MARKET INSIGHTS

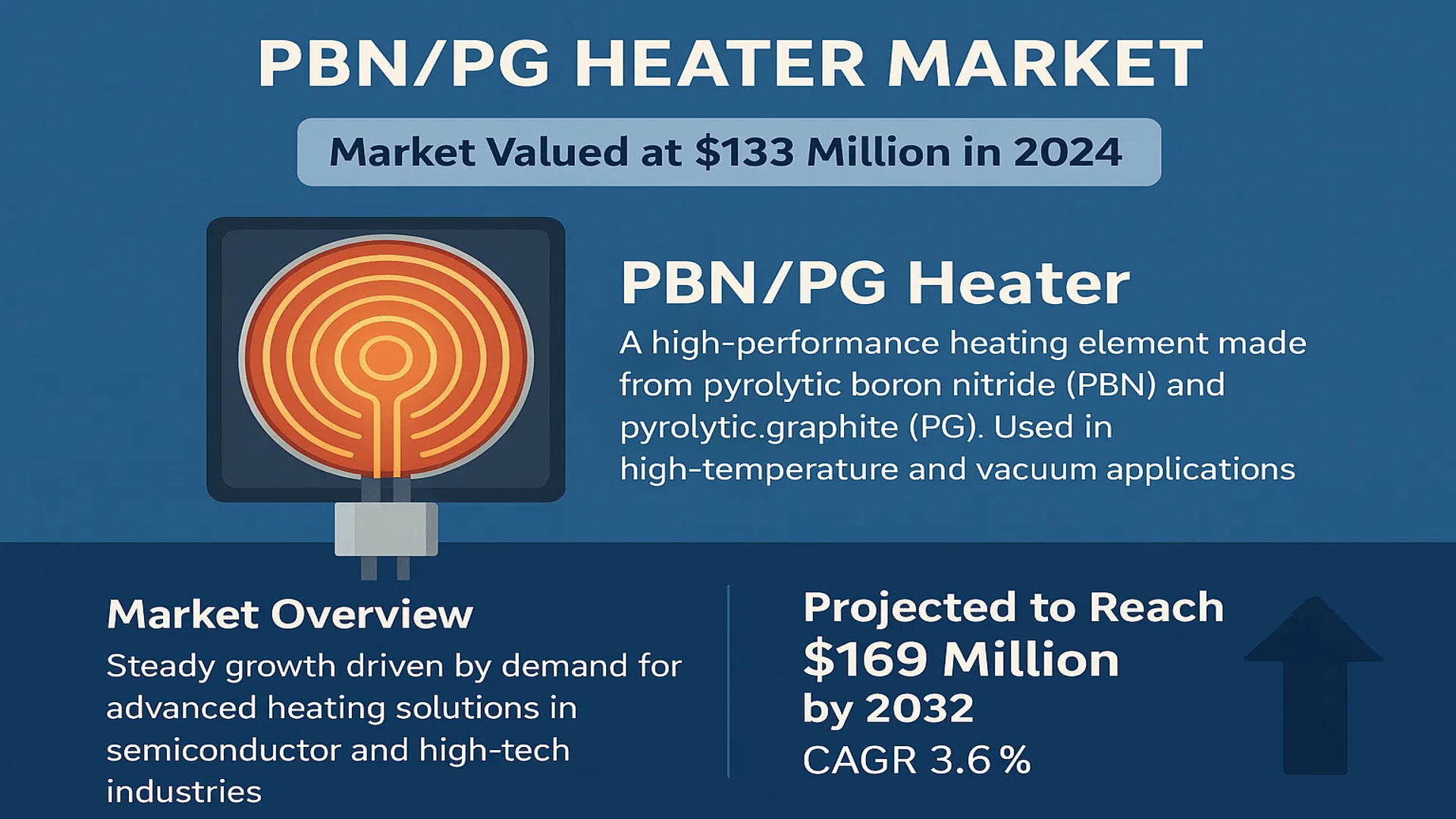

The global PBN/PG Heater Market was valued at 133 million in 2024 and is projected to reach US$ 169 million by 2032, at a CAGR of 3.6% during the forecast period.

