PCB embedded planar capacitor for PDN impedance reduction Market Insights

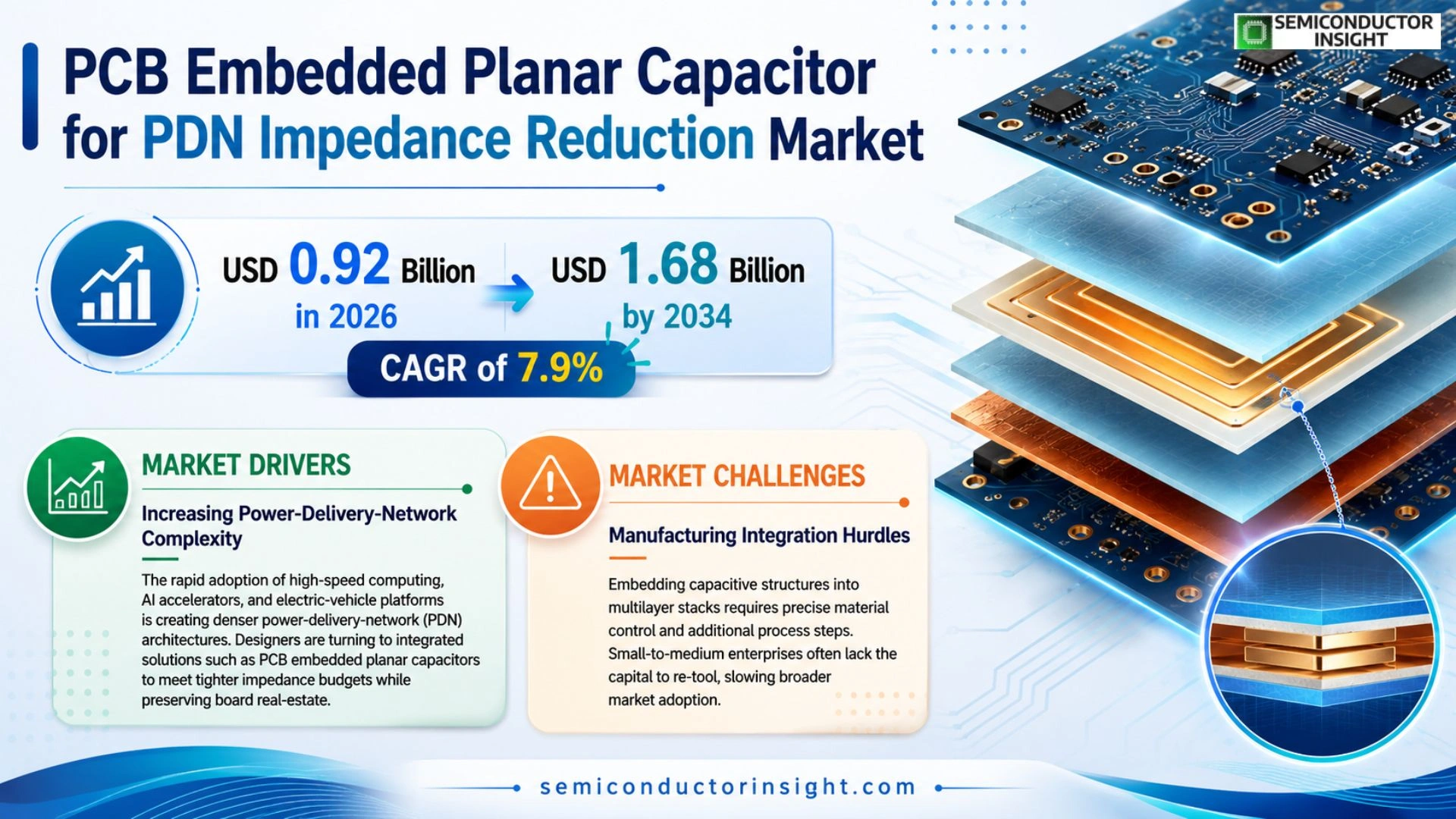

Global PCB embedded planar capacitor for PDN impedance reduction market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 092 billion in 2026 to USD 168 billion by 2034, exhibiting a CAGR of 7.9% during the forecast period.

