PCIe SSD for AI Market Insights

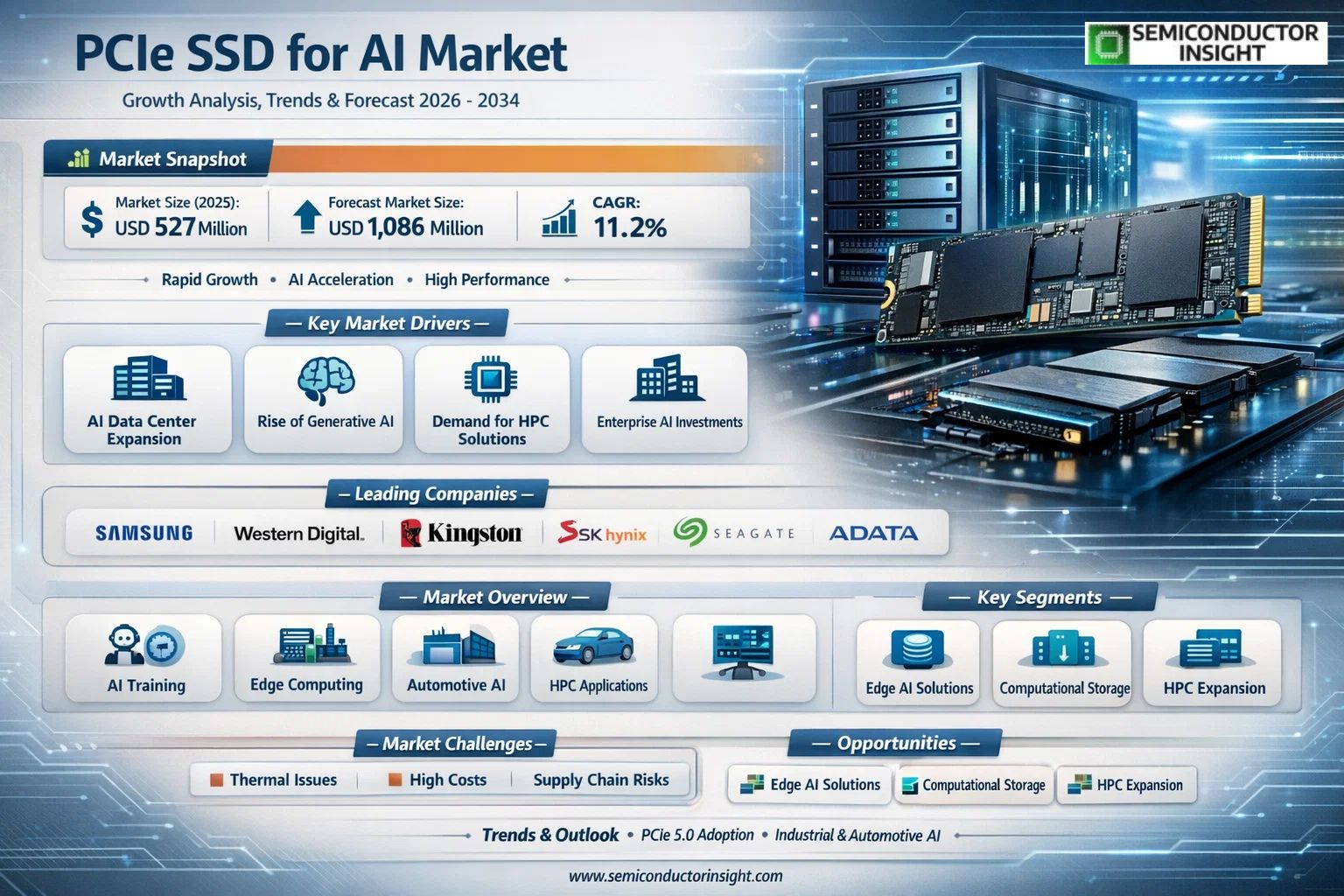

Global PCIe SSD for AI market size was valued at USD 527 million in 2025. The market is projected to grow from USD 585 million in 2026 to USD 1,086 million by 2034, exhibiting a CAGR of 11.2% during the forecast period.

