MARKET INSIGHTS

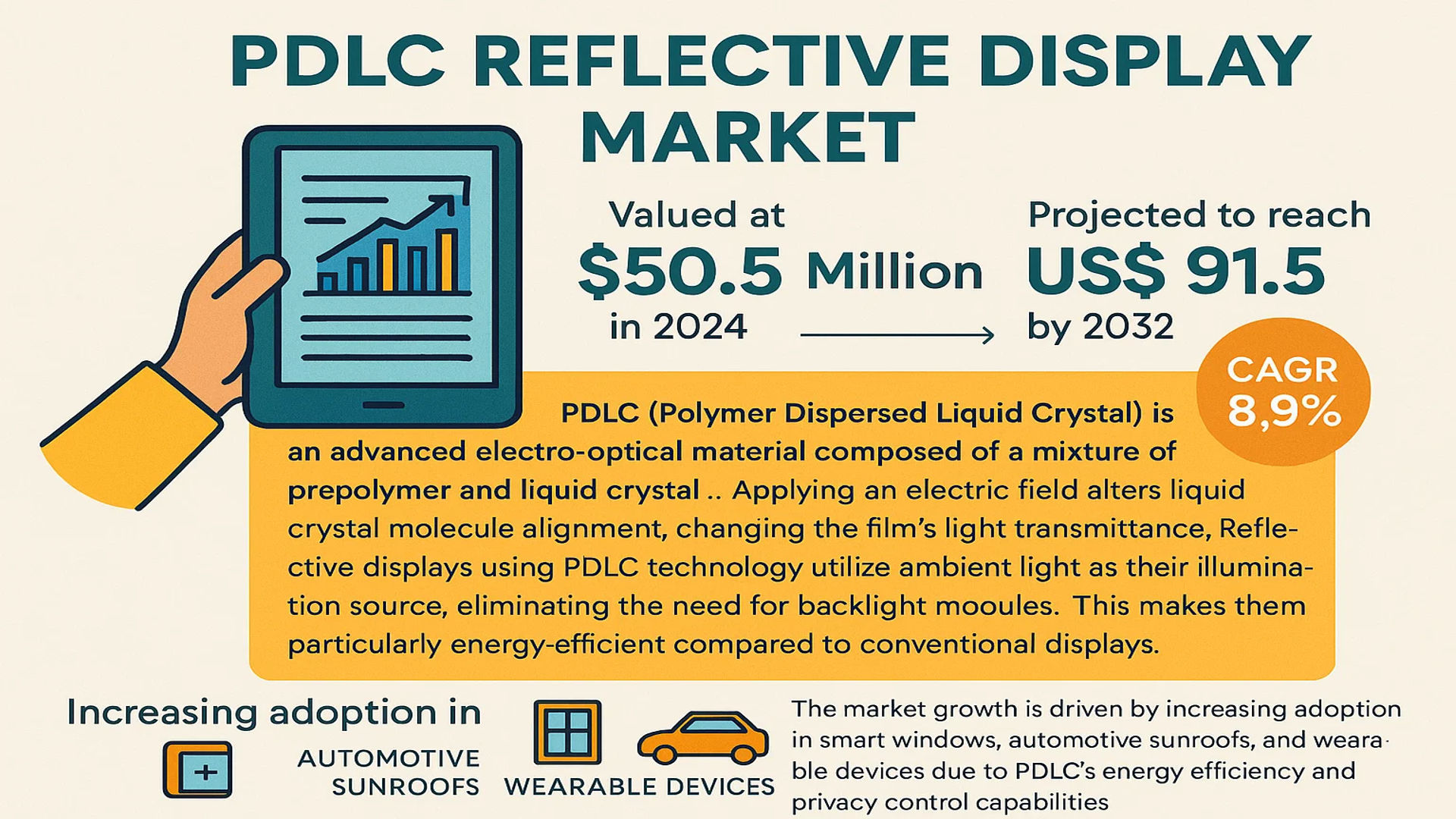

The global PDLC Reflective Display Market was valued at 50.5 million in 2024 and is projected to reach US$ 91.5 million by 2032, at a CAGR of 8.9% during the forecast period.

