Market Insights

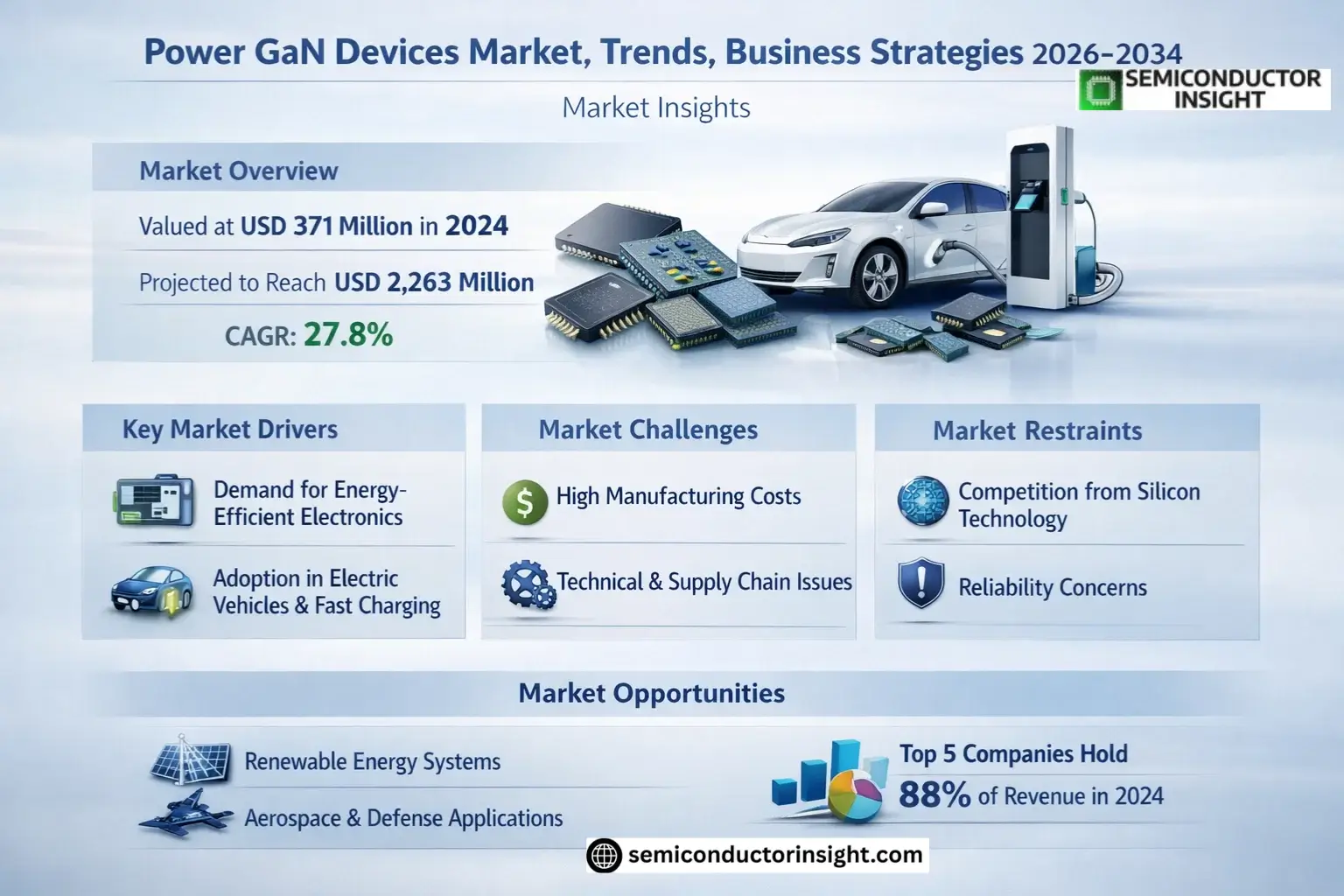

Global Power GaN Devices Market was valued at USD 371 million in 2024 and is projected to reach USD 2,263 million by 2032, exhibiting a CAGR of 27.8% during the forecast period.

