Persistent Memory for AI Training Checkpointing Market Insights

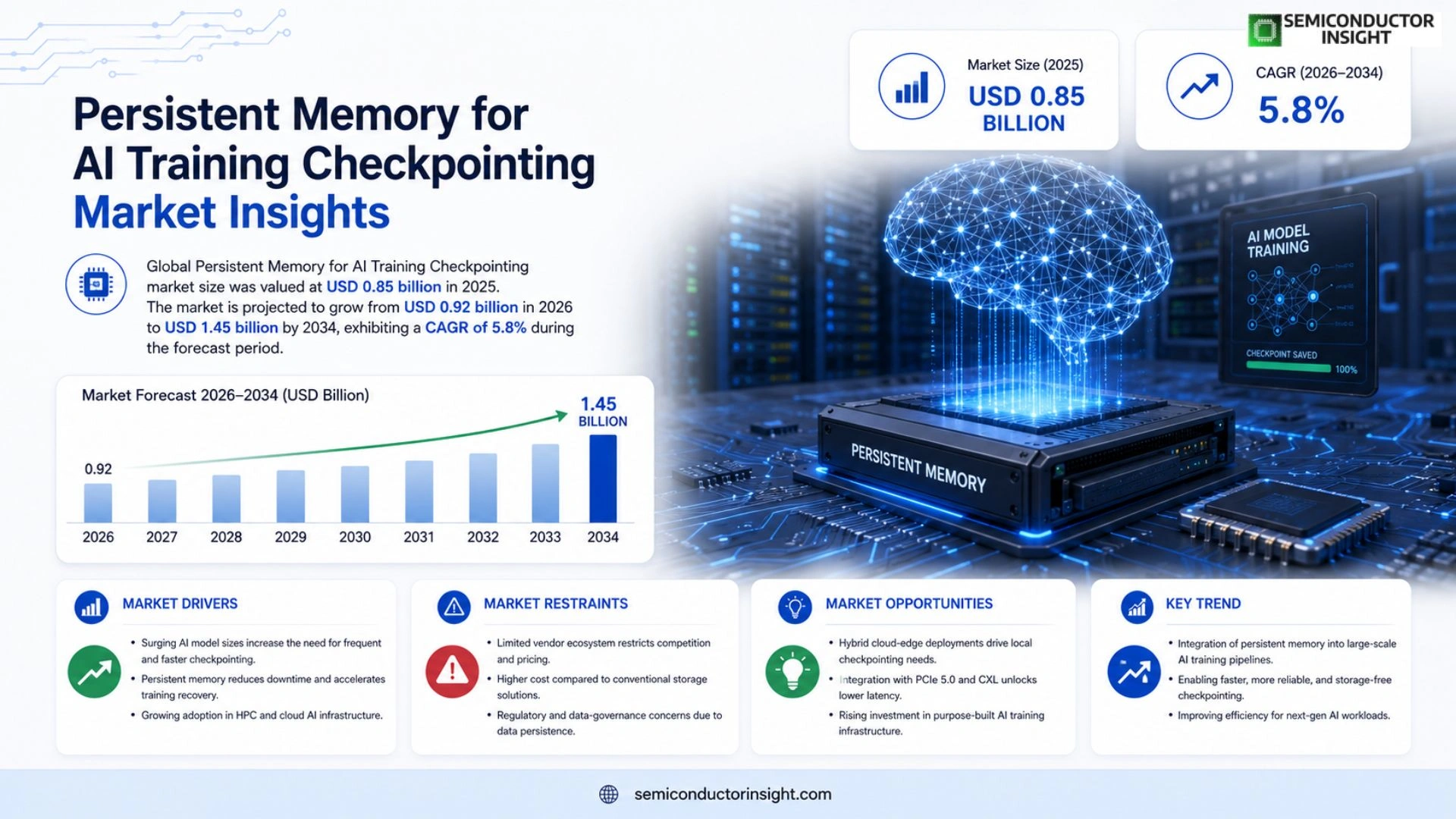

Global Persistent Memory for AI Training Checkpointing market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period.