PDLC (Polymer Dispersed Liquid Crystal) is an advanced electro-optical material composed of a mixture of prepolymer and liquid crystal. When exposed to specific conditions, these components phase-separate to form a film with unique optoelectronic properties. The technology enables electrically controlled light modulation – applying an electric field alters liquid crystal molecule alignment, changing the film’s light transmittance. Reflective displays using PDLC technology utilize ambient light as their illumination source, eliminating the need for backlight modules. This makes them particularly energy-efficient compared to conventional displays.

The market growth is driven by increasing adoption in smart windows, automotive sunroofs, and wearable devices due to PDLC’s energy efficiency and privacy control capabilities. Technological advancements in flexible and transparent displays are creating new application opportunities. Major players like BOE Technology, Tianma Microelectronics, and Polytronix are investing heavily in R&D to improve switching speeds and optical performance. The automotive sector is emerging as a key growth area, with PDLC films being increasingly used in sunroofs and windows for privacy and thermal management applications.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Energy-Efficient Displays to Propel PDLC Market Growth

The global push toward energy efficiency is accelerating the adoption of PDLC reflective displays as they consume significantly less power than conventional LCD screens. Unlike traditional displays that require continuous backlighting, PDLC technology relies on ambient light reflection, reducing energy consumption by up to 60% in typical usage scenarios. This advantage is particularly compelling for battery-powered devices like smartwatches and IoT displays, where power efficiency directly impacts product usability. Furthermore, increasing environmental regulations across North America and Europe are mandating lower power consumption in consumer electronics, creating a strong market pull for PDLC solutions.

Automotive Sector Adoption Driving Market Expansion

The automotive industry’s shift toward smart glass applications is creating substantial demand for PDLC reflective displays. These technologies are being integrated into sunroofs, side windows, and rear-view mirrors to provide dynamic light control and heads-up display functionality. Leading automotive manufacturers have begun incorporating PDLC films in over 15% of premium vehicle models as standard equipment, with the penetration rate expected to double by 2028. The technology’s ability to reduce cabin temperature by up to 12°F through smart light modulation has become a key selling point in warmer climates.

Another significant driver is the emergence of augmented reality applications in wearable devices. PDLC reflective displays are increasingly favored for AR glasses and smart helmets due to their sunlight readability and low power requirements.

➤ For instance, recent product launches in the defense sector feature PDLC-based helmet displays that maintain visibility in direct sunlight while operating for 72+ hours on a single charge.

Furthermore, expanding 5G network infrastructure is enabling new use cases for IoT displays, where PDLC technology’s combination of visibility and energy efficiency provides competitive advantages.

MARKET RESTRAINTS

High Production Costs Limiting Mass Market Adoption

While PDLC technology offers numerous advantages, its manufacturing costs remain approximately 30-40% higher than conventional display technologies. The complex fabrication process involving precise liquid crystal alignment and polymer matrix formation requires specialized equipment with stringent environmental controls. These factors contribute to significantly higher unit costs compared to standard LCD panels, making PDLC displays economically viable primarily in premium product segments.

Color rendering limitations present another challenge for market expansion. Current PDLC reflective displays typically achieve only 60-70% of the color gamut offered by emissive displays, restricting their use in applications requiring vibrant color reproduction. This technical constraint has slowed adoption in consumer electronics where display quality is a primary purchase consideration.

Durability concerns under extreme environmental conditions also pose adoption barriers. Exposure to temperatures beyond 85°C can degrade PDLC film performance, limiting applications in industrial and automotive settings without additional protective measures that further increase costs.