A PBN/PG Heater is a high-performance heating element made from pyrolytic boron nitride (PBN) and pyrolytic graphite (PG). These materials offer exceptional thermal stability, high purity, and excellent electrical conductivity, making them ideal for high-temperature and vacuum applications. They are widely used in industries such as electronics, semiconductors, optics, and aerospace.

The market is witnessing steady growth driven by increasing demand for advanced heating solutions in semiconductor manufacturing and other high-tech applications. While the U.S. remains a key market, China is rapidly catching up due to its expanding semiconductor industry. However, challenges such as high production costs and material limitations may hinder growth in certain segments. Key players like Advanced Ceramic Materials, Shin-Etsu MicroSi, and Momentive Technologies dominate the market with innovative product offerings and strategic partnerships.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Semiconductor and Electronics Industry to Fuel PBN/PG Heater Demand

The global semiconductor industry continues its rapid expansion, with production volumes expected to grow at a steady pace through 2032. PBN/PG heaters play a critical role in semiconductor manufacturing processes, particularly in molecular beam epitaxy (MBE) systems and other high-temperature applications. These advanced heating elements offer superior thermal conductivity compared to traditional materials, enabling more precise temperature control during wafer processing. The accelerating adoption of 5G technology, IoT devices, and AI hardware is creating sustained demand for semiconductor components, indirectly driving growth in the PBN/PG heater market. Recent advances in compound semiconductor manufacturing have particularly increased the need for high-performance heating solutions that can maintain stability in ultra-high vacuum environments.

Growing Aerospace Industry Demanding High-Performance Materials

The aerospace sector presents another significant growth opportunity for PBN/PG heater manufacturers. These materials are increasingly used in satellite components, space exploration equipment, and advanced avionics systems where reliability under extreme conditions is paramount. The global commercial aircraft fleet is projected to expand substantially in the coming decade, with increasing orders for next-generation aircraft that incorporate more advanced electronic systems. PBN/PG heaters’ ability to maintain consistent performance across wide temperature ranges (-200°C to 1800°C) makes them ideal for aerospace applications where thermal cycling resistance is critical. Furthermore, the space industry’s current growth phase, marked by increased private sector participation and smaller satellite deployments, creates new application areas for these specialized heating elements.

Advancements in Optical Technologies Driving Market Expansion

Optical manufacturing represents another key growth area for PBN/PG heater applications. The development of advanced photonic devices, fiber optics, and laser systems requires precise heating elements that can operate cleanly without contaminating sensitive optical surfaces. PBN/PG heaters are particularly valuable for crystal growth processes used in optical component manufacturing due to their chemical inertness and thermal stability. The optical components market is experiencing robust growth as 5G networks expand and data center infrastructure upgrades continue globally. Investments in quantum computing research and development are also creating specialized demand for ultra-pure heating elements in vacuum deposition systems, further supporting market growth for PBN/PG solutions that can meet these stringent requirements.

MARKET RESTRAINTS

High Manufacturing Costs Limiting Market Penetration

While PBN/PG heaters offer superior performance characteristics, their high production costs create significant barriers to broader market adoption. The specialized chemical vapor deposition (CVD) processes required for manufacturing pyrolytic boron nitride and graphite involve sophisticated equipment and rigorous quality control measures, contributing to elevated production expenses. These costs are ultimately passed on to end-users, making PBN/PG heaters considerably more expensive than conventional heating element alternatives. In price-sensitive market segments, this cost differential often leads potential customers to opt for lower-performance solutions despite the technical advantages offered by PBN/PG technology.

Limited Raw Material Availability Creating Supply Chain Challenges

The production of high-quality PBN/PG heaters depends on access to specialized precursor materials that meet strict purity requirements. Certain key raw materials face supply constraints due to limited global production capacity and geopolitical factors affecting mineral supply chains. The boron nitride market in particular is characterized by relatively few suppliers capable of providing the material grades required for PBN heater manufacturing. These supply chain limitations create potential vulnerabilities for producers and may impact their ability to respond quickly to spikes in demand. Furthermore, the specialized nature of these materials makes it difficult for manufacturers to rapidly source alternative supplies when disruptions occur.

