MARKET INSIGHTS

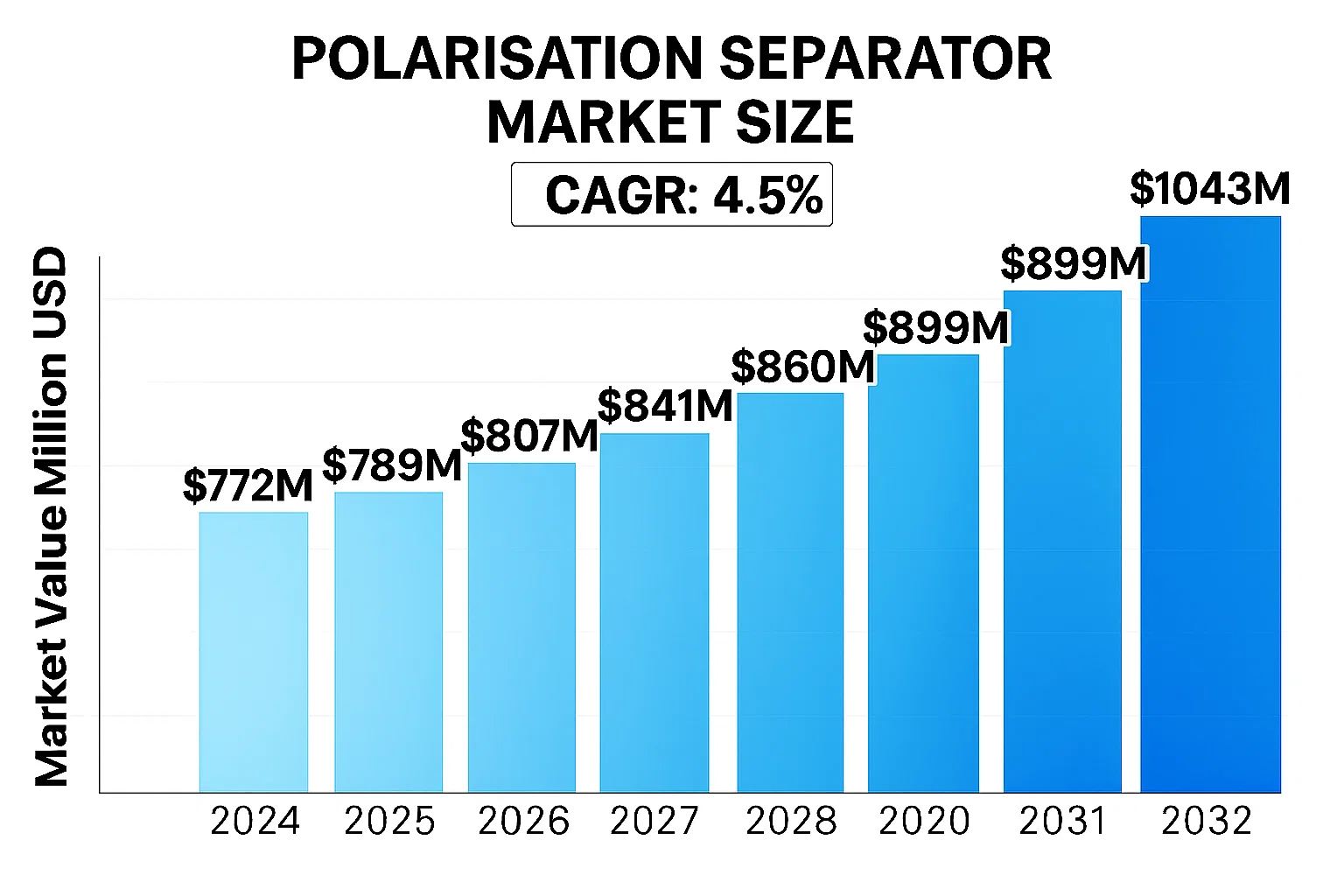

The global Polarisation Separator Market was valued at 772 million in 2024 and is projected to reach US$ 1043 million by 2032, at a CAGR of 4.5% during the forecast period.

