MARKET INSIGHTS

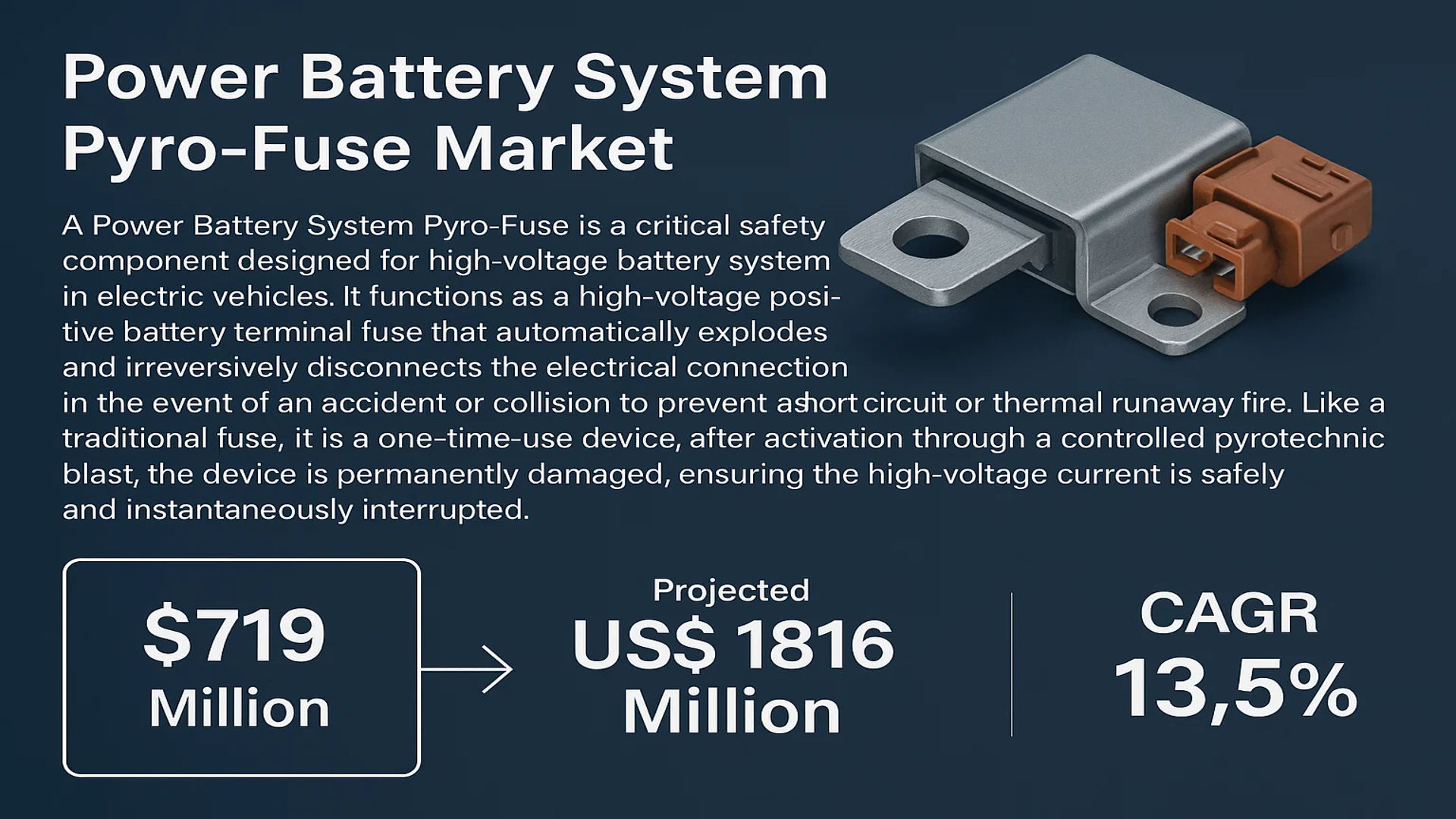

The global Power Battery System Pyro-Fuse Market was valued at 719 million in 2024 and is projected to reach US$ 1816 million by 2032, at a CAGR of 13.5% during the forecast period.

