PCIe 6.0 AI Accelerator Interconnect Market Insights

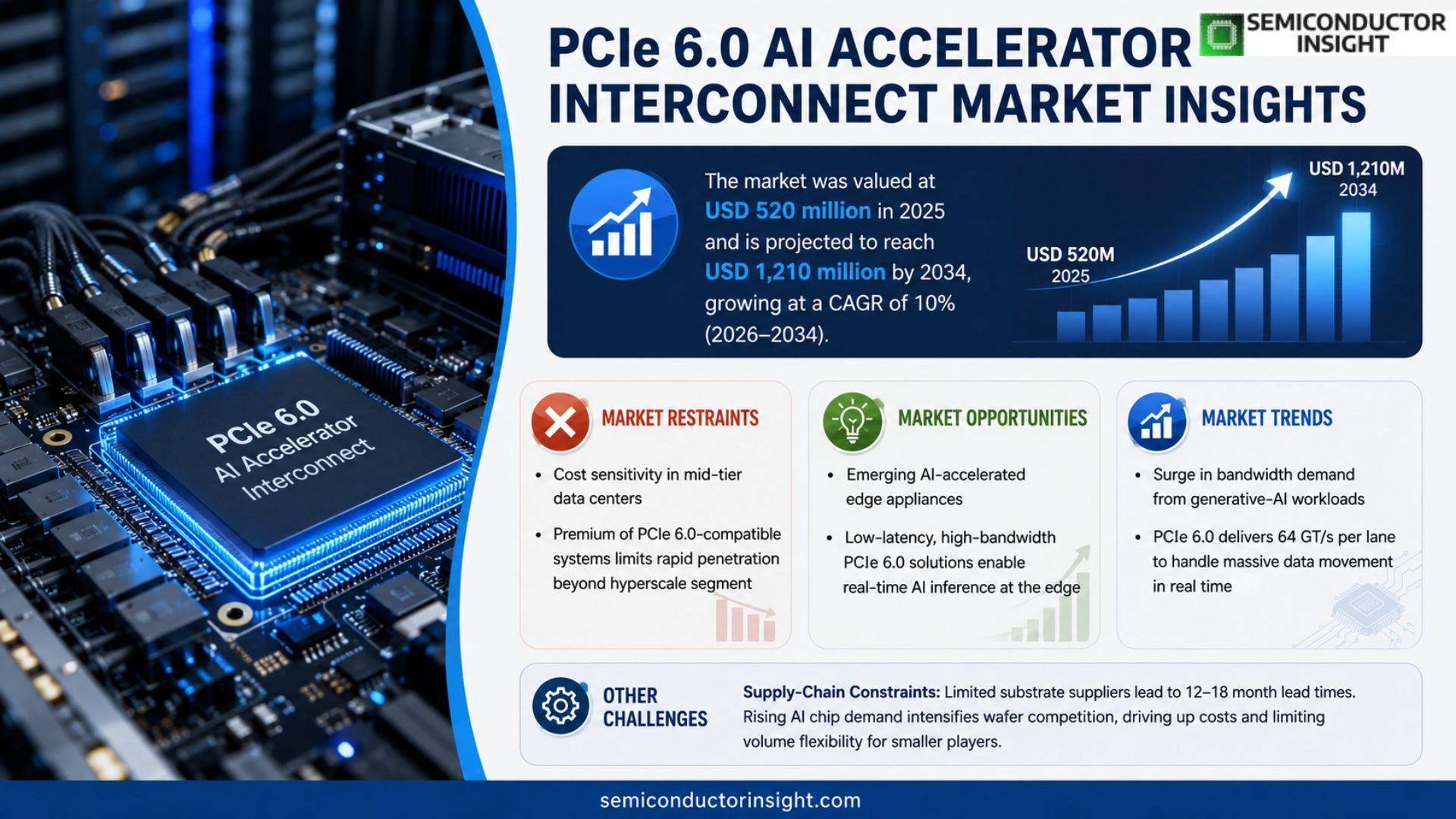

PCIe 6.0 AI accelerator interconnect market was valued at USD 520 million in 2025 and is forecasted to climb to USD 1,210 million by 2034, reflecting an implied CAGR of roughly 10 % over the nine‑year horizon.

