Power Conversion Systems Market Insights

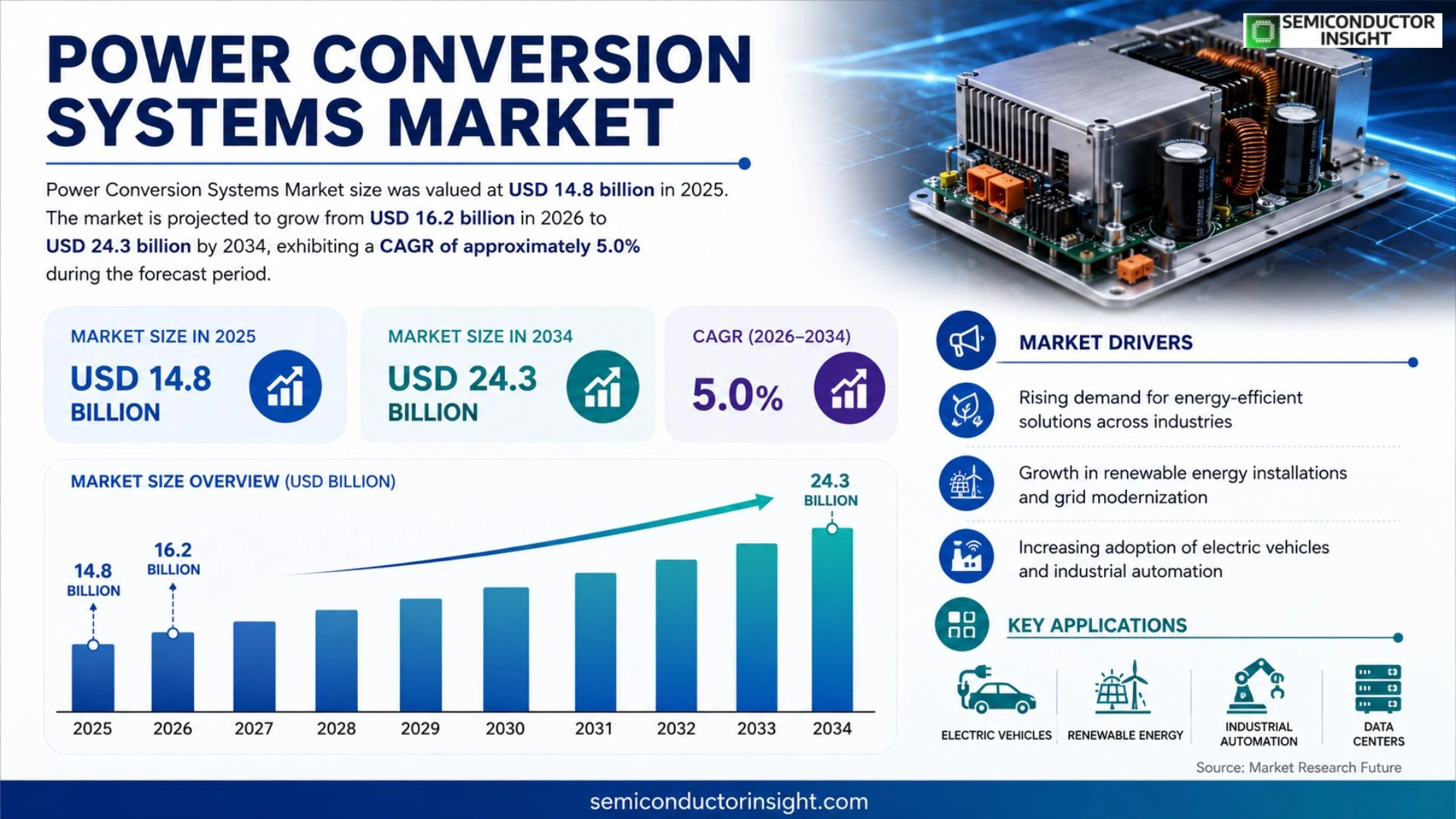

Global Power Conversion Systems Market size was valued at USD 14.8 billion in 2025. The market is projected to grow from USD 16.2 billion in 2026 to USD 24.3 billion by 2034, exhibiting a CAGR of approximately 5.0% during the forecast period.

