Plastic film capacitor with PPS dielectric for SMD automotive Market Insights

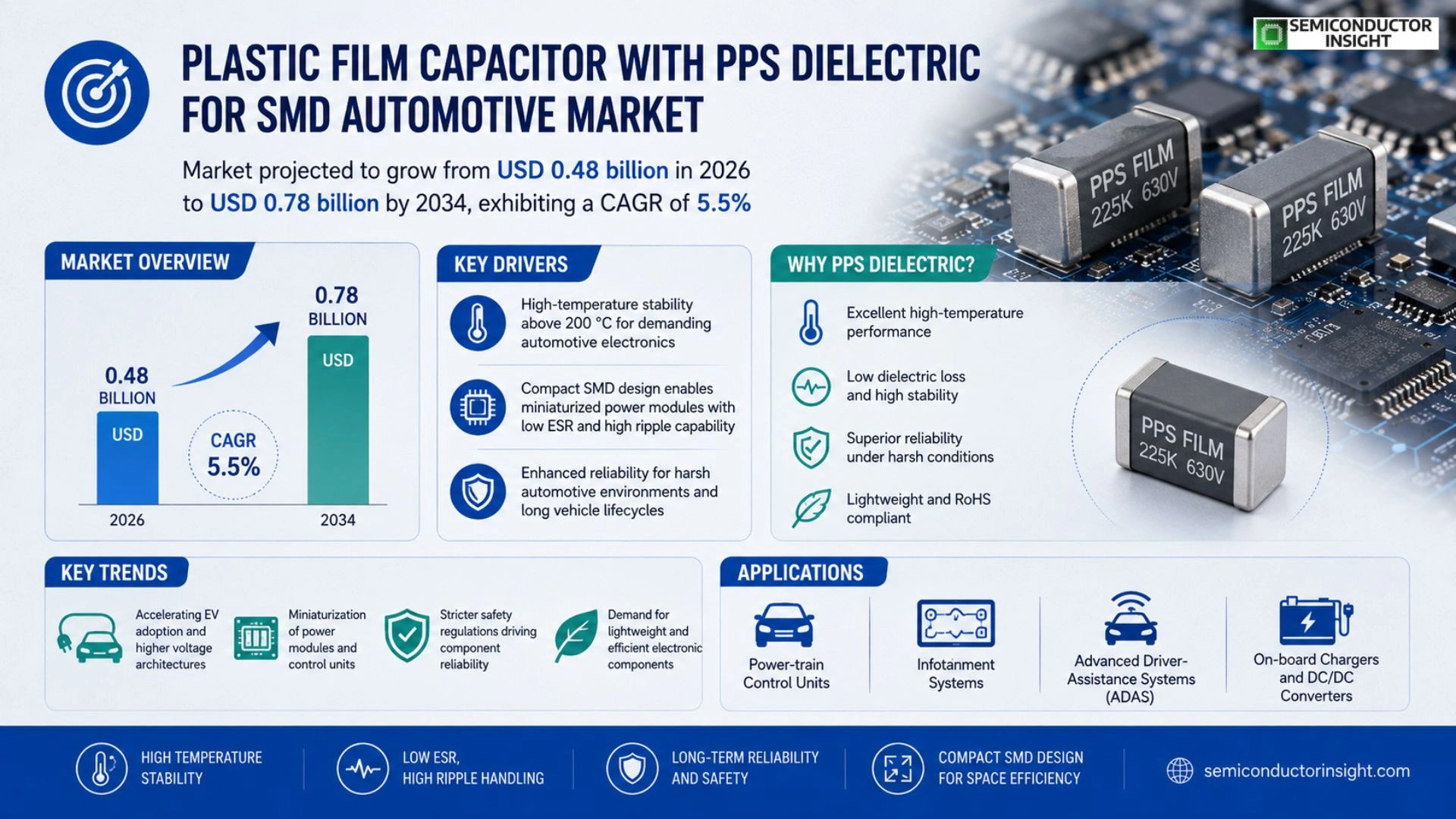

Global Plastic film capacitor with PPS dielectric for SMD automotive market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034, exhibiting a CAGR of 5.5% during the forecast period.