A Power Battery System Pyro-Fuse is a critical safety component designed for high-voltage battery systems in electric vehicles. It functions as a high-voltage positive battery terminal fuse that automatically explodes and irreversibly disconnects the electrical connection in the event of an accident or collision to prevent a short circuit or thermal runaway fire. Like a traditional fuse, it is a one-time-use device; after activation through a controlled pyrotechnic blast, the device is permanently damaged, ensuring the high-voltage current is safely and instantaneously interrupted.

The market’s robust growth is primarily fueled by the rapid global expansion of the electric vehicle (EV) industry, coupled with stringent automotive safety regulations mandating such fail-safe mechanisms. Furthermore, technological advancements in battery energy density and voltage levels are pushing the demand for more sophisticated protection solutions. The market is highly concentrated, with the top three vendors—Autoliv, Daicel, and Pacific Engineering Corporation (PEC)—collectively holding approximately 65% of the global revenue share in 2024, underscoring a market dominated by established players with advanced technological expertise.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Electric Vehicle Production to Accelerate Market Growth

The global electric vehicle market is experiencing unprecedented growth, with projections indicating that over 17 million electric vehicles will be sold annually by 2024, representing a 20% increase from the previous year. This surge in EV adoption directly drives demand for power battery system pyro-fuses, as these safety components are mandatory in high-voltage battery systems to prevent thermal runaway and electrical fires. Government mandates worldwide requiring enhanced safety features in electric vehicles further propel market expansion. For instance, regulations in major automotive markets now require multiple redundant safety systems in battery electric vehicles, with pyro-fuses serving as critical components in these safety architectures. The automotive industry’s transition toward 800V battery systems in premium electric vehicles creates additional demand for high-voltage pyro-fuses capable of handling increased electrical loads while maintaining safety performance.

Increasing Battery Capacity and High-Voltage System Adoption to Fuel Market Demand

Modern electric vehicles are adopting higher capacity battery systems, with average battery capacities increasing from 60 kWh to over 100 kWh in premium segments. This trend toward larger battery packs necessitates more robust safety systems, including advanced pyro-fuse technology. The industry-wide shift to 800V architecture, which reduces charging times and improves efficiency, requires pyro-fuses capable of operating at higher voltages while maintaining rapid disconnection capabilities. Market data indicates that over 35% of new electric vehicle models launched in 2024 feature 800V systems, creating substantial demand for high-voltage pyro-fuses rated above 700V. Furthermore, the growing adoption of battery energy storage systems for grid stabilization and renewable energy integration represents an additional growth vector for pyro-fuse manufacturers, as these systems require similar safety mechanisms to automotive applications.

Enhanced Safety Regulations and Standards to Drive Component Integration

Global automotive safety regulations are becoming increasingly stringent, particularly concerning electric vehicle battery safety. Regulatory bodies worldwide have implemented new standards requiring multiple independent safety systems in high-voltage battery packs. Pyro-fuses have emerged as critical components in these safety architectures due to their ability to provide ultra-fast circuit interruption in milliseconds, significantly faster than traditional electromechanical contactors. The implementation of UNECE R100 and other international safety standards has made pyro-fuses essential components in electric vehicle design. Automotive manufacturers are increasingly integrating pyro-fuses not only as primary safety devices but also as part of comprehensive battery management systems that monitor and protect against various fault conditions including short circuits, overcurrent events, and thermal overload situations.

MARKET RESTRAINTS

High Development and Certification Costs to Limit Market Penetration

The development and certification process for power battery system pyro-fuses involves substantial investment, with typical certification costs ranging between $2-5 million per product variant and requiring 18-24 months of testing and validation. These costs create significant barriers to entry for new market participants and limit the ability of smaller manufacturers to compete effectively. The stringent automotive safety standards require extensive testing under various environmental conditions, including temperature extremes, vibration, and mechanical stress, driving up development expenses. Additionally, the need for compatibility with various battery management systems and vehicle architectures necessitates custom engineering solutions, further increasing development costs. These financial barriers particularly affect manufacturers in price-sensitive markets and regions with developing electric vehicle industries, where cost competitiveness is crucial for market success.