Technical Complexity Restraining Broader Adoption

The advanced nature of PBN/PG heater technology presents adoption challenges in some industrial sectors. While these heating elements offer clear advantages for specialized applications, their integration into existing systems often requires engineering expertise that may not be readily available across all potential market segments. The need for precise power control systems and specialized mounting configurations can add complexity and cost to equipment upgrades or new installations. Some industrial users hesitate to transition to PBN/PG solutions due to concerns about maintaining adequate technical support and the availability of replacement components, particularly in regions where the technology is less established.

MARKET OPPORTUNITIES

Emerging Applications in Quantum Technology and Advanced Research

The rapidly developing field of quantum technology presents significant growth opportunities for PBN/PG heater manufacturers. Quantum computing research facilities and emerging commercial quantum devices often require ultra-stable thermal environments that can only be achieved with high-performance heating elements. The unique properties of PBN/PG materials make them particularly suitable for these applications, where even minor thermal fluctuations or contaminants can impact system performance. National research initiatives and private sector investments in quantum technologies are creating new demand channels for specialized heating solutions that can operate with exceptional precision in vacuum environments.

Expansion in Medical Device Manufacturing

The medical device sector represents another promising growth area for PBN/PG heater applications. Advanced diagnostic equipment and minimally invasive surgical tools increasingly incorporate sophisticated electronic components that require precision heating during manufacturing. The biocompatibility and cleanliness advantages of PBN/PG materials make them particularly attractive for medical applications where contamination risks must be minimized. As medical device manufacturers continue to push the boundaries of miniaturization and performance, the need for specialized heating solutions that can support these advancements is expected to increase significantly.

Growing Focus on Sustainable Manufacturing Processes

Increasing emphasis on sustainable industrial practices is creating opportunities for PBN/PG heater technology in various manufacturing environments. These heating elements often outperform conventional alternatives in energy efficiency and longevity, potentially reducing overall energy consumption and material waste in industrial processes. The ability of PBN/PG heaters to maintain stable performance over extended periods between replacements aligns well with sustainability goals across multiple industries. As environmental regulations tighten and manufacturers seek to improve their operational sustainability metrics, the value proposition of high-performance, long-lasting heating solutions becomes increasingly compelling.

MARKET CHALLENGES

Intense Competition from Alternative Technologies

The PBN/PG heater market faces ongoing competitive pressure from conventional heating element technologies that continue to improve in performance and reliability. Manufacturers of silicon carbide, molybdenum disilicide, and other ceramic heating elements are making significant advancements in product durability and thermal characteristics. While these alternatives may not match the full performance spectrum of PBN/PG solutions, their lower price points and established supply chains make them attractive options for cost-conscious buyers. This competitive landscape requires PBN/PG heater manufacturers to continually innovate and demonstrate the unique value of their products to justify the premium pricing structure.

Rapid Technological Changes in End-Use Industries

The dynamic nature of key customer industries presents another significant challenge for PBN/PG heater manufacturers. Semiconductor fabrication techniques, aerospace materials, and optical technologies all evolve rapidly, requiring constant adaptation from component suppliers. Keeping pace with these changes demands substantial investments in research and development to ensure that PBN/PG heater designs remain compatible with next-generation manufacturing processes. The need to anticipate future technical requirements while maintaining current production capabilities creates a challenging balancing act for industry participants.

Geopolitical Factors Impacting Global Supply Chains

Geopolitical tensions and trade policy shifts create uncertainties that impact the PBN/PG heater market’s global operations. Restrictions on technology transfers, export controls on advanced materials, and regional trade disputes can disrupt established supply chains and customer relationships. The specialized nature of PBN/PG heater production means that local supply chain disruptions in one region may not be easily mitigated by sourcing from alternative locations. Manufacturers must navigate these challenges while maintaining compliance with evolving international trade regulations and regional market requirements.

PBN/PG HEATER MARKET TRENDS

Demand for High-Temperature Stability Drives PBN/PG Heater Adoption

The growing need for materials with exceptional thermal and electrical properties is significantly fueling the demand for pyrolytic boron nitride (PBN) and pyrolytic graphite (PG) heaters. These advanced heating solutions are crucial for high-temperature applications due to their superior thermal conductivity, low outgassing, and chemical inertness. The market is witnessing increased adoption in semiconductor manufacturing, where precision heating under extreme conditions is essential. Recent advancements in thin-film deposition and epitaxial growth technologies have further amplified the utilization of PBN/PG heaters. Furthermore, their ability to maintain stability in ultra-high vacuum environments makes them indispensable for aerospace and optical coating applications.

