MARKET INSIGHTS

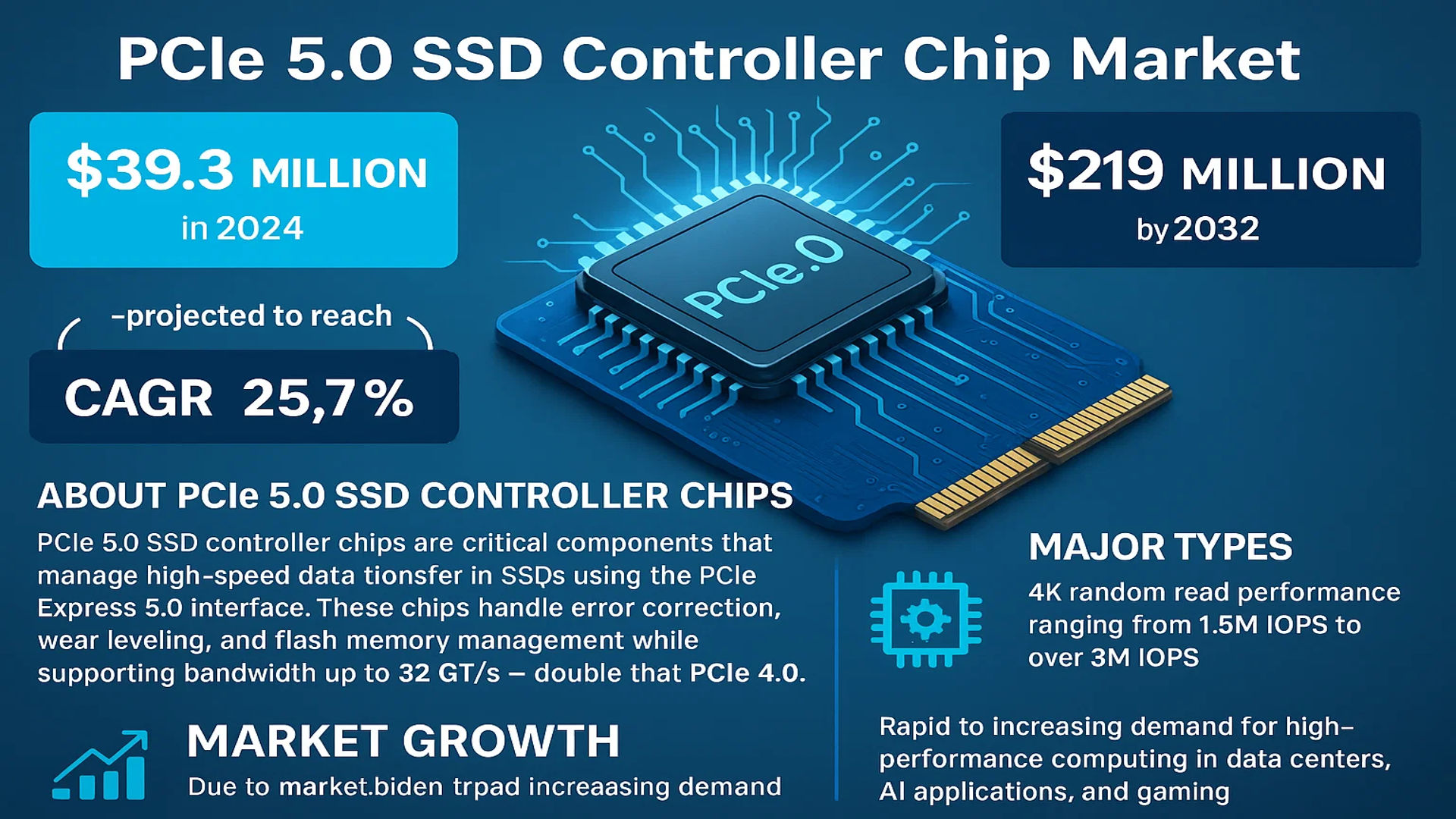

The global PCIe 5.0 SSD Controller Chip Market was valued at 39.3 million in 2024 and is projected to reach US$ 219 million by 2032, at a CAGR of 25.7% during the forecast period.