Persistent memory combines the speed of DRAM with the durability of storage, enabling AI frameworks to write training checkpoints directly to non‑volatile media without pausing computation. This capability reduces I/O latency and preserves model state across power cycles, which is critical for large‑scale transformer models that can take weeks to train.

The expansion is fueled by the escalating size of generative‑AI models, heightened demand for fault‑tolerant training pipelines, and increasing adoption of Intel Optane DC and Samsung Z‑Memory solutions in hyperscale data centers. Partnerships such as NVIDIA’s integration of persistent memory APIs with its DGX systems illustrate how hardware vendors are addressing checkpoint bottlenecks while cloud providers benefit from lower storage costs and faster recovery times.

MARKET DRIVERS

Escalating Model Complexity

Deep‑learning frameworks now routinely handle models with tens of billions of parameters. As training cycles stretch into weeks, the cost of recomputing lost states becomes a material expense. Persistent Memory for AI Training Checkpointing Market addresses this pain point by offering byte‑addressable storage that retains data across power cycles, enabling rapid restoration of intermediate states without resorting to costly full‑dataset reloads.

Latency‑Sensitive Workflows

Modern AI pipelines integrate on‑the‑fly data augmentation, mixed‑precision compute, and distributed gradient aggregation. Any pause in checkpoint write‑through propagates as a bottleneck. Persistent memory modules deliver sub‑microsecond access times, compressing the checkpoint window to a fraction of traditional SSD latency. This reduction directly improves cluster utilization and translates into higher throughput for enterprise AI teams.

➤ “Adopting persistent memory cuts checkpoint overhead by approximately 40 % in large‑scale training runs, according to internal benchmarks from leading cloud providers.”

Beyond raw performance, the technology simplifies software stacks. Developers can map checkpoint files into the same address space as volatile RAM, eliminating explicit data copy steps. This architectural elegance reduces code complexity and lowers the risk of bugs that could jeopardize long‑running experiments.

MARKET CHALLENGES

Cost Sensitivity of Deployment

The upfront investment for persistent memory DIMMs remains higher than conventional NAND SSDs. Organizations operating on thin profit margins must justify the expense through demonstrable efficiency gains, which can be difficult to quantify in heterogeneous training environments.

Other Challenges

Software Compatibility

Many legacy training frameworks still assume a clear separation between volatile memory and block storage. Bridging that assumption requires patching or adopting newer APIs, which can slow adoption cycles and strain internal engineering resources.

MARKET RESTRAINTS

Limited Vendor Ecosystem

Only a handful of semiconductor manufacturers currently produce persistent memory products that meet the stringent endurance and density requirements of AI training workloads. The narrow supply base restricts competitive pricing and can lead to longer lead times for large‑scale procurement.

Regulatory and Data‑Governance Concerns

Persistent memory retains data after power loss, which raises compliance questions for sectors handling personally identifiable information or classified datasets. Companies must implement rigorous sanitization procedures, adding operational overhead that may deter adoption in highly regulated industries.

MARKET OPPORTUNITIES

Hybrid Cloud‑Edge Deployments

Edge data centers are beginning to run inference‑heavy models that still require periodic retraining. Persistent memory can bridge the gap between on‑site compute and centralized cloud resources by providing fast, locally durable checkpoints, thereby reducing bandwidth consumption and latency in model sync operations.

Integration with Next‑Gen Interconnects

Emerging PCIe 5.0 and CXL (Compute Express Link) standards promise higher throughput between CPUs and memory modules. Aligning persistent memory solutions with these interfaces will unlock even lower checkpoint latency, making the technology attractive for future AI accelerators and specialized training hardware.

