Polymer hybrid capacitor for automotive LED headlamp Market Insights

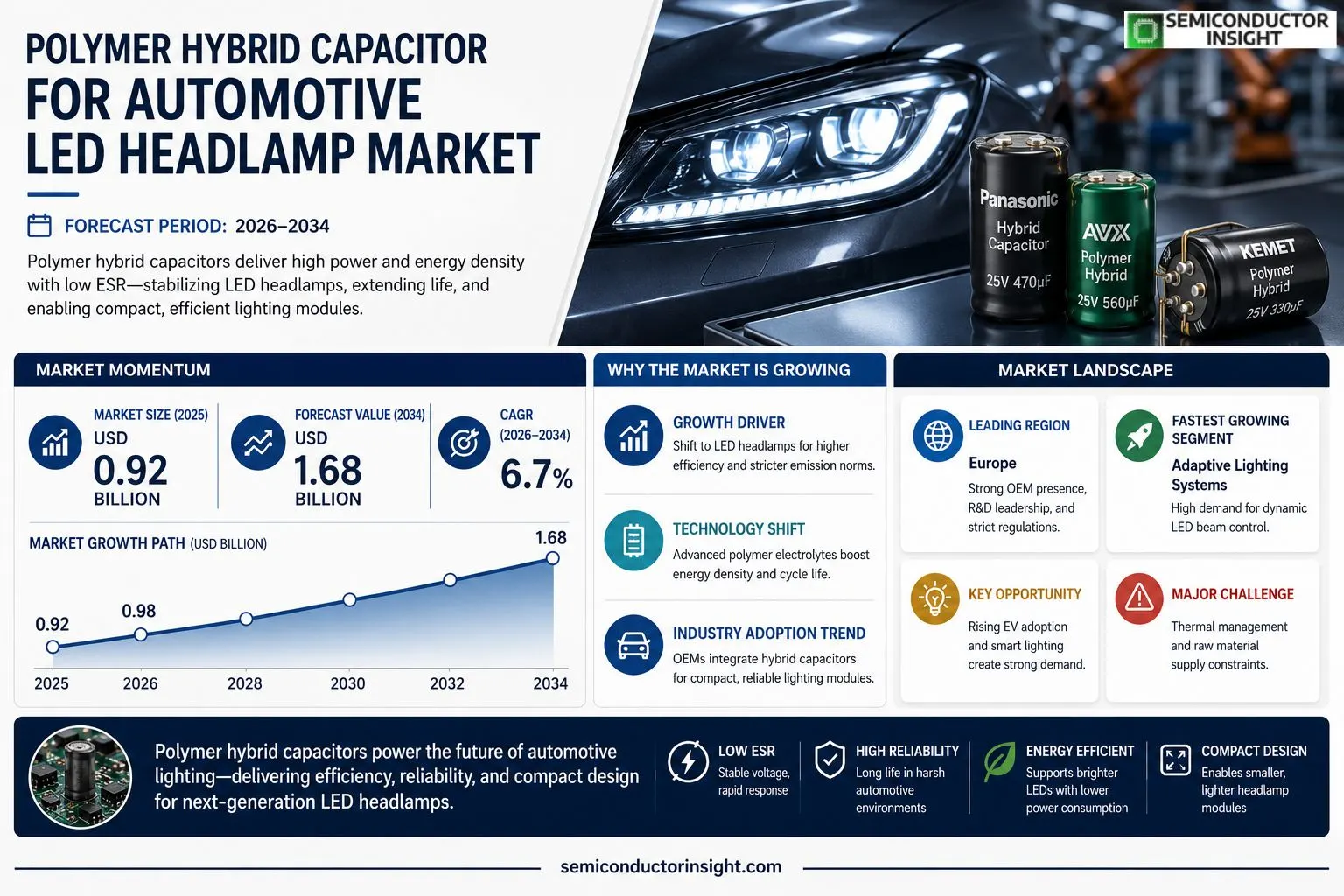

Polymer hybrid capacitor for automotive LED headlamp market size was valued at USD 0.92 billion in 2025. The market is projected to grow from USD 0.98 billion in 2026 to USD 1.68 billion by 2034, exhibiting a CAGR of 6.7% during the forecast period.