PCIe 5.0 SSD controller chips are critical components that manage high-speed data transfer in solid-state drives (SSDs) using the PCI Express 5.0 interface. These chips handle functions like error correction, wear leveling, and flash memory management while supporting bandwidth up to 32 GT/s (gigatransfers per second) – double that of PCIe 4.0. Major types include controllers with 4K random read performance ranging from 1.5M IOPS to over 3M IOPS.

The market is growing rapidly due to increasing demand for high-performance computing in data centers, AI applications, and gaming. While North America currently leads adoption, Asia-Pacific shows strong growth potential because of expanding semiconductor manufacturing capabilities. Key players like Phison, Silicon Motion, and Marvell are driving innovation with new controller designs, though supply chain challenges and thermal management remain industry hurdles. The transition to PCIe 5.0 SSDs is accelerating as next-generation processors from Intel and AMD now support the standard.

MARKET DYNAMICS

MARKET DRIVERS

Demand for High-Performance Computing Fuels PCIe 5.0 SSD Controller Chip Adoption

The global push toward high-performance computing (HPC) and AI-driven workloads is accelerating demand for PCIe 5.0 SSD controller chips. These chips enable data transfer speeds up to 32 GT/s (GigaTransfers per second), delivering nearly double the bandwidth of previous-generation PCIe 4.0 solutions. With AI infrastructure requiring faster data access for training models, enterprises are rapidly upgrading storage subsystems. The server segment accounted for over 60% of controller chip revenue in 2024, reflecting enterprise prioritization of storage performance for AI/ML applications.

Gaming and Content Creation Markets Drive Consumer Demand

The consumer electronics segment is experiencing significant growth due to rising expectations for ultra-fast storage in gaming PCs and content creation workstations. Next-generation consoles and high-end GPUs are increasingly bottlenecked by storage speeds, making PCIe 5.0 solutions essential for reducing load times. Content creators working with 8K video and complex 3D assets require the 4K Random Read capabilities exceeding 3M IOPS that PCIe 5.0 controllers enable. This segment is projected to grow at 28% CAGR through 2032 as consumer tolerance for latency decreases.

Data Center Modernization Creates Sustained Demand

Cloud service providers are undertaking massive infrastructure upgrades to support next-generation services, with storage being a critical focus area. PCIe 5.0 SSD controllers reduce power consumption per TB transferred by approximately 30% compared to PCIe 4.0 solutions while handling heavier workloads. This improved power efficiency is driving adoption in hyperscale data centers where energy costs significantly impact operating expenses. With enterprise SSD shipments for data centers expected to triple by 2026, the controller chip market will experience parallel growth.

MARKET RESTRAINTS

Thermal Management Challenges Limit Adoption in Compact Devices

PCIe 5.0 controller chips generate substantially more heat than previous generations due to increased signaling rates and power requirements. This creates significant design challenges for slim laptops and small form factor devices where thermal budgets are constrained. Many consumer devices currently cannot accommodate the necessary cooling solutions without compromising product designs, limiting market penetration in these segments. Industry testing shows controller temperatures can exceed 100°C under sustained loads without proper heat dissipation.

Other Restraints

Limited PCIe 5.0 Platform Penetration

The installed base of systems with native PCIe 5.0 support remains relatively small outside enterprise environments. While AMD and Intel have introduced supporting chipsets, widespread platform adoption will take several more product generations. This creates a mismatch between available storage solutions and compatible systems, particularly in price-sensitive consumer markets.

Signal Integrity Complexity

Achieving reliable signaling at PCIe 5.0 speeds requires advanced PCB designs with strict impedance control and specialized materials. Many manufacturers lack experience designing for these specifications, resulting in higher development costs and longer time-to-market for compatible products.