Polarisation separators are advanced optical components that split incoming light into two orthogonally polarised beams with complementary spectra. These devices combine multiple polarisation beam splitters to create multi-channel birefringent filters, enabling precise spectral analysis in applications ranging from spectroscopy to quantum optics. The technology offers superior performance compared to conventional polarisers by producing two perpendicularly polarised output channels with continuous transmission bands.

Polarisation separators are advanced optical components that split incoming light into two orthogonally polarised beams with complementary spectra. These devices combine multiple polarisation beam splitters to create multi-channel birefringent filters, enabling precise spectral analysis in applications ranging from spectroscopy to quantum optics. The technology offers superior performance compared to conventional polarisers by producing two perpendicularly polarised output channels with continuous transmission bands.

The market growth is driven by increasing adoption in photonics applications, particularly in telecommunications, laser systems, and quantum computing. The rising demand for high-precision optical components in aerospace and medical imaging further contributes to market expansion. Notably, innovations in photonic integration and fiber optic networks are creating new opportunities for polarisation separator applications. Key players like Thorlabs, Newport Corporation, and EKSMA Optics are actively developing advanced solutions to meet the evolving requirements of these high-tech industries.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption in Optical Communication Systems Accelerates Market Expansion

The rapid growth of fiber optic networks worldwide is creating substantial demand for polarisation separators. With data traffic projected to increase exponentially due to rising internet penetration and 5G deployments, optical communication systems require advanced components for signal processing. Polarisation separators play a critical role in minimizing signal degradation and improving transmission efficiency in dense wavelength division multiplexing (DWDM) systems. Leading telecom operators are investing heavily in network upgrades, with global fiber optic component expenditures expected to surpass $10 billion annually by 2026. This infrastructure development directly benefits the polarisation separator market as new installations and equipment replacements drive consistent demand.

Advancements in Laser Technology Boost Industrial Applications

Industrial laser systems are increasingly incorporating polarisation separators to enhance precision in material processing applications. The global industrial laser market has shown steady growth at approximately 7% CAGR, supported by adoption in manufacturing sectors like automotive and electronics. Recent technological improvements have enabled polarisation separators to handle higher power densities while maintaining beam quality – a critical factor for laser cutting, welding and micromachining operations. Several tier-1 laser manufacturers have integrated next-generation polarisation control components into their 2024 product lines, demonstrating the component’s growing importance in industrial automation solutions.

Emerging Quantum Technologies Create New Growth Avenues

Quantum computing and quantum communication systems are emerging as significant drivers for precision optical components. Polarisation separators perform essential functions in quantum key distribution (QKD) systems by enabling precise photon state manipulation. With governments and private entities investing over $30 billion collectively in quantum technology development, specialized optical components are experiencing unprecedented demand. The unique requirements of quantum applications are pushing manufacturers to develop ultra-high-performance polarisation separators with extinction ratios exceeding 30 dB and superior thermal stability characteristics.

MARKET RESTRAINTS

High Manufacturing Costs Limit Market Penetration in Price-Sensitive Segments

The precision manufacturing requirements for polarisation separators result in substantially higher production costs compared to conventional optical components. Achieving the necessary extinction ratios and wavelength specifications demands specialized materials and stringent quality control processes, with reject rates in some manufacturing batches exceeding 15%. These cost factors make commercial-grade polarisation separators prohibitively expensive for budget-constrained applications, particularly in developing markets. While demand exists across multiple sectors, price sensitivity remains a significant barrier preventing broader market penetration in cost-conscious industries.

