MARKET INSIGHTS

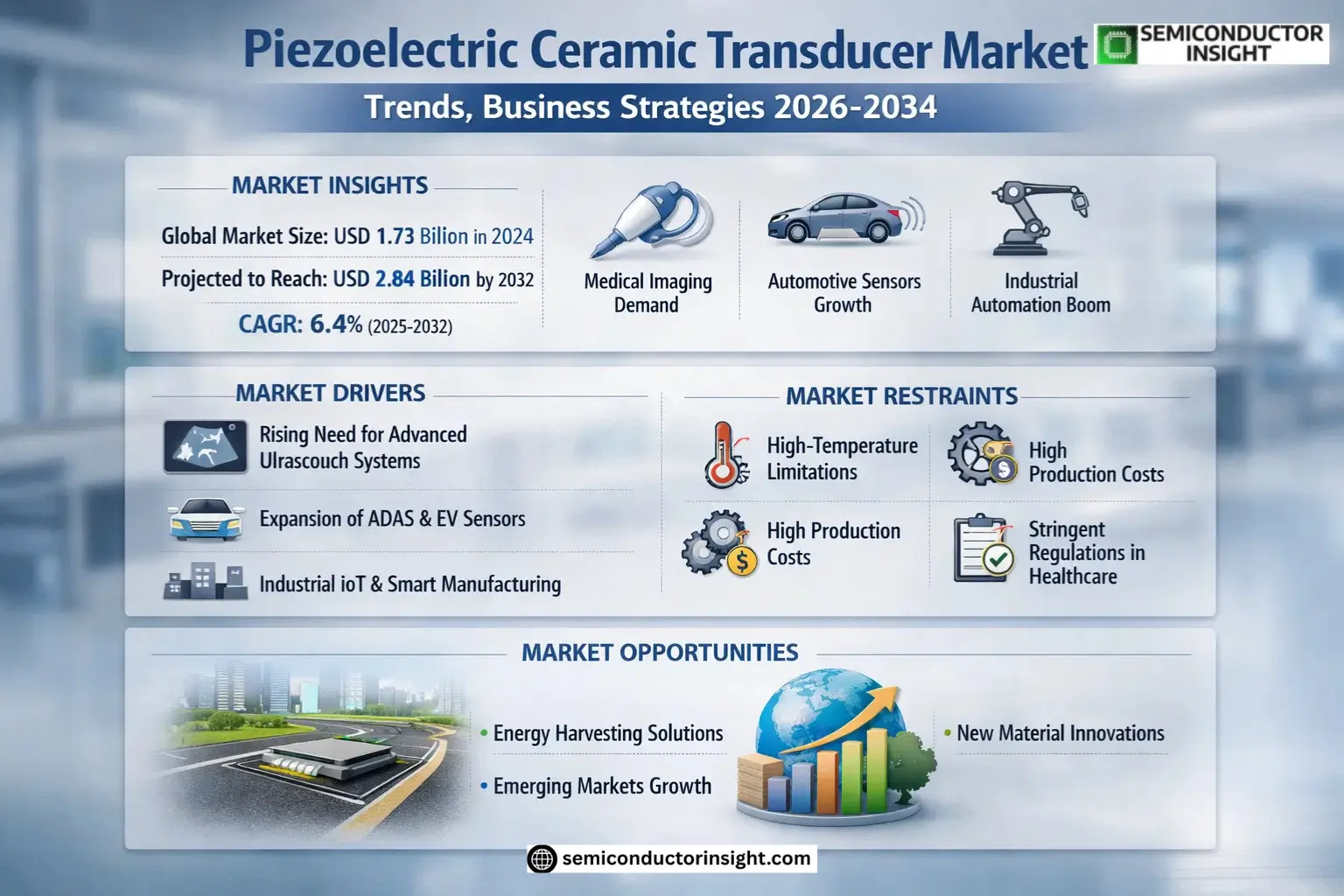

Global Piezoelectric Ceramic Transducer Market size was valued at USD 1.73 billion in 2024 and is projected to reach USD 2.84 billion by 2032, at a CAGR of 6.4% during the forecast period 2025-2032.

