MARKET INSIGHTS

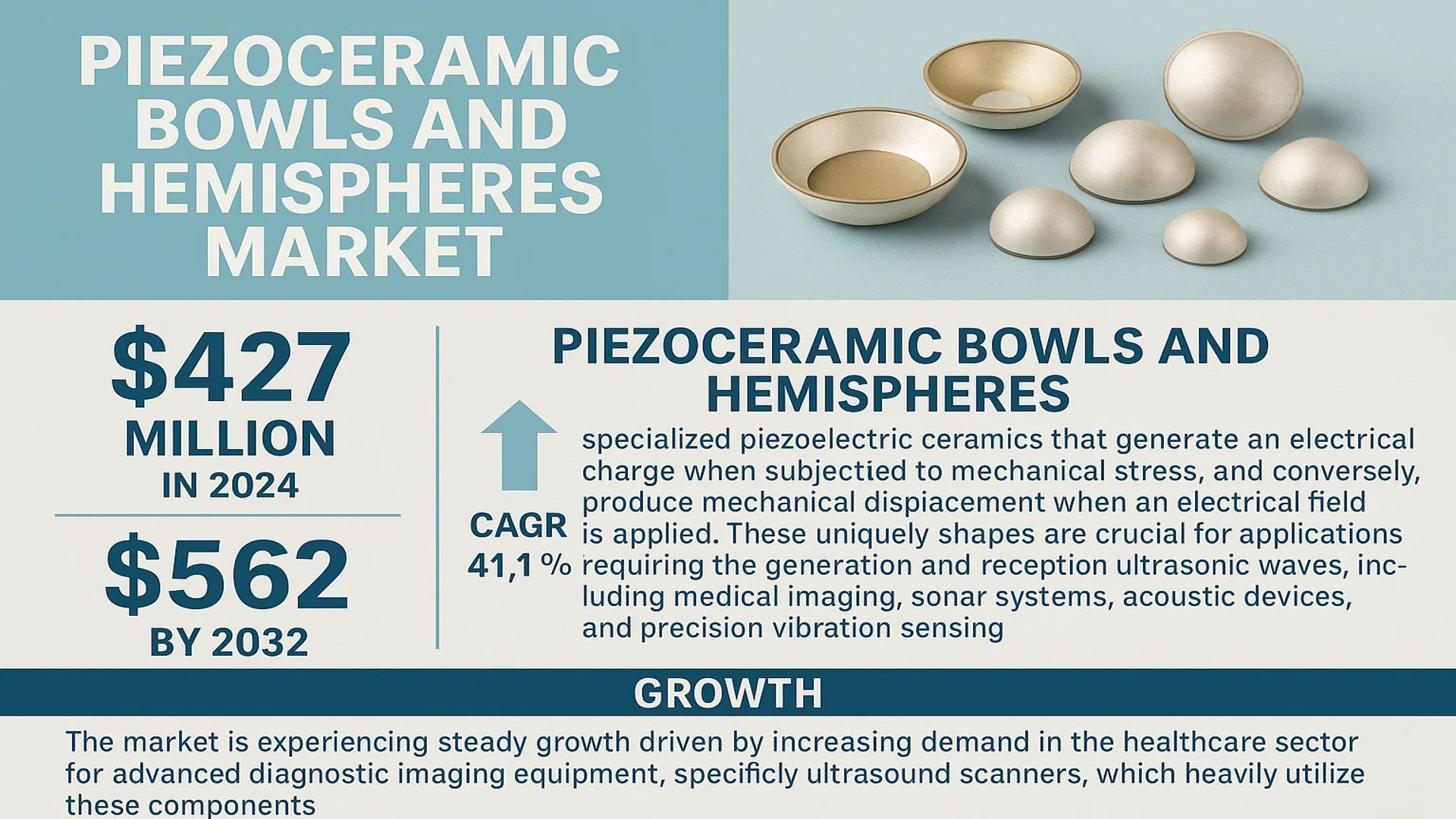

The global Piezoceramic Bowls and Hemispheres Market was valued at 427 million in 2024 and is projected to reach US$ 562 million by 2032, at a CAGR of 4.1% during the forecast period.

