MARKET INSIGHTS

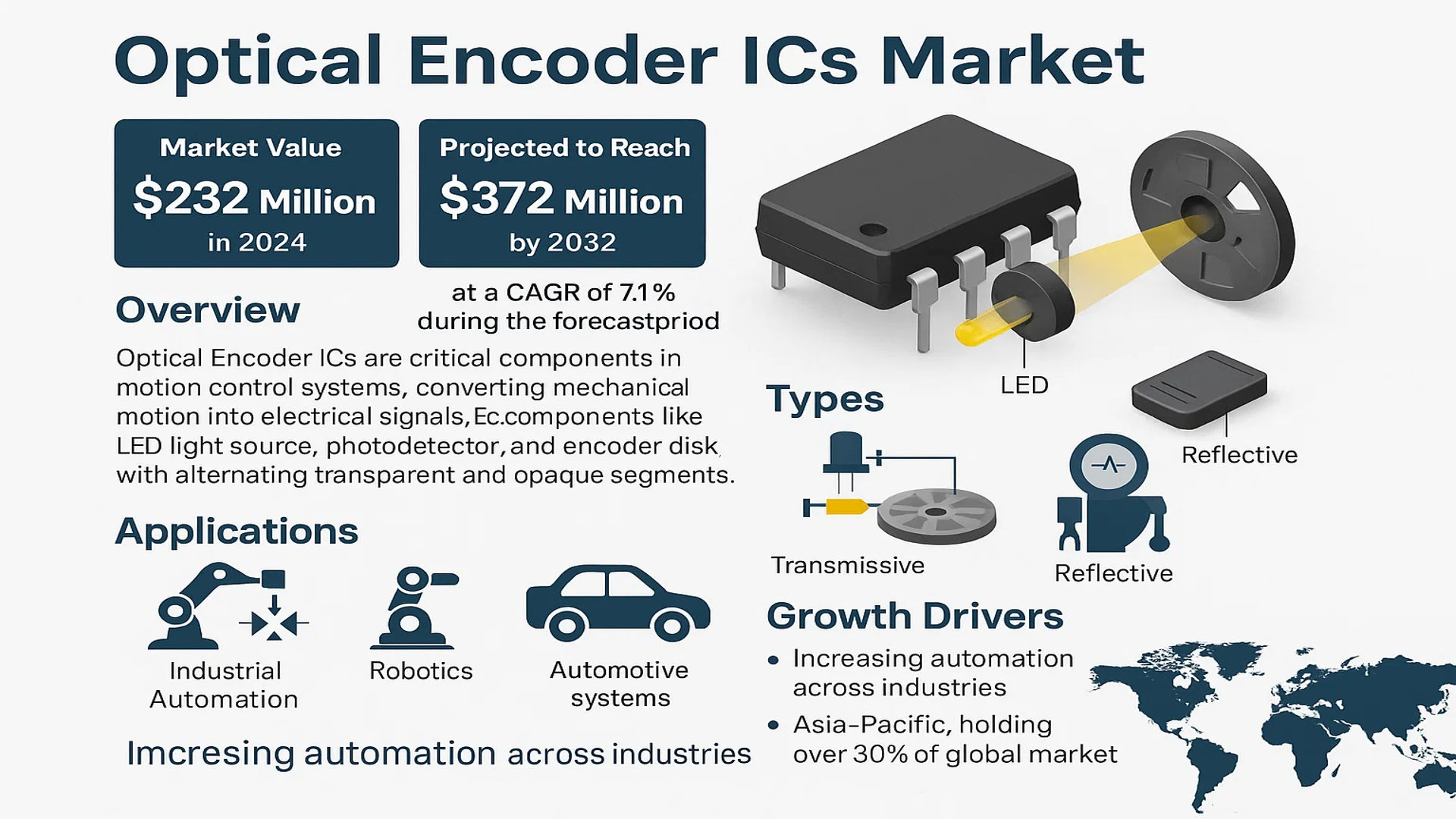

The global Optical Encoder ICs Market was valued at 232 million in 2024 and is projected to reach US$ 372 million by 2032, at a CAGR of 7.1% during the forecast period.

Optical Encoder ICs are critical components in motion control systems, converting mechanical motion into electrical signals. They consist of an LED light source, a photodetector, and an encoder disk with alternating transparent and opaque segments. These ICs generate precise quadrature signals (A & B pulses) to determine rotational position, speed, and direction—essential for applications in industrial automation, robotics, and automotive systems. The two primary types are transmissive and reflective optical encoders, with the latter dominating market share due to its compact design and versatility.

