Market Insights

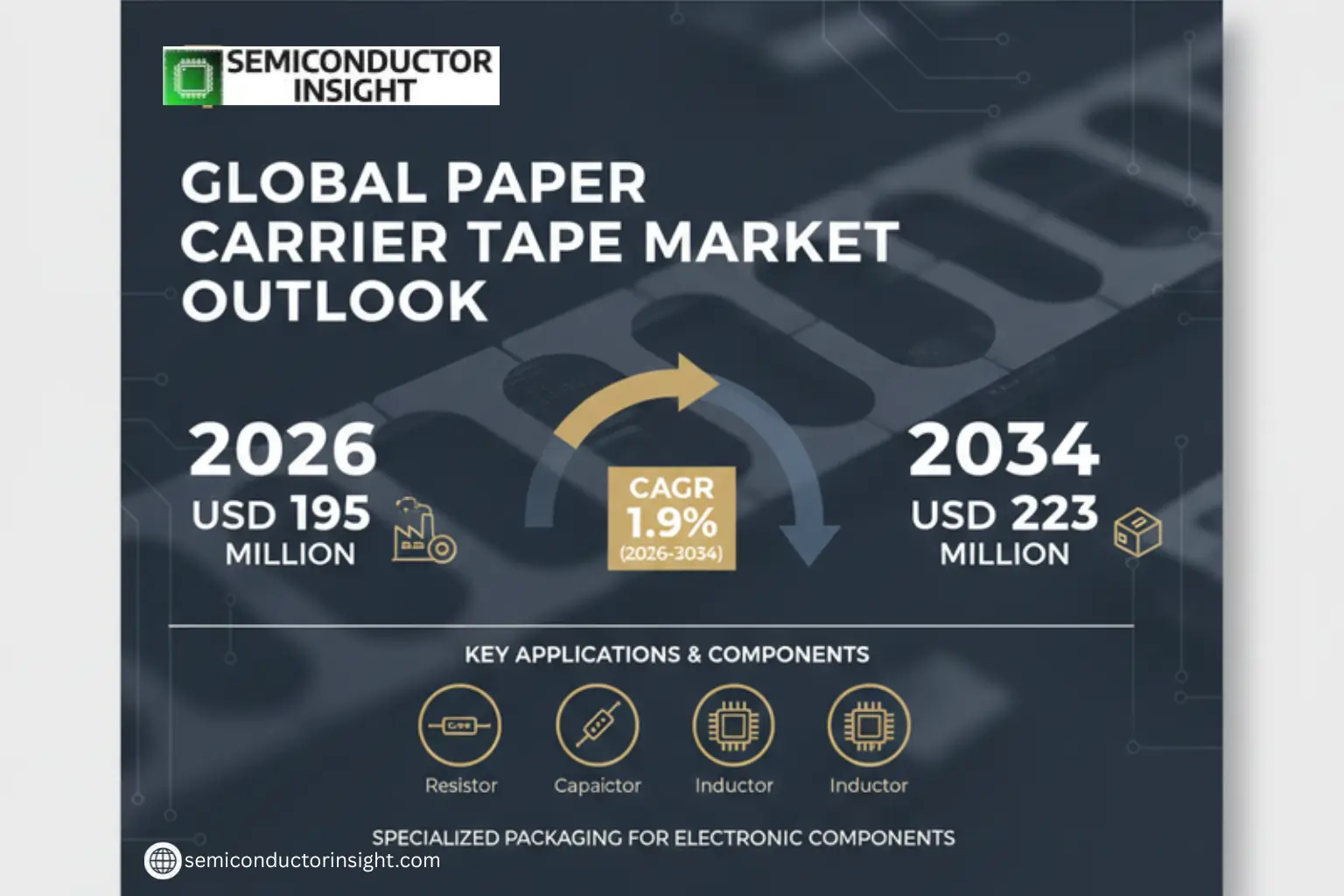

Global Paper Carrier Tape Market was valued at USD 195 million in 2026 and is projected to reach USD 223 million by 2034, exhibiting a CAGR of 1.9% during the forecast period.

Paper carrier tape is a specialized packaging material used for transporting and protecting electronic components such as resistors, capacitors, and inductors. Manufactured from electronic-grade specialty paper, it undergoes processes like slitting, coating, and die punching to create a multilayer composite structure with precise cavity formations. The tape features sprocket holes for automated handling while ensuring moisture resistance and cushioning performance for fragile components.