Piezoceramic bowls and hemispheres are specialized piezoelectric ceramic components that generate an electrical charge when subjected to mechanical stress, and conversely, produce mechanical displacement when an electrical field is applied. These uniquely shaped components are crucial for applications requiring the generation and reception of ultrasonic waves, including medical imaging, sonar systems, acoustic devices, and precision vibration sensing.

The market is experiencing steady growth driven by increasing demand in the healthcare sector for advanced diagnostic imaging equipment, such as ultrasound scanners, which heavily utilize these components. Furthermore, expansion in underwater sonar applications for defense and marine exploration contributes significantly to market expansion. The PZT (Lead Zirconate Titanate) material segment dominates the market due to its superior piezoelectric properties. Key players, including CTS Corporation, PI Ceramic, and CeramTec, are focusing on technological advancements and strategic collaborations to strengthen their market position and cater to the evolving needs of various high-tech industries.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Medical Imaging Applications to Propel Market Growth

The global piezoceramic bowls and hemispheres market is experiencing significant growth driven by expanding applications in medical imaging technologies. Ultrasonic transducers utilizing these components are fundamental to diagnostic ultrasound systems, which represent over 40% of the global medical imaging equipment market. The increasing prevalence of chronic diseases requiring frequent diagnostic imaging, coupled with aging populations worldwide, has created sustained demand for advanced medical imaging solutions. Recent technological advancements have enabled higher frequency transducers capable of providing superior image resolution, particularly in ophthalmology and dermatology applications where precision imaging is critical. The medical ultrasound equipment market is projected to maintain a growth rate exceeding 5% annually, directly driving demand for high-performance piezoceramic components.

Growing Defense and Marine Sonar Expenditure to Accelerate Market Expansion

Defense modernization programs and increasing maritime security concerns are significantly contributing to market growth. Global military expenditure reached approximately 2.2 trillion dollars in recent years, with naval defense systems accounting for a substantial portion of this investment. Piezoceramic bowls and hemispheres are critical components in sonar systems used for submarine detection, underwater navigation, and marine research applications. The increasing deployment of autonomous underwater vehicles (AUVs) and unmanned underwater vehicles (UUVs) for both military and commercial purposes has created additional demand for compact, high-performance acoustic transducers. Naval modernization programs across Asia-Pacific regions, particularly in countries with extensive coastlines, are driving substantial investments in advanced sonar technologies that utilize these specialized components.

Advancements in Industrial Automation and Non-Destructive Testing to Fuel Demand

Industrial automation and quality control applications represent another significant growth driver for the piezoceramic components market. The global non-destructive testing (NDT) market is expanding at approximately 8% annually, driven by increasing requirements for structural integrity testing in aerospace, automotive, and construction industries. Piezoceramic hemispheres are extensively used in ultrasonic testing equipment for detecting flaws and measuring material thickness without causing damage. The automation of manufacturing processes has also increased the adoption of ultrasonic sensors for precision measurement, object detection, and process control applications. The industrial sensors market, which incorporates these piezoelectric components, is projected to grow significantly as industries continue to prioritize efficiency and quality assurance measures.

MARKET CHALLENGES

High Manufacturing Complexity and Precision Requirements to Constrain Market Development

The production of piezoceramic bowls and hemispheres involves complex manufacturing processes that present significant challenges for market participants. These components require extremely precise geometrical tolerances, often within micrometer ranges, to ensure optimal acoustic performance and electrical characteristics. The manufacturing process involves multiple critical stages including powder preparation, forming, sintering, electrode application, and poling, each requiring specialized equipment and stringent quality control measures. The capital investment for establishing production facilities can exceed several million dollars, creating substantial barriers to entry for new market participants. Additionally, maintaining consistent quality across production batches remains challenging due to the sensitive nature of piezoelectric properties and the need for precise material composition control.