Persistent Memory for AI Training Checkpointing Market Trends

Integration of Persistent Memory into Large‑Scale AI Training Pipelines

Persistent Memory for AI Training Checkpointing Market is witnessing a shift as AI developers replace traditional storage‑bound checkpointing with byte‑addressable, non‑volatile buffers. By allowing training frameworks to write checkpoint data directly to memory that survives power loss, the latency penalty associated with disk I/O disappears. This technical advantage shortens the recovery window for massive transformer models that require weeks of compute time, thereby improving overall time‑to‑insight for enterprises that rely on generative‑AI workloads.

Other Trends

Hardware Vendor Alliances Accelerating Adoption

Recent collaborations between leading silicon manufacturers and AI system integrators illustrate a concerted effort to embed persistent memory into next‑generation compute racks. Intel’s Optane DC line and Samsung’s Z‑Memory modules have become preferred building blocks for hyperscale operators seeking to tighten the loop between compute and storage. NVIDIA’s release of persistent‑memory‑aware APIs for its DGX portfolio demonstrates how software stacks are being tuned to exploit the new hardware interface. Cloud providers that integrate these solutions report lower per‑epoch storage costs and faster restart times after failure events, which translates into measurable savings on utility‑scale billing.

Economic Incentives Driving Data Center Investments

From a financial perspective, Persistent Memory for AI Training Checkpointing Market benefits from the reduction in total cost of ownership that stems from fewer write‑amplification cycles and diminished reliance on high‑capacity SSD arrays. Enterprises that adopt persistent memory cite a tighter capital‑expenditure profile because the same hardware can serve both high‑speed caching and durable checkpoint storage roles. As competition among cloud platforms intensifies, the ability to promise sub‑second fault recovery becomes a differentiator that can attract AI‑intensive workloads, encouraging further deployment of the technology across global data centers.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Persistent Memory for AI Training Checkpointing

Intel’s Optane DC Persistent Memory remains the de‑facto benchmark for large‑scale AI training platforms. By blending DRAM‑class latency with non‑volatile durability, Optane enables checkpoint writes without halting tensor computations, a capability that directly translates into higher utilisation of hyperscale GPU clusters. Samsung’s Z‑Memory, anchored in its 3‑D XPoint technology, is rapidly closing the performance gap and has secured strategic design wins in several cloud‑provider reference architectures. The duopoly creates a tiered market where most hyperscalers gravitate toward one of these two vendors, while the remaining ecosystem aligns its software stack to the corresponding APIs. The concentration of IP and economies of scale pressures smaller suppliers to differentiate through niche form‑factors, integrated controller logic, or bundled services such as automated recovery orchestration.

Beyond the two market leaders, a constellation of specialised manufacturers contributes depth and resilience to the supply chain. Micron’s QuantX line offers a cost‑effective alternative for mid‑range training workloads, whereas SK Hynix and Kioxia (formerly Toshiba Memory) exploit their NAND‑derived 3‑D architectures to target edge‑AI deployments. Western Digital’s SanDrive portfolio supplies high‑capacity modules for archival checkpointing, and Dell Technologies bundles persistent‑memory‑enabled servers as part of its AI‑ready portfolio. HPE and its Cray super‑computing division embed Optane‑compatible blades in exascale research installations, while IBM integrates persistent memory into its Power Systems to support hybrid cloud AI pipelines. NetApp and Cisco focus on software‑defined storage layers that expose persistent‑memory tiers through unified data services, extending the value proposition beyond raw performance.

List of Key Persistent Memory Companies Profiled

- Intel Corporation

- Samsung Electronics

- Micron Technology

- SK Hynix Inc.

- Kioxia Corporation

- Western Digital Corp.

- Dell Technologies

- Hewlett Packard Enterprise

- IBM

- NetApp

- Cisco Systems

- Cray (HPE Cray)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Intel Optane DC Persistent Memory

|

| By Application |

|

Large Language Model Training

|

| By End User |

|

Hyperscale Cloud Providers

|

| By Architecture |

|

Memory‑Centric Architecture

|

| By Deployment Model |

|

Public Cloud Services

|

Regional Analysis: Persistent Memory for AI Training Checkpointing Market

North America

Cloud providers and large enterprises are embedding persistent‑memory modules in AI‑focused servers, allowing checkpoint data to reside directly on the memory fabric. This reduces the I/O overhead that traditionally hamppered checkpoint‑restore cycles, making iterative model training more economical.