Power GaN (Gallium Nitride) devices are semiconductor components designed for high-efficiency power electronics applications. These devices leverage the superior material properties of GaN, including higher breakdown voltage, faster switching speeds, and lower conduction losses compared to traditional silicon-based solutions. They are particularly suited for compact, high-performance systems in electric vehicles (EVs), data centers, renewable energy systems, and consumer electronics.

The market growth is driven by increasing demand for energy-efficient power solutions across industries. The automotive sector’s rapid electrification and the expansion of 5G infrastructure are key contributors to adoption. In 2024, the top five manufacturers including Infineon (GaN Systems), Navitas (GeneSiC), and Renesas Electronics (Transphorm) collectively held approximately 88% of global market revenue, indicating a concentrated competitive landscape.

MARKET DRIVERS

Rising Demand for Energy-Efficient Electronics

Global push for energy efficiency across consumer electronics, data centers, and industrial systems is a primary driver for the Power GaN Devices Market. Gallium Nitride (GaN) semiconductors offer superior performance over traditional silicon, enabling significant reductions in power losses and system size. This efficiency is critical for meeting stringent global energy regulations and consumer demand for longer battery life in portable devices.

Accelerated Adoption in Electric Vehicles and Fast Charging

The rapid expansion of the electric vehicle (EV) industry and the market for ultra-fast chargers creates substantial demand for Power GaN Devices. These devices are essential for developing compact, high-efficiency onboard chargers (OBCs) and DC-DC converters, which are crucial for reducing charging times and improving vehicle range. The ability of GaN technology to operate at higher frequencies and temperatures makes it ideal for these demanding applications.

Furthermore, ongoing advancements in 5G telecommunications infrastructure require robust and efficient power amplifiers and RF components, an area where Power GaN Devices are increasingly becoming the standard, further propelling market growth.

MARKET CHALLENGES

High Initial Manufacturing and Material Costs

Despite the performance advantages, the Power GaN Devices Market faces challenges related to cost. Fabricating GaN-on-Si or GaN-on-SiC wafers is more complex and expensive than producing standard silicon-based power devices. This higher cost can be a barrier to adoption, particularly in highly price-sensitive consumer market segments, slowing widespread implementation.

Other Challenges

Technical and Supply Chain Complexities

The relative novelty of GaN technology presents challenges in thermal management and circuit design, requiring specialized expertise. Additionally, establishing a resilient and scalable global supply chain for high-quality GaN substrates and epitaxial wafers remains a critical hurdle for manufacturers aiming to meet rising demand.

MARKET RESTRAINTS

Strong Competition from Mature Silicon Technologies

A significant restraint for the Power GaN Devices Market is the entrenched position of silicon-based power semiconductors like IGBTs and Super-Junction MOSFETs. These technologies benefit from decades of optimization, massive manufacturing scale, and deeply established design ecosystems, making them a cost-effective and low-risk choice for many applications, thereby limiting the immediate addressable market for GaN solutions.

Reliability and Longevity Perception

Although GaN HEMTs have demonstrated high reliability, the long-term field data is less extensive compared to silicon. Some designers in critical applications, such as automotive and industrial systems, remain cautious about adopting the newer technology until more extensive, long-term reliability data becomes widely available, acting as a temporary restraint on market penetration.

MARKET OPPORTUNITIES

Expansion into Renewable Energy Systems

The transition to renewable energy presents a major opportunity for the Power GaN Devices Market. GaN-based power converters are ideal for solar inverters and energy storage systems due to their high efficiency and ability to operate at high switching frequencies, which reduces the size and weight of magnetic components. This can lead to more compact and cost-effective renewable energy solutions.

Growth in Aerospace and Defense Applications

The unique properties of GaN, including its high-power density and radiation hardness, open significant opportunities in the aerospace and defense sectors. These applications require components that can perform reliably in extreme environments, and Power GaN Devices are increasingly being adopted for radar systems, electronic warfare, and satellite communications, representing a high-growth niche market.