PCIe SSD for AI are specialized solid-state drives designed to meet the high-performance requirements of artificial intelligence (AI) and machine learning (ML) workloads in data centers and enterprise environments. Unlike standard SSDs, these drives are engineered to handle the immense data throughput, low latency, and high IOPS (Input/Output Operations Per Second) demands of AI applications such as deep learning, neural network training, and real-time data analytics. The product landscape spans across key interface generations, including PCIe 4.0 SSDs, PCIe 5.0 SSDs, and other advanced variants, each tailored to address evolving computational demands across sectors.

The market is experiencing robust growth driven by the accelerating adoption of AI infrastructure across data centers, the rapid expansion of high-performance computing (HPC) environments, and growing enterprise investments in AI-powered workloads. Furthermore, the transition from PCIe 4.0 to PCIe 5.0 architectures is significantly enhancing data transfer speeds and bandwidth capabilities, making these SSDs indispensable in AI deployment pipelines. Key manufacturers shaping this competitive landscape include Samsung, Western Digital, Kingston, SK Hynix, Seagate Technology, ADATA, Micron Technology, Gigabyte, KIOXIA, and Intel, among others, all of whom continue to expand their AI-optimized storage portfolios to capture growing global demand.

MARKET DRIVERS

Surging Demand for High-Speed Storage in AI Training and Inference Workloads

The rapid expansion of artificial intelligence across industries has created an unprecedented need for storage solutions capable of delivering extreme throughput and minimal latency. PCIe SSD for AI Market growth is being propelled by the intensive data ingestion requirements of large language models, computer vision systems, and deep learning pipelines. Unlike traditional SATA-based drives, PCIe Gen 4 and Gen 5 SSDs offer sequential read speeds exceeding 12,000 MB/s, enabling AI accelerators and GPUs to access training datasets without bottlenecking compute performance. As model sizes continue to scale into the hundreds of billions of parameters, enterprise data centers and hyperscale cloud providers are prioritizing PCIe NVMe SSDs as a foundational infrastructure component.

Proliferation of Generative AI Applications Accelerating Enterprise Storage Upgrades

The mainstream adoption of generative AI tools across sectors including healthcare diagnostics, financial modeling, autonomous systems, and content generation is driving organizations to upgrade their storage infrastructure at scale. PCIe SSDs are uniquely positioned to support the AI market’s demand for low-latency random read performance, which is critical during inference stages where real-time responsiveness is non-negotiable. Enterprises deploying on-premises AI clusters are increasingly standardizing on PCIe NVMe SSDs over HDDs or legacy flash storage, citing a measurable reduction in data pipeline stall rates and improved GPU utilization efficiency. This migration cycle is expected to sustain robust hardware procurement activity through the latter half of this decade.

➤ As generative AI model complexity increases and real-time inference demands grow, PCIe Gen 5 NVMe SSDs are emerging as the de facto storage standard for next-generation AI infrastructure, replacing legacy storage tiers in both hyperscale and enterprise environments.

Government-led AI initiatives and national digital transformation programs across North America, Europe, and the Asia-Pacific region are further amplifying infrastructure investment. Public sector funding directed toward AI research supercomputers and sovereign cloud programs is creating structured procurement pipelines for high-performance PCIe SSD solutions for AI workloads. This institutional demand complements private sector spending and ensures a diversified, resilient growth base for storage hardware vendors operating in the AI segment.

MARKET CHALLENGES

Thermal Management and Power Consumption Constraints in High-Density AI Deployments

One of the most pressing technical challenges confronting PCIe SSD for AI market is the management of heat dissipation under sustained, high-throughput workloads. PCIe Gen 5 SSDs, while delivering superior bandwidth, generate substantially higher thermal output compared to their Gen 4 predecessors. In high-density rack deployments common to AI data centers, inadequate thermal regulation can trigger dynamic throttling mechanisms within the SSD controller, degrading sequential performance by a significant margin during extended AI training runs. Vendors are responding with advanced thermal interface materials, active cooling solutions, and controller-level power state management, but these additions increase total cost of ownership and introduce additional design complexity for system integrators.