Other Challenges

Material Sourcing and Supply Chain Vulnerabilities

The market faces significant challenges related to raw material availability and supply chain stability. Key materials including lead zirconate titanate (PZT) require rare earth elements and specialized ceramic compounds that are subject to price volatility and supply disruptions. Recent global supply chain issues have highlighted the vulnerability of dependent industries, with lead times for certain critical materials extending beyond six months in some cases. The specialized nature of these materials means that few suppliers exist globally, creating potential bottlenecks and price inflation risks that can significantly impact manufacturing costs and profitability.

Technical Performance Limitations in Extreme Environments

Performance limitations under extreme operating conditions present ongoing challenges for market advancement. Piezoceramic components exhibit temperature-dependent characteristics that can affect their performance in high-temperature applications exceeding 150°C. Additionally, these materials face degradation issues when exposed to high humidity environments or corrosive substances, limiting their application in certain industrial and marine settings. The development of materials capable of maintaining stable piezoelectric properties across wider temperature ranges and harsh environmental conditions remains a significant technical challenge that requires continued research and development investment.

MARKET RESTRAINTS

Environmental Regulations and Material Restrictions to Limit Market Progress

Stringent environmental regulations governing the use of lead-based materials represent a significant restraint for market growth. Lead zirconate titanate (PZT), which accounts for approximately 75% of piezoceramic components, contains substantial lead content that falls under strict environmental regulations such as the Restriction of Hazardous Substances (RoHS) directive. These regulations require manufacturers to implement comprehensive waste management systems and environmental protection measures, increasing operational costs significantly. The development of lead-free alternatives has progressed but these materials generally exhibit inferior piezoelectric properties compared to traditional PZT compositions. The regulatory pressure is particularly strong in European markets, where environmental standards are among the most rigorous globally, potentially limiting market expansion in these regions.

Intensive Research and Development Requirements to Hinder Market Expansion

The requirement for continuous research and development investment presents another significant market restraint. Developing advanced piezoceramic formulations with improved performance characteristics requires substantial financial resources and specialized expertise. The average research and development expenditure for companies in this sector typically ranges between 8-12% of annual revenue, representing a considerable financial burden particularly for smaller market participants. Additionally, the lengthy development cycles for new materials and manufacturing processes, often extending beyond three years from concept to commercial production, delay market responsiveness to emerging application requirements. This extensive development timeline combined with high failure rates in new material development creates financial risks that can deter investment and innovation within the industry.

Technical Specialization and Workforce Limitations to Impede Market Growth

The highly specialized nature of piezoceramic technology creates significant workforce challenges that restrain market development. The industry requires professionals with expertise in materials science, electrical engineering, acoustics, and precision manufacturing – a combination of skills that is rare in the labor market. The aging workforce in traditional manufacturing sectors and the limited educational programs focused on advanced ceramic technologies have created a talent shortage that affects companies globally. This skills gap is particularly acute in regions with developing piezoceramic industries, where experienced professionals are scarce and training new personnel requires substantial time investment. The competition for qualified technical staff has driven labor costs upward, affecting overall production economics and potentially limiting market competitiveness.

MARKET OPPORTUNITIES

Emerging Applications in Energy Harvesting and IoT Devices to Create New Growth Avenues

The expanding Internet of Things (IoT) ecosystem and growing focus on sustainable energy solutions present substantial opportunities for market expansion. Piezoceramic components are increasingly being utilized in energy harvesting applications where mechanical vibrations are converted into electrical energy to power wireless sensors and low-power electronic devices. The global energy harvesting system market is projected to grow at approximately 10% annually, driven by increasing deployment of IoT devices in industrial, automotive, and smart infrastructure applications. The development of more efficient piezoceramic materials capable of generating higher power outputs from ambient vibrations opens new application possibilities in remote monitoring systems and self-powered sensors, particularly in environments where battery replacement is impractical or costly.

