MARKET INSIGHTS

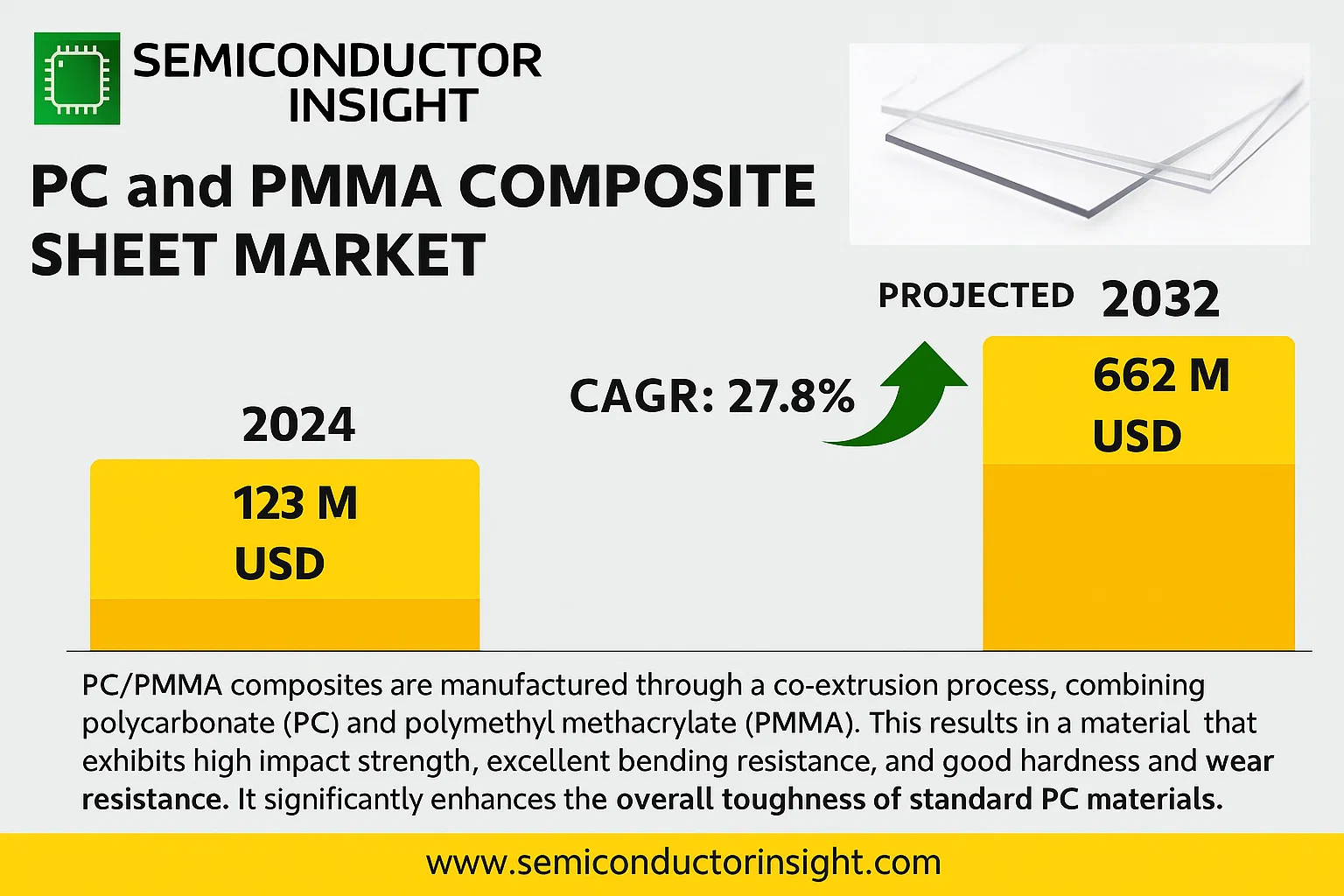

Global PC and PMMA Composite Sheet Market was valued at USD 123 million in 2024 and is projected to reach USD 662 million by 2032, exhibiting a CAGR of 27.8% during the forecast period.