Other Challenges

Supply Chain Vulnerabilities and NAND Flash Pricing Volatility

PCIe SSD AI market remains exposed to cyclical fluctuations in NAND flash memory pricing, which directly impact SSD bill-of-materials costs and vendor margin stability. Concentrated NAND production among a limited number of semiconductor manufacturers creates geographic and geopolitical supply risk. During periods of oversupply, aggressive pricing can compress vendor profitability, while undersupply conditions delay hardware procurement cycles for AI infrastructure projects and cloud capacity expansions.

Interoperability and Ecosystem Fragmentation Across AI Platforms

The diversity of AI hardware platforms , spanning GPU clusters, custom AI ASICs, and heterogeneous computing architectures , creates interoperability challenges for PCIe SSD vendors. Optimizing firmware, queue depth configurations, and NVMe protocol implementations across varied host environments requires sustained engineering investment. Smaller vendors without dedicated AI-segment validation programs risk compatibility gaps that can limit design wins in competitive enterprise and hyperscale procurement processes.

MARKET RESTRAINTS

High Acquisition Costs Limiting Adoption Among Mid-Market and Emerging Economy Enterprises

Despite clear performance advantages, the premium price positioning of enterprise-grade PCIe SSDs for AI applications remains a meaningful adoption barrier for mid-market organizations and enterprises operating in cost-sensitive emerging economies. PCIe Gen 5 NVMe SSDs command a substantial price premium over Gen 4 alternatives and significantly exceed the per-gigabyte cost of high-capacity HDD storage. For AI workloads involving large-scale cold data storage or archival training datasets, this cost differential makes full PCIe SSD deployment economically impractical, leading many organizations to adopt tiered storage architectures that partially dilute the performance benefits available to AI compute infrastructure.

Limited PCIe Gen 5 Platform Readiness Slowing Full-Ecosystem Adoption

The full performance potential of next-generation PCIe SSDs in the AI market is contingent on host platform compatibility, including motherboard chipsets, CPU PCIe lane availability, and system firmware maturity. As of current market conditions, PCIe Gen 5 SSD adoption is constrained by the relatively limited installed base of Gen 5-compatible server platforms, particularly among enterprises operating hardware refresh cycles of five years or longer. This platform readiness gap creates a temporal restraint on addressable market expansion, with widespread Gen 5 deployment expected to accelerate only as next-generation server CPU platforms achieve broader market penetration over the coming years.

MARKET OPPORTUNITIES

Expansion of Edge AI Infrastructure Creating New Demand Vectors for Compact PCIe SSD Solutions

The decentralization of AI inference from centralized cloud data centers toward edge computing environments represents a significant emerging opportunity for PCIe SSD for AI market. Edge AI deployments in industrial automation, smart city infrastructure, autonomous vehicle platforms, and retail analytics require compact, ruggedized, high-performance storage capable of sustaining low-latency data access under variable environmental conditions. M.2 and U.2 form factor PCIe NVMe SSDs are well-suited to these edge AI use cases, and vendors that develop purpose-built, thermally optimized edge AI storage solutions stand to capture meaningful incremental revenue as enterprise edge infrastructure investment accelerates globally.

Computational Storage and Near-Data Processing as a Differentiating Growth Frontier

Computational storage devices (CSDs) , a class of intelligent PCIe SSDs integrating embedded processing capabilities , are gaining traction as a transformative technology for AI data preprocessing workloads. By performing data filtering, compression, encryption, and feature extraction directly within the storage device, CSDs reduce the volume of data transferred across the PCIe bus, alleviating memory bandwidth constraints that limit AI accelerator utilization. Early enterprise deployments have demonstrated measurable reductions in data movement overhead for AI training pipelines, and leading storage vendors are actively developing CSD product lines targeted at hyperscale and AI-native cloud operators. This segment represents a high-value, differentiated opportunity within the broader PCIe SSD AI market that rewards early movers with strong IP positioning and long-term customer lock-in.