MARKET OPPORTUNITIES

Emerging Applications in Smart Architecture to Unlock New Growth Potential

The construction industry’s accelerating adoption of smart glass solutions represents a substantial growth opportunity for PDLC reflective displays. Building-integrated photovoltaics combined with PDLC films are being tested in commercial skyscrapers to optimize both energy generation and interior climate control. Early pilot projects have demonstrated 25-35% reductions in HVAC energy consumption through dynamic sunlight modulation, creating strong incentives for broader implementation.

Medical applications are emerging as another high-value segment. The healthcare sector is adopting PDLC-based surgical displays that maintain visibility under variable lighting conditions in operating rooms. These medical-grade solutions command premium pricing with profit margins exceeding 45%, attracting significant R&D investment from display manufacturers.

Advancements in flexible PDLC films are opening doors for innovative product designs. Recent breakthroughs in roll-to-roll manufacturing processes now enable production of bendable reflective displays suitable for wearable devices and foldable electronics. These developments align perfectly with the consumer electronics industry’s push toward more ergonomic and versatile form factors.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impacting Production Stability

The PDLC reflective display market faces significant challenges in securing stable supplies of critical raw materials. Several key components, including specialized liquid crystal mixtures and conductive polymers, are produced by only a handful of suppliers worldwide. Recent geopolitical tensions have exposed vulnerabilities in this concentrated supply chain, with lead times for essential materials extending from 8-10 weeks to over 6 months in some cases.

Technical limitations in switching speed continue to hinder adoption in certain applications. Current PDLC films typically require 50-100ms for full opacity transition, making them unsuitable for video-rate content display without advanced compensation techniques. While lab prototypes have achieved sub-20ms switching, these solutions have yet to prove commercially viable at scale.

Standardization gaps across the industry present another obstacle to market growth. The lack of unified specifications for optical performance parameters and interface protocols has led to fragmentation, increasing development costs for OEMs integrating PDLC displays into their products. Industry alliances are working to address this challenge, but progress has been slow due to competing technological approaches among major players.

Rising Demand for Energy-Efficient Display Technologies to Drive PDLC Reflective Display Market Growth

The global PDLC (Polymer Dispersed Liquid Crystal) reflective display market is experiencing significant growth, projected to expand from $50.5 million in 2024 to $91.5 million by 2032 at a CAGR of 8.9%. This surge is primarily driven by increasing demand for energy-efficient display solutions across various industries. Unlike traditional LCDs that require constant backlighting, PDLC reflective displays utilize ambient light, reducing power consumption by up to 80% in certain applications. The technology’s ability to maintain visibility even in bright sunlight makes it particularly valuable for outdoor devices and automotive applications, where conventional displays often struggle with glare and readability issues.

Other Trends

Expansion in Wearable Technology Applications

The wearable device sector is emerging as a key growth area for PDLC reflective displays, with smartwatches and fitness trackers increasingly adopting this technology. Manufacturers are drawn to its low power requirements, which can extend battery life by 30-50% compared to conventional displays. Recent advancements in flexible PDLC films have further enabled the development of curved and foldable displays for next-generation wearables. This trend aligns with the broader market shift toward always-on displays in consumer electronics, where visibility under all lighting conditions is becoming a standard expectation.

Automotive Sector Adoption Creating New Opportunities

Automotive manufacturers are progressively integrating PDLC reflective displays into dashboards, heads-up displays (HUDs), and smart windows. The technology’s sunlight readability and energy efficiency make it ideal for electric vehicles where power conservation is critical. Leading manufacturers are developing hybrid systems that combine reflective and emissive display technologies to optimize visibility across different lighting conditions. The automotive segment is expected to account for over 25% of the market by 2030, driven by the increasing electrification of vehicles and demand for advanced driver information systems.

Technological Innovations Enhancing Market Potential

Recent breakthroughs in material science are significantly improving PDLC display performance. New polymer formulations have increased contrast ratios to over 15:1 while reducing switching voltages below 30V, making the technology more versatile for portable applications. Manufacturers are also developing color-reflective PDLC displays, addressing one of the technology’s traditional limitations. These advancements are opening new applications in consumer electronics, where vibrant color reproduction was previously a barrier to adoption, while maintaining the technology’s signature low power consumption.