Plastic film capacitors employing polyphenylene sulfide (PPS) dielectric offer high temperature stability, low loss, and excellent reliability, making them ideal for surface‑mount device (SMD) applications in automotive electronics such as power‑train control units, infotainment systems, and advanced driver‑assistance systems (ADAS).

The market is experiencing steady growth driven by the automotive industry’s shift toward electrification and higher voltage architectures, which demand components that can withstand harsh thermal cycles. Furthermore, stricter safety regulations and the push for lightweight designs encourage manufacturers to adopt PPS‑based film capacitors because of their superior performance under demanding conditions.

MARKET DRIVERS

Demand for High‑Temperature Reliability

Plastic film capacitor with PPS dielectric for SMD automotive applications is increasingly favored because PPS can sustain temperatures above 200 °C, matching the thermal profiles of modern powertrain electronics. OEMs prioritize components that maintain capacitance stability under prolonged heat exposure, reducing warranty failures.

Shift Toward Miniaturized Power Modules

Compact SMD footprints enable designers to pack higher functionality into limited board area. The thin‑film construction of PPS‑based capacitors offers low ESR and high ripple current capability, supporting the trend toward electric‑vehicle power modules that demand both size efficiency and robust performance.

➤ “Manufacturers report a 12 % year‑over‑year increase in selection of PPS dielectric films for automotive SMD capacitors, citing superior temperature tolerance and dielectric strength.”

Furthermore, regulatory pressures for longer vehicle lifecycles encourage adoption of components that can endure harsh automotive environments without degradation, positioning Plastic film capacitor with PPS dielectric for SMD automotive Market as a strategic supply‑chain choice.

MARKET CHALLENGES

Integration Compatibility with Existing PCB Processes

While PPS dielectric offers performance benefits, its manufacturing tolerances sometimes require adjustments in solder reflow profiles. Small‑scale manufacturers may encounter yield issues when shifting from traditional polyester films, necessitating process validation.

Other Challenges

Cost Sensitivity

The material cost of PPS is higher than conventional polymers, which can affect the price competitiveness of SMD capacitors, especially in high‑volume segments where margin pressures are acute.

MARKET RESTRAINTS

Limited Supplier Base for PPS Film

Only a few qualified producers currently supply high‑purity PPS film suitable for automotive capacitors, creating bottlenecks that can delay product introductions and increase lead times for end‑users.

MARKET OPPORTUNITIES

Expansion into Electrified Power‑train Segments

As electric and hybrid vehicles demand capacitors with superior thermal performance and long‑term reliability, Plastic film capacitor with PPS dielectric for SMD automotive Market is well‑positioned to capture new design wins in inverter modules, DC‑DC converters, and high‑voltage safety systems, driving growth opportunities for early adopters.

Plastic film capacitor with PPS dielectric for SMD automotive Market Trends

Growth of PPS‑Based Film Capacitors in Electrified Vehicles

The shift toward electrified powertrains and higher‑voltage architectures is creating a clear demand for components that can endure extreme thermal cycles while maintaining low dielectric loss. Plastic film capacitors that incorporate a polyphenylene sulfide (PPS) dielectric meet these requirements, offering temperature stability up to 150 °C, minimal loss tangent, and long‑term reliability. Automotive manufacturers are therefore specifying PPS‑based film capacitors for a range of surface‑mount device (SMD) applications, including power‑train control modules, infotainment processors, and advanced driver‑assistance systems (ADAS). The result is a steady expansion of the PPS capacitor segment within the broader automotive component ecosystem.

Other Trends

Electrification Impact on Component Selection

Electrification drives the need for higher voltage ratings and compact form factors. PPS dielectric film capacitors provide a superior combination of high voltage capability and reduced footprint compared with traditional polyethylene or polyester alternatives. This enables designers to consolidate circuitry and achieve weight savings, which are critical for extending electric vehicle range. In addition, the inherent moisture resistance of PPS improves durability in harsh automotive environments, reducing the risk of premature failure during long service life.