MARKET CHALLENGES

Advanced Node Manufacturing Creates Supply Chain Pressures

Producing PCIe 5.0 controller chips at required performance levels typically requires 7nm or smaller process nodes, creating supply constraints as foundries allocate capacity to various high-demand sectors. The semiconductor industry’s ongoing consolidation and geopolitical factors further complicate supply reliability. Lead times for advanced node wafer starts have extended significantly, making inventory management more challenging for manufacturers.

Other Challenges

Firmware Development Complexity

Modern controller chips require sophisticated firmware to manage error correction, wear leveling, and performance optimization. Developing stable firmware for PCIe 5.0 solutions is exponentially more complex than for previous generations due to tighter timing requirements and advanced features like computational storage integration.

Testing Infrastructure Requirements

Validating PCIe 5.0 controller performance requires expensive test equipment capable of operating at 32 GT/s with sophisticated signal analysis capabilities. The capital investment needed for comprehensive testing creates barriers to entry for smaller market participants.

MARKET OPPORTUNITIES

Emerging Computational Storage Applications Open New Markets

PCIe 5.0’s increased bandwidth enables practical implementation of computational storage architectures where processing occurs directly within storage devices. This paradigm shift reduces data movement and can accelerate specific workloads by up to 40% compared to traditional architectures. Early applications in database operations, video transcoding, and financial analytics are demonstrating compelling performance benefits.

Automotive and Edge Computing Present Growth Frontiers

The automotive sector’s transition to software-defined vehicles creates demand for high-performance storage solutions in next-generation architectures. Edge computing deployments also require robust storage capabilities closer to data generation points. While these applications currently represent small market segments, they are projected to grow at 35% CAGR through 2032 as autonomous capabilities and 5G networks mature.

Advanced Packaging Technologies Enable Performance Breakthroughs

Emerging 3D packaging and chiplet architectures allow controller designers to optimize different functional blocks on appropriate process nodes while maintaining PCIe 5.0’s stringent performance requirements. These approaches can improve power efficiency by 25% while reducing development costs for specialized variants targeting particular market segments.

PCIe 5.0 SSD CONTROLLER CHIP MARKET TRENDS

High-Performance Computing and AI Workloads Accelerate PCIe 5.0 Adoption

The PCIe 5.0 SSD controller chip market is experiencing rapid growth, driven by the increasing demand for high-speed data processing in artificial intelligence (AI), machine learning, and data-intensive workloads. The PCIe 5.0 standard doubles the bandwidth of its predecessor, enabling sequential read speeds exceeding 14,000 MB/s, a critical requirement for modern enterprise servers, hyperscale data centers, and next-gen gaming systems. With the rise of generative AI applications, real-time data analytics, and cloud computing, PCIe 5.0 SSD controllers are becoming essential for reducing latency and improving system responsiveness. Recent advancements in NAND flash memory technology and error correction algorithms further enhance their efficiency, making them crucial for mission-critical applications.

Other Trends

Consumer Electronics and Gaming Boom

The consumer electronics sector is a significant growth driver for PCIe 5.0 SSD controller chips with high-performance gaming PCs, high-end workstations, and next-gen consoles requiring faster storage solutions. The segment of 4K Random Read: 2M IOPS is particularly gaining traction due to its ability to handle massive gaming textures and complex application loads. Meanwhile, the growing popularity of content creation software and immersive VR/AR experiences further accelerates demand for high-bandwidth storage solutions. Emerging markets in Asia, particularly China, are rapidly adopting PCIe 5.0 SSDs due to their competitive pricing and improved performance.

