Organic Solar Cells Market Insights

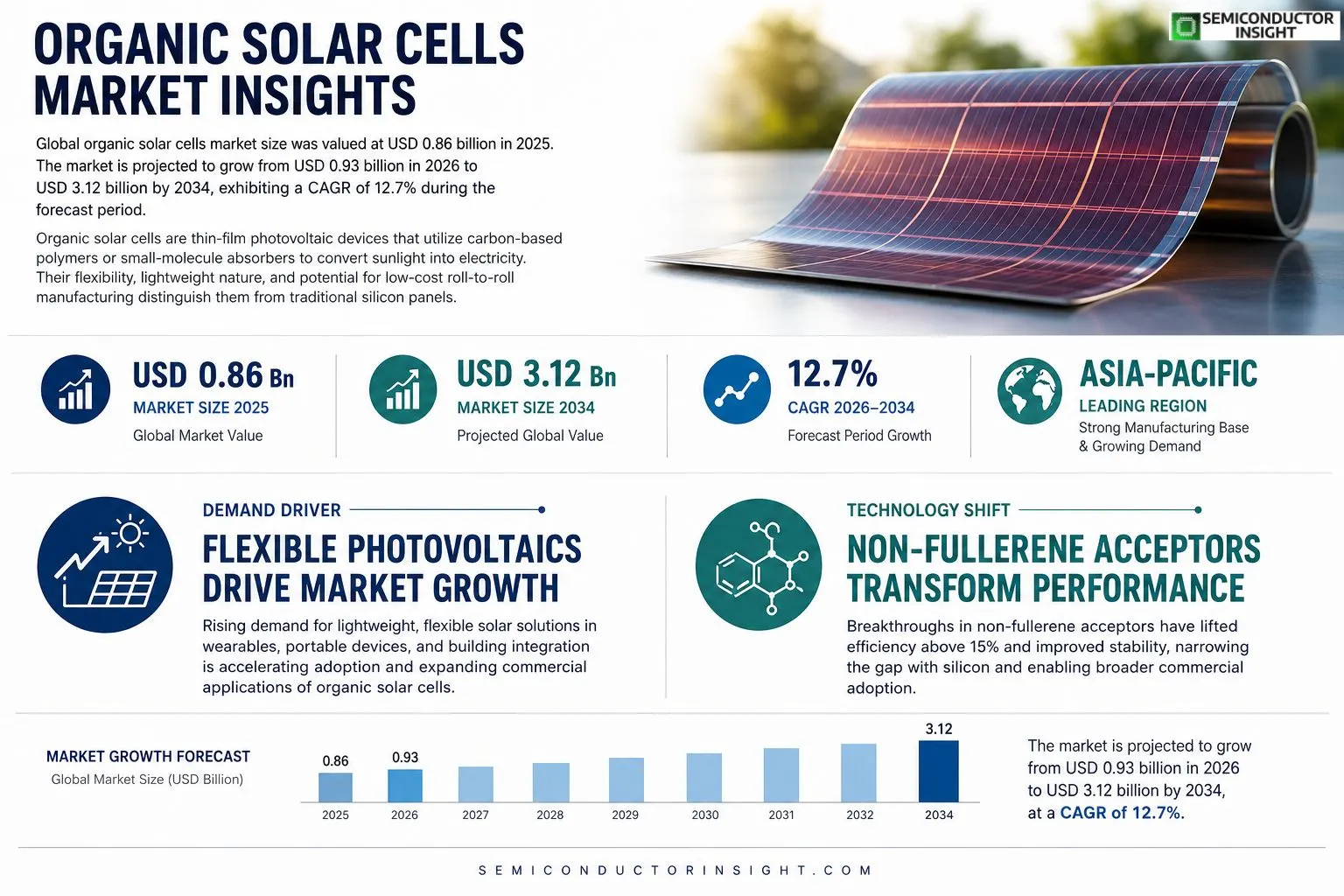

Global organic solar cells market size was valued at USD 0.86 billion in 2025. The market is projected to grow from USD 0.93 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 12.7% during the forecast period.