Polymer hybrid capacitors combine the high power capability of traditional electrolytic capacitors with the superior energy density of solid‑state Polymers, delivering rapid charge‑discharge cycles and low ESR (equivalent series resistance). In automotive LED headlamps they stabilize voltage spikes, extend lamp life, and enable compact lighting modules that meet stringent weight and space constraints.The market is experiencing robust growth because automakers are accelerating the shift toward LED‑based illumination systems to improve fuel efficiency and comply with stricter emission standards. Furthermore, rising consumer demand for brighter yet energy‑saving headlights drives adoption of advanced capacitor technologies. Key industry players such as Panasonic Corporation, AVX Corporation, and KEMET Corporation are expanding their product portfolios and investing in R&D to capture this expanding opportunity.

MARKET DRIVERS

Increasing Adoption of LED Headlamps

Polymer hybrid capacitor for automotive LED headlamp Market is being propelled by a rapid shift toward LED headlamp systems, which offer superior luminous efficiency and longer service life compared to traditional halogen lamps. Automakers worldwide are integrating LED modules to meet stricter fuel‑efficiency standards, creating a strong demand for reliable energy storage solutions.

Advancements in Polymer Hybrid Capacitor Technology

Recent breakthroughs in Polymer electrolyte formulations have increased the energy density and cycle life of hybrid capacitors, making them well‑suited for the high‑burst power requirements of automotive LED headlamps. These improvements enable faster startup times and smoother dimming transitions, which are critical for safety‑critical lighting functions.

➤ “Hybrid Polymer capacitors now deliver up to 30 % higher power density while maintaining low ESR, directly enhancing LED headlamp performance.”

Combined with decreasing component costs, these technology gains are encouraging OEMs to adopt Polymer hybrid capacitors as standard ancillary devices, further accelerating market growth.

MARKET CHALLENGES

Thermal Management Issues

LED headlamps generate localized heat, and Polymer hybrid capacitors must operate within tight temperature windows to preserve capacitance and lifespan. Insufficient thermal design can lead to premature degradation, posing reliability concerns for manufacturers.

Other Challenges

Cost Sensitivity

Although performance has improved, the capital expense of high‑purity Polymer electrolytes remains higher than that of conventional electrolytic capacitors, limiting adoption in cost‑constrained vehicle segments.

MARKET RESTRAINTS

Supply Chain Constraints

shortages of key Polymer raw materials, driven by competing electronics demand, are tightening supply pipelines for automotive applications. This can create lead‑time variances that disrupt production schedules.Additionally, the need for stringent quality‑control testing specific to automotive safety standards adds processing overhead, further restraining rapid scale‑up.Regulatory certification processes, while essential for vehicle safety, introduce additional time and cost barriers that can delay market entry for new capacitor designs.

MARKET OPPORTUNITIES

Emerging Electric Vehicle (EV) Platforms

Electric vehicles rely heavily on efficient power management across lighting, infotainment, and driver‑assist systems. Polymer hybrid capacitor for automotive LED headlamp Market stands to benefit as EV manufacturers seek lightweight, high‑power‑density storage that complements battery packs.Integration of smart control algorithms that dynamically adjust capacitor discharge profiles opens avenues for energy‑recovery schemes, further enhancing vehicle range and reducing overall electrical load.Regional incentives for low‑emission vehicles in North America, Europe, and Asia‑Pacific are accelerating EV adoption, indirectly boosting demand for advanced capacitor solutions tailored to LED headlamp applications.

Polymer hybrid capacitor for automotive LED headlamp Market Trends

Accelerated Shift to LED Headlamps

The market for Polymer hybrid capacitor in automotive LED headlamps was valued at USD 0.92 billion in 2025. Forecasts indicate a rise to USD 0.98 billion in 2026 and a reach of USD 1.68 billion by 2034, reflecting a compound growth rate of roughly 6.7 percent per year. This expansion is driven by automakers’ rapid transition to LED illumination, which reduces vehicle weight and improves fuel efficiency while meeting stricter emission regulations. In addition, consumer demand for brighter, energy‑saving headlights fuels the need for components that can handle frequent charge‑discharge cycles without degradation. The shift also aligns with governmental incentives for low‑emission vehicles, encouraging manufacturers to adopt advanced power‑management solutions. As a result, supply chains are prioritizing high‑reliability capacitor production to satisfy volume growth expectations.