Technical Complexity and Integration Challenges to Hinder Market Expansion

Power battery system pyro-fuses represent highly specialized components requiring precise integration with vehicle safety systems and battery management electronics. The technical complexity involved in ensuring reliable operation across various fault conditions, while maintaining compatibility with different vehicle architectures, presents significant challenges for widespread adoption. Integration issues are particularly pronounced in retrofit applications and secondary markets, where compatibility with existing systems must be carefully engineered. The need for specialized installation equipment and trained technicians further complicates market penetration, especially in regions with developing automotive service infrastructures. These technical barriers require substantial investment in training and equipment, which can delay market growth in price-sensitive segments and emerging markets where cost considerations often outweigh advanced safety features.

Supply Chain Constraints and Material Availability to Restrict Market Growth

The specialized materials required for pyro-fuse manufacturing, including specific explosive compounds and high-temperature resistant materials, face supply chain challenges that impact production scalability. Recent global supply chain disruptions have affected the availability of critical components, with lead times for certain specialized materials extending to 6-9 months. The automotive industry’s just-in-time manufacturing model creates additional pressure on pyro-fuse suppliers to maintain adequate inventory levels while managing the challenges of limited material availability. Furthermore, the specialized nature of these components means that manufacturing capacity is concentrated among a limited number of suppliers, creating potential bottlenecks as demand increases. These supply chain constraints particularly affect manufacturers seeking to expand production capacity or enter new market segments, as securing reliable material supplies requires long-term contracts and significant inventory investments.

MARKET OPPORTUNITIES

Emerging Applications in Energy Storage Systems to Create New Growth Avenues

The rapidly expanding grid-scale and residential energy storage markets present significant opportunities for power battery system pyro-fuse manufacturers. With global energy storage capacity projected to exceed 500 GWh by 2025, the demand for safety components in stationary battery systems is creating new market segments beyond automotive applications. Energy storage systems require similar safety mechanisms to electric vehicles, particularly in large-scale installations where battery failures could have significant consequences. The development of new safety standards for energy storage systems is driving adoption of pyro-fuse technology in this sector. Manufacturers are developing specialized pyro-fuse products optimized for stationary applications, featuring different triggering mechanisms and form factors suited to energy storage system requirements. This market diversification reduces dependence on automotive applications and provides additional revenue streams for manufacturers.

Advancements in Smart Pyro-Fuse Technology to Enable Premium Applications

Technological innovations are creating opportunities for smart pyro-fuse systems that integrate monitoring and communication capabilities. These advanced systems can provide real-time status information, enable predictive maintenance, and offer enhanced diagnostics capabilities. The integration of IoT connectivity and data analytics transforms pyro-fuses from passive safety components into active system elements that contribute to overall vehicle or system health monitoring. Market analysis indicates that smart safety components could command premium pricing of 30-40% above conventional pyro-fuses, creating significant revenue opportunities for innovative manufacturers. The development of these advanced systems requires collaboration between pyro-fuse manufacturers, semiconductor companies, and software developers, creating opportunities for strategic partnerships and technology licensing arrangements. These technological advancements are particularly relevant for premium vehicle segments and critical applications where enhanced safety and monitoring capabilities justify higher component costs.

Geographical Expansion and Emerging Market Penetration to Drive Future Growth

The accelerating adoption of electric vehicles in emerging markets presents substantial growth opportunities for pyro-fuse manufacturers. Markets in Southeast Asia, Latin America, and Eastern Europe are experiencing rapid electric vehicle adoption rates, with year-over-year growth exceeding 50% in some regions. Local manufacturing initiatives and government incentives are driving electric vehicle production in these regions, creating demand for safety components including pyro-fuses. Manufacturers are establishing local production facilities and distribution networks to capitalize on these growth markets, often in partnership with regional automotive suppliers. The development of cost-optimized pyro-fuse solutions tailored to the requirements and price points of emerging market vehicles represents a significant opportunity for market expansion. These initiatives are supported by regional safety regulations that are increasingly adopting international standards, creating consistent demand for certified safety components across global markets.

MARKET CHALLENGES

Intense Market Competition and Price Pressure to Challenge Profitability

The power battery system pyro-fuse market faces significant competitive pressures, with established manufacturers defending market share against new entrants offering lower-cost alternatives. Price competition has intensified as electric vehicle manufacturers seek to reduce costs, with component prices experiencing annual reductions of 5-8% despite increasing technical requirements. The concentration of purchasing power among major automotive OEMs enables them to negotiate aggressive pricing terms, squeezing manufacturer margins. Additionally, the emergence of manufacturers from regions with lower production costs is increasing price competition, particularly in price-sensitive market segments. These competitive pressures challenge manufacturers to maintain profitability while investing in research and development necessary to meet evolving technical requirements and safety standards.