Piezoelectric ceramic transducers are specialized devices that convert electrical energy into mechanical vibrations and vice versa. These components leverage the piezoelectric effect, where certain materials generate an electric charge in response to applied mechanical stress. Key applications include ultrasonic sensors, actuators, medical imaging devices, and industrial automation systems.

The market growth is driven by increasing demand in healthcare applications such as ultrasound equipment, alongside expanding industrial automation needs. While the U.S. dominates with a projected 2024 market size of USD 320 million, China is rapidly catching up with an estimated USD 280 million valuation. The power ultrasonic transducers segment shows particular promise, expected to grow at 7.3% CAGR through 2030 due to widespread adoption in cleaning and welding applications. Leading manufacturers including PI Ceramic, APC International, and Murata hold approximately 45% of the global market share.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand in Medical Imaging to Accelerate Piezoelectric Ceramic Transducer Adoption

The medical imaging sector’s rapid expansion is significantly driving demand for piezoelectric ceramic transducers. These components are critical in ultrasound imaging systems, where they convert electrical signals into high-frequency sound waves for diagnostic purposes. With technological advancements enabling higher-resolution imaging, transducer materials with superior piezoelectric properties are increasingly sought after. Recent innovations in 3D/4D ultrasound and portable diagnostic devices have further amplified market growth, with medical applications accounting for over 35% of the total transducer market revenue. The aging global population and rising prevalence of chronic diseases are key factors sustaining this demand, as non-invasive diagnostic tools become essential in modern healthcare.

Automotive Sensor Expansion Creates New Growth Avenues

Automotive manufacturers are increasingly incorporating piezoelectric transducers in advanced driver assistance systems (ADAS) and parking sensors, creating substantial market opportunities. The transition toward autonomous vehicles, combined with stricter safety regulations, has led to transducer integration in blind-spot detection, collision avoidance, and ultrasonic parking systems. Industry data indicates that the average premium vehicle now contains 8-12 ultrasonic sensors, with mid-range models following this technology adoption trend. Furthermore, the electric vehicle boom presents additional applications in battery health monitoring systems, where transducers detect structural changes in battery components, enhancing safety and performance.

Industrial Automation Wave Boosts Market Prospects

The fourth industrial revolution is driving unprecedented demand for precise measurement and control systems where piezoelectric transducers play a vital role. In manufacturing environments, these components enable critical functions such as non-destructive testing, flow measurement, and precision positioning systems. The growing adoption of industrial IoT solutions has created a D 2.4 billion opportunity for smart sensing technologies that incorporate advanced transducer elements. Recent developments in Industry 4.0 have particularly emphasized the need for robust, high-temperature-resistant piezoelectric materials that can withstand harsh industrial conditions while maintaining accuracy.

MARKET RESTRAINTS

Material Limitations Challenge Performance in Extreme Conditions

While piezoelectric ceramics offer excellent electromechanical coupling, they face significant performance degradation in high-temperature and high-humidity environments. This limits their application in sectors like aerospace and energy, where components often operate above 200°C – beyond the Curie temperature of most commercial piezoelectric materials. Recent studies indicate that nearly 15% of potential industrial applications currently avoid piezoelectric solutions due to these material constraints. The development of new composite materials and doping techniques shows promise but requires substantial R&D investment before commercial viability can be achieved.

Complex Manufacturing Processes Elevate Production Costs

The precision required in piezoelectric ceramic transducer manufacturing creates substantial cost barriers. The process involves multiple high-precision steps including powder preparation, sintering, poling, and electrode deposition, each requiring specialized equipment and expertise. Small variations in any manufacturing parameter can significantly impact product performance, leading to yield challenges. Production cost analyses reveal that material waste accounts for approximately 25-30% of total manufacturing expenses in this sector. While automated production techniques are being developed, the capital investment required presents a significant hurdle for market newcomers.

