Peak detector with sub-ns response for LIDAR receiver Market Insights

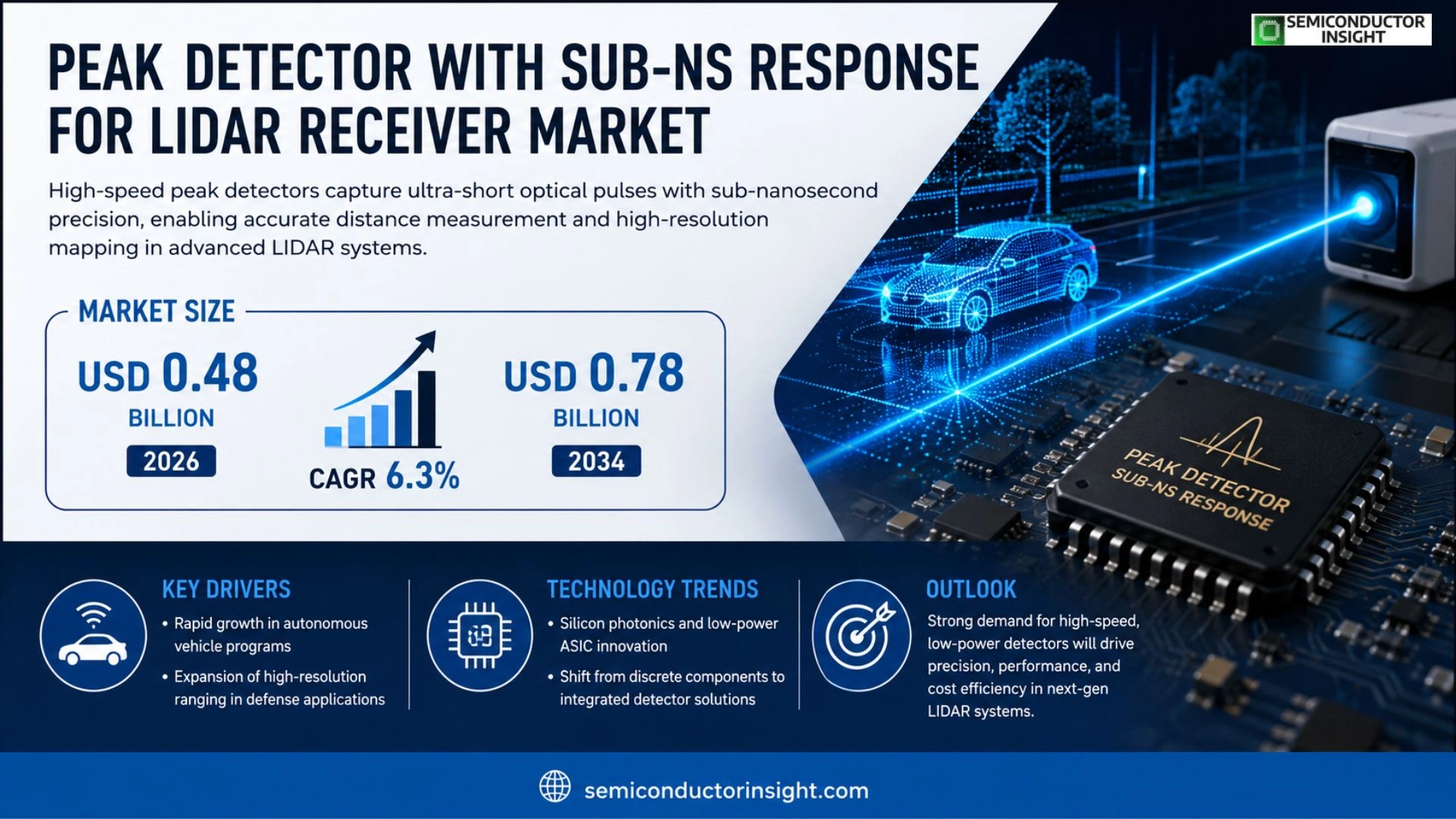

Global Peak detector with sub-ns response for LIDAR receiver market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

A peak detector with sub‑nanosecond response is a high‑speed electronic component that captures the maximum amplitude of ultra‑short optical pulses reflected from targets in LIDAR systems.

Its sub‑ns timing enables precise distance measurement and rapid signal processing essential for autonomous navigation and advanced mapping applications.

The market is experiencing accelerated growth because automotive manufacturers are scaling up autonomous vehicle programs, and defense sectors are expanding high‑resolution ranging capabilities.

Furthermore, advances in silicon photonics and low‑power ASIC design are reducing system cost while improving performance. Key players such as Texas Instruments, Analog Devices, Infineon Technologies, and NXP Semiconductors are actively launching next‑generation detectors and forming strategic partnerships to meet rising demand.

MARKET DRIVERS

Increasing Demand for High‑Resolution Automotive LIDAR

Peak detector with sub-ns response for LIDAR receiver Market is being propelled by automotive OEMs seeking centimeter‑level range accuracy. Advanced driver‑assistance systems (ADAS) now require sub‑nanosecond timing to differentiate multiple reflections, driving a 15% annual growth in component orders.