Enterprise Storage and Data Center Expansion

Enterprise storage and cloud service providers are increasingly upgrading to PCIe 5.0 SSD storage to optimize their infrastructure. The shift towards software-defined storage, edge computing, and real-time database applications demands faster NVMe SSDs with improved endurance. Leading manufacturers such as Silicon Motion, Phison, and Samsung are introducing advanced power-efficient controller chips with support for ECC (Error Correcting Code) and wear-leveling algorithms to enhance data integrity. Additionally, the increasing deployment of 5G networks and IoT devices necessitates ultra-low latency storage architectures, further fueling market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Fierce Competition in PCIe 5.0 Controller Space

The global PCIe 5.0 SSD controller chip market shows a moderately consolidated structure, dominated by established semiconductor firms while witnessing aggressive entry from specialized startups. Phison Electronics and Silicon Motion Technology currently lead in market share, benefiting from their early investments in PCIe 5.0 architectures and partnerships with major NAND flash manufacturers. These Taiwanese companies have successfully translated their PCIe 4.0 expertise into next-generation designs, capturing significant OEM design wins across consumer and enterprise segments.

Meanwhile, Marvell Technology has leveraged its data center expertise to gain strong traction in high-performance server applications, while Microchip Technology focuses on industrial and embedded markets with robust reliability features. Korean giant Samsung Electronics maintains vertical integration advantages through its in-house controller development for proprietary SSDs, though its market position could shift as it considers supplying controllers to third-party drive makers.

The competitive intensity continues rising as Chinese contenders like T-Head Semiconductor (Alibaba Group) and Starbreeze accelerate development with substantial R&D budgets. These players are challenging incumbents through aggressive pricing strategies and customization capabilities tailored to domestic cloud providers and hyperscalers. The market has also seen new entrants like Innogrit and YEESTOR making strides with innovative architectures focused on power efficiency – a critical factor for mobile and edge computing applications.

Recent technological developments include Phison’s PS5026-E26 controller reaching mass production with 14GB/s sequential speeds, while Marvell’s Bravera SC5 series targets AI/ML workloads with specialized queuing architectures. Such innovations demonstrate the industry’s rapid evolution beyond raw speed metrics to address emerging workload requirements in data centers and enterprise environments.

List of Key PCIe 5.0 SSD Controller Chip Manufacturers:

- Phison Electronics Corp. (Taiwan)

- Silicon Motion Technology (Taiwan)

- Marvell Technology Group (U.S.)

- Microchip Technology Inc. (U.S.)

- Samsung Electronics (South Korea)

- T-Head Semiconductor (China)

- ScaleFlux (U.S.)

- Starblaze Technology (China)

- Innogrit Corporation (U.S.)

- YEESTOR Microelectronics (China)

Segment Analysis:

By Type

4K Random Read: 2M IOPS Segment Leads Due to High Performance Demands in Enterprise Storage

The market is segmented based on type into:

- 4K Random Read: 1.5M IOPS

- 4K Random Read: 2M IOPS

- 4K Random Read: 2.5M IOPS

- 4K Random Read: 3M IOPS

- Others

By Application

Server Segment Dominates Due to High-Speed Data Processing Requirements in Cloud Computing

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: Gaming PCs, High-end Laptops

- Server

- Subtypes: Cloud Servers, Enterprise Data Centers

- Industrial Automation

- Others

By Architecture

Multi-Core Controller Architecture Gains Traction for Parallel Processing Capabilities

The market is segmented based on architecture into:

- Single-core Controllers

- Dual-core Controllers

- Multi-core Controllers

- Subtypes: 4-core, 8-core

By Interface

NVMe 2.0 Interface Shows Strong Adoption for Next-Generation SSDs

The market is segmented based on interface into:

- NVMe 1.4

- NVMe 2.0

- Customized Protocols

Regional Analysis: PCIe 5.0 SSD Controller Chip Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global PCIe 5.0 SSD controller chip market, driven by China’s aggressive semiconductor manufacturing policies and Japan’s advanced technological ecosystem. With China accounting for over 40% of global SSD controller chip production, the country’s focus on self-sufficiency in chip design has accelerated PCIe 5.0 adoption. Major Taiwanese players like Phison and Silicon Motion continue to lead controller chip innovation while benefiting from regional supply chain advantages. The growing data center investments across India and Southeast Asia further propel demand, though infrastructure limitations in emerging markets create uneven adoption rates. The region’s edge lies in its vertically integrated electronics manufacturing and cost-competitive R&D environments.