PC/PMMA composites are manufactured through a co-extrusion process, combining polycarbonate (PC) and polymethyl methacrylate (PMMA). This results in a material that exhibits high impact strength, excellent bending resistance, and good hardness and wear resistance. It significantly enhances the overall toughness of standard PC materials.

The market is experiencing rapid growth due to several factors, including the increasing demand for lightweight and durable materials in consumer electronics, particularly for smartphone and tablet casings. The automotive industry’s shift towards lightweight components to improve fuel efficiency is another significant driver. Additionally, the expansion of the construction sector, where these sheets are used for glazing and decorative panels, contributes to market expansion.

Key players are focusing on innovation and strategic partnerships. For instance, in January 2024, Mitsubishi Gas Chemical and Teijin Limited announced a collaboration to develop next-generation composite sheets with enhanced flame retardancy, targeting the electric vehicle interior market.

MARKET DRIVERS

Rising Demand from Electronics and Automotive Sectors

The global PC and PMMA composite sheet market is experiencing significant growth, primarily driven by their increasing adoption in the electronics and automotive industries. These materials offer a superior combination of high impact strength, excellent optical clarity, and lightweight properties, making them ideal for applications such as smartphone and tablet casings, automotive glazing, and interior components. The trend towards lightweighting in automotive design to improve fuel efficiency and the growing consumer electronics market are key factors propelling demand.

Superior Performance Characteristics Over Traditional Materials

PC/PMMA composites outperform many traditional materials like glass and standard plastics. They provide excellent weatherability, UV resistance, and surface hardness, which are critical for outdoor applications and products requiring long-term durability. This performance advantage is leading to material substitution across various end-use industries, further accelerating market growth.

➤ The market for PC/PMMA composite sheets is projected to grow at a CAGR of approximately 6.5% over the next five years, fueled by these converging industrial trends.

Additionally, advancements in co-extrusion and lamination technologies have improved the production efficiency and quality of these composite sheets, enabling manufacturers to meet the precise specifications required by high-tech applications. This technological progress is a fundamental driver for market expansion.

MARKET CHALLENGES

Fluctuating Raw Material Prices

The market faces considerable challenges due to the volatility in the prices of raw materials, particularly the petrochemical derivatives used to produce polycarbonate (PC) and polymethyl methacrylate (PMMA). Price instability can squeeze profit margins for manufacturers and create pricing unpredictability for end-users, potentially hindering market growth.

Other Challenges

Technical Processing and Recycling Complexities

Processing PC/PMMA composites requires specialized equipment and precise control over temperature and pressure, posing a barrier for new entrants. Furthermore, the recycling of these multi-material composites is complex and not yet widely established, raising environmental concerns and increasing end-of-life management costs.

Intense Competition from Alternative Materials

The market faces strong competition from other high-performance plastics and glass composites, which continue to improve their properties and cost-effectiveness. This competition pressures manufacturers of PC/PMMA sheets to continuously innovate and justify their value proposition.

MARKET RESTRAINTS

High Initial Production and Material Costs

The relatively high cost of PC and PMMA resins compared to commodity plastics like polypropylene or PVC acts as a significant restraint on market growth. The advanced manufacturing processes for creating high-quality composite sheets also contribute to a higher final product cost, which can limit adoption in price-sensitive market segments.

Stringent Regulatory and Environmental Standards

Increasingly stringent global regulations concerning chemical emissions, recyclability, and the use of certain additives (like BPA in polycarbonate) pose challenges for manufacturers. Compliance necessitates ongoing research and development investments, which can restrain market expansion, particularly for smaller players.

MARKET OPPORTUNITIES

Expansion in Sustainable and Bio-based Alternatives

There is a significant opportunity for growth in the development and commercialization of bio-based or recycled-content PC/PMMA composite sheets. As sustainability becomes a core focus for brands and consumers, offering eco-friendly variants can open up new markets and applications, aligning with circular economy principles.