Other Trends

Enhanced Energy Density and Low ESR

Polymer hybrid capacitors combine the high power capability of traditional electrolytic designs with the superior energy density offered by solid‑state Polymers. The resulting low equivalent series resistance enables rapid charge acceptance, which is critical for LED headlamp modules that experience sudden voltage spikes during start‑up. By stabilizing the supply voltage, these capacitors prolong lamp life and allow manufacturers to pursue more compact designs, addressing the stringent weight and space constraints of modern vehicle architectures. The technology also supports higher lumen output without increasing overall power consumption, aligning with automotive trends toward brighter, more efficient lighting solutions. Moreover, the improved thermal performance reduces the need for additional cooling components, contributing to overall system weight savings and reliability enhancements.

Intensified Competition and Product Innovation

Key industry players such as Panasonic Corporation, AVX Corporation, and KEMET Corporation are intensifying R&D investments to broaden their Polymer hybrid capacitor portfolios. These firms are introducing modules with higher voltage ratings and integrated thermal management, targeting the growing requirement for reliable, long‑lasting LED headlamp systems. Partnerships with automotive OEMs are accelerating product qualification cycles, enabling faster market entry and ensuring compliance with safety standards. As the segment matures, strategic collaborations and acquisitions are expected to reshape the competitive landscape, driving cost reductions and further performance improvements. This heightened innovation activity reinforces the market’s upward trajectory and underscores its significance within the broader automotive electrification agenda. In parallel, supply chain resilience is being bolstered through diversified sourcing and advanced manufacturing techniques, positioning the industry to meet sustained demand. Analysts anticipate that continued regulatory pressure and consumer preference for sustainable lighting will sustain growth through the next decade.

COMPETITIVE LANDSCAPE

Key Industry Players

Polymer Hybrid Capacitor Market for Automotive LED Headlamps – Competitive Overview

Panasonic Corporation remains the dominant supplier of Polymer hybrid capacitors for automotive LED headlamps, leveraging its extensive automotive electronics portfolio and deep R&D capabilities. AVX Corporation and KEMET Corporation follow closely, each offering high‑power, low‑ESR modules that meet the stringent automotive reliability standards such as AEC‑QM. These three firms account for roughly 45 % of shipments, shaping a market structure where a few large OEM‑aligned manufacturers drive pricing, technology road‑maps, and large‑volume contracts with Tier‑1 automotive suppliers. Their product portfolios increasingly integrate advanced Polymer dielectrics that enable rapid charge‑discharge cycles, essential for stabilising the high‑frequency pulsed currents of LED headlamp modules. The concentration among these leaders also encourages strategic partnerships with automakers seeking to co‑develop next‑generation lighting systems that reduce weight and improve luminous efficacy.Beyond the dominant trio, a diverse set of specialized capacitor makers intensifies competition in niche segments. Vishay Intertechnology and Murata Manufacturing supply compact, high‑voltage Polymer hybrids that are favoured in premium vehicle segments where space constraints are critical. Taiyo Yuden, TDK (EPCOS), and Nichicon focus on ultra‑low ESR designs that support fast transient response in high‑beam LED arrays. Rubycon and United Chemi‑Con provide cost‑effective solutions targeting emerging markets and mid‑range models, while Cornell‑Dubilier and Samsung Electro‑Mechanics expand their automotive portfolios with Polymer‑based offerings that comply with ISO‑26262 functional safety requirements. These players differentiate through application‑specific form factors, proprietary Polymer chemistries, and aggressive local manufacturing footprints, enabling them to capture regional contracts and supplement the supply chain resilience for automotive manufacturers.