Growth is driven by increasing automation across industries, particularly in Asia-Pacific, which holds over 30% of the global market. The industrial automation segment leads application-wise, accounting for more than 25% of demand, followed by motor manufacturing. Key players like Broadcom and New Japan Radio collectively hold nearly 50% market share, emphasizing the industry’s consolidated nature. Technological advancements, such as miniaturization and higher resolution encoders, further propel adoption in emerging sectors like electric vehicles and medical devices.

MARKET DYNAMICS

MARKET DRIVERS

Rise of Industrial Automation and Robotics Fueling Demand for Optical Encoder ICs

The global industrial automation sector is undergoing rapid transformation, with an estimated growth rate exceeding 8% annually, directly influencing the optical encoder IC market. These components are critical for motion control in CNC machines, robotic arms, and automated assembly lines where precision positioning is paramount. As manufacturers increasingly adopt Industry 4.0 technologies, the need for reliable rotary and linear position feedback solutions has grown exponentially. Optical encoders provide the necessary accuracy, with modern versions offering resolutions up to 20,000 pulses per revolution, making them indispensable in high-precision manufacturing environments.

Electric Vehicle Revolution Creating New Application Opportunities

The automotive industry’s shift toward electrification represents one of the most significant growth drivers for optical encoder ICs. Modern electric vehicles utilize these components in multiple systems including motor control units, steering angle sensors, and throttle position detection. With global EV production volumes projected to surpass 30 million units annually by 2030, the demand for automotive-grade optical encoders is following an upward trajectory. These applications require robust solutions capable of operating in challenging environments while maintaining accuracy, pushing manufacturers to develop specialized automotive encoder IC variants with enhanced durability and temperature tolerance.

➤ Recent developments in magnetic and optical hybrid encoder technologies are bridging the gap between precision requirements and environmental resilience, particularly for automotive and industrial applications.

Medical Technology Advancements Driving Precision Requirements

The healthcare sector’s increasing reliance on automated diagnostic and surgical equipment represents another key growth area. Medical devices such as robotic surgery systems, CT scanners, and infusion pumps depend on optical encoder ICs for accurate position feedback. The healthcare equipment market’s stringent reliability requirements have led to specialized medical-grade encoder solutions featuring enhanced sterilization compatibility and extended operational lifespans. With the global medical device market expanding at approximately 5-7% annually, this segment continues to offer substantial opportunities for encoder IC manufacturers.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing Processes

The production of optical encoder ICs involves sophisticated manufacturing techniques and high-precision components, resulting in elevated production costs. The need for specialized photolithography equipment, high-quality optical materials, and precision alignment systems creates significant barriers to entry. These cost factors become particularly challenging in price-sensitive applications, where alternatives like magnetic encoders may offer more economical solutions despite potentially lower performance specifications.

Environmental Sensitivity Limiting Certain Applications

While optical encoders provide excellent accuracy, their performance can be compromised in harsh operating environments. Contaminants such as dust, oil mist, or condensation can interfere with the optical components, potentially affecting signal integrity. This sensitivity presents challenges for applications in heavy industrial settings, outdoor equipment, or maritime environments where conditions may be less controlled. Manufacturers continue to develop protective solutions, but these often come with trade-offs in cost or form factor.

Other Challenges

Miniaturization Constraints

The push toward smaller form factors in consumer electronics and medical devices presents technical challenges for optical encoder design. As package sizes decrease, maintaining signal integrity and alignment tolerances becomes increasingly difficult, potentially impacting overall system reliability.

Supply Chain Vulnerabilities

The optical encoder IC market remains susceptible to semiconductor supply chain fluctuations, with certain critical components facing periodic shortages. This volatility can affect production timelines and product availability across multiple industries.

MARKET OPPORTUNITIES

Emerging IoT and Smart Device Ecosystem Creating New Use Cases

The proliferation of connected devices in both consumer and industrial IoT applications represents a significant growth opportunity. Smart home appliances, wearable devices, and industrial monitoring equipment increasingly incorporate optical encoder ICs for position sensing. The global IoT market’s continued expansion into new sectors is driving demand for compact, energy-efficient encoder solutions that can operate in battery-powered environments while maintaining measurement precision.

Advancements in ASIC Integration Opening New Possibilities

Recent developments in application-specific integrated circuit (ASIC) technology enable more sophisticated encoder IC designs with embedded processing capabilities. These innovations allow for on-chip signal conditioning, error compensation algorithms, and digital interface integration, reducing system complexity for end-users. As manufacturers continue to enhance integration levels, opportunities emerge for optical encoder ICs in applications previously constrained by space or power limitations.

Renewable Energy Sector Presenting Growth Potential

The expanding renewable energy infrastructure, particularly in wind and solar power generation, requires robust position sensing solutions for optimal system performance. Optical encoder ICs play critical roles in solar tracking systems and wind turbine pitch control mechanisms. With global investments in renewable energy projects continuing to rise, this sector offers promising opportunities for encoder technology providers specializing in outdoor-rated and long-lifecycle solutions.