Power GaN Devices Market Trends

Accelerated Market Growth and Dominant Applications

Global Power GaN Devices Market is in a phase of exceptionally rapid expansion. The market was valued at USD 371 million in 2024 and is projected to achieve a size of USD 2,263 million by 2032, representing a compound annual growth rate of 27.8%. The demand for high-efficiency, high-power-density electronics is the primary driver of this growth. This trend is most evident in the consumer electronics, automotive, and data center sectors, where the superior switching speeds and thermal performance of Power GaN Devices are critical for next-generation applications. The market is currently consolidated, with the top five global manufacturers accounting for approximately 88% of revenue in 2024.

Other Trends

Short-Term Adoption in Low-Power Applications

The immediate trend for the Power GaN Devices Market is accelerating adoption in a range of lower-power applications. GaN technology has only recently begun to penetrate the power supply market and is now seeing increased use in products such as consumer appliances, televisions, automotive subsystems, and residential networking equipment. This accelerated adoption is being driven by the need for more compact and efficient power conversion solutions in these high-volume markets.

Medium-Term Focus on High-Power Data Centers

A significant medium-term opportunity for the Power GaN Devices Market is in high-power applications, with artificial intelligence (AI) data centers representing a massive potential. Data center operators are actively seeking innovative power solutions to support the immense energy demands of AI workloads. While the potential is clear, the adoption of discrete GaN in these high-reliability systems has been slowed by technical challenges that industry players are working to overcome.

Long-Term Potential in Electric Vehicle Drivetrains

Looking at the long-term horizon, the Power GaN Devices Market has the potential to achieve power levels suitable for electric vehicle (EV) drivetrains. Analysts believe that GaN technology could offer a significantly lower-cost alternative to silicon carbide, which is currently the dominant technology in many EV power systems. This long-term trend represents a substantial future growth vector as the global automotive industry continues its shift towards electrification, expanding the total addressable market for Power GaN Devices substantially beyond current applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominance of Top Five Players Shapes High-Growth Sector

Global Power GaN Devices Market is characterized by a relatively concentrated competitive landscape, with the top five manufacturers accounting for approximately 88% of the global revenue share in 2024, highlighting a high degree of market consolidation. Infineon Technologies, following its strategic acquisition of GaN Systems, has solidified its leadership position. Other leading players, including Navitas Semiconductor (which acquired GeneSiC), Innoscience, Power Integrations, and Renesas Electronics (following its acquisition of Transphorm), command significant market influence. These established players benefit from extensive R&D capabilities, robust patent portfolios, and strong relationships with major OEMs across consumer electronics, automotive, and data center applications, creating a high barrier to entry for new competitors.

Beyond the dominant players, a number of other companies are carving out significant niches or growing their market presence. Texas Instruments, ROHM, and STMicroelectronics leverage their broad semiconductor expertise to compete in specific power application segments. Specialized pure-play GaN companies like Efficient Power Conversion Corporation (EPC) continue to drive innovation in high-performance discretes. The landscape is further populated by regional players such as China Resources Microelectronics Limited and Nexperia, as well as emerging entities like GaNPower and CorEnergy, which focus on cost-competitive solutions and specific regional markets, adding diversity to the competitive environment.

List of Key Power GaN Devices Companies Profiled

- Innoscience

- Navitas Semiconductor (GeneSiC)

- Efficient Power Conversion Corporation (EPC)

- Power Integrations, Inc.

- Infineon Technologies (GaN Systems)

- Renesas Electronics (Transphorm)

- Texas Instruments

- ROHM Semiconductor

- STMicroelectronics

- Nexperia

- China Resources Microelectronics Limited

- CorEnergy

- Qingdao Cohenius Microelectronics

- Hangzhou Silan Microelectronics

- Runxin Microelectronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

200V to 600V devices represent a pivotal segment balancing performance and versatility for widespread adoption. This voltage range is critically aligned with the operational requirements of consumer fast chargers, data center power supplies, and industrial motor drives, creating a substantial addressable market. Furthermore, the technological maturity and cost-effectiveness of devices in this bracket make them the preferred choice for system designers seeking to upgrade from traditional silicon without venturing into the more demanding high-voltage territory. Ongoing innovation is focused on enhancing the thermal performance and reliability within this crucial power band to support next-generation applications. |