Technical Complexity Hinders Widespread Adoption

Polarisation separator implementation presents notable technical challenges that restrain market growth. The components require precise alignment and integration within optical systems, often demanding specialized installation expertise that many end-users lack. Environmental factors such as temperature fluctuations and mechanical vibrations can significantly impact performance, requiring additional stabilization measures. Furthermore, maintaining optimal performance over extended periods remains challenging, as even minor misalignments can degrade system efficiency. These technical considerations add considerable implementation costs and complexity, discouraging adoption in less sophisticated applications where simpler alternatives exist.

MARKET OPPORTUNITIES

Medical Imaging Innovations Open New Application Frontiers

Recent advancements in biomedical imaging techniques are creating significant opportunities for polarisation separator applications. Polarisation-sensitive optical coherence tomography (PS-OCT) systems, which provide enhanced tissue contrast in ophthalmology and dermatology, rely critically on high-performance polarisation management components. The global medical imaging equipment market is projected to maintain strong growth above 5% annually, with increasing adoption of advanced optical diagnostic methods. Manufacturers developing application-specific polarisation separators for medical devices can capitalize on this growing demand while benefiting from the healthcare sector’s relative insulation from economic downturns.

Miniaturization Trends Drive Product Innovation

The ongoing miniaturization of photonic systems is prompting manufacturers to develop compact polarisation separator solutions. Integrated photonics platforms and silicon photonics applications require polarization control components with dramatically reduced footprints while maintaining performance standards. Several leading optical component suppliers have announced development programs targeting micro-optic and on-chip polarisation management solutions. These innovations position the industry to address emerging requirements in data center interconnects, LiDAR systems, and wearable optical devices – markets where size and weight constraints previously limited polarisation separator adoption.

MARKET CHALLENGES

Intense Competition from Alternative Technologies

The polarisation separator market faces growing competition from alternative polarization control technologies that offer potentially lower costs or simpler implementations. Liquid crystal-based polarization controllers and fiber-integrated solutions are gaining traction in certain applications, particularly where compact designs and electrical controllability are prioritized. Meanwhile, digital signal processing techniques are reducing reliance on physical polarization management in some optical communication systems. These technological alternatives threaten conventional polarisation separator market share, pressuring manufacturers to demonstrate clear performance advantages that justify their products’ premium pricing.

Supply Chain Vulnerabilities Impact Manufacturing Stability

Specialized raw materials and components required for polarisation separator production remain susceptible to supply chain disruptions. Certain optical crystals and precision coating materials face limited global availability, with lead times extending beyond 12 months in some cases. The industry’s reliance on a small number of specialized suppliers creates potential bottlenecks, as demonstrated during recent geopolitical tensions that affected rare earth element supplies. Manufacturers must navigate these supply chain risks while meeting growing demand, requiring strategic inventory management and potential vertical integration initiatives to ensure production continuity.

POLARISATION SEPARATOR MARKET TRENDS

Rising Demand in Photonics and Optical Communications to Drive Market Expansion

The global polarisation separator market is experiencing robust growth, fueled by increasing applications in photonics and optical communication systems. Valued at $772 million in 2024, the market is projected to reach $1,043 million by 2032, growing at a CAGR of 4.5%. This surge is largely driven by advancements in fiber optic networks, where polarisation separators play a critical role in signal processing and data transmission. Emerging technologies such as 5G communication and quantum computing further amplify demand, as these systems require high-precision optical components to manage light polarization.

Other Trends

Technological Innovations in Optical Engineering

The development of compact, high-efficiency polarisation separators is reshaping industrial applications. Recent innovations include multi-channel birefringent filters that enable continuous spectral distribution, crucial for imaging, spectroscopy, and laser systems. The trend towards miniaturization in optical devices has also led manufacturers to introduce nano-engineered separators with improved durability and thermal stability. In laser technology, polarisation separators are increasingly used for beam combining, enhancing efficiency in industrial cutting and medical laser applications.