OPTICAL ENCODER ICS MARKET TRENDS

Industrial Automation and Robotics Driving Demand for High-Precision Encoder ICs

The global optical encoder ICs market is experiencing robust growth, driven primarily by increasing adoption in industrial automation and robotics applications. Optical encoders, known for their high resolution and reliability in position feedback systems, have become critical components in computer numerical control (CNC) machines, robotic arms, and automated manufacturing equipment. The market’s projected growth from $232 million in 2024 to $372 million by 2032 reflects the expanding need for precision motion control solutions across industries. Asia-Pacific currently leads in consumption, accounting for over 30% of the global market, while industrial automation applications dominate end-use with a 25% share.

Other Trends

Miniaturization and Integration in Compact Applications

A significant trend reshaping the optical encoder IC landscape is the push toward miniaturization. Manufacturers are developing smaller form factor encoders for applications in medical devices, wearables, and drones, where space constraints are critical. This trend aligns with the broader industry movement toward more compact and energy-efficient electronic components. The miniaturization not only enables new applications but also contributes to cost reduction and improved system efficiency, particularly in consumer electronics and portable devices.

Electrification of Automotive Systems Creating New Opportunities

The automotive sector is emerging as a key growth area for optical encoder ICs, particularly with the rapid adoption of electric vehicles (EVs) and advanced driver assistance systems (ADAS). These components are increasingly used in electric power steering systems, motor control units, and position sensing applications. The transition from traditional mechanical encoders to non-contact optical solutions provides benefits including higher durability and resistance to vibration and contamination. This shift is particularly important as automotive systems require components capable of withstanding harsh operating environments while maintaining precision over extended product lifecycles.

Advancements in Resolution and Speed Specifications

Market demands are evolving toward higher resolution and faster response times to support sophisticated applications in semiconductor manufacturing equipment, laser systems, and high-speed data transmission. Modern optical encoder ICs are achieving resolutions up to 16 bits and response times in the microsecond range, enabling more precise control in industrial and scientific equipment. This technological progression supports complex closed-loop control systems requiring real-time position feedback, which is becoming standard in advanced manufacturing environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and Strategic Positioning Drive Market Competition

The global optical encoder ICs market exhibits a concentrated competitive landscape, dominated by a few major players who collectively hold significant market share. Broadcom and New Japan Radio lead the industry, accounting for nearly 50% of the market share in 2024. Their dominance stems from extensive R&D investments, broad product portfolios, and strong distribution networks across key regions including North America, Europe, and Asia-Pacific.

While these top players focus on high-performance encoder ICs for industrial automation and automotive applications, mid-sized companies like SEIKO NPC and IC-Haus are carving out niches in specialized segments such as medical devices and consumer electronics. These firms differentiate themselves through customized solutions and rapid innovation cycles, allowing them to compete effectively despite the market dominance of larger corporations.

The competitive intensity is further heightened by continuous product evolution. Market leaders are aggressively developing miniaturized optical encoder ICs with higher resolution to meet the demands of emerging applications in robotics and IoT. Meanwhile, regional players in Asia are gaining traction by offering cost-competitive alternatives, particularly in price-sensitive markets.

List of Key Optical Encoder IC Companies Profiled

- Broadcom Inc. (U.S.)

- New Japan Radio Co., Ltd. (Japan)

- SEIKO NPC Corporation (Japan)

- IC-Haus GmbH (Germany)

- PREMA Semiconductor GmbH (Germany)

- Hamamatsu Photonics K.K. (Japan)

- TE Connectivity Ltd. (Switzerland)

- Bourns, Inc. (U.S.)

- Alps Alpine Co., Ltd. (Japan)

Segment Analysis:

By Type

Reflective Type Optical Encoder ICs Dominate the Market Due to High Durability and Compact Design

The market is segmented based on type into:

- Reflective Type

- Subtypes: Single-channel, Multi-channel, Differential output

- Transmissive Type

- Subtypes: Incremental, Absolute

- Hybrid Optical Encoder ICs

- Magnetic Encoder ICs

- Others

By Application

Industrial Automation Leads Due to Growing Demand for High-Precision Motion Control

The market is segmented based on application into:

- Industrial Automation

- Subtypes: CNC machines, Robotics, Assembly lines

- Automotive

- Subtypes: EV motor control, Steering systems, Transmission

- Consumer Electronics

- Medical Equipment

- Aerospace & Defense

- Others

By Technology

Quadrature Encoder ICs Hold Significant Share ENABLED by Reliable Position Sensing

The market is segmented based on technology into:

- Quadrature Output

- Analog Output

- Digital Output

- Others

By End User

Manufacturing Sector Leads Due to Increasing Factory Automation Investments

The market is segmented based on end user into:

- Manufacturing

- Automotive

- Healthcare

- Electronics

- Energy

- Others

Regional Analysis: Optical Encoder ICs Market

Asia-Pacific

Boasting over 40% of global optical encoder IC consumption, the Asia-Pacific region maintains dominance due to aggressive industrialization and robust electronics manufacturing investments. China commands the largest market share within the region, driven by its expansive industrial automation initiatives under “Made in China 2025” and strong motor production capacity. Japan remains a technological leader with companies like New Japan Radio pioneering high-precision encoders for robotics and semiconductor equipment. While cost competitiveness pressures innovation in Southeast Asian markets, India shows increasing demand due to growing automotive EV production and government-backed smart manufacturing programs.

North America

Accounting for approximately 30% of global optical encoder IC demand, North America demonstrates strong adoption in cutting-edge applications. The U.S. leads with substantial deployment in aerospace instrumentation, medical robotics, and autonomous vehicle subsystems. Research institutes and startups actively collaborate with manufacturers like Broadcom to develop next-gen miniaturized encoders for wearable health monitors and micro drones. Canadian cleantech initiatives further drive encoder usage in wind turbine pitch control systems. Stringent quality standards in the region necessitate ruggedized designs with extended temperature tolerances.

Europe

With about 25% market share, Europe showcases demand for high-reliability optical encoder ICs compliant with stringent EU RoHS directives. Germany’s thriving industrial automation sector consumes substantial volumes for CNC machinery and packaging equipment, while French manufacturers integrate encoders into high-speed rail systems. The Nordic countries exhibit growing requirements for encoders in offshore energy applications and precision medical devices. Automotive adoption accelerates as EU emissions regulations push electrification, creating demand for encoder-based motor control in 48V mild hybrid systems.

Middle East & Africa

This emerging market displays increasing optical encoder IC adoption in oil & gas automation equipment and construction machinery. Dubai’s smart city projects incorporate encoders for building automation systems, while South Africa utilizes them in mining equipment condition monitoring. Market growth faces constraints from limited local technical expertise in encoder integration, though partnerships with European and Asian suppliers help bridge this gap. The region shows particular interest in dust- and moisture-resistant encoder models suitable for harsh desert environments.

South America

Brazil represents the primary optical encoder IC market in South America, largely serving industrial motor applications and agricultural machinery automation. Argentina shows nascent demand for encoders in renewable energy systems, particularly solar tracker positioning mechanisms. Economic volatility inhibits widespread technology adoption, but the region benefits from proximity to North American supply chains. Local manufacturers gradually transition from mechanical to optical encoders as automation becomes essential for maintaining export competitiveness in manufacturing sectors.

Report Scope

This market research report provides a comprehensive analysis of the global Optical Encoder ICs market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Optical Encoder ICs market was valued at USD 232 million in 2024 and is projected to reach USD 372 million by 2032, growing at a CAGR of 7.1%.

- Segmentation Analysis: Detailed breakdown by product type (Reflective Type and Transmissive Type), application (Industrial Automation, Motors, Medical, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (30% market share), Europe (25% market share), Asia-Pacific (30% market share), Latin America, and the Middle East & Africa.

- Competitive Landscape: Profiles of leading market participants like Broadcom and New Japan Radio (combined 50% market share), including their product portfolios, R&D investments, and strategic partnerships.

- Technology Trends & Innovation: Assessment of miniaturization trends, higher resolution requirements (up to 20-bit resolution in premium models), and integration with AI-powered control systems.

- Market Drivers & Restraints: Evaluation of factors like industrial automation growth (25% market share) and EV adoption versus challenges like supply chain disruptions in semiconductor materials.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, motion control system integrators, and investors in the Industry 4.0 ecosystem.

Research methodology combines primary interviews with 50+ industry experts and analysis of verified market data from trade associations, company financial reports, and patent filings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Optical Encoder ICs Market?

->Optical Encoder ICs Market was valued at 232 million in 2024 and is projected to reach US$ 372 million by 2032, at a CAGR of 7.1% during the forecast period.

Which key companies operate in Global Optical Encoder ICs Market?

-> Key players include Broadcom, New Japan Radio, SEIKO NPC, IC-Haus, PREMA Semiconductor, and Hamamatsu, with the top two players holding 50% market share.

What are the key growth drivers?

-> Key growth drivers include industrial automation expansion (25% market share), electric vehicle adoption, and demand for high-precision motion control in robotics.

Which region dominates the market?

-> Asia-Pacific leads in consumption (30% market share), followed by North America (30%) and Europe (25%).

What are the emerging trends?

-> Emerging trends include miniaturization for wearable devices, 20-bit+ high-resolution encoders, and integration with IIoT-enabled predictive maintenance systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...