Other Trends

Reshaping Semiconductor Fabrication Processes

The semiconductor industry is undergoing a transformation with the increasing complexity of chip manufacturing. PBN/PG heaters are playing a pivotal role in chemical vapor deposition (CVD) and molecular beam epitaxy (MBE) systems, enabling uniform heating essential for advanced node production. The shift toward smaller, more efficient semiconductor devices has necessitated higher process temperatures, which conventional heaters struggle to sustain without degradation. In contrast, PBN/PG heaters exhibit minimal thermal expansion and extended lifespan, reducing downtime and operational costs.

Emerging Opportunities in Aerospace and Optics

The aerospace sector is leveraging PBN/PG heaters for applications requiring lightweight, corrosion-resistant, and high-temperature-resistant components. These heaters are extensively used in thermal management systems for satellites, spacecraft, and precision optical instruments. Additionally, the optics industry benefits from their use in coating processes where contamination-free heating is critical for achieving high-quality optical layers. The increasing investment in space exploration and defense technologies is expected to further propel the demand, supported by advancements in ceramic-based heating technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Expansion Drive Competition in the PBN/PG Heater Market

The global PBN/PG Heater market exhibits a competitive yet dynamic landscape with a mix of established players and emerging companies vying for market share. Advanced Ceramic Materials leads the market with its comprehensive portfolio of high-temperature resistant heating solutions, supported by a strong presence across North America and Asia-Pacific regions. The company’s expertise in pyrolytic boron nitride applications gives it a competitive edge in semiconductor and aerospace applications.

Shin-Etsu MicroSi and Momentive Technologies have also captured significant market share, accounting for approximately 15% and 12% of global revenues respectively in 2024. Their growth stems from continuous R&D investments in advanced heater designs, particularly for ultra-high vacuum environments where material purity is critical. Furthermore, both companies have expanded their production capacities in the past two years to meet growing demand from the electronics sector.

The market is seeing increased competition in the Asia-Pacific region, where Beijing Boyu Semiconductor Vessel Craftwork Technology and Shandong Guojing New Materials have strengthened their positions through government collaborations and local manufacturing advantages. These companies are challenging traditional Western manufacturers by offering cost-competitive solutions without compromising on thermal performance specifications.

Recent developments indicate a trend towards strategic partnerships, with Morgan Advanced Materials announcing a joint venture with a European aerospace component manufacturer in Q1 2024. Similarly, CVT GmbH has been focusing on proprietary coating technologies to enhance heater lifespan in corrosive environments, demonstrating how specialized solutions create differentiation in this competitive space.

List of Key PBN/PG Heater Manufacturers

- Advanced Ceramic Materials (U.S.)

- Shin-Etsu MicroSi (Japan)

- Heeger Materials (U.S.)

- ATT Advanced Elemental Materials (Germany)

- Nextgen Advanced Materials (South Korea)

- Momentive Technologies (U.S.)

- Shin-Etsu Chemical (Japan)

- Thermic Edge (U.K.)

- CVT GmbH (Germany)

- Beijing Boyu Semiconductor Vessel Craftwork Technology (China)

- Shandong Guojing New Materials (China)

- Morgan Advanced Materials (U.K.)

Segment Analysis:

By Type

Resistance Heating Segment Leads Owing to High Efficiency in Semiconductor Manufacturing

The market is segmented based on type into:

- Resistance Heating

- Subtypes: Graphite-based, Ceramic-based, and others

- Induction Heating

By Application

Electronics and Semiconductors Segment Dominates Due to Rising Demand for High-Purity Components

The market is segmented based on application into:

- Electronics and Semiconductors

- Optics

- Aerospace

By End-User

Industrial Manufacturing Leads as PBN/PG Heaters Are Critical for High-Temperature Processes

The market is segmented based on end-user into:

- Industrial Manufacturing

- Research Institutions

- Defense and Aerospace

By Material

Pyrolytic Boron Nitride Segment Gains Traction for Thermal Stability

The market is segmented based on material into:

- Pyrolytic Boron Nitride (PBN)

- Pyrolytic Graphite (PG)

Regional Analysis: PBN/PG Heater Market

Asia-Pacific

The Asia-Pacific region dominates the global PBN/PG Heater market, accounting for the largest share in 2024 due to rapid industrialization and extensive semiconductor manufacturing in countries like China, Japan, and South Korea. China, in particular, is experiencing significant growth in demand for high-purity heating solutions, driven by its expanding electronics and semiconductor industry. Key players such as Shin-Etsu Chemical and Beijing Boyu Semiconductor Vessel Craftwork Technology have a strong foothold here, leveraging local supply chains. While cost sensitivity remains a challenge, increasing investments in R&D and the adoption of advanced materials for aerospace and optical applications are accelerating market expansion.