Power conversion systems encompass a range of technologies that transform electrical energy from one form to another,such as AC‑to‑DC converters, DC‑to‑AC inverters, voltage regulators, and motor drives,enabling efficient power management across industrial automation, renewable energy integration, data‑center infrastructure, and transportation electrification.

The market is experiencing rapid growth because rising adoption of renewable energy sources drives demand for high‑efficiency converters, while expanding electric vehicle production fuels need for robust onboard power electronics. Furthermore, increasing emphasis on grid resilience and smart‑grid initiatives accelerates investments in advanced UPS and inverter solutions. However, supply‑chain constraints for semiconductor components pose challenges that manufacturers are addressing through diversified sourcing strategies.

MARKET DRIVERS

Growing Renewable Energy Integration

The rise of solar and wind installations is compelling utilities to adopt advanced power conversion equipment. Efficient conversion reduces losses and supports grid stability, making Power Conversion Systems Market a strategic focal point for renewable projects across North America and Europe.

Increasing Demand for Efficient DC/AC Conversion

Industrial automation and data‑center expansions rely on high‑performance converters to manage fluctuating loads. Compact designs and higher power density are driving OEM investments, accelerating market growth in Asia‑Pacific regions.

➤ Power Conversion Systems Market is projected to surpass $12 billion by 2030, fueled by grid modernization and electric vehicle charging infrastructure.

Regulatory incentives for low‑carbon technologies further boost adoption, encouraging manufacturers to innovate in silicon‑carbide (SiC) and gallium‑nitride (GaN) devices, which promise lower switching losses and longer lifespans.

MARKET CHALLENGES

High Initial Capital Expenditure

Deploying state‑of‑the‑art converters often requires substantial upfront investment, which can deter small‑scale operators. Cost‑benefit analyses frequently show long payback periods, limiting rapid market penetration in emerging economies.

Other Challenges

Supply Chain Constraints

Component shortages, particularly for SiC wafers, have created lead‑time extensions. Manufacturers must balance inventory levels against demand forecasts to avoid production bottlenecks.

MARKET RESTRAINTS

Stringent Safety and Compliance Standards

Regulatory frameworks mandate rigorous testing for electromagnetic interference and thermal performance. Non‑compliance can result in costly redesigns and market entry delays, especially in regions with evolving standards.

Additionally, legacy infrastructure in many utility networks lacks compatibility with next‑generation converters, necessitating costly retrofits that can slow adoption rates.

Finally, limited availability of skilled engineers proficient in high‑frequency power electronics adds a human‑resource restraint to scaling production.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Charging Networks

Global rollout of fast‑charging stations creates a sizable demand for high‑efficiency converters capable of handling rapid power surges. Modular architectures enable operators to scale capacity while maintaining reliability.

Another opportunity lies in the adoption of edge computing for industrial IoT, where low‑latency power conversion is critical. Companies that integrate advanced thermal management can capture niche segments.

Emerging markets in Africa and Latin America are beginning large‑scale renewable projects, representing untapped potential for suppliers willing to offer cost‑effective, robust solutions.

Power Conversion Systems Market Trends

Renewable Energy Integration Driving Growth

Power Conversion Systems Market is responding to the accelerated rollout of solar and wind installations worldwide. Operators require high‑efficiency AC‑to‑DC converters and DC‑to‑AC inverters that can handle variable generation while maintaining tight voltage regulation. Modern converters now achieve efficiencies above 98 %, reducing losses and supporting lower levelized electricity costs. This trend is reinforced by policy incentives that prioritize low‑carbon generation, prompting system designers to select converters with advanced maximum power point tracking and modular architectures that simplify scaling.