Universities and research institutes along the West Coast feed a pipeline of engineers who understand both hardware nuances and AI workload characteristics, accelerating the adoption curve for memory‑centric checkpointing solutions.

Data‑sovereignty rules in the United States encourage on‑premise storage of intermediate training artifacts, reinforcing demand for memory that can retain state without reliance on external cloud buckets.

Leading chipmakers are launching product families expressly marketed for checkpoint resilience, compelling system integrators to differentiate on latency and durability rather than raw throughput alone.

Europe

European AI labs are integrating persistent memory to address stringent data‑privacy mandates that limit cross‑border checkpoint storage. The region benefits from a strong consortium model where hardware manufacturers, cloud operators, and academic groups co‑develop reference architectures. While budgetary constraints are more pronounced than in North America, the emphasis on energy‑efficient compute is driving interest in memory solutions that curtail repeated training passes. Integration pilots in Germany and France illustrate how regulatory compliance can become a catalyst for technical innovation, positioning Europe as a nuanced but increasingly influential market for Persistent Memory for AI Training Checkpointing Market.

Asia‑Pacific

In the Asia‑Pacific, rapid expansion of AI startups is matched by a burgeoning demand for checkpointing mechanisms that can survive frequent power fluctuations in emerging data‑center hubs. Nations such as Singapore and Japan are investing heavily in national AI strategies that earmark funding for next‑generation memory technologies. The region’s heterogeneous manufacturing base enables swift prototyping, allowing local firms to tailor memory modules to specific model sizes. This agility, coupled with a cultural emphasis on rapid product cycles, makes Asia‑Pacific a laboratory for iterative improvements in checkpoint efficiency within Persistent Memory for AI Training Checkpointing Market.

South America

South American enterprises are cautiously exploring persistent memory as part of broader digitization initiatives aimed at reducing reliance on costly cloud egress fees. Brazil’s leading research consortia are conducting proof‑of‑concept deployments that demonstrate how on‑site checkpoint storage can lower operational expenses for large‑scale language model training. Although the market remains nascent, the combination of fiscal incentives for local hardware production and a growing pool of data‑science talent suggests a gradual but steady uptake of the technology over the next several years.

Middle East & Africa

The Middle East & Africa region is witnessing early‑stage interest driven by sovereign AI programs that prioritize data residency. UAE and South Africa are establishing pilot data‑centers where persistent memory is evaluated for its ability to safeguard checkpoint data against intermittent power supply issues common in some locales. Partnerships with global chip vendors supply the necessary hardware expertise, while regional universities contribute research on memory‑centric AI workflows. Though adoption is still limited, the strategic focus on resilient AI infrastructure positions this region as an emerging participant in Persistent Memory for AI Training Checkpointing Market.

Report Scope

This market research report provides a comprehensive analysis of the Persistent Memory for AI Training Checkpointing Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Persistent Memory for AI Training Checkpointing Market?

-> Persistent Memory for AI Training Checkpointing market size is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034

Which key companies operate in Persistent Memory for AI Training Checkpointing Market?

-> Key players include Intel (Optane DC), Samsung (Z‑Memory), Micron, NVIDIA, and SK Hynix, among others.

What are the key growth drivers?

-> Key growth drivers include the rapid expansion of generative‑AI model sizes, demand for fault‑tolerant training pipelines, and the need for cost‑effective high‑performance storage solutions.

Which region dominates the market?

-> North America leads the market due to early adoption in hyperscale data centers, while Asia‑Pacific is the fastest‑growing region.

What are the emerging trends?

-> Emerging trends include deeper integration of persistent memory APIs into AI frameworks, hybrid DRAM‑persistent memory architectures, and strategic collaborations between semiconductor vendors and cloud providers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...