Market Insights

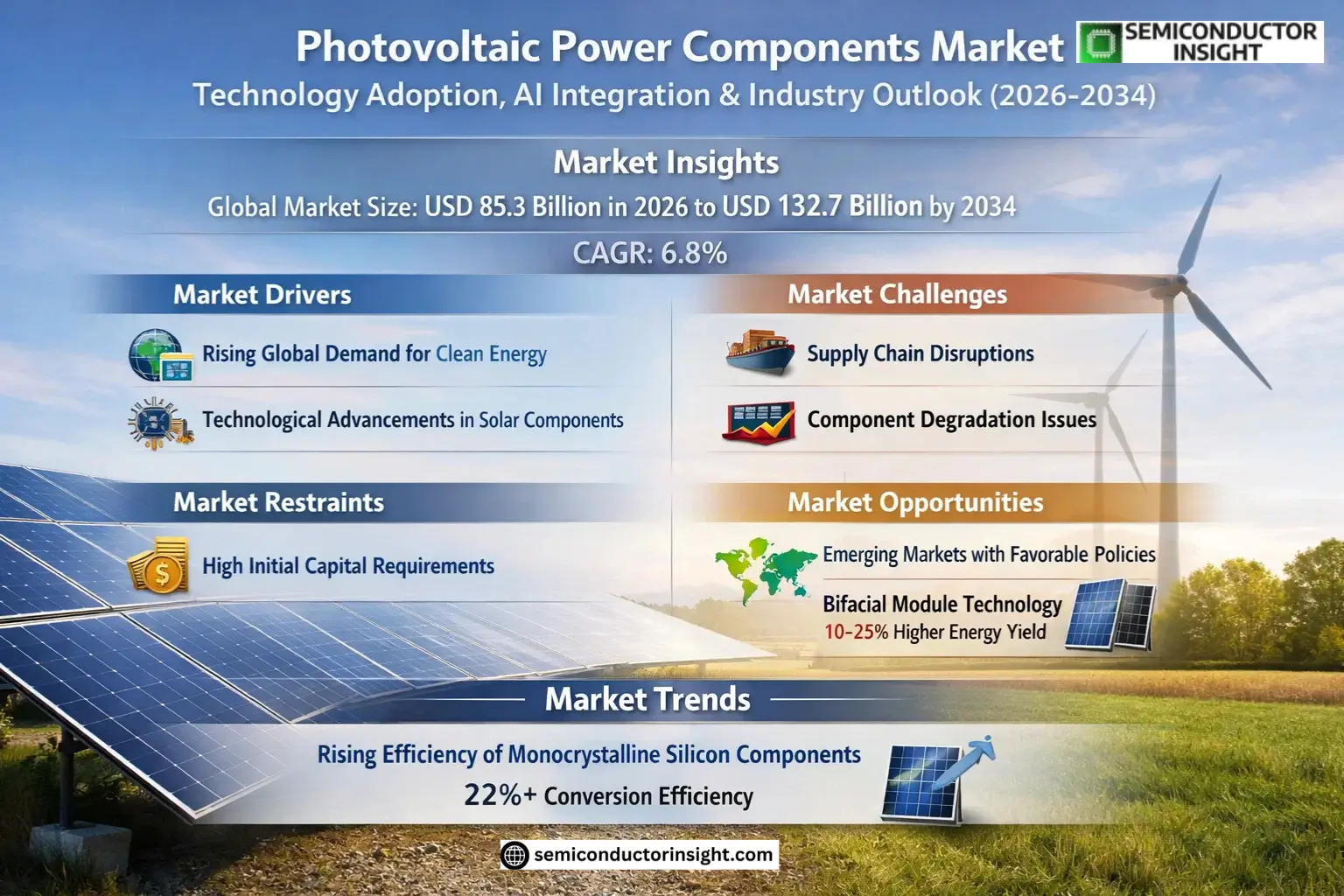

Global Photovoltaic Power Components Market size was valued at USD 78.5 billion in 2025. The market is projected to grow from USD 85.3 billion in 2026 to USD 132.7 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

Photovoltaic power components are optoelectronic devices that convert sunlight into electricity through the photovoltaic effect. These components include solar cells, inverters, mounting systems, and balance-of-system (BOS) components such as wiring and connectors. The technology is widely used in residential, commercial, and utility-scale solar installations.

The market growth is driven by increasing demand for renewable energy solutions, government incentives for solar adoption, and declining costs of photovoltaic technology. Key players like Longji Green Energy, Trina Solar, and First Solar are expanding production capacities to meet rising demand. However, supply chain disruptions and raw material price volatility remain challenges for industry stakeholders.