Geographic Market Developments

Asia-Pacific Emerging as Production Hub

With China projected to reach a market size of $XX million by 2032, the Asia-Pacific region is establishing itself as both a major consumer and manufacturer of PDLC reflective displays. This growth is supported by substantial investments in display manufacturing infrastructure and the presence of key players like BOE Technology and Tianma Microelectronics. Meanwhile, North America maintains strong demand from technology and automotive sectors, with the U.S. market estimated at $XX million in 2024. European markets are showing particular interest in architectural applications, where PDLC smart glass is gaining traction for energy-efficient building solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Leverage Innovation to Expand Their PDLC Reflective Display Solutions

The global PDLC (Polymer Dispersed Liquid Crystal) reflective display market exhibits a competitive landscape dominated by established players with strong technological expertise and regional presence. BOE Technology emerges as a frontrunner in this space, holding a significant market share as of 2024, owing to its robust R&D capabilities and extensive manufacturing footprint, particularly in the Asia-Pacific region.

Tianma Microelectronics and Sharp Corporation maintain strong positions in the sector, benefitting from their legacy in display technologies and diversified product portfolios. These companies continue to invest in enhancing the energy efficiency and optical performance of their PDLC solutions, which is critical for applications in automotive and wearable devices.

Strategic collaborations are increasingly shaping the competitive dynamics, with companies like Research Frontiers and Polytronix forming alliances to co-develop next-generation smart glass solutions. Such partnerships enable technology transfer and help accelerate product commercialization in high-growth verticals.

Meanwhile, emerging players such as Gauzy and Prodisplay are carving out niche positions through specialized offerings that target architectural and transportation applications. Their focus on customization and rapid prototyping gives them an edge in serving specific customer requirements.

List of Key PDLC Reflective Display Companies

- BOE Technology (China)

- Tianma Microelectronics (China)

- Polytronix (U.S.)

- Gauzy (Israel)

- Prodisplay (U.K.)

- Beneq (Finland)

- Research Frontiers/Smart Glass International (U.S.)

- DMDisplay (China)

- Sharp Corporation (Japan)

- Giantplus Technology (Taiwan)

- Ricoh Company (Japan)

- Zhonghe Technology (Changzhou) (China)

The competitive intensity in the PDLC reflective display space continues to escalate as companies diversify their application focus beyond traditional smart windows to include emerging sectors like automotive HUDs and wearable displays. This evolution is compelling market participants to strengthen their IP portfolios and enhance production efficiencies to maintain profitability amid pricing pressures.

Segment Analysis:

By Type

Passive PDLC Segment Dominates the Market Due to Cost-Effectiveness and Energy Efficiency

The market is segmented based on type into:

- Passive PDLC

- Characteristics: No external power required for operation, relies on ambient light reflection

- Active PDLC

By Application

Automotive Field Segment Leads Due to Growing Adoption in Sunroofs and Window Displays

The market is segmented based on application into:

- Wearable Device Field

- Automotive Field

- Others

By Technology

Reflective Technology Segment Dominates Due to Superior Visibility in Bright Conditions

The market is segmented based on technology into:

- Reflective

- Transflective

- Others

By Component

Liquid Crystal Layer Segment Dominates as Core Functional Component

The market is segmented based on component into:

- Liquid Crystal Layer

- Polymer Matrix

- Conductive Substrates

- Others

Regional Analysis: PDLC Reflective Display Market

Asia-Pacific

The Asia-Pacific region dominates the PDLC reflective display market, driven by rapid technological advancements, strong manufacturing capabilities, and increasing demand for energy-efficient display solutions. China leads the market with companies like BOE Technology and Tianma Microelectronics spearheading innovation. The country’s vast electronics manufacturing ecosystem and government support for advanced display technologies contribute to its leadership position. Japan and South Korea also hold significant shares due to established players like Sharp Corporation and Ricoh Company investing heavily in reflective display R&D. The region benefits from high adoption in consumer electronics, automotive HUDs (Heads-Up Displays), and wearable devices, with growing applications in smart windows and augmented reality.