Regulatory Hurdles in Medical Applications

Stringent regulatory requirements for medical device components create lengthy approval timelines for new piezoelectric transducer designs. The FDA’s increasingly rigorous performance and biocompatibility standards have extended the average certification period for new medical ultrasound transducers to 18-24 months. This regulatory burden particularly impacts small and medium manufacturers, who may lack the resources to navigate complex compliance processes. Additionally, divergent standards across regions create challenges for companies operating in global markets, requiring multiple certification processes for essentially identical products.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impact Raw Material Availability

Piezoelectric Ceramic Transducer Market faces significant supply chain challenges, particularly regarding rare earth materials essential for producing advanced piezoceramics. Over 85% of global rare earth production is concentrated in a single geographic region, creating vulnerability to geopolitical tensions and trade restrictions. Recent disruptions have caused lead times for critical raw materials to extend beyond six months, forcing manufacturers to maintain large inventories. Additionally, the specialized nature of these supply chains makes alternative sourcing difficult, with qualification of new material sources often requiring 12-18 months of testing.

Skilled Workforce Shortage Limits Innovation

The highly specialized nature of piezoelectric technology has created a talent gap that threatens market growth. Industry surveys indicate that over 60% of manufacturers report difficulty finding engineers with expertise in both materials science and precision transducer design. The interdisciplinary knowledge required—spanning ceramics engineering, electrical engineering, and acoustics—makes workforce development particularly challenging. While academic programs are beginning to address this need, the time lag between educational initiatives and industry-ready professionals continues to constrain market expansion.

Competition from Alternative Technologies

Emerging sensing technologies present increasing competition for certain piezoelectric transducer applications. Optical and MEMS-based sensors are making inroads in markets traditionally dominated by piezoelectric solutions, particularly in industrial automation and consumer electronics. While piezoceramics maintain advantages in specific frequency ranges and power handling capabilities, ongoing improvements in competing technologies have eroded some market share. Manufacturers must continually demonstrate the cost-performance benefits of their solutions, particularly in price-sensitive applications where alternatives may offer adequate performance at lower cost points.

MARKET OPPORTUNITIES

Energy Harvesting Applications Present Untapped Potential

The growing focus on sustainable energy solutions has created significant opportunities for piezoelectric transducers in energy harvesting applications. Urban infrastructure projects are increasingly incorporating piezoelectric elements in sidewalks, roads, and building materials to convert mechanical vibrations into usable electricity. Pilot projects demonstrate that strategic placement of these systems can generate 5-15 watts per square meter in high-traffic areas. The Internet of Things (IoT) sector also presents opportunities for self-powered sensors using piezoelectric energy harvesters, eliminating battery replacement needs in remote monitoring applications.

Emerging Markets Offer Expansion Potential

Developing economies in Asia and Latin America present substantial growth opportunities as their healthcare and industrial sectors modernize. Governments in these regions are investing heavily in medical infrastructure, with ultrasound systems being prioritized due to their diagnostic versatility and relatively low cost compared to other imaging modalities. Economic data suggests that healthcare expenditure in these markets is growing at 8-12% annually, significantly faster than developed markets. Local manufacturing initiatives and favorable investment policies are making these regions increasingly attractive for transducer manufacturers looking to establish production facilities closer to growth markets.

Material Science Breakthroughs Enable New Applications

Recent advancements in piezoelectric materials are unlocking previously inaccessible applications. The development of lead-free piezoceramics addresses environmental concerns while maintaining performance characteristics, potentially opening markets with strict material regulations. Novel composite materials combining piezoelectric ceramics with polymers or metals are demonstrating improved toughness and flexibility, enabling applications in wearable devices and flexible electronics. Research investments in this sector have increased by 40% over the past five years, indicating strong confidence in future breakthroughs that could significantly expand the addressable market for piezoelectric technologies.

PIEZOELECTRIC CERAMIC TRANSDUCER MARKET TRENDS

Expanding Applications in Medical and Industrial Sectors Driving Market Growth

Global Piezoelectric Ceramic Transducer Market is experiencing robust growth, propelled by increasing adoption across healthcare, industrial automation, and consumer electronics. With an estimated market valuation of D 900 million in 2024, the sector is projected to grow at a CAGR of 6.8% through 2032. Medical imaging equipment such as ultrasound scanners account for nearly 35% of total demand, while industrial non-destructive testing applications are growing at 8.2% annually. Technological improvements in material composition have enhanced energy conversion efficiency above 85% in modern transducers, making them indispensable for precision applications.