Regulatory and Design Drivers

Stricter safety standards and emissions regulations are prompting OEMs to prioritize components that deliver both performance and compliance. The low loss characteristics of PPS film capacitors help minimize heat generation, supporting thermal management strategies required to meet regulatory limits on component temperature. Moreover, the lightweight nature of plastic film technology aligns with industry goals for reduced vehicle mass, aiding fuel‑efficiency targets for internal combustion engines and range enhancements for electric platforms. As a result, the adoption of PPS‑based film capacitors is becoming a standard practice in new vehicle platforms, reinforcing their role as a key enabler of next‑generation automotive electronics.

COMPETITIVE LANDSCAPE

Key Industry Players

Plastic Film Capacitor with PPS Dielectric – SMD Automotive Market Competitive Overview

The market is dominated by a handful of global capacitor manufacturers that have leveraged their extensive R&D capabilities to qualify PPS‑based film capacitors for demanding automotive SMD applications. AVX (now part of Yageo) leads with a broad portfolio covering high‑temperature (up to 200 °C) and high‑voltage parts that are preferentially selected for power‑train control units and ADAS modules. Vishay and TDK follow closely, offering differentiated dielectric formulations that improve loss characteristics and enable more compact module footprints. Murata’s focus on miniaturized SMD packages has secured it a strong position in infotainment and ECU designs, while KEMET’s legacy in film capacitor technology continues to provide a reliable supply chain for OEMs seeking long‑term part availability. These tier‑1 players benefit from deep automotive qualification programs (AEC‑Q200, IATF 16949) and maintain a consolidated market structure where a few large firms capture the majority of volume.

Beyond the tier‑1 group, several niche manufacturers contribute significant innovation and competitive pressure. Nippon Chemi‑Con and Cornell‑Dubilier specialize in ultra‑low ESR solutions for high‑frequency switching circuits, addressing emerging 48 V vehicle architectures. Samsung Electro‑Mechanics and Taiyo Yuden provide cost‑effective alternatives for mass‑market vehicle models, often partnering with Tier‑1 OEMs for co‑development projects. Smaller European firms such as EPCOS (a TDK subsidiary) and Aurelia focus on customized dielectric blends that target specific thermal cycling requirements, while emerging Asian players like Yageo’s subsidiary, KEMET, and Hongfa Technology expand their presence through aggressive pricing and localized manufacturing. Collectively, these companies enrich the competitive landscape, driving technology advancement and price erosion across the PPS film capacitor segment.

List of Key Plastic Film Capacitor with PPS Dielectric Companies Profiled

- AVX (Yageo Group)

- Vishay Intertechnology

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Samsung Electro‑Mechanics

- KEMET Corporation

- Nippon Chemi‑Con Corporation

- Cornell‑Dubilier Electronics

- Taiyo Yuden Co., Ltd.

- EPCOS (TDK Group)

- Aurelia Electronics Ltd.

- Hongfa Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Film capacitors with PPS dielectric

|

| By Application |

|

Power‑train control units

|

| By End User |

|

Tier‑1 suppliers

|

| By Reliability Requirement |

|

High‑temperature stability

|

| By Design Integration |

|

Miniature SMD footprints

|

Regional Analysis: Plastic film capacitor with PPS dielectric for SMD automotive Market

European Union directives on vehicle emissions and safety compel manufacturers to adopt high‑performance capacitors. PPS dielectric offers superior thermal resistance, satisfying the stringent reliability tests required for Euro 6 and upcoming zero‑emission standards, making it a preferred choice across the region.

A well‑integrated supply network spanning Germany, Italy and the Netherlands ensures timely availability of high‑purity polypropylene films and PPS resins. Strategic partnerships between capacitor producers and automotive OEMs mitigate raw‑material price volatility and enhance production agility.

Leading research institutions in the UK and Sweden focus on nano‑structured PPS dielectrics, delivering higher dielectric constants without compromising reliability. Collaborative projects accelerate the transfer of breakthroughs into commercial SMD capacitor designs for electric and hybrid vehicles.

