MARKET INSIGHTS

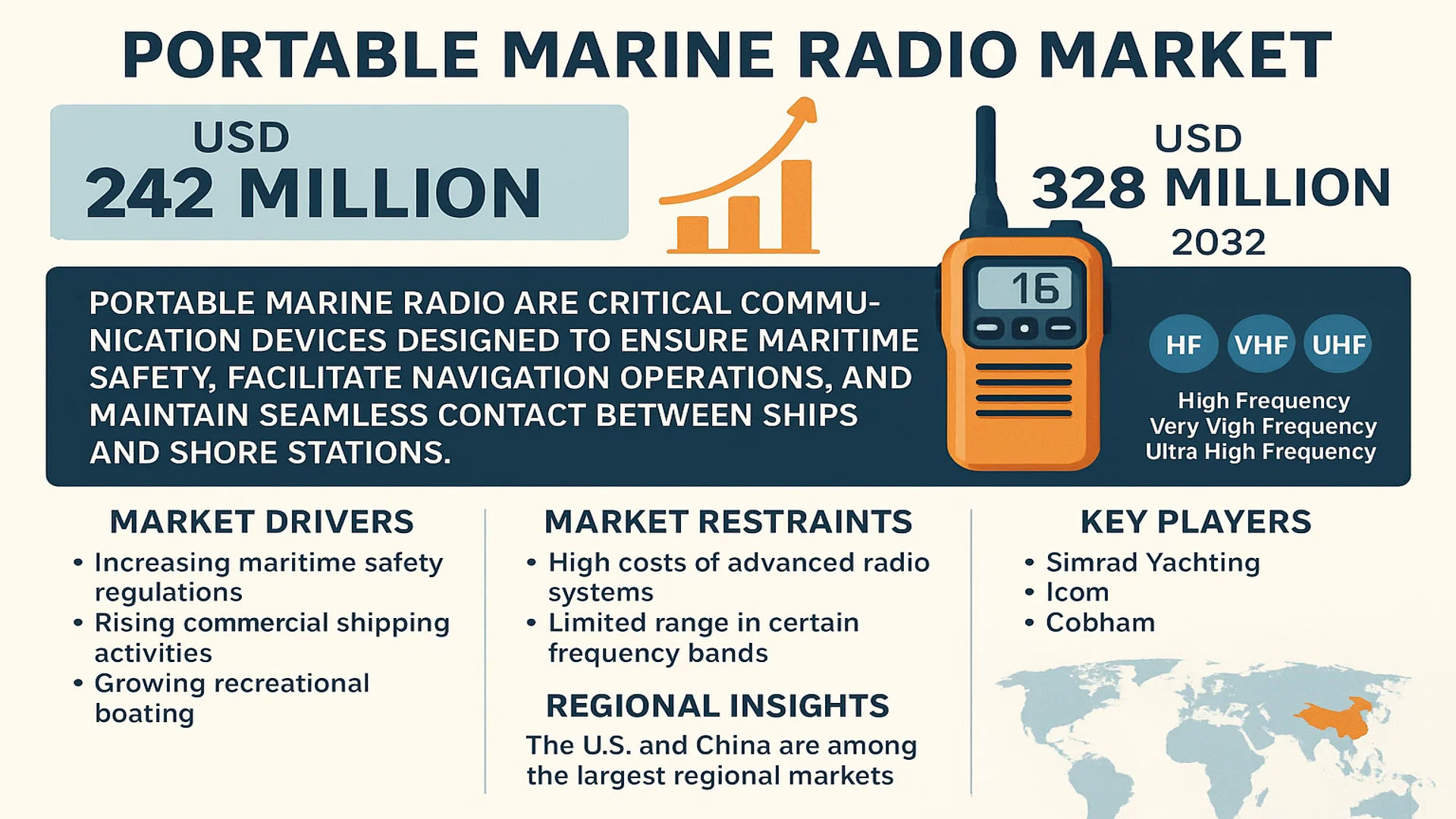

The global Portable Marine Radio Market was valued at 242 million in 2024 and is projected to reach US$ 328 million by 2032, at a CAGR of 4.5% during the forecast period.

Portable marine radios are critical communication devices designed to ensure maritime safety, facilitate navigation operations, and maintain seamless contact between ships and shore stations. These radios operate across multiple frequency bands, including HF (High Frequency), VHF (Very High Frequency), and UHF (Ultra High Frequency), each serving distinct communication needs in marine environments.