Growing Industrial Applications Across Sectors

Beyond telecommunications, polarisation separators are gaining traction in aerospace, medical technology, and automotive industries where precision optics are essential. In aerospace, these components are integrated into navigation and sensing systems, while medical imaging devices leverage polarisation separation for enhanced diagnostic accuracy. The automotive sector’s shift towards LiDAR systems for autonomous vehicles presents another growth avenue, with polarisation separators improving signal clarity in adverse weather conditions. This diversification across industries underscores the component’s versatility and expanding market potential.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Competitiveness

The global polarisation separator market exhibits a dynamic competitive landscape, characterized by established optical component manufacturers and emerging technology-focused firms. Thorlabs Inc. and Newport Corporation dominate the market share, leveraging their extensive product portfolios and strong distribution networks across North America and Europe. Thorlabs captured approximately 18% of the 2024 market revenue, attributed to its vertically integrated manufacturing capabilities and rapid innovation cycle.

Edmund Optics and EKSMA Optics have secured notable positions by specializing in high-precision polarisation separators for research and industrial applications. These companies benefit from increasing demand in quantum computing and advanced spectroscopy, where polarization control is critical. Meanwhile, Asia-Pacific players like CASTECH and Shanghai Optics are gaining traction through cost-competitive manufacturing and government support for photonics infrastructure development.

Recent strategic developments include Lambda Research Optics’ acquisition of a specialty coatings manufacturer to enhance its polarization separator durability, and Chromatech Technology’s partnership with a German automation firm to expand into industrial laser applications. Such moves are reshaping supply chain dynamics while improving component performance metrics like extinction ratio and wavelength range.

The market also sees increasing competition from integrated photonics companies such as NTT Advanced Technology Corporation, which combines polarisation separation functionality with other optical components in compact modules. This trend reflects the industry’s shift toward system-level solutions rather than discrete components, particularly in telecommunications and medical imaging sectors.

List of Key Polarisation Separator Manufacturers

- Thorlabs Inc. (U.S.)

- Newport Corporation (U.S.)

- Edmund Optics (U.S.)

- EKSMA Optics (Lithuania)

- CASTECH (China)

- Shanghai Optics (China)

- Lambda Research Optics (U.S.)

- Chroma Technology Corp (U.S.)

- NTT Advanced Technology Corporation (Japan)

- Rocky Mountain Instrument (U.S.)

- Solaris Optics (Poland)

- Altechna (Lithuania)

Segment Analysis:

By Type

Plate Type Dominates the Market Due to High Demand in Laser and Optical Systems

The market is segmented based on type into:

- Plate Type

- Subtypes: Single Plate, Double Plate, and others

- Three-dimensional Type

- Customized Designs

- Others

By Application

Photonics & Optics Industry Leads Due to Increasing Need for Precision Light Control

The market is segmented based on application into:

- Photonics & Optics

- Telecommunications

- Medical Technology

- Industrial Manufacturing

- Research & Development

By End User

Research Institutions Segment Holds Significant Share Due to Extensive Optical Experiments

The market is segmented based on end user into:

- Research Institutions

- Industrial Manufacturers

- Telecom Providers

- Healthcare Organizations

- Others

By Technology

Birefringent Technology Segment Shows Strong Growth Potential

The market is segmented based on technology into:

- Birefringent Crystal-based

- Thin-film Polarizing

- Beam-splitting Cube

- Others

Regional Analysis: Polarisation Separator Market

North America

The North American market for polarisation separators is driven by robust investments in photonics research, quantum computing initiatives, and defense applications. The United States, in particular, remains the largest consumer due to its advanced optical communication networks and substantial R&D spending by institutions like DARPA and NASA. Canada is emerging as a notable contributor with government-backed photonics programs and expanding telecom infrastructure. Key manufacturers like Thorlabs and Newport Corporation maintain strong market presence, with product innovation focusing on high-precision optical components for telecom and aerospace applications. While environmental regulations are less directly impactful than in other industries, the focus remains on energy-efficient optical solutions.