The market growth is driven by increasing demand for cost-effective component packaging in consumer electronics manufacturing. While plastic alternatives exist, paper carrier tapes maintain dominance in mid-to-low-end applications due to their lightweight properties and competitive pricing. In 2026, global production reached 29,074 million meters with an average selling price of USD 7.33 per kilometer. Key manufacturers are focusing on process improvements to reduce dust generation and enhance punching precision for smaller components.

MARKET DRIVERS

Growing Demand for Eco-Friendly Packaging Solutions

Paper Carrier Tape Market is witnessing significant growth due to the rising demand for sustainable packaging in the electronics industry. With over 65% of manufacturers shifting toward biodegradable materials, paper-based carrier tapes offer an environmentally responsible alternative to plastic counterparts.

Expansion of Semiconductor Manufacturing

Global semiconductor production is projected to increase by 8.3% annually, directly driving demand for Paper Carrier Tape Market products. These tapes provide optimal protection for sensitive components during transportation and handling.

Additionally, stringent regulations on single-use plastics across multiple countries are accelerating adoption rates in the Paper Carrier Tape Market.

MARKET CHALLENGES

High Initial Conversion Costs

Shifting from traditional plastic carrier tapes to paper-based solutions requires substantial capital investment in new machinery and process adjustments, creating a barrier for small-scale manufacturers in the Paper Carrier Tape Market.

Other Challenges

Moisture Sensitivity

Paper carrier tapes exhibit lower resistance to humidity compared to plastic variants, requiring additional protective measures in certain climates.

MARKET RESTRAINTS

Limited High-Temperature Applications

Paper Carrier Tape Market faces constraints in high-temperature manufacturing environments where traditional materials remain preferred. Paper tapes typically have a maximum operating temperature of 120°C, restricting certain industrial applications.

MARKET OPPORTUNITIES

Automotive Electronics Sector Growth

The expanding automotive electronics market, valued at USD 382 billion in 2023, presents significant opportunities for Paper Carrier Tape Market players. The need for component protection in electric vehicle manufacturing is driving adoption of specialized paper carrier solutions.

Customization and Value-Added Services

Manufacturers offering printed or branded Paper Carrier Tapes with enhanced technical specifications are gaining market share by addressing specific customer requirements in component handling and logistics.

Paper Carrier Tape Market Trends

Sustainable Growth in Paper Carrier Tape Demand

Global Paper Carrier Tape Market is projected to grow from USD 195 million in 2026 to USD 223 million by 2034, at a steady CAGR of 1.9%. This growth is driven by increasing demand for electronic component packaging in consumer electronics and general applications. Paper carrier tape remains the preferred choice for passive components due to its cost-effectiveness and protective properties.

Other Trends

Asia Dominates Production and Consumption

Asia accounts for the largest share of Paper Carrier Tape production and consumption, closely following regional electronics manufacturing clusters. Countries like China, Japan, and South Korea lead in both component manufacturing and carrier tape usage, while Europe and North America maintain stable demand with focus on localized supply chains.

Technological Advancements in Material Composition

Manufacturers are increasingly incorporating multilayer composite structures with fiber reinforcement and moisture-resistant resins to enhance performance. These advancements improve the tape’s durability and protective capabilities while maintaining its lightweight advantage over plastic alternatives. Process improvements also focus on reducing dust and burrs during high-speed production.

Other Trends

Diversification by Product Type and Application

The market segments by product type into slitting, punching, and pressing paper tapes, with punching paper tape being the most widely used. Key applications include packaging for resistors, capacitors, and inductors, which together account for over 60% of Paper Carrier Tape consumption in electronic component manufacturing.

Competitive Landscape and Future Outlook

Paper Carrier Tape Market features a mix of large-scale manufacturers and regional players, with competition focused on consistent quality, pricing, and delivery reliability. Future trends include process automation, improved moisture-resistant formulations, and enhanced precision for smaller components, driving further market consolidation.

COMPETITIVE LANDSCAPE

Key Industry Players

Paper Carrier Tape Market Dominated by Asian Manufacturers with Strong Technical Expertise

Global Paper Carrier Tape Market features a competitive landscape with established Asian players dominating production due to their proximity to passive component manufacturers and cost advantages. Zhejiang Jiemei Electronic Technology leads the market with extensive production capabilities and proprietary coating technologies, followed closely by Japanese firms like NIPPO CO.,LTD and Oji F-Tex that emphasize precision punching and moisture-resistant formulations. The top five companies collectively hold approximately 42% of the market share, with margins ranging from 18-28% depending on product specialization.