OEMs across Europe increasingly request compact, high‑temperature capacitors to meet space constraints in battery‑management and power‑inverter modules. The PPS‑based film capacitor fulfills these needs, driving consistent demand across premium and mainstream vehicle segments.

North America

The North American market benefits from a strong focus on electric‑vehicle (EV) adoption and a robust automotive electronics ecosystem. U.S. and Canadian OEMs prioritize capacitors that can endure high power densities while maintaining a small footprint, positioning PPS dielectric film capacitors as a strategic component. Investment in domestic semiconductor fabs and the presence of major capacitor manufacturers foster rapid prototyping and short lead times. Additionally, federal incentives for clean‑energy vehicles stimulate demand for reliable SMD solutions that can operate under the thermal stresses typical of high‑performance power‑train applications. Industry analysts note that collaboration between Tier‑1 suppliers and automotive engineers accelerates design integration, reinforcing the region’s growth trajectory.

Asia‑Pacific

Asia‑Pacific emerges as a high‑growth region, driven by rapid vehicle production volumes in China, Japan, South Korea and India. Manufacturers are embracing PPS dielectric technology to address the aggressive cost‑reduction targets while preserving thermal stability for increasingly complex electronic architectures. Local supply chains provide cost‑effective raw materials, and government policies encouraging EV penetration create a fertile environment for advanced capacitor adoption. However, market fragmentation and varying quality standards pose challenges, prompting multinational firms to establish localized quality‑control centers. The region’s focus on scaling production capacity aligns with the broader shift toward electrified mobility, positioning it as a pivotal market for future expansion.

South America

In South America, market growth is anchored by Brazil’s expanding automotive sector and regional efforts to modernize vehicle electronics. While overall vehicle volumes are lower than in other continents, the push for fuel‑efficiency and stricter emission norms encourages OEMs to seek reliable SMD capacitor solutions. PPS‑based film capacitors offer the thermal resilience needed for hot‑climate operation, making them attractive for both passenger and commercial vehicles. Local distributors play a critical role in bridging gaps between global manufacturers and regional assemblers, and collaborative initiatives focused on technology transfer aim to enhance component reliability and reduce dependence on imports.

Middle East & Africa

The Middle East & Africa region experiences modest yet steady demand, primarily driven by the United Arab Emirates and South Africa’s automotive assembly activities. Harsh environmental conditions demand capacitors with high temperature tolerance, positioning PPS dielectric film capacitors as a suitable choice for power‑train and chassis control modules. Investments in renewable‑energy‑powered transportation and government‑backed initiatives for greener fleets are beginning to influence component specifications. Though market size remains limited, strategic partnerships with European and Asian manufacturers facilitate technology diffusion, supporting the region’s gradual shift toward more sophisticated automotive electronics.

Report Scope

This market research report provides a comprehensive analysis of the Plastic film capacitor with PPS dielectric for SMD automotive Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Plastic film capacitor with PPS dielectric for SMD automotive Market?

-> Plastic film capacitor with PPS dielectric for SMD automotive market size is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034.

Which key companies operate in Plastic film capacitor with PPS dielectric for SMD automotive Market?

-> Key players include Murata Manufacturing, KEMET Corporation, AVX Corp., TDK Corporation, Vishay Intertechnology, and Cornell‑Dubilier, among others.

What are the key growth drivers?

-> Key growth drivers include automotive electrification, adoption of higher‑voltage architectures, stricter safety regulations, and the push for lightweight designs that benefit from the high temperature stability and low loss of PPS‑based film capacitors.

Which region dominates the market?

-> Asia‑Pacific is experiencing the fastest growth due to rapid EV adoption, while Europe remains a strong, mature market for automotive capacitors.

What are the emerging trends?

-> Emerging trends include integration of PPS film capacitors in advanced driver‑assistance systems (ADAS), power‑train control units for electric vehicles, and the development of ultra‑low‑loss capacitors to support higher efficiency in automotive electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...