PCIe 6.0 AI accelerator interconnects constitute ultra‑high‑bandwidth serial pathways that link artificial‑intelligence processors directly to host CPUs or memory subsystems. Each lane can sustain up to 64 GT/s while maintaining power efficiency through adaptive equalization and advanced error correction mechanisms. The architecture supports flexible lane aggregation,ranging from x8 up to x16 configurations,allowing system designers to balance throughput against board real estate when building hyperscale training clusters or compact edge inference appliances.

The upward trajectory stems from several intertwined forces: cloud operators are scaling generative‑AI services that demand ever‑higher data movement rates; semiconductor vendors such as Intel and Nvidia have introduced reference designs that embed PCIe 6.0 compliance as a baseline feature; meanwhile standards bodies have accelerated certification timelines, making it easier for OEMs to adopt the technology across server generations.

MARKET DRIVERS

Bandwidth Demands from Generative AI Models

The surge in generative‑AI workloads forces data‑center architects to seek interconnects that can sustain multi‑terabyte per second traffic. PCIe 6.0 AI Accelerator Interconnect Market delivers a raw data path that exceeds 64 GT/s, cutting latency by roughly 30 % compared with its predecessor. This performance edge translates into faster model training cycles, a factor that large cloud providers cite when allocating capital for new chassis.

Standardization Momentum in Edge Deployments

Edge‑centric AI inference faces a fragmented connector landscape, inflating integration costs. Recent consortium agreements around the PCI‑SIG specification have aligned firmware updates across multiple vendors, easing the transition to the sixth‑generation interface. Companies that adopt the unified standard report up to a 20 % reduction in bill‑of‑materials, a compelling economic incentive for early migration.

➤ “The jump to PCIe 6.0 reshapes the cost‑performance curve for AI accelerators, making it the new baseline for high‑throughput workloads,” says a senior architect at a leading hyperscale operator.

Beyond raw speed, the newer protocol incorporates advanced error‑correction mechanisms, which enhance overall system availability. For enterprises that cannot afford downtime, the reliability uplift supports service‑level‑agreement (SLA) compliance and unlocks premium pricing opportunities for latency‑sensitive AI services.

MARKET CHALLENGES

Design Complexity for Heterogeneous Systems

Integrating PCIe 6.0 with legacy components demands intricate PHY tuning and power‑budget reallocation. Vendors that overlook these nuances risk signal integrity issues that can erode the promised throughput gains. The resulting redesign cycles add months to product roadmaps, especially for firms relying on mixed‑generation accelerator fleets.

Other Challenges

Supply‑Chain Constraints

The semiconductor substrate required for the high‑speed transceivers is currently sourced from a limited pool of manufacturers, creating lead‑time extensions of 12‑18 months. Concurrently, the rise in demand for AI‑specific silicon intensifies competition for wafer capacity, pressuring pricing and limiting the ability of smaller players to secure volume discounts.

MARKET RESTRAINTS

Cost Sensitivity in Mid‑Tier Data Centers

Mid‑tier operators often balance performance upgrades against budgetary ceilings. The premium associated with PCIe 6.0‑compatible motherboards and power delivery subsystems can exceed 15 % of total server cost, prompting many to defer migration until the technology attains broader price parity. This price barrier curtails rapid market penetration beyond the hyperscale segment.

MARKET OPPORTUNITIES

Emerging AI‑Accelerated Edge Appliances

Edge appliances that embed AI inference engines stand to benefit from the low‑latency, high‑bandwidth profile of the newest interconnect. Manufacturers that bundle PCIe 6.0 with compact, power‑efficient accelerator modules can capture a growing niche where real‑time decision making is a competitive differentiator. Early entrants are positioning themselves to lock in design wins as telecom operators roll out 5G‑enabled AI services, creating a clear pathway for revenue expansion within the PCIe 6.0 AI Accelerator Interconnect Market.

PCIe 6.0 AI Accelerator Interconnect Market Trends

Surge in Bandwidth Demand from Generative‑AI Workloads

The launch of generative‑AI services at cloud scale has reshaped data‑movement requirements. Operators now routinely shuffle terabytes of model parameters and inference tensors within sub‑second windows, a regime where legacy interconnects become bottlenecks. PCIe 6.0, with its 64 GT/s per lane capability, delivers the headroom needed to keep latency on a floor and sustain throughput as model sizes swell. The market’s valuation of USD 520 million in 2025 and its projection to USD 1,210 million by 2034 reflect a near‑doubling that mirrors the acceleration of AI‑driven traffic across hyperscale facilities. The underlying driver is not merely incremental speed but a shift toward real‑time, multi‑modal generation that forces system architects to rethink link topology and power budgeting.