MARKET DRIVERS

Rising Global Demand for Clean Energy

Photovoltaic Power Components Market is experiencing significant growth due to increasing global demand for renewable energy solutions. Governments worldwide are implementing policies favoring solar energy adoption, with investment in photovoltaic systems growing by approximately 12% annually. Solar module efficiency improvements have further accelerated market expansion.

Technological Advancements in Solar Components

Recent breakthroughs in photovoltaic cell technology, including PERC and heterojunction designs, have boosted power output while reducing manufacturing costs. The average cost of photovoltaic power components has decreased by over 60% in the past decade, making solar energy more accessible. Innovations in mounting systems and inverters are also contributing to market growth.

Modern photovoltaic components now feature enhanced durability and weather resistance, with many manufacturers offering 25+ year performance guarantees, increasing consumer confidence in solar investments.

MARKET CHALLENGES

Supply Chain Disruptions

Photovoltaic Power Components Market faces ongoing challenges from global supply chain constraints, particularly for critical materials like silicon and silver used in solar cell production. Logistics bottlenecks have led to extended lead times and increased costs for system integrators.

Other Challenges

Component Degradation Issues

Despite improvements, photovoltaic components still experience performance degradation of 0.5-1.0% annually, impacting long-term system efficiency and requiring careful maintenance planning.

Regulatory Hurdles

Differing certification requirements and trade policies across countries create complexity for photovoltaic component manufacturers operating in multiple markets.

MARKET RESTRAINTS

High Initial Capital Requirements

Despite cost reductions, photovoltaic power systems still require significant upfront investment, which remains a barrier for many residential and commercial customers. Financing options and government incentives help mitigate this restraint, but access to capital continues to influence market growth rates.

MARKET OPPORTUNITIES

Emerging Markets with Favorable Policies

Developing nations in Asia, Africa, and Latin America are presenting new opportunities for photovoltaic component manufacturers, with governments establishing renewable energy targets and attractive subsidy programs. These regions currently account for approximately 35% of new photovoltaic installations globally.

Bifacial Module Technology

The growing adoption of bifacial photovoltaic modules, which can capture sunlight from both sides, represents a significant growth opportunity. These components can increase energy yield by 10-25% compared to conventional modules, commanding a premium price in the market.

Photovoltaic Power Components Market Trends

Increasing Efficiency of Monocrystalline Silicon Components

Photovoltaic Power Components Market is witnessing significant advancements in monocrystalline silicon technology. Manufacturers are achieving higher conversion efficiencies, with leading products now exceeding 22% efficiency rates. This trend is driven by intensive R&D investments from key players like Tongwei Corporation and Longji Green Energy, pushing the boundaries of photovoltaic performance.

Other Trends

Rise of Bifacial Solar Modules

Bifacial photovoltaic components, which capture sunlight on both sides, are gaining traction in the market. Companies such as Trina Solar and JA Solar Technology report growing demand for these dual-sided solutions, particularly in utility-scale installations where they can deliver up to 15% additional energy yield compared to traditional modules.

Expansion of Thin-Film Photovoltaic Technologies

Photovoltaic Power Components Market shows increasing diversification with thin-film technologies. First Solar continues to lead in cadmium telluride (CdTe) thin-film production, while new entrants are exploring organic and perovskite solar cells. These alternatives offer advantages in lightweight applications and flexible installations across transportation and building-integrated photovoltaics.

Growing Adoption in Emerging Economies

Developing nations are accelerating solar deployments, creating robust demand for photovoltaic components. Markets in Southeast Asia and Africa are seeing particular growth, with regional players adopting solutions tailored to local conditions. This expansion is supported by government incentives and falling component prices.

Integration with Energy Storage Systems

Photovoltaic Power Components Market is increasingly converging with energy storage solutions. Companies like SolarEdge and Enphase Energy are developing integrated systems that combine high-efficiency photovoltaics with smart inverters and battery storage, enhancing system reliability and grid independence for end-users.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Photovoltaic Power Components Market Dominated by Industry Leaders and Emerging Innovators

Photovoltaic Power Components Market is characterized by the dominance of established players like Hamamatsu Photonics and First Solar, which collectively hold significant market shares. The industry exhibits a moderately concentrated structure, with the top five companies accounting for a substantial portion of global revenues in 2025. Market leaders continue to expand their production capacities while investing heavily in R&D for advanced monocrystalline silicon and thin-film technologies.