| By Application |

|

Automotive and Mobility is an exceptionally dynamic application segment, driven by the global transition to electric vehicles. The inherent advantages of GaN, such as superior efficiency and power density, are critical for extending EV driving range and reducing charging times. Beyond the main drivetrain, which represents a longer-term opportunity, GaN is rapidly being adopted in onboard chargers and DC-DC converters. The stringent reliability and safety standards of the automotive industry are pushing manufacturers to develop robust GaN solutions, creating a high barrier to entry but also fostering intense competition and innovation among leading suppliers to capture this high-growth market. |

| By End User |

|

OEMs (Original Equipment Manufacturers) constitute the primary end-user segment, as they integrate GaN devices directly into their final products. These companies are driving demand by designing GaN into new generations of servers, EVs, and consumer electronics to achieve competitive advantages in performance and efficiency. OEMs typically engage in deep technical collaborations with GaN device makers to co-develop optimized solutions, influencing the roadmap of GaN technology. Their procurement strategies are increasingly focused on securing a stable supply of high-reliability components, which shapes the competitive landscape and partnership models within the GaN ecosystem. |

| By Device Configuration |

|

GaN System-in-Package (SiP) is emerging as a leading configuration, offering a compelling balance of performance and ease of integration. SiP solutions bundle the GaN transistor with drivers and sometimes passive components into a single package, which significantly simplifies the design-in process for engineers accustomed to silicon-based solutions. This reduces development time and mitigates the challenges associated with high-frequency layout, a common hurdle with discrete GaN HEMTs. As the market matures, the value proposition of SiP for achieving higher power density and reliability in space-constrained applications like laptop adapters and server power supplies is becoming increasingly recognized. |

| By Technology Maturity |

|

Growth Applications represent the most active and strategically important segment, characterized by accelerating adoption and significant future potential. This category includes AI data center power systems and various automotive subsystems, where the performance benefits of GaN are clear but system-level integration and reliability validation are ongoing. Market participants are heavily investing in R&D and forming strategic partnerships to overcome technical barriers and establish design wins in these areas. The competitive dynamics in this segment are intense, as success here is seen as a precursor to capturing the massive long-term opportunities in emerging high-power applications like EV drivetrains. |

Regional Analysis: Power GaN Devices Market

Asia-Pacific

Asia-Pacific’s dominance is underpinned by an unparalleled semiconductor manufacturing ecosystem. The region hosts the world’s largest concentration of foundries and packaging facilities specifically adapting to wide-bandgap semiconductors. This integrated supply chain, from substrate production to final device testing, reduces lead times and costs, providing a critical competitive edge for Power GaN device manufacturers operating within the region and attracting significant foreign investment.

The massive consumer electronics industry in Asia-Pacific is a primary driver for Power GaN devices. The push for smaller, more efficient fast chargers for smartphones, laptops, and other gadgets has been widely adopted. Local device makers are rapidly integrating GaN technology to achieve superior power density and efficiency, creating a vast and continuously growing domestic market that fuels local production and innovation cycles.

The region’s strong automotive industry, particularly in China and Japan, is accelerating the integration of Power GaN devices in electric vehicle powertrains, onboard chargers, and DC-DC converters. Additionally, industrial motor drives and renewable energy systems are increasingly utilizing GaN technology for improved efficiency. This diversification beyond consumer electronics ensures sustained long-term demand and technological advancement within the regional Power GaN Devices Market.

Supportive government policies across the Asia-Pacific, including subsidies, tax incentives, and national research programs focused on wide-bandgap semiconductors, have been instrumental. Countries are strategically positioning themselves in the global semiconductor value chain, with significant public and private investment flowing into GaN research and development. This proactive stance ensures the region remains at the cutting edge of Power GaN device technology.