Market growth is driven by increasing maritime safety regulations, rising commercial shipping activities, and growing recreational boating. However, challenges such as high costs of advanced radio systems and limited range in certain frequency bands may restrain adoption. Key players like Simrad Yachting, Icom, and Cobham dominate the market with innovations in waterproofing, GPS integration, and emergency signaling features. The U.S. and China are among the largest regional markets, contributing significantly to global demand.

MARKET DYNAMICS

MARKET DRIVERS

Mandatory Maritime Safety Regulations to Accelerate Market Adoption

The implementation of stringent maritime safety regulations by organizations like the International Maritime Organization (IMO) and national coast guards is driving the adoption of portable marine radios. In 2023, over 90% of commercial vessels globally were required to carry VHF radios under SOLAS (Safety of Life at Sea) conventions, creating ongoing demand for replacement and upgraded units. Modern regulations increasingly mandate digital selective calling (DSC) capabilities, pushing vessel operators towards newer, compliant models. This regulatory pressure isn’t limited to commercial shipping – many recreational boating jurisdictions now require portable marine radios for vessels over specific lengths or operating beyond coastal boundaries.

Growth in Marine Tourism and Recreational Boating to Stimulate Demand

The global marine tourism industry, valued at over $150 billion, continues to expand with increased participation in recreational boating, fishing charters, and cruise activities. North America and Europe account for approximately 65% of recreational boat sales, each requiring marine radios for safety compliance and operational coordination. As adventure tourism grows in coastal regions, demand for compact, waterproof portable units suitable for small craft and water sports has risen sharply. Dive operators, fishing guides, and coastal tour businesses increasingly equip staff with portable marine radios as standard safety equipment, driving both initial purchases and replacement cycles every 3-5 years due to harsh marine environments.

Technological Advancements Enhancing Product Capabilities

Recent innovations in portable marine radio technology are removing traditional adoption barriers while creating new use cases. Modern units now integrate GPS positioning, Bluetooth smartphone pairing, and emergency beacon functions in compact form factors weighing under 500g. Battery technology improvements have extended operating times to 24+ hours on single charges, with solar charging options gaining traction. Waterproof ratings have improved to IPX8 standards, allowing full submersion protection crucial for marine environments. These advancements address historical complaints about bulk, complexity, and limited functionality that previously discouraged widespread adoption among casual boaters and marine professionals alike.

MARKET RESTRAINTS

High Product Costs and Certification Expenses Limiting Market Penetration

While portable marine radios serve critical safety functions, their premium pricing creates adoption barriers, particularly in developing maritime markets. Certified marine-grade VHF radios typically cost 3-5 times more than comparable land mobile radios due to specialized waterproofing, shock resistance, and certification requirements. Type approval processes from regulatory bodies can add 15-20% to product development costs, expenses ultimately passed to end-users. In price-sensitive markets like Southeast Asia and Africa, many small-scale fishermen and boat operators resort to uncertified alternatives that fail to meet safety standards, creating both regulatory non-compliance issues and potential safety hazards in emergencies.

Competition from Satellite Communication Devices Challenging Traditional Radio Use

The marine communication market faces growing competition from satellite messaging devices and hybrid communication systems offering global coverage beyond traditional VHF range limitations. While marine radios maintain advantages for local coordination and regulatory compliance, recreational boaters and commercial operators increasingly supplement them with satellite systems. This trend is particularly pronounced among offshore operators and adventure tourists who require communication capabilities beyond coastal VHF networks. The annual growth rate of satellite emergency notification devices has exceeded 30%, gradually eroding potential market expansion opportunities for traditional marine radios in certain segments.

Regulatory Fragmentation Creating Market Complexity

Differing national and regional certification requirements for marine radio equipment create manufacturing challenges and market access barriers. Products often require extensive redesign and retesting to meet varying technical standards across major boating markets like the US, EU, and Asia-Pacific regions. These regulatory inconsistencies particularly disadvantage smaller manufacturers lacking resources for multi-market compliance, thereby limiting product availability and innovation. Recent efforts toward international standards harmonization have made progress but still fall short of creating truly uniform global requirements, maintaining operational complexities for industry participants.