Other Trends

Adoption Across Server and Edge Segments

While hyperscale data centers dominate early volume, the same interconnect is finding traction in edge inference boxes where board space is scarce. PCIe 6.0’s flexible lane aggregation,from x8 up to x16,allows designers to balance raw bandwidth against form‑factor constraints. In compact edge appliances, a x8 configuration can still move enough data to support on‑device large‑language model inference without exhausting thermal budgets. Conversely, training clusters favor x16 lanes to saturate GPU‑to‑CPU pathways, ensuring that the massive gradients exchanged during back‑propagation do not stall. This dual‑use scenario widens the addressable base for the PCIe 6.0 AI Accelerator Interconnect Market, prompting vendors to ship reference boards that span both ends of the spectrum.

Ecosystem Alignment and Certification Acceleration

Semiconductor leaders such as Intel and Nvidia have embedded PCIe 6.0 compliance into their reference designs, effectively setting a new baseline for AI accelerator products. Simultaneously, standards bodies have shortened certification cycles, turning what was a multi‑year qualification into a streamlined process that OEMs can incorporate into regular product refreshes. The combined effect reduces time‑to‑market for next‑generation servers and shortens the risk horizon for system integrators. As a result, companies that adopt the technology earlier can leverage higher throughput to differentiate services, while late adopters may face competitive pressure to retrofit existing platforms or risk falling behind in AI performance metrics.

COMPETITIVE LANDSCAPE

Key Industry Players

PCIe 6.0 AI Accelerator Interconnect Market – Competitive Overview

Intel dominates the early‑stage ecosystem, leveraging its long‑standing PCIe leadership and its Xeon Scalable family to ship reference platforms that integrate PCIe 6.0 lanes directly to AI‑focused add‑in cards. The company’s aggressive silicon roadmap, combined with a deep OEM network, forces downstream suppliers to align their design‑in strategies with Intel’s timing, effectively creating a tiered supplier hierarchy. Nvidia follows a parallel path; its DGX systems now ship with PCIe 6.0‑ready networking fabrics, positioning the firm as the de‑facto benchmark for high‑throughput training clusters. The duopoly of Intel and Nvidia shapes pricing pressure and accelerates certification cycles, compelling smaller vendors to either specialize in niche form‑factors or partner with one of the two giants to gain market traction.

Beyond the two titans, a constellation of niche innovators competes on differentiated IP and custom silicon. AMD, through its acquisition of Xilinx, offers programmable logic that can be tuned for PCIe 6.0 lane aggregation, appealing to edge‑compute OEMs that value flexibility over raw density. Marvell and Broadcom provide controller chips that embed advanced equalization, enabling board‑level power savings. Qualcomm and MediaTek are exploring integration of PCIe 6.0 into next‑generation SoCs for AI inference at the network edge, where latency dominates design decisions. Arm’s ecosystem partners, such as Synopsys and Cadence, supply verification and design‑enable tools that lower the barrier for new entrants. Samsung and IBM, while not primary vendors of accelerator cards, contribute high‑performance memory subsystems that complement PCIe 6.0 pathways, reinforcing the overall value chain. Collectively, these players sustain a vibrant competitive fabric that pushes performance envelopes while keeping the supply base diversified.

List of Key PCIe 6.0 AI Accelerator Interconnect Companies Profiled

- Intel

- Nvidia

- AMD

- Xilinx

- Marvell

- Broadcom

- Qualcomm

- MediaTek

- Arm

- Synopsys

- Cadence

- Samsung

- IBM

- Ambarella

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Compute‑focused Accelerators

|

| By Application |

|

Data Center Training

|

| By End User |

|

Cloud Service Providers

|

| By Performance Tier |

|

Ultra‑High Performance

|

| By Deployment Environment |

|

Hyperscale Server Farms

|

Regional Analysis: PCIe 6.0 AI Accelerator Interconnect Market

North America

The semiconductor fabs across the United States and Canada have already qualified advanced node processes for the higher signal‑integrity demands of PCIe 6.0. This readiness shortens time‑to‑market for AI accelerator chips, while close proximity to design houses reduces iteration cycles and logistical friction.

