity inspection, and financial analytics where workload diversity favors programmable hardware.

Which region dominates the market?

-> Asia is the fastest-growing region, particularly in China, Japan, and South Korea, while North America remains a dominant market with strong presence of key players.

What are the emerging trends?

-> Emerging trends include FPGA-based accelerators, reconfigurable compute architectures, hybrid programmable SoCs, and increasing adoption in edge computing applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...