MARKET OPPORTUNITIES

Integration with Digital Navigation Systems Creating New Product Ecosystems

The convergence of marine radios with digital navigation and vessel monitoring systems presents significant growth opportunities. Modern marine electronics increasingly utilize NMEA 2000 networks to integrate radios with chartplotters, AIS transponders, and engine monitoring systems. This integration allows advanced features like automatic distress signaling with position data, voice communication logging, and fleet coordination – capabilities driving premium product demand. As recreational and commercial vessels continue adopting comprehensive digital navigation suites, compatible marine radios offering seamless system integration command substantial market premiums and replacement cycles aligned with other bridge electronics.

Expanding Offshore Renewable Energy Sector Driving Professional Demand

The rapid growth of offshore wind farms and other marine renewable energy installations creates specialized communication needs that portable marine radios are uniquely positioned to address. Construction and maintenance operations across wind farms require reliable, waterproof communications for crew coordination and emergency situations. Unlike traditional marine applications where radio use is often limited to emergencies, offshore energy crews utilize radios for continuous operational communications, creating both higher unit volumes and accelerated replacement cycles. Industry projections suggest offshore wind capacity will triple globally by 2030, indicating sustained demand growth from this emerging professional marine sector.

Emerging Economies Present Untapped Growth Potential

Developing coastal nations represent the next frontier for portable marine radio adoption as maritime safety awareness grows and regulatory frameworks mature. Countries with expanding commercial fishing fleets and growing middle-class participation in recreational boating – particularly in Southeast Asia and Latin America – show accelerating demand for safety equipment that previously saw limited uptake. While price sensitivity remains a challenge, manufacturers addressing these markets with value-engineered products meeting basic safety requirements without premium features can capture first-time buyer segments. Localized distribution partnerships and government safety initiatives further enhance market access opportunities in these developing regions.

MARKET CHALLENGES

Durability and Reliability Issues in Harsh Marine Environments

Despite technological advances, portable marine radios continue facing operational challenges in real-world marine conditions. Saltwater corrosion, UV degradation, and physical impacts from marine operations remain leading causes of premature product failure. Even with IPX8 ratings, constant exposure to spray, immersion, and temperature extremes significantly shortens operational lifespans compared to land-based communication equipment. These durability challenges not only impact user satisfaction but also create ongoing warranty and support costs for manufacturers balancing ruggedness requirements against consumer expectations for compact, lightweight designs.

Limited Consumer Awareness of Proper Usage Protocols

A persistent industry challenge involves the gap between equipment ownership and proper operational knowledge among recreational users. Surveys indicate less than 40% of recreational boaters with marine radios can properly use DSC emergency functions or understand channel protocols. This knowledge deficit leads to improper use that can compromise safety systems and create radio traffic congestion. Manufacturers face ongoing challenges educating users through documentation and training while maintaining simple, intuitive product interfaces – a balance difficult to achieve with increasingly complex feature sets required by modern safety standards and consumer expectations.

Supply Chain Vulnerabilities Affecting Product Availability

The marine electronics sector continues experiencing supply chain disruptions affecting component availability and production timelines. Specialized waterproof connectors, marine-grade plastics, and radio frequency components remain subject to extended lead times and price volatility following global supply chain realignments. These challenges particularly impact smaller manufacturers lacking bulk purchasing power or alternative sourcing options. With average production lead times increasing from 8 to 16 weeks industry-wide, maintaining consistent product availability across global markets has become an ongoing operational challenge affecting sales growth potential and customer satisfaction metrics.

PORTABLE MARINE RADIO MARKET TRENDS

Integration of Advanced Communication Technologies Driving Market Growth

The global portable marine radio market, valued at $242 million in 2024, is witnessing robust growth due to advancements in marine communication technologies. One of the most notable trends is the increasing adoption of Digital Selective Calling (DSC) and Automatic Identification System (AIS) capabilities in portable marine radios. These features enhance maritime safety by enabling automated distress signaling and real-time vessel tracking. Regulatory mandates from organizations such as the International Maritime Organization (IMO) are accelerating this shift, with over 70% of commercial vessels now integrating DSC-compliant radios. Additionally, manufacturers are incorporating waterproof, shockproof, and compact designs, catering to the demands of maritime professionals and recreational boaters alike.