Growth in Emerging Economies and New Applications

The rapid industrialization and urbanization in emerging economies across Asia-Pacific and Latin America present substantial growth opportunities. The rising middle class in these regions drives demand for consumer electronics, automobiles, and modern architectural materials, all key application areas for PC/PMMA sheets. Furthermore, new applications in medical devices and renewable energy sectors, such as protective covers for solar panels, are emerging as promising frontiers for market expansion.

PC and PMMA Composite Sheet Market Trends

Explosive Market Growth Driven by Consumer Electronics

The global PC and PMMA Composite Sheet market is in a phase of exceptionally strong expansion, with a valuation of $123 million in 2024 that is projected to surge to US$ 662 million by 2032. This represents a remarkable Compound Annual Growth Rate (CAGR) of 27.8% during the forecast period. The primary catalyst for this growth is the escalating demand from the consumer electronics sector, where these sheets are favored for device back covers and other components due to their superior material properties. The co-extruded sheet combines the high impact strength and bending resistance of Polycarbonate (PC) with the good hardness and wear resistance of Polymethyl Methacrylate (PMMA), making it an ideal material for modern, durable electronic devices.

Other Trends

High Market Concentration and Regional Dominance

The global industry for PC and PMMA composite sheets is characterized by a high level of concentration. The top two players, Sichuan Longhua Film and Teijin, collectively hold a dominant market share of approximately 50%. Geographically, production is led by China, which accounts for over 40% of the global output, followed by Japan. The Asia-Pacific region is unequivocally the leading consumption market, commanding about 92% of the global share, fueled by its massive electronics manufacturing base. Europe and North America are smaller markets, holding shares of 5% and 3%, respectively.

Product Segmentation and Application Diversification

The market is segmented by product type, primarily into two-layer and three-layer sheets, catering to different application requirements. In terms of application, the consumer electronics segment leads usage, followed by the automotive industry and other niche markets. The material’s ability to enhance the overall toughness of PC-based components makes it increasingly attractive for automotive interiors and exteriors, signaling potential for diversification beyond its core electronics application.

Innovation and Competitive Landscape

Key players, including Mitsubishi Gas Chemical, Wavelock Advanced Technology, and Plazit-Polygal Group, are actively engaged in innovation and strategic development to strengthen their market positions. The competitive dynamics are shaped by factors such as price, sales volume, and technological advancements in co-extrusion processes. The industry’s future trajectory will be influenced by evolving material science, manufacturing capabilities, and the continued global demand for high-performance composite materials in key end-use sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Characterized by High Concentration and Regional Dominance

The global PC and PMMA composite sheet market is highly concentrated, with the top two players, Sichuan Longhua Film and Teijin, collectively accounting for approximately 50% of the market share. This dominance is underpinned by their extensive production capabilities, established supply chains, and strong focus on research and development to enhance product properties such as high impact strength, bending resistance, and superior hardness. China stands as the largest production base globally, contributing over 40% of the market’s output, with Japan being another significant hub. The Asia-Pacific region is the unequivocal leader in consumption, accounting for about 92% of the global market, driven by its massive consumer electronics and automotive manufacturing sectors.

Beyond the top tier, the market includes a roster of significant niche players and regional suppliers that contribute to the global supply chain. Companies like Mitsubishi Gas Chemical and Wavelock Advanced Technology are key participants with strong technological expertise. Other notable manufacturers such as Takiron, Daoming Optical, and Foshan Dafu New Material cater to specific regional demands and application segments, including high-precision components for electronics and automotive interiors. The competitive dynamics are further shaped by companies focusing on product innovation, particularly in developing multi-layer sheets (two-layer and three-layer) to meet the evolving requirements for durability and aesthetics in end-use industries.

List of Key PC and PMMA Composite Sheet Companies Profiled

- Sichuan Longhua Film

- Teijin Limited

- Mitsubishi Gas Chemical Company, Inc.