Specialized manufacturers like Laser Tek Taiwan focus on high-precision tape for crystal resonators, while Jiangyin Winpack has gained traction in the Chinese domestic market through aggressive pricing. Emerging players compete primarily through regional distribution networks and customization for specific component types (resistors/capacitors). The market shows strong qualification stickiness, requiring 12-18 months for new suppliers to pass component maker validations.

List of Key Paper Carrier Tape Companies Profiled

- Zhejiang Jiemei Electronic Technology

- NIPPO CO.,LTD

- Oji F-Tex

- Laser Tek Taiwan Co.,Ltd.

- Jiangyin Winpack

- Advantek

- Accu-Glass Products

- Keystone Electronics Corp

- Desco Industries

- YAC Garter

- Asahi Kasei

- SHin-Etsu Polymer

- 3M Electronics

- Sumitomo Bakelite

- Dou Yee Enterprises

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Punching Paper Carrier Tape dominates the market due to:

|

| By Application |

|

Capacitors application shows strongest growth potential because:

|

| By End User |

|

Consumer Electronics Manufacturers remain the primary customers due to:

|

| By Electrostatic Properties |

|

Static Dissipative Type is gaining market traction because:

|

| By Manufacturing Process |

|

Multi-layer Lamination shows technological advantages including:

|

Regional Analysis: Paper Carrier Tape Market

China holds the largest paper carrier tape production capacity globally, with specialized facilities supplying both domestic and international markets. The country’s mature electronics industry maintains stringent quality requirements for component packaging.

Japan leads in high-performance paper carrier tape innovations, with manufacturers developing advanced moisture-resistant and static-free solutions for sensitive electronic components, particularly in automotive electronics applications.

South Korea’s Paper Carrier Tape Market emphasizes precision engineering to meet the demands of advanced semiconductor packaging, with manufacturers collaborating closely with major chip producers on customized solutions.

Emerging production bases in Malaysia, Thailand, and Vietnam are driving paper carrier tape adoption as multinational electronics firms diversify supply chains across the region, creating new demand centers.

North America

North America maintains significant paper carrier tape demand from aerospace and defense electronics manufacturers requiring high-reliability packaging. The region sees growing preference for sustainable paper solutions among medical device producers. Domestic suppliers focus on specialized tapes for high-value components, with Mexico emerging as a key manufacturing hub serving both local and export markets. Regulatory pressures to reduce plastic packaging waste influence purchasing decisions across the value chain.

Europe

European paper carrier tape adoption benefits from strict environmental regulations governing electronic component packaging. Germany and Italy lead in industrial electronics applications, while Nordic countries prioritize biodegradable tape solutions. The region shows increasing demand from automotive electronics suppliers transitioning to paper-based packaging. Local manufacturers emphasize recyclability certifications and cradle-to-cradle design principles to differentiate offerings.

South America

Brazil represents the largest Paper Carrier Tape Market in South America, supported by growing electronics assembly operations. Regional manufacturers focus on cost-effective solutions for consumer electronics production. Import restrictions on certain plastic packaging materials have accelerated paper tape adoption. Infrastructure challenges affect distribution efficiency compared to other global regions.

Middle East & Africa

The Middle East shows emerging demand for paper carrier tapes from electronics manufacturing investments in free trade zones. Africa’s market remains small but demonstrates potential with improving electronics production capabilities in North African countries. Both regions rely heavily on imports, with local converter operations beginning to establish presence in key markets.

Report Scope

This market research report provides a comprehensive analysis of the Paper Carrier Tape Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Paper Carrier Tape Market?

-> Paper Carrier Tape Market was valued at USD 195 million in 2026 and is projected to reach USD 223 million by 2034, exhibiting a CAGR of 1.9% during the forecast period.

What is the growth rate of Paper Carrier Tape Market?

-> The market is expected to grow at a CAGR of 1.9% during 2026-2034.

Which key companies operate in Paper Carrier Tape Market?

-> Key players include Zhejiang Jiemei Electronic Technology, NIPPO CO.,LTD, Oji F-Tex, Laser Tek Taiwan Co.,Ltd., and Jiangyin Winpack.

What are the key growth drivers?

-> Key growth drivers include increasing demand for consumer electronics, growth in passive components market, and advantages of paper carrier tape in cost-sensitive applications.

Which region dominates the market?

-> Asia is the main production and consumption region, accounting for the largest market share.

What are the emerging trends?

-> Emerging trends include development of low-dust/low-burr processes, improved moisture-resistant materials, and automation in manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...