PCB‑embedded planar capacitors are thin‑film dielectric structures fabricated directly within the substrate layers of printed circuit boards, providing localized decoupling capacitance without adding discrete components.

Because they reside close to power‑delivery networks (PDNs), they effectively lower loop inductance and suppress high‑frequency noise,critical for modern high‑speed digital and mixed‑signal designs.

The market is experiencing rapid expansion driven by increasing demand for higher data‑rate electronics, electric‑vehicle power systems, and stringent electromagnetic compatibility (EMC) requirements.

Furthermore, advances in low‑loss dielectric materials and automated embedding processes are reducing cost barriers.

MARKET DRIVERS

Increasing Power‑Delivery‑Network Complexity

The rapid adoption of high‑speed computing, AI accelerators, and electric‑vehicle platforms is creating denser power‑delivery‑network (PDN) architectures. Designers are turning to integrated solutions such as PCB embedded planar capacitors to meet tighter impedance budgets while preserving board real‑estate.

Demand for Miniaturization and Reliability

Embedded planar capacitors eliminate the need for discrete components, reducing solder‑joint failures and improving thermal performance. This reliability advantage is especially valued in aerospace and telecommunications where uptime is critical.

➤ Customers report up to a 30% reduction in PDN resonances when implementing embedded planar capacitors.

Regulatory pressures for energy‑efficient designs are also pushing manufacturers toward solutions that lower overall system impedance, positioning PCB embedded planar capacitor for PDN impedance reduction Market as a strategic enabler of next‑generation electronics.

MARKET CHALLENGES

Manufacturing Integration Hurdles

Embedding capacitive structures into multilayer stacks requires precise material control and additional process steps. Small‑to‑medium enterprises often lack the capital to re‑tool, slowing broader market adoption.

Other Challenges

Design Knowledge Gap

Many PCB designers are accustomed to discrete components and may underestimate the simulation expertise needed to model embedded planar capacitors accurately.

MARKET RESTRAINTS

Cost Sensitivity in High‑Volume Segments

Although embedded capacitors improve performance, the incremental material and processing costs can be prohibitive for consumer‑grade products where price elasticity is high. Companies must balance the benefit of impedance reduction against the added unit cost.

The return on investment is less clear for legacy platforms that are not being redesigned, limiting the incentive for retrofitting existing production lines with new embedding capabilities.

Supply‑chain volatility for high‑purity dielectric films further restricts consistent pricing, creating uncertainty for long‑term procurement planning.

MARKET OPPORTUNITIES

Growth in AI‑Accelerated Data Centers

Data centers powering AI workloads require ultra‑low PDN impedance to sustain rapid voltage transients. The need for stable power delivery opens a clear pathway for embedded planar capacitors to capture a sizable share of the upcoming hardware refresh cycles.

Emerging standards for automotive electrification, such as 48 V architectures, also demand compact, high‑Q decoupling solutions. OEMs are actively evaluating PCB embedded planar capacitor technologies as part of their next‑generation vehicle electronics roadmap.

Collaborative design tools that integrate electromagnetic simulation with PCB layout are lowering the expertise barrier, thereby expanding the addressable market for this technology.

PCB embedded planar capacitor for PDN impedance reduction Market Trends

Growing Adoption in High‑Speed Digital Systems

PCB embedded planar capacitor for PDN impedance reduction Market was valued at USD 0.85 billion in 2025. Forecasts indicate growth to USD 0.92 billion in 2025 and USD 1.68 billion by 2034, reflecting a compound annual growth rate of approximately 7.9 % over the projection period. The primary driver is the need for lower loop inductance and improved high‑frequency noise suppression in increasingly dense, high‑speed digital and mixed‑signal designs. By embedding thin‑film dielectric structures directly within PCB substrates, designers achieve localized decoupling without additional discrete components, which shortens power‑delivery paths and enhances overall system efficiency.

Other Trends

Material Innovation and Cost Reduction

Advances in low‑loss dielectric formulations are lowering the insertion loss of embedded planar capacitors, making them viable for cost‑sensitive applications. Automated embedding processes have matured, reducing labor intensity and material waste. These improvements are expanding the addressable market beyond flagship servers to include consumer electronics, where tighter Bill‑of‑Materials constraints demand economical solutions that still meet stringent electromagnetic compatibility requirements.