Other Trends

Miniaturization and IoT Integration

Advances in microfabrication techniques are enabling smaller, more efficient piezoelectric transducers that integrate seamlessly with IoT devices. The market for MEMS-based piezoelectric components grew by 12.4% in 2023, particularly for wearable health monitors and smart industrial sensors. Manufacturers are shifting toward lead-free piezoelectric ceramics to comply with RoHS and REACH regulations, with zirconate titanate alternatives showing promise in maintaining performance while meeting environmental standards.

Regional Manufacturing Shifts and Supply Chain Optimization

While China dominates production with over 45% market share, rising labor costs are prompting manufacturers to diversify operations to Southeast Asia and Eastern Europe. The U.S. and EU markets are responding with increased R&D investments, growing at 7.1% and 6.3% CAGR respectively. Automotive applications for parking sensors and fuel injectors represent a D 220 million segment, with demand accelerating as electric vehicle adoption intensifies globally. Meanwhile, emerging applications in energy harvesting systems are projected to triple market value by 2028.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Expand Technological Capabilities to Capture Market Share

Global Piezoelectric Ceramic Transducer Market exhibits a moderately fragmented competitive landscape, characterized by the presence of both established manufacturers and emerging innovators. TG (Tokyo Denpa Co., Ltd.) and HC Sonic have emerged as frontrunners in the industry, commanding significant market share due to their extensive product portfolios and strong foothold in Asian markets. These companies have invested heavily in precision engineering capabilities to meet growing demand from industrial automation and medical imaging applications.

Meanwhile, Western competitors like PI (Physik Instrumente) and APC International maintain technological leadership through proprietary material formulations and custom transducer solutions. Their dominance in high-performance applications such as aerospace and defense systems stems from rigorous quality standards and advanced R&D facilities. The European market particularly favors these precision-focused manufacturers for mission-critical implementations.

Chinese manufacturers including Hongsheng Acoustics and Kesen are rapidly gaining traction through cost-effective volume production. Their competitive pricing strategies have enabled significant penetration in consumer electronics and automotive sensor markets. However, these players now face increasing pressure to enhance product reliability and technical support services to compete with established global brands.

The market has witnessed strategic consolidation in recent years, with notable acquisitions strengthening geographical presence. Most manufacturers are channeling investments into next-generation composite materials and miniaturized designs, anticipating future demand from emerging IoT and wearable technology segments. Service differentiators such as application engineering support and rapid prototyping capabilities are becoming key competitive advantages in this technically demanding sector.

List of Key Piezoelectric Ceramic Transducer Manufacturers

- TG (Tokyo Denpa) (Japan)

- HC Sonic (China)

- PI (Physik Instrumente) (Germany)

- SE (Sensitron) (U.S.)

- Hongsheng Acoustics (China)

- Kesen (China)

- Devey (U.K.)

- Henbo (Japan)

- SWT (South Korea)

- NTK (Japan)

- Siansonic (China)

- APC International (U.S.)

- Piezo Technologies (U.S.)

Segment Analysis:

By Type

Power Ultrasonic Transducers Lead the Market Due to Wide Industrial Applications

The market is segmented based on type into:

- Power Ultrasonic Transducers

- Subtypes: High-power, medium-power, and low-power

- Test Ultrasonic Transducers

- Subtypes: Contact, immersion, and delay line

By Application

Industrial Automation Dominates Due to Increasing Demand for Smart Sensors

The market is segmented based on application into:

- Piezo Switches

- Ink Printing Head

- Video Triggers

- Piezoelectric Gyrometer

- Others

By End-User Industry

Manufacturing Sector Accounts for Significant Adoption

The market is segmented based on end-user industry into:

- Automotive

- Healthcare

- Consumer Electronics

- Industrial Manufacturing

- Aerospace & Defense

Regional Analysis: Piezoelectric Ceramic Transducer Market

Asia-Pacific

The Asia-Pacific region dominates the global Piezoelectric Ceramic Transducer Market, driven by rapid industrialization and technological advancements in countries like China, Japan, and South Korea. China leads production and consumption due to its massive electronics manufacturing sector, which accounts for over 40% of global demand. The country’s focus on ultrasonic applications in healthcare (e.g., medical imaging) and industrial automation has accelerated market growth. Meanwhile, Japan remains a hub for high-precision transducer development, particularly for automotive sensors and consumer electronics. India is emerging as a key growth market with increasing adoption in energy harvesting and vibration detection systems, supported by government initiatives like Make in India.

North America

North America represents the second-largest market, with the U.S. contributing approximately 30% of regional revenue. The presence of major players like APC International and Piezo Technologies drives innovation in advanced applications such as aerospace sensors and precision instrumentation. Stringent FDA regulations for medical devices have increased demand for high-quality ultrasonic transducers in diagnostic equipment. The region also sees growing R&D investments in piezoelectric energy harvesting technologies for IoT applications. Canada’s market is smaller but shows steady growth in industrial NDT (non-destructive testing) applications.

Europe

Europe maintains a strong position in specialized piezoelectric transducer applications, particularly in Germany and the UK. The automotive sector accounts for significant demand, with piezoelectric components used in fuel injection systems and active vibration control. EU environmental directives promoting energy-efficient technologies have boosted adoption in smart building systems and energy harvesting devices. France and Italy show increasing demand for medical ultrasound transducers, while Nordic countries focus on marine acoustic applications. However, high production costs compared to Asian manufacturers remain a challenge for regional growth.

South America

The South American market is developing, with Brazil as the primary consumer of piezoelectric transducers for industrial automation and consumer electronics. Argentina shows potential in agricultural ultrasonic applications for pesticide spraying systems. Infrastructure limitations and economic instability have slowed adoption compared to other regions, but increasing foreign investments in manufacturing are creating opportunities. The market remains price-sensitive, favoring imports of cost-effective Asian products over locally manufactured alternatives.

Middle East & Africa

This region represents an emerging market, with growth centered in UAE and South Africa. The oil & gas industry drives demand for ultrasonic transducers in pipeline monitoring and equipment maintenance. Israel has developed niche applications in defense and security systems. While infrastructure development is creating opportunities in building automation, limited local manufacturing capabilities and reliance on imports constrain market expansion. Long-term growth potential exists as industrialization accelerates across the region.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Piezoelectric Ceramic Transducer Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Piezoelectric Ceramic Transducer market was valued at USD 1.73 billion in 2024 and is projected to reach USD 2.84 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Power Ultrasonic Transducers, Test Ultrasonic Transducers), application (Piezo Switches, Ink Printing Head, Video Triggers, Piezoelectric Gyrometer), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including TG, HC Sonic, PI, SE, Hongsheng Acoustics, Kesen, Devey, Henbo, SWT, and NTK, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in piezoelectric materials, manufacturing processes, and application-specific transducer designs.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges in raw material supply, manufacturing complexity, and competition from alternative technologies.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding market opportunities and strategic positioning.

The research employs both primary and secondary methods, including interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Piezoelectric Ceramic Transducer Market?

-> Piezoelectric Ceramic Transducer Market size was valued at USD 1.73 billion in 2024 and is projected to reach USD 2.84 billion by 2032, at a CAGR of 6.4% during the forecast period 2025-2032.

Which key companies operate in Global Piezoelectric Ceramic Transducer Market?

-> Key players include TG, HC Sonic, PI, SE, Hongsheng Acoustics, Kesen, Devey, Henbo, SWT, and NTK, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for ultrasonic applications, automation in manufacturing, and advancements in medical imaging technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America holds significant market share due to technological advancements.

What are the emerging trends?

-> Emerging trends include development of lead-free piezoelectric materials, miniaturization of transducers, and integration with IoT applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...