Alongside these giants, specialized players such as SolarEdge and Enphase Energy are gaining traction with innovative power optimization solutions. Regional manufacturers like Tongwei Corporation and Longji Green Energy are strengthening their positions in Asian markets through cost-effective production strategies. The competitive intensity is further amplified by technological collaborations and strategic acquisitions across the value chain.

List of Key Photovoltaic Power Components Companies Profiled

- Hamamatsu Photonics

- Teledyne Judson Technologies

- Tongwei Corporation

- Longji Green Energy

- JKS-US

- Trina Solar

- JA Solar Technology

- Artus

- First Solar

- Hanwha Q CELLS

- SolarEdge

- Enphase Energy

- SMA Solar Technology

- Canadian Solar

- Renesola

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Monocrystalline Silicon dominates due to:

|

| By Application |

|

Power Industry leads with:

|

| By End User |

|

Utility Providers remain key users because:

|

| By Technology |

|

Standard PV Systems maintain dominance due to:

|

| By Manufacturing Process |

|

Czochralski Process leads market preference because:

|

Regional Analysis: Asia-Pacific Photovoltaic Power Components Market

China maintains vertical integration across the photovoltaic power components value chain, from polysilicon to module assembly. The country’s scale advantages enable cost leadership, with clustered production facilities optimizing logistics and component sourcing.

India’s photovoltaic components market expands rapidly through utility-scale projects and rooftop solar initiatives. Domestic content requirements stimulate local inverter and mounting structure manufacturing while maintaining imports for advanced cell technologies.

Japanese manufacturers lead in high-efficiency photovoltaic components, particularly heterojunction and back-contact cell technologies. The market emphasizes reliability and performance optimization for limited rooftop spaces and challenging installation environments.

Vietnam, Malaysia and Thailand develop photovoltaic component manufacturing capabilities, benefiting from trade policies and lower production costs. The region serves as alternative production bases amid global supply chain diversification trends.

North America

The North American Photovoltaic Power Components Market grows through utility-scale deployments and residential solar adoption. U.S. supply chain initiatives aim to reduce dependence on Asian imports, with new manufacturing facilities emerging for solar cells and trackers. California and Texas drive demand while Canadian provinces implement supportive procurement policies. Emerging bifacial module and PERC cell technologies gain market share alongside smart inverter adoption.

Europe

European markets accelerate photovoltaic component deployment through the REPowerEU initiative, emphasizing energy security. Germany and Spain lead installations while Italy and Poland show rapid growth. The region focuses on sustainable manufacturing practices and circular economy approaches for solar components. Microinverter and power optimizer adoption increases in residential segments along with building-integrated photovoltaic solutions.

Middle East & Africa

Gulf nations invest heavily in utility-scale photovoltaic projects utilizing high-efficiency components suitable for desert conditions. South Africa and Egypt emerge as regional manufacturing hubs while East African nations adopt off-grid solar solutions. The market sees increasing hybrid system deployments combining photovoltaic components with battery storage technologies.

South America

Brazil dominates South America’s photovoltaic components market through distributed generation policies and auction-based utility projects. Chile and Colombia follow with growing commercial and industrial solar adoption. The region benefits from high solar irradiation levels favoring standard module technologies with durable mounting systems for varied terrain.

Report Scope

This market research report provides a comprehensive analysis of the Photovoltaic Power Components Market , covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of photovoltaic components in powering advancements across industries such as power generation, transportation, and communication.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, including Monocrystalline Silicon Photovoltaic Element, Polycrystalline Silicon Photovoltaic Element, Thin Film Photovoltaic Components, and Others, to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies and evolving industry standards in photovoltaic power components.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Photovoltaic Power Components Market?

-> Photovoltaic Power Components Market size was valued at USD 78.5 billion in 2025. The market is projected to grow from USD 85.3 billion in 2026 to USD 132.7 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

Which key companies operate in Photovoltaic Power Components Market?

-> Key players include Hamamatsu Photonics, Teledyne Judson Technologies, Tongwei Corporation, Longji Green Energy, JKS-US, Trina Solar, JA Solar Technology, Artus, First Solar, Hanwha Q CELLS, SolarEdge, Enphase Energy, and SMA Solar Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for renewable energy, government incentives for solar power, and technological advancements in photovoltaic components.

Which region dominates the market?

-> Asia is the dominant market, with China projected to reach USD million by 2034, while the U.S. market is estimated at USD million in 2025.

What are the emerging trends?

-> Emerging trends include advancements in monocrystalline silicon technology, increased adoption of thin film photovoltaic components, and the integration of AI in solar power systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...