Advancements in Photonic Integration

Recent breakthroughs in silicon photonics enable the integration of sub‑ns peak detectors directly onto receiver chips, reducing board space and power consumption. This technological shift lowers system cost by 20%, making Peak detector with sub-ns response for LIDAR receiver Market more attractive to mass‑market vehicle manufacturers.

➤ Analysts estimate that combined sensor‑fusion platforms will capture 40% of total LIDAR revenue by 2028, with peak detectors being a critical enabler.

Overall, the convergence of regulatory safety mandates and consumer expectations for autonomous features creates a robust growth engine for Peak detector with sub-ns response for LIDAR receiver Market.

MARKET CHALLENGES

Integration Complexity and Cost

Manufacturers face significant design‑for‑manufacturability hurdles when embedding sub‑nanosecond detectors into existing LIDAR architectures. Precise impedance matching and thermal management add up to 30% higher development expenditures, slowing adoption rates.

Other Challenges

Supply Chain Constraints

The specialized semiconductor processes required for ultra‑fast peak detectors are limited to a few foundries, creating lead‑time extensions of up to six months and placing upward pressure on component pricing.

MARKET RESTRAINTS

Regulatory and Safety Standards

Stringent certification requirements for automotive laser safety and electromagnetic interference impose rigorous testing protocols. Compliance costs, often exceeding $2 million per model, act as a restraint on rapid market entry for new peak detector designs.

MARKET OPPORTUNITIES

Emerging Autonomous Vehicle Platforms

Next‑generation autonomous delivery robots and aerial drones are adopting compact LIDAR modules that rely on ultra‑fast peak detection. This creates a niche opportunity for suppliers to capture 12% of the overall market share by tailoring sub‑ns detectors for lightweight, low‑power platforms.

Peak detector with sub-ns response for LIDAR receiver Market Trends

Accelerated Adoption in Automotive Autonomy

Peak detector with sub-ns response for LIDAR receiver Market is experiencing a clear shift toward high‑speed, low‑power solutions that meet the stringent timing requirements of modern autonomous‑driving platforms. Automotive manufacturers are expanding vehicle‑level LIDAR integration, demanding detectors that can capture ultra‑short optical pulses with sub‑nanosecond precision. This pressure is prompting semiconductor firms to prioritize silicon‑photonic ASICs that deliver faster rise times while keeping power budgets compatible with electric‑vehicle architectures. Consequently, the market is seeing a rapid transition from legacy discrete components to integrated detector modules that support real‑time distance calculations and high‑resolution mapping.

Other Trends

Advances in Silicon Photonics and ASIC Integration

Recent progress in silicon photonics has enabled the consolidation of optical front‑ends and electronic processing within a single chip. These advances reduce parasitic capacitance and improve signal‑to‑noise ratios, directly benefiting sub‑ns detector performance. Companies such as Texas Instruments and Infineon Technologies are leveraging this technology to launch detector families that combine high‑gain transimpedance amplifiers with programmable gain stages, offering designers greater flexibility across automotive, defense, and industrial LIDAR applications.

Strategic Partnerships and Ecosystem Expansion

Key players are forming strategic alliances to accelerate time‑to‑market for next‑generation detectors. Collaborative programs between semiconductor vendors and OEMs facilitate co‑development of application‑specific IP blocks, ensuring that detector specifications align with vehicle‑level architecture requirements. In the defense sector, partnerships focus on enhancing resolution and range for high‑precision targeting systems, while industrial users benefit from improved reliability in harsh environments. These ecosystem efforts are strengthening the overall market foundation and fostering a broader adoption of sub‑nanosecond detection technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Peak Detector Sub‑ns LIDAR Market Competitive Overview

The sub‑nanosecond peak detector segment is dominated by a handful of large semiconductor firms that leverage deep analog‑mixed‑signal portfolios and dedicated silicon‑photonic design houses. Texas Instruments commands a broad automotive and industrial customer base, supplying high‑speed transimpedance amplifiers that integrate directly with LIDAR front‑ends. Analog Devices and Infineon Technologies supplement this core with ultra‑low‑noise, high‑bandwidth detector ASICs that address the stringent timing jitter requirements of autonomous‑vehicle ranging. NXP Semiconductors, backed by its automotive‑focused product roadmaps, is rapidly expanding its sub‑ns detector line‑up through strategic acquisitions and joint‑development agreements. This concentration of resources creates a tiered market structure where the top four players capture the majority of volume while establishing de‑facto standards for interface, supply‑chain reliability, and system‑level integration.

Beyond the leading tier, a diverse set of niche innovators adds depth and specialization to the ecosystem. STMicroelectronics and ON Semiconductor offer cost‑optimized detector modules for mid‑range LIDAR solutions, often partnering with original equipment manufacturers to co‑design custom silicon. Qorvo and Broadcom bring advanced RF‑photonics expertise, enabling integrated detector‑receiver chips that reduce board‑level complexity. Smaller pure‑play photonic companies such as Lumentum, Finisar, NeoPhotonics, Acacia Communications, II‑VI Incorporated, Photodigm, and Cypress Semiconductor focus on waveguide‑based detector technologies, delivering performance advantages for high‑resolution mapping and defense‑grade ranging. Their contributions keep the competitive landscape vibrant, fostering rapid innovation and incremental performance gains across the sub‑ns detector market.