Other Challenges

Technical Standardization Issues

The lack of universal technical standards for pyro-fuse interfaces and performance parameters creates compatibility challenges across different vehicle platforms and manufacturers. This standardization gap requires manufacturers to develop multiple product variants, increasing development costs and complicating inventory management. The absence of industry-wide standardization also hinders the development of second-source suppliers, as alternative components must undergo extensive validation testing before adoption.

Cybersecurity Concerns

The increasing integration of electronic control and monitoring capabilities in pyro-fuse systems introduces cybersecurity vulnerabilities that must be addressed. As these safety-critical components become connected elements in vehicle networks, they represent potential attack vectors that could compromise vehicle safety. Ensuring cybersecurity while maintaining functional safety represents a significant technical challenge requiring substantial investment in secure development practices and ongoing vulnerability management.

POWER BATTERY SYSTEM PYRO-FUSE MARKET TRENDS

Rapid Electrification of Automotive Fleets to Emerge as a Dominant Trend

The global transition towards electric vehicles is the primary catalyst driving the Power Battery System Pyro-Fuse market, with sales of battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs) projected to exceed 40 million units annually by 2030. This massive scale of vehicle production directly correlates with increased pyro-fuse adoption, as these safety devices are mandated in nearly all high-voltage automotive battery systems. Regulatory bodies across North America, Europe, and Asia-Pacific have implemented stringent safety standards requiring instantaneous high-voltage disconnection during collisions, creating a non-negotiable market for pyro-fuse technology. The automotive industry’s shift toward higher voltage architectures—with 800V systems becoming the new standard for premium EVs—further accelerates demand for advanced pyro-fuse solutions capable of handling increased electrical loads and faster disconnect times. This trend is particularly pronounced in China, where government mandates for EV adoption have resulted in the world’s largest electric vehicle market, accounting for approximately 58% of global EV sales in 2024.

Other Trends

Technological Innovation in Safety Systems

Manufacturers are developing increasingly sophisticated pyro-fuse systems that integrate with vehicle safety networks to provide predictive disconnection before impact occurs. These next-generation systems utilize sensor fusion technology combining accelerometer data, crash anticipation algorithms, and vehicle-to-vehicle communication to trigger pyro-fuse activation milliseconds before actual collision. The integration of artificial intelligence and machine learning has enabled these systems to distinguish between minor impacts and serious collisions with 99.7% accuracy, reducing unnecessary activation while ensuring reliable protection when needed. Recent developments include multi-stage pyro-fuse systems that can partially disconnect circuits during moderate impacts while maintaining full disconnection capability for severe collisions. This technological evolution addresses the automotive industry’s need for both safety and reliability, as unnecessary pyro-fuse activation renders the vehicle inoperable and requires expensive replacement.

Supply Chain Localization and Regional Manufacturing

The geopolitical landscape and supply chain disruptions have accelerated the trend toward regional manufacturing of critical safety components, including pyro-fuse systems. Automotive manufacturers are establishing local supply partnerships to mitigate risks associated with global supply chain dependencies, particularly following recent semiconductor shortages that affected automotive production worldwide. This trend is most evident in North America and Europe, where legislation such as the Inflation Reduction Act in the United States and the European Green Deal have created incentives for local component manufacturing. Major pyro-fuse manufacturers have responded by establishing production facilities in key automotive regions, with recent investments totaling approximately $450 million in new manufacturing capacity across North America, Europe, and Southeast Asia. This regionalization strategy not only addresses supply chain security concerns but also reduces transportation costs and lead times, which is particularly important for safety-critical components that automotive manufacturers require on just-in-time delivery schedules.