North America

North America represents a highly innovative and technologically advanced market for Power GaN Devices, characterized by strong demand from the data center, aerospace, and defense sectors. The region is home to several leading GaN semiconductor developers and fabless companies that drive technological innovation. The need for high-efficiency power conversion in hyperscale data centers to reduce enormous energy consumption is a major growth driver. Furthermore, stringent energy regulations and a focus on electrification in the automotive and industrial sectors are pushing adoption. While manufacturing capacity is less concentrated than in Asia-Pacific, North America’s strength lies in its high-value, specialized applications and robust intellectual property landscape, making it a critical center for research and early adoption of next-generation GaN solutions.

Europe

The European Power GaN Devices Market is propelled by a strong emphasis on energy efficiency, renewable energy integration, and the automotive industry’s transition. Strict regulatory frameworks, such as the European Green Deal, incentivize the adoption of efficient power electronics in industrial equipment, consumer appliances, and automotive applications. The region has a well-established automotive sector that is rapidly electrifying, creating significant demand for GaN-based converters and inverters. European research institutions and companies are also active in developing GaN technology for use in solar inverters and wind turbines. Collaboration between academia and industry fosters innovation, positioning Europe as a key market focused on high-reliability and high-performance applications for Power GaN devices.

South America

The Power GaN Devices Market in South America is in a developing phase, with growth primarily driven by gradual modernization of telecommunications infrastructure and the nascent electric vehicle market. The adoption rate is slower compared to other regions, constrained by economic volatility and less developed local semiconductor industries. However, opportunities are emerging as countries invest in upgrading their power grids and expanding renewable energy capacity, where GaN devices can offer advantages. The market growth is expected to be incremental, relying heavily on imports and technology transfer from leading regions, with Brazil and Argentina showing the most potential for early adoption in specific industrial and telecommunications applications.

Middle East & Africa

The Middle East & Africa region presents a market for Power GaN Devices that is currently niche but holds long-term potential, particularly in the Middle East. Growth is linked to investments in telecommunications infrastructure, especially for 5G deployment, and diversification strategies away from hydrocarbon dependence towards technology and renewable energy. Countries like the UAE and Saudi Arabia are investing in smart city projects and data centers, which could drive future demand for efficient power solutions. In Africa, the market is very nascent, with adoption limited by infrastructure challenges. Overall, the region’s growth is anticipated to be gradual, focusing on specific high-value projects rather than widespread consumer or industrial adoption in the near term.

Report Scope

This market research report provides a comprehensive analysis of the Power GaN Devices, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as electric vehicles, data centers, consumer electronics, and renewable energy systems.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (GaN HEMT Discretes, GaN SiP, SoC), voltage range (Below 200V, 200V-600V, Above 600V), and application (Mobile & Consumer, Telecom, Automotive, Industrial, Defense).

- Regional Insights: Insights into market performance across North America, Europe, Asia, and other regions, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including Infineon, Navitas, Innoscience, and their product offerings, market share (top 5 held 88% in 2024), and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in high-efficiency power electronics, fast switching speeds, high power density applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth including EV adoption, data center demand, along with challenges in high-reliability system integration.

- Stakeholder Insights: Strategic insights for component suppliers, OEMs, investors regarding the evolving GaN ecosystem and opportunities in AI data centers and EV drivetrains.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Power GaN Devices?

-> Power GaN Devices Market was valued at USD 371 million in 2024 and is projected to reach USD 2,263 million by 2032, exhibiting a CAGR of 27.8% during the forecast period.

Which key companies operate in Power GaN Devices Market?

-> Key players include Infineon (GaN Systems), Navitas (GeneSiC), Innoscience, Power Integrations, Inc., Renesas Electronics (Transphorm), and Efficient Power Conversion Corporation (EPC), with top 5 companies holding 88% market share in 2024.

What is the growth rate (CAGR) of Power GaN Devices Market?

-> The market is projected to grow at a CAGR of 27.8% from 2024 to 2032.

What are the key applications of Power GaN Devices?

-> Key applications include electric vehicles, data centers, consumer electronics, renewable energy systems, telecom infrastructure, and industrial applications.

What are the emerging opportunities for GaN technology?

-> Emerging opportunities include AI data center power solutions, EV drivetrains, and high-power industrial applications where GaN offers cost advantages over silicon carbide.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...