Other Trends

Rising Demand for VHF Radios in Recreational Boating

The VHF (Very High Frequency) segment holds the largest market share, accounting for nearly 55% of total sales, driven by its widespread use in both commercial shipping and recreational boating. The recreational sector is experiencing a surge in demand, particularly in North America and Europe, due to increasing water-based leisure activities. Over 12 million recreational boats operate in the U.S. alone, emphasizing the necessity for reliable communication devices. Advanced features like built-in GPS and Bluetooth connectivity are further enhancing user convenience, making modern VHF radios indispensable for safety and navigation.

Expansion of Maritime Safety Regulations Boosting Market Potential

Stringent maritime safety regulations are significantly influencing the portable marine radio market. Countries with extensive coastlines, such as China and Indonesia, are implementing stricter vessel communication requirements to prevent accidents and improve search-and-rescue operations. The Global Maritime Distress and Safety System (GMDSS) mandates the use of marine radios on all commercial vessels, driving steady demand in the shipping industry. Furthermore, emerging economies are investing in coastal surveillance and emergency response infrastructure, contributing to market growth. This trend is expected to continue, with the Asia-Pacific region projected to register the highest CAGR of 5.8% from 2024 to 2032 due to expanding maritime trade and domestic boating activities.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Product Innovation and Safety Compliance Drive Market Leadership

The global portable marine radio market displays moderate consolidation, with established brands and emerging specialists competing across regions. Icom Inc. leads the market with approximately 25% revenue share in 2024, largely due to its proprietary Digital Selective Calling (DSC) technology and extensive distribution network covering 150+ countries. The company’s IC-M94D handheld VHF model remains an industry benchmark for waterproof performance and GPS integration.

Standard Horizon (Yaesu) and Jotron AS collectively hold 35% market share, distinguished by their focus on ruggedized designs meeting IPX8 standards. Recent innovations include battery life optimization reaching 20+ hours in continuous operation and integrated Automatic Identification System (AIS) receivers—critical features driving adoption among commercial shipping operators.

The competitive intensity increased notably after Cobham Marine launched its SAILOR 6215 VHF series in 2023, featuring AI-based channel scanning and 40% faster distress signal transmission. Meanwhile, ACR Electronics gained traction through strategic partnerships with coast guard agencies across North America and Europe, reinforcing brand credibility in safety-critical applications.

List of Key Portable Marine Radio Manufacturers

- Icom Inc. (Japan)

- Standard Horizon (U.S.)

- Jotron AS (Norway)

- Simrad Yachting (Norway)

- Cobham Marine (UK)

- ACR Electronics (U.S.)

- McMurdo Group (UK)

- Entel UK Ltd.

- GME Electrophones (Australia)

- Ocean Signal (UK)

Regional specialists like GME Electrophones dominate Australasia with localized frequency compliance, while European Union’s updated Radio Equipment Directive (RED) 2023 compelled manufacturers to accelerate R&D investments—particularly in interference reduction technologies. The market’s evolution toward hybrid HF/VHF systems suggests upcoming consolidation as smaller players struggle with R&D scalability.

Segment Analysis:

By Type

VHF Segment Dominates the Market Due to its Reliable Short-Range Communication Capabilities

The market is segmented based on type into:

- HF (High Frequency)

- Subtypes: Long-range communication systems and others

- VHF (Very High Frequency)

- Subtypes: Fixed and handheld models

- UHF (Ultra High Frequency)

- Subtypes: Military-grade and commercial systems

By Application

Ship Shore Communication Segment Leads Due to Mandatory Regulatory Requirements

The market is segmented based on application into:

- Ship to Ship Communication

- Ship Shore Communication

- Ship Aircraft Communication

- Emergency Communication

By End User

Commercial Shipping Segment Holds the Largest Share Owing to High Volume Usage

The market is segmented based on end user into:

- Commercial Shipping

- Subtypes: Cargo vessels, tankers, and others

- Defense

- Recreational Boating

- Fishing Vessels

By Technology

Digital Radios Gain Momentum Due to Enhanced Features and Reliability

The market is segmented based on technology into:

- Analog

- Digital

- Subtypes: DSC (Digital Selective Calling), AIS, and others

- Hybrid

Regional Analysis: Portable Marine Radio Market

North America

The North American market for portable marine radios is driven by strict maritime safety regulations and thriving recreational boating activities. The United States Coast Guard mandates VHF radios for most commercial vessels, creating steady demand. With over 12 million registered recreational boats in the U.S. alone, consumer adoption of waterproof and GPS-integrated models is rising. Advanced technologies like DSC (Digital Selective Calling) are gaining traction due to enhanced emergency communication features. While established players dominate, price sensitivity in the recreational segment presents a challenge for premium brands. The region also sees gradual adoption of UHF radios for short-range communication in inland waterways.