Organic solar cells are thin‑film photovoltaic devices that utilize carbon‑based polymers or small‑molecule absorbers to convert sunlight into electricity. Their flexibility, lightweight nature, and potential for low‑cost roll‑to‑roll manufacturing distinguish them from traditional silicon panels.The market is experiencing rapid expansion because consumer demand for flexible and portable energy solutions is rising, while substantial public and private investment accelerates research on material stability and efficiency improvements. Furthermore, breakthroughs in non‑fullerene acceptors have pushed power conversion efficiencies above 15%, encouraging broader commercial adoption. Key players such as Heliatek, DSM NanoTech, and Solvay are launching new product lines and forming strategic partnerships that are expected to further drive growth.

MARKET DRIVERS

Increasing Demand for Flexible Photovoltaics

Organic Solar Cells Market is benefiting from a surge in demand for lightweight and flexible photovoltaic solutions that can be integrated into wearable devices, portable chargers, and textile applications. Recent advances in roll‑to‑roll printing have reduced form‑factor constraints, enabling manufacturers to target niche consumer segments that value design freedom over traditional silicon rigidity.

Advancements in Materials and Manufacturing

Innovations in donor‑acceptor polymers and non‑fullerene acceptors have pushed laboratory efficiencies above 15 %, narrowing the performance gap with inorganic counterparts. Simultaneously, scalable coating techniques such as blade coating and slot‑die printing are lowering production costs, which supports broader commercial adoption of organic photovoltaic modules.

➤ “Efficiency improvements and cost‑effective roll‑to‑roll processes are the twin engines driving Organic Solar Cells Market toward mainstream viability.”

These technical and manufacturing breakthroughs are creating a virtuous cycle: higher efficiencies attract investment, which in turn funds further R&D, strengthening the overall growth trajectory of the market.

MARKET CHALLENGES

Stability and Longevity Issues

Despite rapid efficiency gains, Organic Solar Cells Market continues to grapple with degradation pathways caused by oxygen, moisture, and UV exposure. Limited operational lifetimes relative to crystalline silicon panels hinder large‑scale deployment, especially in outdoor installations where durability is paramount.

Other Challenges

Cost Competitiveness

While manufacturing costs are decreasing, the overall cost per watt remains higher than mature silicon technologies. Achieving price parity requires further scale‑up, optimized encapsulation solutions, and economies of scope across multiple product lines.

MARKET RESTRAINTS

Limited Commercial Scale Production

Current production facilities for Organic Solar Cells Market are primarily pilot‑scale, limiting the ability to meet growing demand. Capital investment for full‑line factories is substantial, and the uncertainty surrounding long‑term device reliability deters many potential investors.Furthermore, supply chain constraints for high‑purity organic semiconductors add to the production bottleneck, making it challenging to achieve consistent product quality at volume.Regulatory approvals for new organic photovoltaic modules can also be protracted, especially in regions with stringent building codes, which slows market entry for innovative designs.

MARKET OPPORTUNITIES

Emerging Applications in Building‑Integrated Photovoltaics

Architectural integration of organic solar modules onto façades, windows, and roofing membranes offers a compelling growth avenue for Organic Solar Cells Market. The aesthetic versatility of organic films enables designers to create semi‑transparent or colored panels that blend seamlessly with building envelopes.In addition, the lightweight nature of organic photovoltaics facilitates retrofitting of existing structures without imposing significant additional loads, accelerating adoption in urban redevelopment projects.Government incentives for renewable‑energy‑compatible construction and increasing consumer preference for sustainable building materials further amplify the commercial potential of these applications.

Organic Solar Cells Market Trends

Rising Demand for Flexible Photovoltaics

Organic Solar Cells Market is witnessing a clear shift toward flexible and lightweight photovoltaic solutions. Consumers and enterprises alike are seeking energy‑generating materials that can conform to irregular surfaces, be integrated into wearable devices, or be installed on vehicles where traditional rigid panels are impractical. This demand is reinforced by the increasing adoption of portable electronics that require on‑the‑go power sources. Manufacturers are responding by expanding roll‑to‑roll production lines, which reduce material waste and lower unit costs. As a result, the market is moving from niche applications toward broader commercial deployment, especially in the consumer electronics and automotive sectors.