Trends

Rising Demand for High-Performance Storage in AI Workloads Drives PCIe SSD for AI market

PCIe SSD for AI market is experiencing robust momentum as enterprises and data centers accelerate their adoption of artificial intelligence and machine learning technologies. Unlike conventional storage solutions, PCIe SSDs engineered for AI environments are purpose-built to handle the extraordinary data throughput, ultra-low latency, and high IOPS demands characteristic of deep learning, neural network training, and real-time analytics workloads. As AI model complexity continues to grow, organizations are increasingly prioritizing storage infrastructure capable of sustaining continuous, high-bandwidth data pipelines, making PCIe SSD for AI a foundational component of modern AI computing architectures.

Other Trends

Transition from PCIe 4.0 to PCIe 5.0 Technology

A significant trend reshaping PCIe SSD for AI market is the accelerating transition from PCIe 4.0 to PCIe 5.0 interface technology. PCIe 5.0 SSDs deliver nearly double the sequential read and write speeds compared to their PCIe 4.0 counterparts, enabling AI systems to process and transfer massive datasets with greater efficiency. Data centers running large-scale AI training clusters are among the earliest adopters of PCIe 5.0 drives, as the performance gains directly translate to reduced model training cycles and improved throughput across distributed computing nodes. Leading manufacturers including Samsung, SK Hynix, Micron Technology, and KIOXIA are actively expanding their PCIe 5.0 SSD portfolios to address this surging demand.

Expansion Across High Performance Computing and Industrial Applications

PCIe SSD for AI market is witnessing growing adoption beyond traditional data center environments, with High Performance Computing (HPC), industrial automation, and automotive sectors emerging as key application areas. In HPC environments, PCIe SSDs are being deployed to support compute-intensive simulations and AI-driven analytics at scale. The industrial sector is leveraging these drives for real-time machine vision and edge AI processing, while the automotive industry increasingly relies on high-speed PCIe SSD storage for autonomous driving systems that demand instantaneous data access and processing reliability.

Asia-Pacific Emerges as a Key Growth Region for PCIe SSD for AI Adoption

From a regional perspective, Asia-Pacific , led by China, South Korea, Japan, and Southeast Asia , is establishing itself as a critical growth hub for PCIe SSD for AI market. Significant government investments in AI infrastructure, the expansion of hyperscale data centers, and the strong presence of leading semiconductor manufacturers in the region are collectively driving accelerated deployment of AI-optimized PCIe SSDs. North America continues to represent a mature and technology-forward market, with enterprises actively upgrading storage architectures to support next-generation AI and machine learning initiatives. Meanwhile, Europe is witnessing steady growth as digital transformation programs and AI research initiatives gain traction across key economies including Germany, France, and the United Kingdom.

COMPETITIVE LANDSCAPE

Key Industry Players

PCIe SSD for AI Market , Competitive Dynamics, Strategic Positioning, and Leading Manufacturer Profiles

The global PCIe SSD for AI market is characterized by intense competition among a handful of technologically advanced semiconductor and storage solution providers. Samsung Electronics maintains its position as the dominant force in this space, leveraging its vertically integrated NAND flash manufacturing capabilities and extensive R&D investments to deliver high-performance PCIe 4.0 and PCIe 5.0 SSDs tailored for AI and machine learning workloads. The South Korean giant’s enterprise-grade SSD portfolio , engineered for ultra-low latency, exceptional IOPS, and sustained data throughput , makes it the preferred supplier for hyperscale data centers and AI infrastructure deployments globally. Western Digital and Micron Technology closely follow, each bringing formidable NAND fabrication expertise and robust product roadmaps focused on next-generation PCIe interfaces. SK Hynix, buoyed by its acquisition of Intel’s NAND and SSD business, has significantly strengthened its competitive standing, offering storage solutions optimized for high-performance computing (HPC) and AI training environments. The top five players collectively commanded a substantial share of global market revenue in 2025, underscoring the oligopolistic nature of this high-barrier industry, which was valued at approximately USD 527 million in 2025 and is projected to reach USD 1,086 million by 2034, growing at a CAGR of 11.2%.