North America

North America represents the second-largest market for PDLC reflective displays, characterized by strong R&D investments and early adoption of emerging technologies. The U.S. accounts for over 70% of the regional market share, with key players such as Research Frontiers and Polytronix driving innovation. The automotive sector is a major growth driver, with reflective displays being increasingly integrated into vehicle smart windows and instrument clusters. Furthermore, the region’s focus on energy-efficient building solutions has accelerated demand for PDLC-based smart glass in architectural applications. However, higher costs compared to conventional displays and competition from OLED technologies present challenges.

Europe

Europe maintains a technologically mature but steadily growing PDLC reflective display market, with Germany, the UK, and France leading adoption. The region benefits from stringent energy efficiency regulations that favor reflective display technologies in both consumer electronics and architectural applications. Companies like Gauzy and Smart Glass International are expanding their product portfolios to cater to the automotive and smart home sectors. Europe’s strong focus on sustainability aligns well with the energy-saving benefits of PDLC displays. However, market growth is somewhat restrained by the high cost of advanced PDLC solutions and competition from established display technologies.

Middle East & Africa

The MEA region shows emerging potential for PDLC reflective displays, particularly in smart building applications across Gulf Cooperation Council (GCC) countries. The extreme sunlight conditions in the region make reflective displays particularly suitable for outdoor and architectural applications. Countries like UAE and Saudi Arabia are driving demand through smart city initiatives and infrastructure projects. However, the market faces challenges including limited local manufacturing capabilities, reliance on imports, and price sensitivity. Despite these barriers, the region’s focus on futuristic urban development creates long-term growth opportunities for PDLC display solutions.

South America

South America represents the smallest but growing market for PDLC reflective displays, with Brazil accounting for the majority of regional demand. The market is primarily driven by automotive and architectural applications, though adoption remains limited by economic volatility and infrastructure challenges. While the region lacks significant local manufacturing, international players are beginning to establish distribution channels to serve the emerging demand for energy-efficient display solutions. The market shows promise for gradual growth as urbanization increases and building efficiency standards evolve across major economies in the region.

Report Scope

This market research report provides a comprehensive analysis of the global PDLC Reflective Display market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global PDLC Reflective Display market was valued at USD 50.5 million in 2024 and is projected to reach USD 91.5 million by 2032, growing at a CAGR of 8.9%.

- Segmentation Analysis: Detailed breakdown by type (Passive, Active), application (Wearable Device Field, Automotive Field, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants including BOE Technology, Tianma Microelectronics, Polytronix, Gauzy, and Sharp Corporation, covering their product offerings, market share, and strategic developments.

- Technology Trends: Assessment of emerging PDLC technologies, material innovations, and integration with smart devices and automotive applications.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand for energy-efficient displays, growth in wearable devices, alongside challenges like high production costs.

- Stakeholder Analysis: Strategic insights for display manufacturers, component suppliers, investors, and policymakers regarding market opportunities.

The research employs both primary and secondary methodologies, including interviews with industry experts and analysis of verified market data to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global PDLC Reflective Display Market?

->PDLC Reflective Display Market was valued at 50.5 million in 2024 and is projected to reach US$ 91.5 million by 2032, at a CAGR of 8.9% during the forecast period

Which key companies operate in Global PDLC Reflective Display Market?

-> Key players include BOE Technology, Tianma Microelectronics, Polytronix, Gauzy, Prodisplay, Beneq, and Sharp Corporation, among others.

What are the key growth drivers?

-> Growth is driven by increasing demand for energy-efficient displays, adoption in wearable devices, and automotive smart glass applications.

Which region dominates the market?

-> Asia-Pacific leads in both production and consumption, with China being a major manufacturing hub.

What are the emerging trends?

-> Emerging trends include integration with IoT devices, development of flexible PDLC displays, and applications in smart windows.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...