Other Trends

Electric Vehicle Electrification

Rapid expansion of electric vehicle (EV) production is creating sustained demand for robust onboard power electronics. Inverters and motor drives must deliver high torque density and thermal resilience to meet performance targets for both passenger and commercial fleets. Manufacturers are integrating silicon‑carbide (SiC) devices, which enable higher switching frequencies and smaller packaging, thereby improving vehicle range and reducing weight. The cumulative effect is a noticeable shift in component sourcing strategies toward suppliers that can guarantee stable SiC wafer supplies.

Smart‑Grid and UPS Advancements

Utilities are investing in smart‑grid solutions that require reliable, fast‑acting voltage regulators and uninterruptible power supply (UPS) systems. Power Conversion Systems Market is seeing increased adoption of grid‑forming inverters that can provide ancillary services such as frequency regulation and fault ride‑through. These devices are built with digital control loops that communicate with distribution management software, enabling real‑time optimization of power flow. As grid resilience becomes a priority, the market is also seeing growth in modular UPS designs that combine scalability with predictive maintenance analytics.

Supply‑chain constraints for semiconductor components remain a challenge across all segments. To mitigate risk, manufacturers are diversifying their supplier base, engaging in long‑term joint development programs, and stockpiling critical parts. These actions help stabilize production schedules and support consistent delivery of conversion equipment to end‑users. Overall, the convergence of renewable integration, EV electrification, and smart‑grid initiatives is shaping a dynamic environment for Power Conversion Systems Market, with technology innovation and supply‑chain agility emerging as key competitive factors.

COMPETITIVE LANDSCAPE

Key Industry Players

Power Conversion Systems Market Competitive Overview

Power Conversion Systems Market is dominated by a small cohort of global electrical manufacturers that combine deep semiconductor expertise with extensive system‑integration capabilities. ABB Ltd. leads the segment with a broad portfolio covering high‑voltage AC‑DC converters, modular multilevel converters for HVDC transmission, and scalable inverter platforms for renewable integration. Its strong R&D pipeline, worldwide service network, and strategic acquisitions in silicon‑carbide (SiC) device technology allow ABB to set pricing benchmarks and capture the majority of large‑scale utility and data‑center contracts. Siemens Energy and Schneider Electric follow closely, leveraging their legacy in industrial drives and grid‑level UPS solutions to present end‑to‑end conversion architectures that appeal to OEMs and system integrators seeking reliability and lifecycle support.

Beyond the top tier, a diverse set of niche innovators shapes specialized segments of the market. Delta Electronics and Mitsubishi Electric excel in compact, high‑efficiency DC‑DC converters for electric‑vehicle charging infrastructure, while Hitachi’s motor‑drive division targets robotics and factory‑automation applications. General Electric’s Power Conversion business focuses on gas‑turbine and offshore wind inverter modules, and Toshiba provides rugged AC‑DC solutions for rail‑transport electrification. Smaller but rapidly growing firms such as Power Electronics Inc., Phoenix Contact, and Eaton’s Power Quality group address emerging opportunities in micro‑grid stabilization and edge‑computing UPS equipment. The competitive landscape is further enriched by regional players like LG Electronics (South Korea) and Fujian Jiangmen Power (China), which deliver cost‑optimized modules for consumer‑grade power supplies and telecom back‑haul equipment.

List of Key Power Conversion Systems Companies Profiled

- ABB Ltd.

- Siemens Energy

- Schneider Electric

- Delta Electronics

- Mitsubishi Electric

- Hitachi Ltd.

- General Electric

- Toshiba Corporation

- Power Electronics Inc.

- Phoenix Contact

- Eaton Corporation

- LG Electronics

- Fujian Jiangmen Power

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AC‑to‑DC Converters

|

| By Application |

|

Renewable Energy Integration

|

| By End User |

|

Utilities

|

| By Technology |

|

Silicon Carbide (SiC) Power Devices

|

| By Deployment Scenario |

|

Remote Renewable Farms

|

Regional Analysis: North America

Significant investments are being made in upgrading and expanding the power grid to accommodate the growing demand and integrate renewable energy sources effectively. This includes the deployment of smart grid technologies and advanced transmission and distribution systems.