List of Key Polymer Hybrid Capacitor Companies Profiled

- Panasonic Corporation

- AVX Corporation

- KEMET Corporation

- Vishay Intertechnology

- Murata Manufacturing

- Taiyo Yuden

- TDK Corporation (EPCOS)

- Nichicon Corporation

- Rubycon Corporation

- United Chemi‑Con

- Cornell‑Dubilier

- Samsung Electro‑Mechanics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Polymer Electrolytic is preferred for its high power handling and rapid charge‑discharge capability, which aligns with the fast transient demands of LED headlamp circuits. It also offers robustness against harsh automotive environments.

|

| By Application |

|

Adaptive Lighting Systems dominate the application landscape because they rely on precise voltage stability to modulate beam patterns in real time. Polymer hybrid capacitors deliver the low ESR required for seamless dimming and brightening cycles.

|

| By End User |

|

OEMs drive primary adoption as they design next‑generation headlamp modules that demand lighter, more energy‑efficient power solutions. The Polymer hybrid capacitor’s ability to merge high power density with compact form factors aligns with OEM priorities for vehicle weight reduction and design flexibility.

|

| By Voltage Tier |

|

Medium Voltage emerges as the leading tier because it balances the power needs of modern LED arrays with the safety and packaging constraints of automotive electrical architectures. Polymer hybrid capacitors operating in this range provide reliable surge protection while maintaining a slim profile.

|

| By Integration Mode |

|

Embedded within PCB is gaining prominence as vehicle designers prioritize space‑efficiency and signal integrity. Incorporating Polymer hybrid capacitors directly onto the PCB reduces parasitic inductance, leading to cleaner power delivery for LED drivers.

|

Regional Analysis: Polymer hybrid capacitor for automotive LED headlamp Market

Europe

The European Union’s stringent CO₂ reduction targets mandate more efficient lighting, prompting manufacturers to adopt Polymer hybrid capacitors that enhance LED headlamp power management while meeting compliance standards.

A dense network of capacitor manufacturers in Germany and Italy supplies high‑volume, high‑reliability components, reducing lead times and supporting the rapid scaling of automotive LED headlamp applications.

Leading OEMs such as Volkswagen and Stellantis have forged strategic alliances with capacitor developers, ensuring seamless integration of hybrid capacitors into next‑generation headlamp architectures.

Ongoing research in Polymer electrolytes and nanostructured electrodes drives performance gains, delivering faster charge cycles and longer lifespans for automotive LED lighting systems.

North America

In North America, the market is propelled by the high adoption rate of electric and hybrid vehicles, which rely on sophisticated lighting solutions. U.S. manufacturers are prioritizing energy‑efficient LED headlamps, creating demand for Polymer hybrid capacitors that deliver rapid response and durability. While regulatory pressure is less prescriptive than in Europe, industry initiatives and consumer expectations for premium lighting drive incremental growth across the region.

Asia-Pacific

Asia‑Pacific exhibits strong momentum due to rapid automotive production in China, Japan, and South Korea. Manufacturers are seeking cost‑effective capacitor technologies to meet the volume demands of mass‑market vehicles while sustaining performance standards for LED headlamps. Government incentives for green mobility and expanding EV fleets further stimulate interest in hybrid capacitor solutions, positioning the region as a burgeoning market hub.

South America

South America’s market remains nascent, with growth anchored by rising vehicle sales in Brazil and Argentina. Automotive firms are gradually upgrading to LED headlamp systems, recognizing the benefits of Polymer hybrid capacitors for energy savings and reduced maintenance. Economic variability poses challenges, yet localized production initiatives aim to lower component costs and foster market acceptance.

Middle East & Africa

In the Middle East & Africa, the market is driven by luxury vehicle imports and increasing emphasis on safety lighting. While overall vehicle volumes are modest, the premium segment’s preference for advanced LED headlamps creates niche demand for high‑performance Polymer hybrid capacitors. Regional partnerships with European suppliers are emerging, supporting technology transfer and market development.

Report Scope

This market research report provides a comprehensive analysis of the Polymer hybrid capacitor for automotive LED headlamp Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Polymer hybrid capacitor for automotive LED headlamp Market?

-> Polymer hybrid capacitor for automotive LED headlamp Market was valued at USD 0.92 billion in 2025 and is expected to reach USD 1.68 billion by 2034.

Which key companies operate in Polymer hybrid capacitor for automotive LED headlamp Market?

-> Key players include Panasonic Corporation, AVX Corporation, and KEMET Corporation.

What are the key growth drivers?

-> Key growth drivers include automakers’ shift toward LED headlamps, stricter emission regulations, and rising consumer demand for brighter, energy‑saving headlights.

Which region dominates the market?

-> The source does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include development of higher‑energy‑density Polymer hybrids, integration of low‑ESR capacitors in compact lighting modules, and increased R&D investment by leading manufacturers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...