North America

North America holds a prominent position in the PBN/PG Heater market, supported by its thriving aerospace and semiconductor sectors. The U.S. leads the region, with companies like Advanced Ceramic Materials and Momentive Technologies driving innovation in high-temperature applications. Stringent quality standards and a focus on cutting-edge technologies, such as resistance heating for semiconductor fabrication, contribute to steady demand. However, the high cost of PBN/PG materials and competition from alternative heating solutions like ceramic heaters pose challenges to widespread adoption.

Europe

Europe’s market is characterized by steady growth, primarily due to the region’s emphasis on advanced manufacturing and aerospace applications. Germany and France are key markets, where companies like CVT GmbH and ATT Advanced Elemental Materials cater to industrial and research needs. Strict environmental and performance regulations under EU directives encourage the use of PBN/PG heaters for their thermal efficiency and low contamination risks. Nonetheless, market expansion is tempered by high production costs and the preference for localized, small-scale production units.

South America

South America represents a smaller but emerging market, with Brazil leading in semiconductor and aerospace applications. The region’s growth is constrained by limited industrial infrastructure and reliance on imported PBN/PG heating solutions. Though economic instability affects investment, gradual advancements in Brazil’s electronics sector and Argentina’s research institutes create niche opportunities for suppliers. Local manufacturers face hurdles in scaling production due to high material costs and competition from established global players.

Middle East & Africa

The Middle East & Africa region is in the early stages of PBN/PG heater adoption, with Israel and Saudi Arabia emerging as potential growth markets. Demand is fueled by increasing investments in semiconductor manufacturing and advanced optics. However, limited technical expertise and reliance on imports slow market penetration. Long-term opportunities exist in aerospace and defense applications, but progress depends on local industrial development and partnerships with global manufacturers.

Report Scope

This market research report provides a comprehensive analysis of the global PBN/PG Heater market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global PBN/PG Heater market was valued at USD 133 million in 2024 and is projected to reach USD 169 million by 2032, growing at a CAGR of 3.6%.

- Segmentation Analysis: Detailed breakdown by product type (Resistance Heating, Induction Heating), application (Electronics and Semiconductors, Optics, Aerospace), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis. The U.S. and China are key markets driving growth.

- Competitive Landscape: Profiles of leading market participants including Advanced Ceramic Materials, Shin-Etsu MicroSi, Heeger Materials, and others, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of material science advancements in pyrolytic boron nitride and graphite, high-temperature applications, and integration with semiconductor manufacturing processes.

- Market Drivers & Restraints: Evaluation of factors including semiconductor industry growth, demand for high-purity heating solutions, alongside challenges like material costs and supply chain complexities.

- Stakeholder Analysis: Strategic insights for material suppliers, component manufacturers, OEMs, and investors regarding market opportunities and competitive positioning.

The report employs rigorous primary and secondary research methodologies, including expert interviews and verified market data analysis, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global PBN/PG Heater Market?

-> PBN/PG Heater Market was valued at 133 million in 2024 and is projected to reach US$ 169 million by 2032, at a CAGR of 3.6% during the forecast period.

Which key companies operate in Global PBN/PG Heater Market?

-> Key players include Advanced Ceramic Materials, Shin-Etsu MicroSi, Heeger Materials, ATT Advanced Elemental Materials, and Momentive Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of semiconductor manufacturing, demand for high-temperature vacuum applications, and advancements in material science.

Which region dominates the market?

-> Asia-Pacific leads in market share, driven by semiconductor industry growth, while North America remains strong in R&D and specialized applications.

What are the emerging trends?

-> Emerging trends include development of ultra-high purity heating solutions, integration with advanced semiconductor processes, and miniaturization of heating elements.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...