Europe

Europe’s portable marine radio market benefits from stringent Marine Equipment Directive (MED) compliance, which enforces product certification for maritime safety. The region’s strong focus on coastal tourism and fishing industries sustains demand, particularly in Mediterranean and Nordic countries. VHF radios with AIS (Automatic Identification System) integration are increasingly popular among commercial fleets. However, market growth faces constraints from high device costs and competition from non-certified low-cost alternatives in price-sensitive markets. The EU’s push for standardization of maritime communication protocols presents long-term opportunities for compliant manufacturers.

Asia-Pacific

Asia-Pacific represents the fastest-growing region, driven by expanding fishing industries, naval modernization, and coastal trade. Countries like China, Japan, and India are investing in port security and maritime infrastructure, boosting demand for ruggedized and long-range HF/VHF radios. While the commercial sector prefers durable, feature-rich models, recreational users prioritize affordability, leading to a two-tier market structure. The region’s susceptibility to monsoon seasons and natural disasters has also increased demand for emergency-capable radios. However, inconsistent enforcement of maritime communication regulations across some countries creates fragmentation.

South America

South America’s market is characterized by nascent growth, with Brazil and Argentina leading demand due to expanding commercial fishing and coastal trade activities. The region shows preference for mid-range VHF radios due to balanced cost-to-performance needs. However, economic instability and limited regulatory oversight in some countries hinder adoption of advanced marine communication systems. The recreational boating sector remains underdeveloped outside of tourist hotspots, though increasing coastal tourism presents future opportunities. Manufacturers face challenges in distribution and after-sales support across the region’s fragmented markets.

Middle East & Africa

This region presents emerging opportunities focused primarily on port operations and oil & gas maritime activities along the Persian Gulf and Red Sea. Gulf Cooperation Council (GCC) countries are investing in maritime security and navigation safety, driving demand for high-performance marine radios with encryption features. Africa’s market remains constrained by limited recreational boating culture and budget restrictions outside of South Africa’s coastal regions. While piracy concerns in key shipping lanes have increased radio adoption among commercial vessels, counterfeit products remain a challenge for legitimate manufacturers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Portable Marine Radio markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Portable Marine Radio market was valued at USD 242 million in 2024 and is projected to reach USD 328 million by 2032, at a CAGR of 4.5%.

- Segmentation Analysis: Detailed breakdown by product type (HF, VHF, UHF), application (Ship-to-Ship, Ship-Shore, Ship-Aircraft), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market size is estimated at significant value in 2024, while China shows rapid growth potential.

- Competitive Landscape: Profiles of leading market participants including Simrad Yachting, Icom, Jotron, Cobham, and Standard Horizon, covering their product portfolios, market share (top five players held significant share in 2024), and strategic developments.

- Technology Trends & Innovation: Assessment of emerging communication technologies, digital transformation in marine radios, and evolving maritime safety standards.

- Market Drivers & Restraints: Evaluation of factors such as increasing maritime safety regulations, growing commercial shipping activities, alongside challenges like spectrum allocation issues.

- Stakeholder Analysis: Insights for marine electronics manufacturers, ship operators, regulatory bodies, and investors regarding market opportunities and strategic positioning.

Primary and secondary research methods are employed, including interviews with industry experts, data from maritime authorities, and analysis of manufacturer reports to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Portable Marine Radio Market?

-> Portable Marine Radio Market was valued at 242 million in 2024 and is projected to reach US$ 328 million by 2032, at a CAGR of 4.5% during the forecast period.

Which key companies operate in Global Portable Marine Radio Market?

-> Key players include Simrad Yachting, Jotron, Icom, Cobham, McMurdo, ACR, Standard Horizon, and Ocean Signal, among others.

What are the key growth drivers?

-> Key growth drivers include increasing maritime safety regulations, growth in commercial shipping, and rising recreational boating activities.

Which region dominates the market?

-> North America holds significant market share, while Asia-Pacific shows the fastest growth potential.

What are the emerging trends?

-> Emerging trends include integration of GPS/DSC capabilities, waterproof rugged designs, and digital selective calling (DSC) technology.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...