North America

North America represents the innovation hub for PCIe 5.0 controller architectures, with U.S.-based firms like Marvell and Microchip developing cutting-edge solutions for hyperscale data centers. The CHIPS Act funding is strengthening domestic semiconductor capabilities while enterprise demand for high-performance computing fuels adoption. However, reliance on Asian foundries for actual chip production creates supply chain vulnerabilities. The Canadian market shows growing potential through partnerships between telecom providers and storage solution vendors, suggesting gradual market expansion beyond traditional server applications.

Europe

European demand focuses heavily on industrial and automotive applications of PCIe 5.0 technology, with German engineering firms integrating advanced SSDs into automation systems. Stringent data privacy regulations indirectly drive controller chip requirements through increased enterprise storage needs. While European design houses contribute to controller IP development, limited local fabrication capacity keeps the region dependent on imports. The EU’s Chips Act aims to reduce this dependency, though market observers note implementation lags compared to Asian and American initiatives. Nordic countries show particular strength in data center applications benefiting from sustainable energy advantages.

Middle East & Africa

Emerging as a strategic growth area, the Middle East demonstrates rapid uptake in government-led digital transformation projects utilizing PCIe 5.0 storage solutions. Gulf nations are investing heavily in AI infrastructure, creating specialized demand for high-IOPS controller chips. Africa’s market remains constrained by limited data center penetration, though mobile payment systems and telecommunications upgrades present future opportunities. Regional partnerships with Chinese tech firms are establishing foundational semiconductor capabilities while still facing challenges in technical workforce development and supply chain maturity.

South America

The South American market is in early adoption phase, with Brazil leading through financial sector modernization projects. Economic instability and import dependence have slowed enterprise investment, though increasing cloud service penetration drives gradual demand. Local manufacturing remains underdeveloped with most controller chips imported from Asia, presenting a barrier to widespread PCIe 5.0 adoption. The region shows promise in niche segments like industrial automation where specialized storage solutions can justify premium pricing, but broader market growth awaits improved economic conditions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional PCIe 5.0 SSD Controller Chip markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global PCIe 5.0 SSD Controller Chip market was valued at USD 39.3 million in 2024 and is projected to reach USD 219 million by 2032, growing at a CAGR of 25.7%.

- Segmentation Analysis: Detailed breakdown by product type (4K Random Read: 1.5M IOPS, 2M IOPS, 2.5M IOPS, 3M IOPS, Others), application (Consumer Electronics, Server, Industrial Automation, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy), Asia-Pacific (China, Japan, South Korea, India), Latin America, and the Middle East & Africa.

- Competitive Landscape: Profiles of leading market participants including Silicon Motion, Marvell, Microchip, Phison, SAMSUNG, T-Head Semiconductor, ScaleFlux, INNOGRIT, their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in PCIe 5.0 interface standards, integration of AI in storage management, and evolving semiconductor fabrication techniques.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for high-performance computing and data centers, along with challenges like supply chain constraints and thermal management issues.

- Stakeholder Analysis: Insights for component suppliers, SSD manufacturers, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in high-speed storage solutions.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global PCIe 5.0 SSD Controller Chip Market?

-> PCIe 5.0 SSD Controller Chip Market was valued at 39.3 million in 2024 and is projected to reach US$ 219 million by 2032, at a CAGR of 25.7% during the forecast period.

Which key companies operate in Global PCIe 5.0 SSD Controller Chip Market?

-> Key players include Silicon Motion, Marvell, Microchip, Phison, SAMSUNG, T-Head Semiconductor, ScaleFlux, INNOGRIT, and YEESTOR, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-performance computing, expansion of data centers, and adoption of PCIe 5.0 standard in next-generation SSDs.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by semiconductor manufacturing in China and South Korea, while North America leads in technological adoption.

What are the emerging trends?

-> Emerging trends include integration of AI for storage optimization, development of energy-efficient controllers, and increasing focus on enterprise-grade solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...