Europe

Europe’s polarisation separator market benefits from stringent quality standards in optical instrumentation and strong academic-industry collaborations. Germany leads in manufacturing precision optics, while France and the UK show increasing demand for photonic components in quantum technology research (backed by Horizon Europe funding). The region emphasizes efficiency in fiber-optic networks, with polarisation separators playing a critical role in DWDM systems. Companies like EKSMA Optics and Solaris Optics are capitalizing on this demand through specialized coatings and compact designs. However, market growth faces some constraints due to lengthy certification processes for optical components in medical and aerospace applications.

Asia-Pacific

As the fastest-growing region, Asia-Pacific dominates both production and consumption of polarisation separators, with China accounting for over 40% of regional demand. The country’s massive fiber-optic network expansion and local manufacturers like CASTECH drive volume sales, though price competition remains intense. Japan and South Korea focus on high-end applications in semiconductor lithography and biomedical imaging, preferring customized separator solutions. India is becoming an important market with its National Quantum Mission creating opportunities in research optics, though reliance on imports for premium components persists. Overall, while cost-driven purchasing dominates, increasing precision requirements in manufacturing are pushing quality standards upward.

South America

Market development in South America remains gradual, with Brazil constituting approximately 60% of regional demand primarily for industrial laser systems and university research labs. The lack of local manufacturing means most polarisation separators are imported from North America and Asia at competitive prices. Argentina shows potential in astronomical applications, particularly for observatory instrumentation. However, economic instability and limited photonics infrastructure investment continue to restrict market expansion. Emerging opportunities exist in mining sector optical sensors and biomedical devices, though these remain niche applications.

Middle East & Africa

This region presents a developing market concentrated in Israel (defense optics) and Gulf States (telecom infrastructure). The UAE’s focus on becoming a technology hub has increased demand for optical components in research centers like Masdar City. Saudi Arabia’s Vision 2030 includes photonics in its high-tech diversification strategy. Still, limited local expertise and dependence on international suppliers constrain growth. In Africa, South Africa shows early potential in astronomy applications, while other nations require basic optical infrastructure before polarisation separator adoption can accelerate meaningfully.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Polarisation Separator markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Polarisation Separator market was valued at USD 772 million in 2024 and is projected to reach USD 1043 million by 2032, growing at a CAGR of 4.5%.

- Segmentation Analysis: Detailed breakdown by product type (Plate Type, Three-dimensional Type), application (Mechanical Engineering, Automotive, Aerospace, Medical Technology, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific currently dominates with 42% market share in 2024.

- Competitive Landscape: Profiles of 25+ leading market participants including Thorlabs, Newport Corporation, EKSMA Optics, and Lambda Research Optics, covering their product portfolios and strategic developments.

- Technology Trends & Innovation: Analysis of emerging applications in quantum optics, photonic integration, and advanced spectroscopy systems driving market evolution.

- Market Drivers & Restraints: Evaluation of growth drivers like increasing photonics R&D investments versus challenges such as high manufacturing costs and technical complexity.

- Stakeholder Analysis: Strategic insights for optical component manufacturers, system integrators, research institutions, and investors navigating this specialized market.

The research employs primary interviews with industry experts and analysis of verified market data from manufacturers, ensuring reliable and actionable insights for strategic decision-making.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Polarisation Separator Market?

-> Polarisation Separator Market was valued at 772 million in 2024 and is projected to reach US$ 1043 million by 2032, at a CAGR of 4.5% during the forecast period..

Which key companies operate in Global Polarisation Separator Market?

-> Key players include Thorlabs, Newport Corporation, Lambda Research Optics, EKSMA Optics, Solaris Optics, and Altechna, among others.

What are the key growth drivers?

-> Key growth drivers include advancements in photonics technology, increasing R&D investments in optics, and expanding applications in quantum computing and advanced spectroscopy.

Which region dominates the market?

-> Asia-Pacific leads the market with 42% share, followed by North America and Europe, driven by photonics industry growth in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of optical components, development of ultra-precise separators for quantum applications, and integration with AI-driven optical systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...