Increasing Voltage Requirements and System Integration

The automotive industry’s push toward higher efficiency and faster charging capabilities has driven the adoption of higher voltage battery systems, creating new requirements for pyro-fuse technology. Where 400V systems were once standard, 800V architectures are becoming increasingly common in premium electric vehicles, with some manufacturers developing 1000V systems for future models. This voltage escalation demands pyro-fuse systems capable of handling increased electrical stresses while maintaining instantaneous disconnect capabilities. The market has responded with innovative designs featuring advanced arc-quenching technologies and materials capable of withstanding voltages exceeding 1000V. Furthermore, integration with battery management systems has become more sophisticated, with pyro-fuses now serving as active safety components that communicate with vehicle control units rather than functioning as passive protection devices. This evolution enables more comprehensive safety strategies where pyro-fuse activation coordinates with other safety systems including airbag deployment, battery shutdown, and emergency responder notification systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global Power Battery System Pyro-Fuse market exhibits a semi-consolidated structure, characterized by the presence of dominant multinational corporations alongside emerging regional specialists. This landscape is shaped by intense technological innovation and strategic market positioning, driven primarily by the explosive growth in electric vehicle adoption. The market’s competitive dynamics are further influenced by stringent automotive safety regulations worldwide, which mandate the integration of high-reliability safety components like pyro-fuses.

Autoliv stands as the undisputed market leader, commanding a significant portion of global revenue. This dominance is attributable to their deep-rooted relationships with major automotive OEMs, extensive R&D capabilities focused on automotive safety systems, and a robust global manufacturing and supply chain network. Their pyro-fuse products are often integrated as part of broader safety system packages, providing a competitive edge.

Daicel Corporation and Pacific Engineering Corporation (PEC) also hold formidable market positions, collectively accounting for a major share with Autoliv. Daicel leverages its longstanding expertise in pyrotechnics and energetic materials, a core technology for pyro-fuses. PEC, a key Japanese player, is renowned for its precision engineering and strong foothold in the Asian automotive market, particularly with Japanese and Korean automakers.

Furthermore, established electrical component giants like Littelfuse, Eaton, and Mersen are strengthening their market presence. These companies compete by leveraging their vast experience in circuit protection technology, broad product portfolios, and established distribution channels. Their growth strategy often involves significant investments in developing next-generation pyro-fuses with faster response times and higher voltage ratings to meet the evolving demands of 800V battery architectures.

Meanwhile, European specialists such as Miba AG and MTA Group are carving out significant niches, particularly within the premium and performance EV segments. Their focus on high-performance, reliability-critical components resonates with European OEMs. Chinese manufacturers, including Xi’an Sinofuse Electric and Hangzhou Chauron Technology, are rapidly expanding their capabilities and market share, competing aggressively on cost and catering to the massive domestic EV market while increasingly looking toward global exports.

List of Key Power Battery System Pyro-Fuse Companies Profiled

- Autoliv (Sweden)

- Daicel Corporation (Japan)

- Pacific Engineering Corporation (PEC) (Japan)

- Littelfuse, Inc. (U.S.)

- Mersen (France)

- Eaton (Ireland)

- Miba AG (Austria)

- MTA Group (Italy)

- Xi’an Sinofuse Electric Co., Ltd. (China)

- Joyson Electronic (China)

- Hangzhou Chauron Technology Co., Ltd. (China)

Segment Analysis:

By Type

High Voltage Segment Dominates the Market Due to Critical Safety Requirements in Premium Electric Vehicles

The market is segmented based on type into:

- High Voltage (Above 700V)

- Mid Voltage (400V-700V)

- Low Voltage (Below 400V)

By Application

BEV Segment Leads Due to High-Voltage Battery Systems and Stringent Safety Regulations

The market is segmented based on application into:

- BEV (Battery Electric Vehicle)

- HEV (Hybrid Electric Vehicle)

By End User

OEMs Dominate the Market as Pyro-Fuses are Integrated During Vehicle Manufacturing

The market is segmented based on end user into:

- OEMs (Original Equipment Manufacturers)

- Aftermarket

By Vehicle Type

Passenger Vehicles Hold the Largest Share Owing to Mass Adoption of Electric Cars

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Commercial Vehicles

Regional Analysis: Power Battery System Pyro-Fuse Market

Asia-Pacific

The Asia-Pacific region dominates the global Power Battery System Pyro-Fuse market, accounting for over 55% of global revenue in 2024. This leadership position is driven by China’s massive electric vehicle production, which reached approximately 9.58 million units in 2023, representing nearly 60% of global EV output. Government mandates for vehicle safety systems, particularly in China’s New Energy Vehicle sector, coupled with aggressive manufacturing expansion by local battery producers like CATL and BYD, create substantial demand for pyro-fuse technology. While Japanese manufacturers like Daicel and Pacific Engineering Corporation maintain technological leadership, Chinese suppliers including Xi’an Sinofuse Electric and Hangzhou Chauron Technology are rapidly gaining market share through cost-competitive solutions. The region’s growth is further accelerated by Southeast Asian nations developing their EV ecosystems, though technological adoption varies significantly across markets.