Beyond the leading incumbents, several niche and emerging players are actively carving out competitive positions within the PCIe SSD for AI ecosystem. KIOXIA (formerly Toshiba Memory) continues to leverage its deep NAND flash heritage to deliver enterprise SSDs with strong endurance characteristics suited to continuous AI inference workloads. Intel, through its Optane and QLC NAND SSD lines, targets latency-sensitive AI applications in data centers and edge computing environments. Seagate Technology, traditionally a hard disk drive leader, has strategically expanded its SSD portfolio to address AI and HPC storage demands. Kingston Technology and ADATA serve as competitive mid-market players, offering cost-effective PCIe SSD solutions for industrial AI and automotive applications. Gigabyte Technology, primarily known for its motherboards and PC components, also participates in this market with PCIe SSD offerings targeting workstation-class AI development use cases. Collectively, these players are driving innovation across PCIe 4.0 and PCIe 5.0 SSD segments, intensifying competition on performance benchmarks, power efficiency, and total cost of ownership for AI-driven enterprise customers worldwide.

List of Key PCIe SSD for AI Companies Profiled

- Samsung Electronics

- Western Digital

- Kingston Technology

- SK Hynix

- Seagate Technology

- ADATA Technology

- Micron Technology

- Gigabyte Technology

- KIOXIA Holdings

- Intel Corporation

- Sabrent

- Corsair Components

- Solidigm (formerly Intel NAND Business)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

PCIe 5.0 SSD is rapidly emerging as the leading segment, driven by the exponentially growing bandwidth demands of modern AI and machine learning workloads.

|

| By Application |

|

High Performance Computing (HPC) stands as the dominant application segment, underpinned by the insatiable data processing requirements of AI-driven scientific research and enterprise analytics.

|

| By End User |

|

Hyperscale Data Centers & Cloud Providers represent the most influential end-user segment, as these organizations are at the forefront of deploying AI infrastructure at massive scale.

|

| By Form Factor |

|

EDSFF (Enterprise and Datacenter Standard Form Factor) is gaining strong momentum as the preferred form factor for next-generation AI data center deployments.

|

| By Deployment Mode |

|

Cloud-Based Deployment leads the market as the preferred mode for large-scale AI model development and training, offering organizations the flexibility to scale storage resources dynamically in alignment with fluctuating AI workload demands.

|

Regional Analysis: PCIe SSD for AI Market

North America

North America’s hyperscale data center footprint is expanding rapidly to accommodate surging AI workloads. Major cloud and technology operators are commissioning next-generation facilities optimized for PCIe SSD for AI deployments, prioritizing ultra-low latency storage access. This infrastructure buildout directly accelerates regional demand, as AI training pipelines require sustained high-bandwidth storage performance that only advanced PCIe SSD architectures can reliably deliver at scale.

Across healthcare, financial services, and autonomous vehicle industries, North American enterprises are embedding AI capabilities into core operations. This broad sectoral adoption is fueling procurement of PCIe SSD for AI solutions that can handle complex inference tasks and large-scale data pipelines. Decision-makers are prioritizing storage solutions that complement GPU clusters, driving sustained regional investment in high-performance PCIe SSD technologies.

The United States hosts a highly concentrated semiconductor research ecosystem, with leading fabless designers and storage solution innovators continuously advancing PCIe SSD for AI architectures. Collaborative partnerships between universities, national laboratories, and private technology companies are accelerating next-generation PCIe SSD development. This innovation pipeline ensures North America remains at the forefront of performance breakthroughs relevant to AI storage infrastructure demands.

Supportive government policies, including strategic federal investment in domestic semiconductor manufacturing and AI research, are reinforcing North America’s competitive position in PCIe SSD for AI market. Favorable regulatory frameworks reduce market entry barriers for innovative storage solution providers, while public-private partnerships ensure the region maintains a technology leadership posture critical to sustaining AI infrastructure competitiveness well into the 2030s.