- Wavelock Advanced Technology Co., Ltd.

- Takiron Co., Ltd.

- Daoming Optical & Chemical Co., Ltd.

- Foshan Dafu New Material Co., Ltd.

- Shen Zhen CDL Precision Technology Co., Ltd.

- Suzhou OMAY Optical Materials Co., Ltd.

- Sunwoda Electronic Co., Ltd.

- Plazit-Polygal Group

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Two-layer composite sheets are the leading segment due to their balance of performance characteristics and cost-effectiveness, making them the preferred choice for a wide array of standard applications. This structural design provides sufficient surface hardness from the PMMA layer combined with the excellent impact resistance of the PC substrate, meeting the core requirements for many consumer products without the added complexity of a third layer. The manufacturing process for two-layer sheets is well-established and efficient, which contributes to their widespread availability and competitive pricing, thereby reinforcing their dominant position in the market. |

| By Application |

|

Consumer Electronics represents the dominant application segment, driven by the material’s unique combination of optical clarity, scratch resistance, and high impact strength which are essential for smartphone covers, tablet backs, and various device housings. The relentless innovation and high-volume production cycles within the electronics industry create sustained and substantial demand. Furthermore, the aesthetic appeal and durability provided by PC/PMMA composites align perfectly with the requirements for modern, sleek, and durable consumer gadgets, ensuring its continued leadership as emerging applications in wearables and other smart devices further expand the market potential. |

| By End User |

|

Electronics OEMs are the primary end users, leveraging PC/PMMA composite sheets for their critical role in manufacturing high-volume consumer goods. These original equipment manufacturers value the material for its ability to enhance product durability while maintaining a premium look and feel, which is a key differentiator in competitive markets. The close collaboration between material suppliers and major electronics brands drives continuous material innovation tailored to specific design and performance needs, securing the position of electronics OEMs as the most influential segment shaping product development and consumption trends within the industry. |

| By Material Property Dominance |

|

Balanced Performance materials are the leading category, as the core value proposition of PC/PMMA sheets lies in their synergistic combination of properties rather than a single extreme characteristic. This balance between the polycarbonate’s exceptional toughness and the polymethyl methacrylate’s excellent surface hardness and optical clarity creates a versatile material suitable for a multitude of applications where both durability and aesthetic quality are non-negotiable. Market demand strongly favors this balanced profile because it eliminates the need for compromises in product design, allowing manufacturers to achieve a high-quality finish that can withstand everyday wear and tear, which is paramount for mass-market consumer goods. |

| By Manufacturing Process Sophistication |

|

Standard Co-extrusion is the dominant process, forming the backbone of the industry due to its reliability, scalability, and cost-efficiency for producing the widely used two-layer sheets. This well-optimized process allows for high-volume production with consistent quality, which is essential to meet the massive demands of key application sectors like consumer electronics. While advanced processes exist for specialized, high-performance grades, the market’s growth is primarily fueled by the accessibility and economic viability of standard co-extrusion, making it the most significant segment in terms of production volume and market penetration across global supply chains. |

Regional Analysis: PC and PMMA Composite Sheet Market

Asia-Pacific

The region’s dominance is heavily driven by its status as the global epicenter for electronics production. High demand for PC/PMMA sheets for device housings, display covers, and touch panels from smartphone, tablet, and television manufacturers creates a massive and consistent market. Local manufacturers benefit from proximity to these OEMs, enabling just-in-time delivery and collaborative development of new material specifications tailored to evolving product designs.

The booming automotive sector in countries like China, India, and Thailand is a key growth driver. There is increasing adoption of PC/PMMA composite sheets for interior components, instrument panels, and lightweight exterior parts. This trend is fueled by the push for vehicle weight reduction for improved fuel efficiency and the desire for high-gloss, aesthetically pleasing surfaces that enhance the cabin experience.