Advancements in Automotive Sensor Technologies to Drive Future Market Growth

The automotive industry’s transformation toward electrification and advanced driver assistance systems (ADAS) creates significant opportunities for piezoceramic component manufacturers. Modern vehicles incorporate numerous ultrasonic sensors for parking assistance, blind spot detection, and collision avoidance systems, with premium vehicles containing up to twelve ultrasonic sensors each. The transition toward autonomous driving systems is expected to further increase the adoption of acoustic sensors utilizing piezoceramic components. The global automotive sensor market is anticipated to grow substantially as vehicle automation levels increase, with ultrasonic sensors representing a critical technology for short-range object detection and distance measurement applications. This automotive sector expansion provides a substantial growth opportunity for manufacturers of precision piezoceramic bowls and hemispheres.

Development of Advanced Composite Materials to Enable New Application Areas

Technological innovations in material science present promising opportunities for market diversification. Recent developments in composite piezoceramic materials, including polymer-ceramic composites and textured ceramics, offer improved performance characteristics that enable new application possibilities. These advanced materials provide enhanced flexibility, improved acoustic impedance matching, and better mechanical durability compared to traditional piezoceramics. The development of these materials enables applications in wearable medical devices, structural health monitoring systems, and advanced acoustic transducers for scientific research. The ongoing research in lead-free piezoceramic materials also addresses environmental concerns while maintaining performance standards, potentially opening new market segments in environmentally sensitive applications and regions with strict material regulations.

PIEZOCERAMIC BOWLS AND HEMISPHERES MARKET TRENDS

Advancements in Medical Imaging and Ultrasonic Technologies Driving Market Growth

The global piezoceramic bowls and hemispheres market is experiencing significant growth, primarily driven by advancements in medical imaging technologies. These components are critical in ultrasonic transducers used for diagnostic imaging, such as ultrasound scanners and high-intensity focused ultrasound (HIFU) systems for non-invasive surgery. The medical imaging segment accounted for approximately 38% of the total market revenue in 2024, with an estimated value of $162 million. This growth is further accelerated by the increasing prevalence of chronic diseases requiring advanced diagnostic tools and the global shift towards minimally invasive surgical procedures. The integration of artificial intelligence with ultrasound imaging has created new demand patterns for higher precision piezoceramic components capable of producing cleaner acoustic signals with reduced harmonic distortion. Furthermore, the aging global population and rising healthcare expenditures in developed economies are contributing to sustained investment in medical imaging infrastructure, thereby supporting market expansion.

Other Trends

Expansion in Marine and Defense Applications

The marine and defense sectors represent a substantial growth area for piezoceramic bowls and hemispheres, particularly in sonar systems for underwater detection and navigation. Modern naval defense strategies increasingly rely on advanced sonar technologies for submarine detection, mine hunting, and underwater surveillance. The global sonar market, which heavily utilizes these components, is projected to reach $2.8 billion by 2028, creating significant downstream demand for high-performance piezoceramic elements. Additionally, the growing commercial maritime industry requires sophisticated echo-sounding equipment for seabed mapping and fishery applications. Recent developments in multi-beam sonar systems have created demand for larger and more complex piezoceramic hemispheres capable of operating across broader frequency ranges and with higher power handling capabilities. The increasing geopolitical tensions in various maritime regions have also prompted several nations to enhance their naval capabilities, further driving procurement of sonar systems utilizing these specialized components.