Other Trends

Material Stability Improvements

Stability has long been a barrier for organic photovoltaics, but recent research funded by public and private programs has yielded polymers with enhanced resistance to oxygen and moisture. These advances extend operational lifetimes from a few months to several years under real‑world conditions, making the technology a more viable alternative to silicon‑based panels. Companies such as Heliatek and DSM NanoTech have integrated these stabilized materials into new product lines, emphasizing long‑term reliability for building‑integrated and outdoor installations.

Advancements in Non‑Fullerene Acceptors

One of the most significant breakthroughs driving Organic Solar Cells Market is the development of non‑fullerene acceptor molecules. These compounds have pushed power‑conversion efficiencies above 15 %, a threshold that reshapes the competitive landscape. The higher efficiency, combined with the inherent flexibility of organic layers, encourages manufacturers to explore larger‑area modules and innovative form factors. Strategic partnerships among leading players and specialist material suppliers are accelerating the transfer of laboratory‑scale successes into scalable manufacturing processes, positioning the market for sustained growth in the coming years.

COMPETITIVE LANDSCAPEKey Industry Players

Organic Solar Cells Market Competitive Overview

Organic Solar Cells Market is anchored by a handful of vertically integrated innovators that combine material science, roll‑to‑roll manufacturing, and commercial deployment. Heliatek leads the European segment with its flexible, high‑efficiency films, leveraging a proprietary polymer blend that now exceeds 14% power conversion efficiency in pilot modules. DSM NanoTech and Solvay follow closely, offering advanced non‑fullerene acceptors and scalable coating processes that underpin many emerging product lines. These three firms dominate both upstream polymer supply and downstream module integration, creating a quasi‑oligopolistic structure that shapes pricing, technology roadmaps, and partnership dynamics across the value chain.Beyond the core trio, a diverse set of niche players amplifies competition through specialty chemistries, thin‑film architectures, and regional market focus. Sumitomo Chemical contributes innovative small‑molecule absorbers that improve stability under humid conditions, while Panasonic and 3M apply their extensive coating expertise to niche automotive and wearable applications. Bayer and BASF have entered the space with proprietary polymer substrates, targeting large‑area building‑integrated photovoltaics. Nippon Sheet Glass and UBE Industries are piloting transparent organic panels for architectural glazing, and Samsung Advanced Institute of Technology is experimenting with hybrid organic/inorganic stacks for high‑performance rooftop installations. Collectively, these companies expand the technology ecosystem, drive incremental efficiency gains, and diversify end‑use opportunities.

List of Key Organic Solar Cells Companies Profiled

- Heliatek

- DSM NanoTech

- Solvay

- Sumitomo Chemical

- Panasonic

- 3M

- Bayer

- BASF

- Nippon Sheet Glass

- UBE Industries

- Samsung Advanced Institute of Technology

- Oxford Photovoltaics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Flexible thin‑film modules are emerging as the leading segment because they enable integration on curved surfaces and lightweight structures. – Their adaptability drives interest in portable and wearable power solutions. – Manufacturers highlight ease of roll‑to‑roll production, reducing material waste. – Design flexibility supports novel form factors in architecture and transportation. |

| By Application |

|

Wearable electronics dominate this category as developers seek energy‑autonomous smart textiles. – The seamless integration of organic cells onto fabrics aligns with consumer desire for self‑charging wearables. – Lightweight and flexible characteristics reduce bulk, enhancing user comfort. – Collaborative projects between textile firms and photovoltaic innovators accelerate product pipelines. |

| By End User |

|

Consumer gadgets are identified as the primary end‑user segment due to the rapid adoption of portable devices requiring on‑the‑go power. – The market perceives organic cells as a convenient solution for extending battery life. – Integration into smartphones, watches, and remote controls enhances product differentiation. – Brands emphasize sustainability narratives that resonate with eco‑conscious buyers. |