Leading universities and research labs are securing joint grants to explore heterogeneous memory hierarchies that exploit PCIe 6.0’s expanded lane count. The resultant intellectual property is quickly absorbed by start‑ups, fostering a pipeline of niche accelerators that target latency‑critical workloads.

Cloud service providers are standardizing on the new interconnect to future‑proof their hyperscale racks. The ability to double effective bandwidth without a proportional power penalty is especially compelling for transformer‑based models that dominate generative AI pipelines.

Recent guidance from the FCC on electromagnetic emissions for high‑speed links has been incorporated into early silicon designs, allowing manufacturers to certify products faster and avoid costly redesigns downstream.

Europe

European federations are leveraging their strong standards‑development heritage to influence the implementation profile of PCIe 6.0 in AI workloads. The region’s emphasis on data‑sovereignty drives customers to favour on‑premise acceleration solutions that can be tightly integrated with existing enterprise networks. Moreover, a surge in cross‑border collaborations between German chip designers and French AI research institutes is generating bespoke interconnect configurations that prioritize security as well as performance. This nuanced approach creates a niche market for modular accelerator boards that can be re‑certified for compliance in multiple jurisdictions, offering a competitive edge to vendors that embed robust encryption into the link layer.

Asia‑Pacific

The Asia‑Pacific market is distinguished by its rapid scaling of AI compute capacity, particularly in China, Japan, and South Korea. Local manufacturers are embedding PCIe 6.0 directly into system‑on‑chip solutions to meet the massive data‑throughput requirements of next‑generation language models. Government‑backed AI strategies accelerate infrastructure spending, yet the region also grapples with fragmented standards adoption across different supply chains. Companies that can deliver turnkey solutions,combining accelerator silicon, motherboard design, and firmware that harmonizes the new interconnect,are poised to capture enterprise contracts that prize speed of deployment over marginal cost differences.

South America

In South America, the adoption curve is shaped by a mix of legacy data‑center upgrades and a growing appetite for AI‑enabled services in fintech and agritech. While overall investment levels lag behind more mature markets, regional cloud operators are beginning to retrofit edge nodes with PCIe 6.0 capable accelerators to reduce latency for real‑time analytics. The bottleneck often lies in the availability of qualified engineering talent, prompting multinational firms to establish regional development centers focused on integration testing and localized support.

Middle East & Africa

The Middle East & Africa region is entering the PCIe 6.0 era through strategic partnerships with global chipset vendors looking to diversify their supply base. Sovereign wealth funds are earmarking capital for AI research hubs that require high‑performance interconnects to link compute clusters across dispersed data‑center campuses. In Africa, pilot projects in smart‑city initiatives are experimenting with low‑power accelerator modules that still benefit from the bandwidth uplift of the new PCIe specification, signaling a nascent but potentially fast‑growing segment.

Report Scope

This market research report provides a comprehensive analysis of the PCIe 6.0 AI Accelerator Interconnect Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of PCIe 6.0 AI Accelerator Interconnect Market?

-> PCIe 6.0 AI accelerator interconnect market is forecasted to climb to USD 1,210 million by 2034, reflecting an implied CAGR of roughly 10 %

Which key companies operate in PCIe 6.0 AI Accelerator Interconnect Market?

-> Key players include Intel Corporation, Nvidia Corporation, Advanced Micro Devices (AMD), Samsung Electronics, and Micron Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rapid scaling of generative‑AI services by cloud operators, increasing data‑movement requirements in hyperscale training clusters, and the introduction of reference designs by major semiconductor vendors that embed PCIe 6.0 compliance as a baseline feature.

Which region dominates the market?

-> North America holds the largest market share due to early adoption of AI infrastructure, while Asia‑Pacific is emerging as the fastest‑growing region driven by strong semiconductor manufacturing bases and expanding cloud data‑center deployments.

What are the emerging trends?

-> Emerging trends include higher lane aggregation (x8 to x16) for ultra‑high‑bandwidth pathways, adaptive equalization for power‑efficient high‑speed signaling, and accelerated certification timelines from standards bodies that streamline OEM adoption across successive server generations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...