The burgeoning electric vehicle market is driving substantial growth in the demand for high-power charging infrastructure. This encompasses Level 2 chargers for home and workplace use, as well as DC fast chargers for public and commercial applications.

The industrial sector continues to rely on advanced power conversion systems for a wide range of applications, including automation, robotics, and manufacturing processes. The demand for energy-efficient and reliable power supplies is paramount in this segment.

Data centers are significant consumers of power, and efficient power conversion systems are crucial for ensuring reliable operation and minimizing energy costs. The increasing demand for cloud computing and data analytics is further driving this sector.

Europe

Europe is witnessing steady growth Power Conversion Systems Market. The region’s commitment to sustainability and the transition towards renewable energy sources are key drivers. Stringent environmental regulations and government support for green technologies are fueling investments in power electronics for solar, wind, and energy storage applications. The electrification of transportation, particularly in countries like Norway and the UK, is also contributing to the demand for EV charging infrastructure. Innovation in power conversion technologies, including wide bandgap semiconductors, is gaining traction in Europe. Businesses are focusing on developing energy-efficient and compact power solutions to meet the evolving needs of the market. The focus on smart grids and distributed energy resources is also creating new opportunities.

Asia-Pacific

The Asia-Pacific region represents the largest and fastest-growing market for Power Conversion Systems globally. Driven by rapid industrialization, increasing urbanization, and substantial investments in renewable energy, the demand for power electronics is surging. China, in particular, is a major market, with significant deployments of solar power and electric vehicles. India, Southeast Asia, and Australia are also experiencing strong growth. The region is witnessing a shift towards localized manufacturing and the development of domestic power conversion system providers. The demand for power solutions in emerging sectors like electric vehicles, data centers, and industrial automation is contributing significantly to market expansion.

South America

South America presents a promising market for Power Conversion Systems with considerable potential for growth. The region is actively pursuing renewable energy projects, particularly hydro and solar power, which necessitates robust power conversion infrastructure. The expanding electric vehicle market in countries like Brazil and Chile is also fueling demand for EV charging solutions. Industrial growth and infrastructure development further contribute to the market’s expansion. However, challenges such as infrastructure limitations and regulatory complexities can pose obstacles to growth.

Middle East & Africa

The Middle East & Africa region is experiencing increasing demand for Power Conversion Systems driven by infrastructure development, particularly in the power and energy sectors. Significant investments in renewable energy projects, such as solar and wind farms, are boosting the demand for solar inverters and grid integration solutions. The region’s growing transportation sector is also creating opportunities in EV charging infrastructure. Government initiatives promoting energy efficiency and sustainable development are further supporting market growth. The need for reliable power solutions in remote areas also presents a significant market opportunity.

Report Scope

This market research report provides a comprehensive analysis of the Power Conversion Systems Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Power Conversion Systems Market?

-> Power Conversion Systems Market was valued at USD 14.8 billion in 2025 and is expected to reach USD 24.3 billion by 2034, reflecting a CAGR of approximately 5.0% over the forecast period.

Which key companies operate Power Conversion Systems Market?

-> Key players are not enumerated in the provided reference.

What are the key growth drivers?

-> Key growth drivers include rising adoption of renewable energy sources, expanding electric‑vehicle production, increased emphasis on grid resilience and smart‑grid initiatives, and demand for high‑efficiency converters and advanced UPS/inverter solutions.

Which region dominates the market?

-> The reference does not specify a dominant region for Power Conversion Systems Market.

What are the emerging trends?

-> Emerging trends encompass high‑efficiency AC‑DC and DC‑AC conversion technologies, integration of AI/IoT for intelligent power management, and the development of robust semiconductor components to address supply‑chain constraints.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...