| By Material Innovation |

|

Non‑fullerene acceptors have become the focal point of material‑driven growth. – Their chemical versatility allows fine‑tuning of light‑absorption characteristics. – Researchers cite improved operational stability, addressing a historic barrier for commercial deployment. – Collaborative research consortia are accelerating translation from lab to pilot‑scale manufacturing. |

| By Market Driver |

|

Sustainability initiatives underpin the market narrative, positioning organic solar cells as a green alternative. – Companies leverage the low‑impact manufacturing footprint to meet corporate ESG goals. – Public and private funding programs prioritize research that reduces reliance on silicon‑based photovoltaics. – Consumer awareness of circular‑economy principles fuels demand for recyclable, lightweight energy solutions. |

Regional Analysis: North America

United States

Growing consumer interest in green energy solutions is driving the adoption of organic solar cells for residential applications. The aesthetic versatility of OSCs allows for seamless integration into building facades, enhancing architectural design.

The commercial and industrial sectors are increasingly recognizing the potential of OSCs to reduce energy costs and enhance sustainability profiles. BIPV solutions are gaining traction in office buildings and industrial facilities.

The integration of flexible and lightweight OSCs into consumer electronics such as smartphones, laptops, and wearable devices presents a significant growth opportunity. This application segment benefits from the adaptability and design flexibility offered by OSC technology.

Government policies and incentives, including tax credits and subsidies, play a crucial role in supporting the growth of the organic solar cell market in the United States. These initiatives reduce the upfront cost of adoption and encourage investment in OSC technologies.

Europe

European nations are proactively embracing organic solar cells, aligning with stringent environmental regulations and ambitious renewable energy targets. Germany, France, and the United Kingdom are leading the way, fostering innovation through collaborative research projects and supportive policy frameworks. The focus is on developing high-efficiency OSCs for building integration and flexible electronics. The continent’s strong chemical industry provides a competitive advantage in materials manufacturing. Furthermore, a growing emphasis on circular economy principles is driving research into sustainable OSC production and recycling processes.

Asia-Pacific

Asia-Pacific is witnessing rapid growth in the organic solar cell market, particularly in China and Japan. China’s strong manufacturing base and supportive government policies are driving large-scale production and deployment of OSCs. Japan is focusing on advanced OSC technologies for high-performance applications like flexible displays and portable power. The growing demand for affordable and flexible energy solutions across the region is further fueling market expansion for organic solar cells.

South America

South America presents a promising, albeit nascent, market for organic solar cells. Brazil and Argentina are key countries with substantial solar energy potential. The rising demand for electricity in these regions, coupled with increasing awareness of renewable energy benefits, is creating opportunities for OSC adoption. However, challenges related to financing and infrastructure development remain.

Middle East & Africa

The Middle East and Africa represent a long-term growth market for organic solar cells. Countries in the region are actively seeking to diversify their energy sources and reduce reliance on fossil fuels. The high solar irradiance levels in many areas make them particularly suitable for solar energy generation. While the market is currently small, the potential for expansion is significant, driven by government initiatives and increasing investment in renewable energy infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the Organic Solar Cells Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Organic Solar Cells Market?

-> Organic Solar Cells Market was valued at USD 0.86 billion in 2025 and is expected to reach USD 3.12 billion by 2034.

Which key companies operate in Organic Solar Cells Market?

-> Key players include Heliatek, DSM NanoTech, Solvay.

What are the key growth drivers?

-> Key growth drivers include rising consumer demand for flexible portable energy solutions, increased public and private investment in research, and breakthroughs in non‑fullerene acceptors that raise efficiency above 15%.

Which region dominates the market?

-> Asia‑Pacific is a leading region due to a strong manufacturing base and growing demand for flexible solar technologies.

What are the emerging trends?

-> Emerging trends include development of non‑fullerene acceptors, roll‑to‑roll manufacturing, and integration of flexible thin‑film photovoltaics into wearable and portable applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...