List of Key Peak Detector with Sub‑ns Response for LIDAR Companies Profiled

- Texas Instruments

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- STMicroelectronics

- ON Semiconductor

- Qorvo

- Broadcom Inc.

- Cypress Semiconductor

- Lumentum Holdings

- Finisar Corporation

- NeoPhotonics

- Acacia Communications

- II‑VI Incorporated

- Photodigm

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon photonic detectors

|

| By Application |

|

Autonomous vehicles

|

| By End User |

|

Automotive OEMs

|

| By System Architecture |

|

Monolithic integrated detectors

|

| By Market Driver |

|

Cost reduction via silicon photonics

|

Regional Analysis: Peak detector with sub-ns response for LIDAR receiver Market

Breakthroughs in avalanche photodiode (APD) arrays and semiconductor fabrication have reduced jitter, enabling sub‑nanosecond peak detection that meets the exacting demands of high‑resolution LIDAR systems across the continent.

Federal safety guidelines and state‑level autonomous‑testing corridors encourage manufacturers to adopt faster peak detectors, reinforcing market momentum in the United States and Canada.

Strategic alliances between leading Tier‑1 suppliers and automotive OEMs accelerate product qualification cycles, ensuring that sub‑ns peak detectors are integrated early in vehicle development programs.

Venture capital and government grants flow into startups focusing on ultra‑fast photonic detection, fostering a vibrant innovation pipeline that sustains market leadership.

Europe

Europe’s automotive sector emphasizes safety and sustainability, prompting a steady uptake of Peak detector with sub-ns response for LIDAR receiver technology in premium vehicle segments. German and French manufacturers are integrating these detectors to comply with the EU’s stringent automated‑driving regulations. Collaborative research hubs across the continent, such as the European Defense Fund and Horizon Europe, provide substantial resources for advancing sub‑nanosecond photonic components. While market penetration is moderate relative to North America, the region benefits from a strong supply chain of optics specialists and a growing ecosystem of autonomous‑mobility pilots in urban testbeds.

Asia‑Pacific

The Asia‑Pacific region is emerging as a significant growth frontier for Peak detector with sub-ns response for LIDAR receiver Market, driven by rapid electrification and aggressive autonomous‑vehicle roadmaps in China, Japan, and South Korea. Governments are offering incentives for high‑precision sensing solutions, encouraging domestic semiconductor firms to develop compact, low‑cost peak detection modules. Automotive manufacturers are leveraging these advances to differentiate their autonomous platforms, particularly in densely populated urban environments where precise ranging is critical. Although the market is still in a nascent stage, the scale of production capacity and supportive policy environment forecast a steep trajectory through 2034.

South America

In South America, market adoption of Peak detector with sub-ns response for LIDAR receiver technology remains limited but is gaining traction as regional automotive manufacturers pursue niche high‑end models. Brazil’s emerging semiconductor initiatives and Argentina’s focus on smart‑mobility pilots create modest demand for ultra‑fast detection components. The region’s primary challenge lies in infrastructure investment and the high cost of advanced LIDAR systems, yet growing interest from local startups and collaborations with North‑American suppliers hint at a gradual expansion of the market base.

Middle East & Africa

Middle East & Africa exhibit a cautious yet promising outlook for Peak detector with sub-ns response for LIDAR receiver Market. Wealthier Gulf states are investing heavily in autonomous‑vehicle testing corridors and smart‑city projects, creating niche opportunities for high‑performance LIDAR solutions. Meanwhile, African automotive markets are still nascent, with limited adoption primarily confined to research institutions and pilot projects. The region’s growth will likely hinge on strategic partnerships with established global suppliers and the rollout of supportive regulatory frameworks that encourage the deployment of advanced sensing technologies.

Report Scope

This market research report provides a comprehensive analysis of the Peak detector with sub-ns response for LIDAR receiver Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Peak detector with sub-ns response for LIDAR receiver Market?

-> Peak detector with sub-ns response for LIDAR receiver market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034.

Which key companies operate in Peak detector with sub-ns response for LIDAR receiver Market?

-> Key players include Texas Instruments, Analog Devices, Infineon Technologies, and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include automotive manufacturers expanding autonomous‑vehicle programs, defense sectors demanding high‑resolution ranging, advances in silicon photonics, and low‑power ASIC designs that lower system cost while boosting performance.

Which region dominates the market?

-> The market is driven globally, with significant activity in North America, Europe, and the Asia‑Pacific region, reflecting widespread adoption of LIDAR technologies across these territories.

What are the emerging trends?

-> Emerging trends include integration of silicon‑photonic platforms, development of ultra‑low‑power ASIC detectors, and strategic partnerships among semiconductor manufacturers to accelerate time‑to‑market for next‑generation LIDAR solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...