Integration into Electric‑Vehicle Power Architectures

Electric‑vehicle power modules are increasingly reliant on stable PDN performance to support fast‑charging interfaces and high‑power drive electronics. PCB embedded planar capacitor for PDN impedance reduction Market is benefitting from this trend, as manufacturers seek integrated decoupling that occupies minimal board real‑estate while delivering high capacitance density. The convergence of automotive safety standards and the push for higher power‑train efficiency is reinforcing demand for these embedded solutions across the next decade.

COMPETITIVE LANDSCAPE

Key Industry Players

PCB Embedded Planar Capacitor Market Overview

The market is currently dominated by large passive‑component manufacturers that have leveraged their expertise in thin‑film dielectric technologies to offer embedded planar capacitors directly within PCB substrates. TDK leads the segment with its high‑Q, low‑loss ceramic‑based embedded capacitors, supported by a robust portfolio of material patents and a global manufacturing footprint. Murata and AVX (Kyocera) follow closely, differentiating through advanced low‑ESR designs that target high‑speed digital and automotive power‑train applications. Vishay and TE Connectivity complement these leaders by integrating embedded capacitor capabilities into their broader PCB‑assembly services, enabling system‑level optimization of PDN impedance. Collectively, these firms command the majority of market revenue and shape the technology roadmap through heavy R&D investment.

Beyond the majors, a cluster of specialist firms contributes significant niche value and drives incremental innovation. Sunlord, Yageo, Samsung Electro‑Mechanics, and Taiyo Yuden focus on cost‑effective multilayer solutions for consumer electronics, while 3M and Koike produce high‑performance dielectric laminates for aerospace and defense platforms. PCB fabricators such as AT&S, Unimicron, and Zhen Ding Technology have launched embedded‑capacitor lines that embed the component during board build‑up, reducing BOM complexity for OEMs. Emerging players like Melexis and Delta Electronics are exploring integrated sensor‑power solutions that incorporate embedded capacitance to meet stringent EMC requirements in electric‑vehicle power systems. This diversified ecosystem ensures a healthy competitive environment, with both volume‑driven and high‑value players advancing the market toward the projected USD 1.68 billion size by 2034.

List of Key PCB Embedded Planar Capacitor Companies Profiled

- TDK

- Murata Manufacturing Co., Ltd.

- AVX (Kyocera)

- Vishay Intertechnology, Inc.

- TE Connectivity

- Sunlord Electronics

- Yageo Corporation

- Samsung Electro‑Mechanics

- Taiyo Yuden Co., Ltd.

- 3M Company

- Koike Aronson

- AT&S (Advanced Technology & Systems)

- Unimicron Technology Corp.

- Zhen Ding Technology Holding Limited

- Melexis

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thin‑film dielectric capacitors are the dominant type because they integrate seamlessly within the PCB stack‑up, delivering ultra‑low loop inductance.

|

| By Application |

|

High‑speed digital computing platforms lead this segment as designers demand tighter PDN impedance budgets.

|

| By End User |

|

OEMs drive adoption because they control board architecture decisions and prioritize design‑for‑manufacturability.

|

| By Integration Method |

|

In‑plane embedding during laminate build is emerging as the preferred method because it yields the most consistent dielectric thickness and minimizes parasitic inductance.

|

| By End Market |

|

Automotive electronics are a compelling growth driver due to increasing electric‑vehicle power‑train complexity and stringent reliability standards.

|

Regional Analysis: PCB embedded planar capacitor for PDN impedance reduction Market

North American OEMs prioritize planar capacitor integration to meet aggressive PDN impedance targets in high‑speed computing platforms. Early adoption is facilitated by close partnerships with capacitor suppliers, enabling customization of dielectric materials and thicknesses. This collaborative approach accelerates the rollout of low‑profile packages that support tighter voltage regulation across diverse workloads and improve overall system efficiency.