Asia-Pacific leads in developing and applying advanced co-extrusion and lamination technologies for producing high-performance PC/PMMA sheets. Continuous innovation focuses on improving properties like anti-fingerprint coatings, enhanced UV resistance for outdoor applications, and better optical characteristics. This technical expertise allows regional producers to offer sophisticated products that meet stringent international quality standards.

Rapid infrastructure development and urbanization across the region are fueling demand in the construction sector. PC/PMMA sheets are widely used for sound barriers, skylights, canopy roofs, and decorative interior cladding due to their durability, light weight, and design flexibility. Government initiatives for smart city development further amplify the need for modern, high-performance building materials.

North America

The North American market for PC and PMMA composite sheets is characterized by mature, high-value applications and a strong emphasis on quality and performance specifications. The region’s well-established automotive industry is a significant consumer, particularly for premium interior trim components and specialized lighting applications where optical clarity and scratch resistance are paramount. The construction sector also shows steady demand, especially for high-impact glazing in commercial buildings and specialized architectural panels. A key dynamic is the stringent regulatory environment, which drives innovation in flame-retardant and environmentally sustainable composite formulations. While manufacturing costs are generally higher than in Asia-Pacific, North American producers compete through technological superiority, customization, and supplying niche markets that demand the highest material standards.

Europe

Europe maintains a strong position in the PC and PMMA composite sheet market, driven by its advanced automotive design centers and a construction sector with a focus on energy efficiency and modern aesthetics. The automotive industry, particularly in Germany and France, demands high-quality sheets for sophisticated interior designs and innovative lighting solutions. The region’s strict environmental regulations and sustainability goals are shaping market dynamics, prompting increased use of recycled content in composites and development of bio-based alternatives. European manufacturers are leaders in producing specialty sheets for high-end applications, including museum displays, premium retail fixtures, and architectural projects that require specific optical properties and long-term durability, often commanding a premium price in the global market.

South America

The South American market for PC and PMMA composite sheets is emerging, with growth primarily linked to the construction and advertising sectors. Economic fluctuations can impact the pace of adoption, but there is a consistent demand for durable and cost-effective materials for applications like signage, partitions, and basic glazing. The automotive industry is smaller but present, with local assembly plants creating some demand for interior components. The market is largely served by imports, though local production capabilities are developing in larger economies like Brazil. Growth is potential-driven by infrastructure development projects and the gradual modernization of retail and commercial spaces across the region.

Middle East & Africa

The Middle East & Africa region presents a market with distinct opportunities, particularly centered on large-scale construction and infrastructure projects. In the Gulf Cooperation Council (GCC) countries, the demand is driven by the use of PC/PMMA sheets in prestigious architectural projects, shopping malls, and canopy structures where durability against harsh sunlight and aesthetic appeal are crucial. The African market is more fragmented and nascent, with growth potential in urban development and the gradual expansion of the consumer electronics and automotive sectors. The market dynamics are influenced by import dependency and a focus on products that offer a balance between cost and performance for large-volume applications.

Report Scope

This market research report provides a comprehensive analysis of the PC and PMMA Composite Sheet Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of PC and PMMA Composite Sheet Market?

-> PC and PMMA Composite Sheet Market was valued at USD 123 million in 2024 and is projected to reach USD 662 million by 2032, exhibiting a CAGR of 27.8% during the forecast period.

Which key companies operate in PC and PMMA Composite Sheet Market?

-> Key players include Sichuan Longhua Film, Teijin, Mitsubishi Gas Chemical, Wavelock Advanced Technology, and Shen Zhen CDL Precision Technology, among others. The top two players hold about 50% market share.

What are the key growth drivers?

-> Key growth drivers include the material’s high impact strength, bending resistance, good hardness and wear resistance, and its ability to improve the overall toughness of PC materials.

Which region dominates the market?

-> Asia-Pacific is the largest consumption market, accounting for about 92% of the global share, followed by Europe (5%) and North America (3%).

What are the emerging trends?

-> Emerging trends include innovations in co-extrusion technology for two-layer and three-layer sheets and increasing applications in the consumer electronics and automotive sectors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...