Europe

Europe represents a strategically significant and steadily maturing region within the global PCIe SSD for AI market. Nations such as Germany, France, the United Kingdom, and the Netherlands are driving regional momentum through coordinated investment in AI research programs and digital infrastructure modernization initiatives. The European Union’s comprehensive AI strategy and data governance frameworks are prompting enterprises and public-sector organizations to invest in compliant, high-performance storage solutions. PCIe SSD for AI technologies are increasingly deployed across automotive AI research, industrial automation, and smart manufacturing environments, sectors where Europe holds established global competitiveness. Regional data sovereignty requirements are further encouraging local data center operators to upgrade storage infrastructures with advanced PCIe SSD solutions capable of supporting sensitive AI workloads. While Europe’s pace of adoption is somewhat moderated by regulatory compliance complexity, the region’s long-term trajectory remains robustly positive as AI integration deepens across critical industries.

Asia-Pacific

Asia-Pacific is emerging as one of the fastest-evolving regions in the global PCIe SSD for AI market, underpinned by aggressive government-led AI development programs and rapid expansion of digital infrastructure across China, Japan, South Korea, and India. China’s national AI strategy has catalyzed enormous investment in indigenous AI computing infrastructure, creating substantial demand for high-performance PCIe SSD for AI applications within cloud platforms and research institutions. South Korea and Japan contribute through advanced semiconductor manufacturing capabilities and strong enterprise adoption of AI-powered industrial systems. India is experiencing accelerating momentum as a growing AI services hub, prompting increased procurement of PCIe SSD for AI workloads across cloud and enterprise environments. The region’s combination of manufacturing scale, government policy support, and expanding AI application breadth positions Asia-Pacific as a critical growth engine for PCIe SSD for AI market through 2034.

South America

South America occupies an emerging position within the global PCIe SSD for AI market, with Brazil serving as the primary growth driver alongside growing interest from Argentina and Chile. The region is in relatively early stages of enterprise AI adoption; however, expanding cloud infrastructure investments and increasing digitalization across financial services, agriculture technology, and telecommunications sectors are gradually stimulating demand for PCIe SSD for AI solutions. Multinational technology companies are extending data center footprints into South America to serve growing regional cloud consumption, which indirectly accelerates PCIe SSD for AI procurement. Economic variability and infrastructure development gaps present challenges to uniform regional growth, but the long-term outlook remains cautiously optimistic as regional governments increasingly recognize AI infrastructure as a strategic national priority and allocate resources accordingly toward advancing digital capabilities.

Middle East & Africa

The Middle East and Africa region represents a nascent but increasingly strategic segment of the global PCIe SSD for AI market. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are spearheading AI-driven national transformation agendas supported by sovereign wealth fund investments in smart city projects, AI research centers, and next-generation data center facilities. These initiatives are generating early but meaningful demand for high-performance PCIe SSD for AI infrastructure. South Africa and select East African economies are beginning to experience digital infrastructure expansion driven by mobile connectivity growth and emerging cloud service adoption. While the broader African continent remains in nascent stages relative to global counterparts, targeted investment in technology parks and AI capacity-building programs signals a constructive long-term trajectory for PCIe SSD for AI market development across the region through the forecast horizon.

Report Scope

This market research report provides a comprehensive analysis of PCIe SSD for AI market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of PCIe SSDs in powering advancements across industries such as high performance computing, data centers, automotive, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of PCIe SSD for AI Market?

-> Global PCIe SSD for AI Market was valued at USD 527 million in 2025 and is expected to reach USD 1086 million by 2034, growing at a CAGR of 11.2% during the forecast period.

Which key companies operate in PCIe SSD for AI Market?

-> Key players include Samsung, Western Digital, Kingston, SK Hynix, Seagate Technology, ADATA, Micron Technology, Gigabyte, KIOXIA, and Intel, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for AI and machine learning workloads in data centers, increasing adoption of deep learning and neural network training applications, growing need for high IOPS and low-latency storage solutions, and rapid expansion of enterprise AI infrastructure.

Which region dominates the market?

-> Asia-Pacific is a significant and fast-growing region in PCIe SSD for AI market, with North America also holding a substantial market share driven by advanced data center investments and AI adoption.

What are the emerging trends?

-> Emerging trends include adoption of PCIe 5.0 SSDs for next-generation AI workloads, increasing integration of SSDs in high performance computing (HPC) environments, growing utilization in automotive AI applications, and expanding industrial use cases for AI-driven data processing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...