The supply chain in North America benefits from a mature network of silicon wafer fabs, advanced packaging facilities, and specialized PCB manufacturers. Vertical integration strategies reduce lead times for planar capacitor components, while local logistics infrastructure ensures rapid distribution to data‑center builders. This resilience mitigates global disruptions and sustains steady component availability for end‑users throughout.

Regulatory bodies in the United States and Canada emphasize electromagnetic compatibility and power‑integrity standards that indirectly drive adoption of PCB embedded planar capacitors. Guidelines such as IEC 61000‑4‑2 encourage designers to implement low‑impedance solutions, while regional green‑energy initiatives push for efficient power delivery, creating a favorable policy backdrop for market growth across sectors globally today.

Customers in North America seek capacitors that deliver high capacitance per unit area while maintaining a thin profile to accommodate dense board layouts. The rise of AI accelerators and high‑performance GPUs intensifies the need for precise PDN impedance control, prompting buyers to favor embedded planar solutions that simplify routing and improve thermal performance and reliability.

Europe

Europe presents a diversified landscape for PCB embedded planar capacitor for PDN impedance reduction market, with strong activity in Germany, the United Kingdom, and France. The region’s emphasis on automotive electrification and industrial automation drives demand for compact, high‑efficiency power‑delivery components. European manufacturers benefit from advanced materials research funded by EU programs, fostering innovations in low‑loss dielectrics suitable for planar capacitor architectures. While the market adoption pace is slightly slower than North America, regulatory alignment with the European Union’s RoHS and energy‑efficiency directives encourages early integration of impedance‑optimizing solutions. Collaborative design hubs across the continent enable rapid prototyping, allowing OEMs to address the stringent voltage‑stability requirements of emerging 5G infrastructure and edge‑computing devices.

Asia‑Pacific

Asia‑Pacific is emerging as a high‑growth zone for PCB embedded planar capacitor for PDN impedance reduction, propelled by rapid expansion of consumer electronics manufacturing in China, Taiwan, and South Korea. The intense competition among smartphone and laptop producers creates pressure to shrink form‑factor while maintaining power integrity, making planar capacitor integration attractive. Government initiatives supporting semiconductor self‑sufficiency further accelerate local development of advanced dielectric materials and in‑house packaging capabilities. Japan’s focus on automotive and robotics adds another dimension, where precise PDN control is critical for safety‑critical systems. Although the region faces challenges in standardization, collaborative industry consortia are actively defining design guidelines, enabling faster adoption across diverse application segments.

South America

South America shows nascent but steadily increasing interest in PCB embedded planar capacitor for PDN impedance reduction, led primarily by Brazil’s growing electronics assembly sector. The region’s focus on renewable‑energy integration and electric‑vehicle infrastructure creates a need for efficient power‑distribution solutions on compact PCBs. Local design firms are beginning to experiment with planar capacitor embeddings to meet tighter voltage‑fluctuation tolerances in smart‑grid components. While supply‑chain depth remains limited, partnerships with North American and European suppliers are bridging technology gaps, allowing South American manufacturers to adopt proven architectures without extensive in‑house R&D. This collaborative model is expected to foster incremental market expansion over the next decade.

Middle East & Africa

The Middle East & Africa (MEA) region is gradually recognizing the benefits of PCB embedded planar capacitor for PDN impedance reduction, with Saudi Arabia and the United Arab Emirates investing heavily in data‑center and smart‑city projects. These initiatives demand highly reliable power‑delivery networks, prompting designers to explore embedded planar solutions that minimize parasitic inductance. Local universities are collaborating with global capacitor manufacturers to adapt dielectric formulations suitable for the region’s temperature extremes. Although market penetration remains modest, the combination of government‑backed digital‑transformation programs and increasing private‑sector demand for high‑performance computing is laying the groundwork for broader adoption in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the PCB embedded planar capacitor for PDN impedance reduction Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of PCB embedded planar capacitor for PDN impedance reduction Market?

-> PCB embedded planar capacitor for PDN impedance reduction market is projected to grow from USD 092 billion in 2026 to USD 168 billion by 2034 with a CAGR of 7.9%.

Which key companies operate in PCB embedded planar capacitor for PDN impedance reduction Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...