Europe

Europe represents the second-largest market for Power Battery System Pyro-Fuses, characterized by stringent automotive safety regulations and high adoption rates of premium electric vehicles. The EU’s General Safety Regulation, which mandates specific safety features for vehicles, has been a significant driver for pyro-fuse integration. Germany, as the automotive engineering hub, hosts several key manufacturers and research facilities developing advanced pyro-fuse technologies. European automakers’ focus on high-performance EVs with battery systems exceeding 800V creates demand for sophisticated protection systems. However, the market faces challenges from complex certification processes and competition from established Asian suppliers. Recent developments include collaborations between European automakers and fuse manufacturers to develop next-generation protection systems for upcoming EV platforms.

North America

North America’s pyro-fuse market is growing steadily, driven by increasing EV adoption and stringent safety standards from the National Highway Traffic Safety Administration. The United States represents the largest sub-market, with Tesla’s extensive vehicle production and other automakers’ EV initiatives creating consistent demand. The region’s preference for larger battery capacities and higher voltage systems in trucks and SUVs necessitates robust protection solutions. While North American manufacturers like Littelfuse and Eaton have strong positions in traditional fusing, they face competition from European and Japanese pyro-fuse specialists. Recent infrastructure investments through legislation like the Inflation Reduction Act are expected to boost domestic battery production, subsequently increasing demand for localized safety components including pyro-fuses.

South America

The South American market for Power Battery System Pyro-Fuses remains nascent but shows promising growth potential. Brazil and Argentina are gradually developing their EV markets, though adoption rates remain low compared to global standards. The region currently relies heavily on imported components, with limited local manufacturing capabilities for advanced automotive safety systems. Economic volatility and infrastructure challenges hinder rapid market expansion, but increasing environmental awareness and government incentives for electric mobility are creating opportunities. Market growth is primarily driven by premium vehicle segments and fleet electrification projects in major urban centers. International suppliers are establishing distribution networks in anticipation of future market development.

Middle East & Africa

This region represents an emerging market with significant long-term potential but currently minimal market share. Development is concentrated in wealthier Gulf Cooperation Council countries, particularly the United Arab Emirates and Saudi Arabia, where government initiatives promote electric vehicle adoption as part of broader economic diversification strategies. The African continent shows sporadic development, primarily in South Africa and Morocco, where automotive manufacturing hubs are beginning to incorporate electric models. The market faces challenges including limited charging infrastructure, economic constraints, and preference for cost-effective vehicles over premium safety features. However, increasing urbanization and environmental concerns are gradually driving interest in advanced vehicle safety systems, including battery protection technologies.

Report Scope

This market research report provides a comprehensive analysis of the global Power Battery System Pyro-Fuse market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by voltage type (High, Mid, Low), application (BEV, HEV), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging safety technologies, integration with battery management systems, and evolving automotive safety standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, automotive OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Power Battery System Pyro-Fuse Market?

-> Power Battery System Pyro-Fuse Market was valued at 719 million in 2024 and is projected to reach US$ 1816 million by 2032, at a CAGR of 13.5% during the forecast period.

Which key companies operate in Global Power Battery System Pyro-Fuse Market?

-> Key players include Autoliv, Daicel, Pacific Engineering Corporation (PEC), Littelfuse, Mersen, Eaton, Miba AG, MTA Group, Xi’an Sinofuse Electric, Joyson Electronic, and Hangzhou Chauron Technology.

What are the key growth drivers?

-> Key growth drivers include rapid expansion of electric vehicle production, stringent automotive safety regulations, and increasing demand for high-voltage battery safety solutions.

Which region dominates the market?

-> Asia-Pacific dominates the market due to concentration of EV manufacturing and battery production facilities, particularly in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of smart pyro-fuses with integrated sensors, miniaturization of components, and increased adoption in commercial electric vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...