Material Innovation and Environmental Regulations Shaping Product Development

Material science innovations are significantly influencing the piezoceramic bowls and hemispheres market, particularly regarding the development of lead-free alternatives. While traditional lead zirconate titanate (PZT) compositions dominate the market with approximately 72% share due to their superior piezoelectric properties, increasing environmental regulations regarding lead content in electronic components are driving research into alternative materials. The European Union’s Restriction of Hazardous Substances (RoHS) directive and similar regulations in other regions have accelerated the development of viable lead-free piezoceramics, though these alternatives currently face challenges in matching the performance characteristics of PZT-based materials. Manufacturers are investing heavily in research to improve the performance of lithium niobate and barium titanate formulations, with several companies announcing breakthrough developments in achieving higher piezoelectric coefficients in lead-free compositions. This trend is particularly relevant for medical applications where material biocompatibility and environmental safety are paramount concerns. The ongoing material innovation is expected to create new market segments while potentially disrupting established supply chains and manufacturing processes.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Strategic Expansion to Maintain Market Position

The global piezoceramic bowls and hemispheres market exhibits a semi-consolidated competitive structure, featuring a mix of established multinational corporations and specialized regional manufacturers. CTS Corporation emerges as a dominant player, leveraging its extensive expertise in piezoelectric materials and strong distribution networks across North America, Europe, and Asia-Pacific. The company’s significant market position is reinforced by its continuous investment in research and development, particularly in advanced PZT formulations that offer superior electromechanical coupling coefficients.

PI Ceramic and CeramTec GmbH also command substantial market shares, driven by their specialized product portfolios and technological leadership in high-performance piezoceramic components. These companies have demonstrated remarkable growth through their focus on custom solutions for medical imaging and sonar applications, where precision and reliability are paramount. Their expansion strategies often involve collaborations with end-users to develop application-specific geometries and material properties.

Meanwhile, APC International and Sparkler Ceramics are strengthening their global footprint through strategic acquisitions and capacity expansions. APC International’s recent manufacturing facility enhancement in the United States has significantly increased its production capabilities for large-diameter piezoceramic hemispheres, catering to the growing sonar and marine exploration sectors. Similarly, Sparkler Ceramics has expanded its Asian market presence through technical partnerships with medical device manufacturers.

The competitive landscape is further characterized by increasing vertical integration, with leading players investing in backward integration to control raw material quality and supply chain stability. This trend is particularly evident among manufacturers specializing in lead zirconate titanate (PZT) compositions, where consistent material properties are critical for application performance. Companies are also focusing on developing environmentally sustainable manufacturing processes to address regulatory requirements, especially in European and North American markets.

List of Key Piezoceramic Bowls and Hemispheres Manufacturers Profiled

- CTS Corporation (U.S.)

- PI Ceramic GmbH (Germany)

- CeramTec GmbH (Germany)

- APC International, Ltd. (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Wingtek International Co., Limited (China)

- Zibo Yuhai Electronic Ceramic Co., Ltd. (China)

- PZT Electronic Ceramic Co., Ltd. (China)

- TJ Piezo Specialties Co., Ltd. (China)

- HE SHUAI Technology Co., Ltd. (China)

- Sparkler Ceramics Pvt. Ltd. (India)

- Fbelec Company Limited (China)

- Sino Sonics Co., Ltd. (China)

- Weifang Jude Electronic Co., Ltd. (China)

Segment Analysis:

By Type

PZT (Lead Zirconate Titanate) Segment Dominates the Market Due to Superior Piezoelectric Properties and Wide Application Compatibility

The market is segmented based on material type into:

- PZT (Lead Zirconate Titanate)

- Lithium Niobate (LiNbO₃)

- PVDF (Polyvinylidene Fluoride)

- Others

By Application

Medical Imaging Segment Leads Due to Critical Role in Ultrasonic Transducers for Diagnostic Equipment

The market is segmented based on application into:

- Medical Imaging

- Acoustic & Audio Devices

- Sonar & Marine

- Others

By End-User Industry

Healthcare and Life Sciences Segment is a Major Consumer Driven by Demand for Advanced Diagnostic Tools

The market is segmented based on end-user industry into:

- Healthcare and Life Sciences

- Defense and Aerospace

- Industrial Manufacturing

- Consumer Electronics

- Others

By Manufacturing Process

Dry Pressing Segment Holds Significant Share Owing to its Efficiency in Producing High-Density, Complex Shapes

The market is segmented based on manufacturing process into:

- Dry Pressing

- Injection Molding

- Tape Casting

- Others

Regional Analysis: Piezoceramic Bowls and Hemispheres Market

Asia-Pacific

The Asia-Pacific region dominates the global market, accounting for the largest revenue share and highest volume consumption. This leadership is driven by robust manufacturing ecosystems, particularly in China, Japan, and South Korea, which are global hubs for electronics and advanced materials production. China’s significant investments in medical imaging infrastructure and naval defense systems are key drivers, with the country projected to reach a substantial market valuation by 2032. The region benefits from strong government support for technological innovation and a vast network of component suppliers. While cost-competitive manufacturing remains a hallmark, there is a clear trend toward producing higher-value, precision components for advanced applications in healthcare and industrial automation.

North America

North America represents a highly advanced and technologically sophisticated market, characterized by stringent quality standards and significant investment in research and development. The United States, with its large defense budget and advanced healthcare sector, is a primary consumer of high-performance piezoceramic components for sonar systems, medical diagnostic equipment, and aerospace applications. The presence of leading manufacturers like CTS Corporation and APC International reinforces the region’s focus on innovation and premium products. Market growth is further supported by strong intellectual property protections and collaborations between academic institutions and industry players, driving advancements in material science and component design.

Europe

Europe maintains a strong position in the market, underpinned by a mature industrial base and a focus on high-precision engineering and sustainability. Germany, with its renowned manufacturing sector, and the United Kingdom, with its significant defense and marine industries, are key contributors. The region’s market is driven by demand from the automotive sector for ultrasonic sensors, the medical device industry for imaging equipment, and environmental monitoring applications. European regulations, particularly concerning the use of lead-based materials like PZT, are pushing innovation toward developing more environmentally friendly alternatives, such as lead-free piezoceramics, which presents both a challenge and an opportunity for manufacturers.

South America

The market in South America is emerging and characterized by gradual growth, primarily fueled by infrastructure development and industrialization in countries like Brazil and Argentina. Demand stems from the oil and gas sector for non-destructive testing equipment and from growing healthcare investments. However, the market’s expansion is often constrained by economic volatility, which impacts capital expenditure on advanced technologies, and a reliance on imported components due to a less developed domestic manufacturing base for specialized piezoceramics. Despite these challenges, long-term potential exists as regional industries continue to modernize.

Middle East & Africa

This region represents a smaller but developing market with potential driven by investments in defense, healthcare, and energy infrastructure. Countries like Israel, with its strong technology sector, and Saudi Arabia and the UAE, with their strategic investments in economic diversification, are showing increased demand for these components. Applications are often focused on oil and gas exploration equipment and medical devices. Market growth, however, is moderated by geopolitical uncertainties, varying levels of industrial development across the region, and a current dependence on imports for high-specification components, limiting the pace of adoption.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Piezoceramic Bowls and Hemispheres markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of advanced materials, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Piezoceramic Bowls and Hemispheres Market?

-> Piezoceramic Bowls and Hemispheres Market was valued at 427 million in 2024 and is projected to reach US$ 562 million by 2032, at a CAGR of 4.1% during the forecast period.

Which key companies operate in Global Piezoceramic Bowls and Hemispheres Market?

-> Key players include CTS Corporation, PI Ceramic, CeramTec, APC International, L3Harris, Wingtek International, Zibo Yuhai Electronic Ceramics, PZT Electronic Ceramic, TJ Piezo Specialties, and HE SHUAI, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for medical imaging devices, advancements in sonar technology, expansion of acoustic and audio applications, and growing adoption in industrial vibration sensing.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include development of lead-free piezoceramic materials, miniaturization of components for portable devices, integration with IoT systems for smart sensing, and advancements in manufacturing precision for specialized applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...