MARKET INSIGHTS

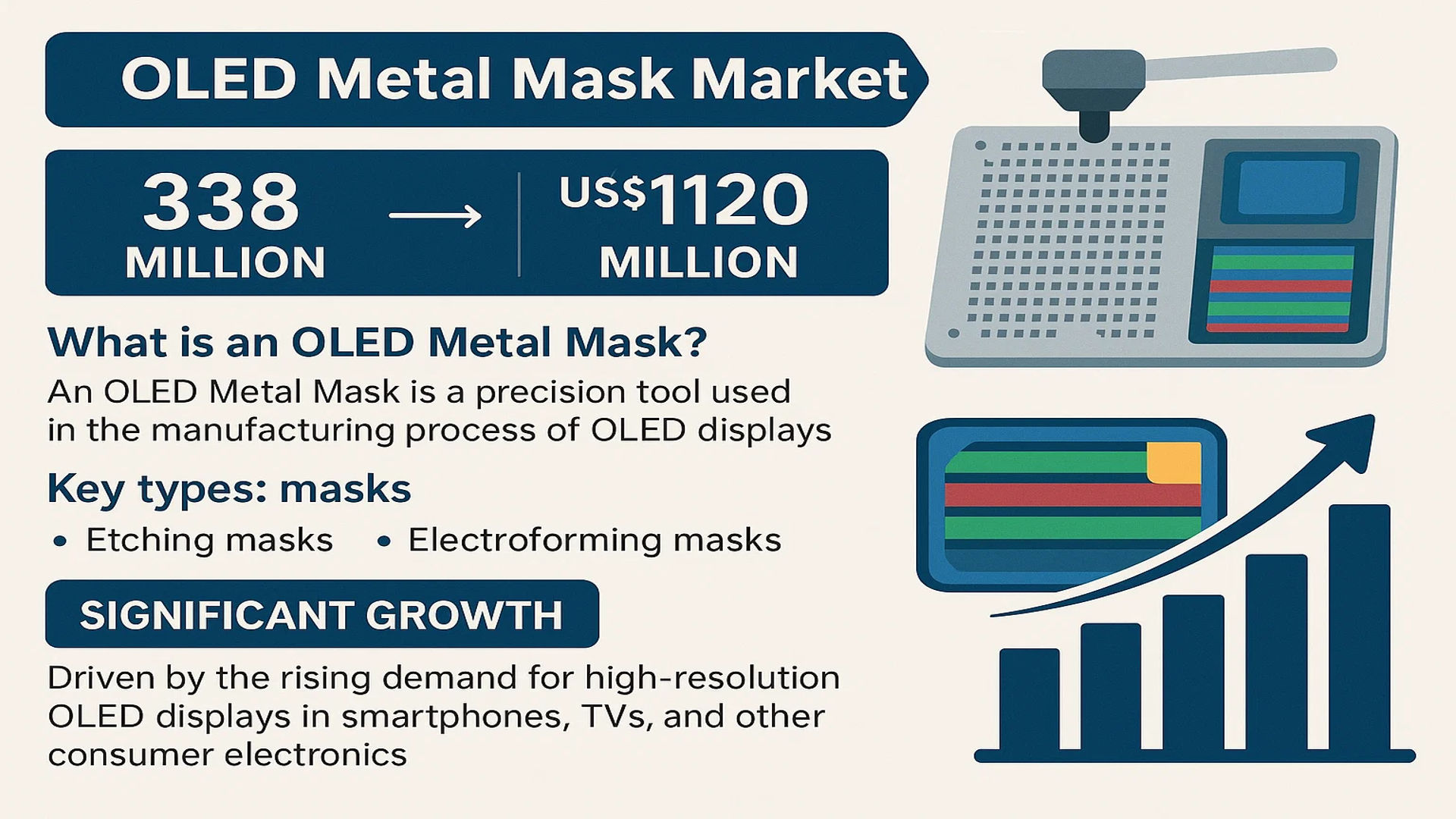

The global OLED Metal Mask Market was valued at 338 million in 2024 and is projected to reach US$ 1120 million by 2032, at a CAGR of 19.2% during the forecast period.

An OLED Metal Mask is a precision tool used in the manufacturing process of OLED (Organic Light Emitting Diode) displays. These masks facilitate the deposition of fine metal patterns onto display substrates, which is critical for defining the pixel structure in OLED screens. Key types include etching and electroforming masks, each offering distinct advantages in terms of resolution and durability.

The market is experiencing significant growth, primarily driven by the rising demand for high-resolution OLED displays in smartphones, TVs, and other consumer electronics. Technological advancements in display manufacturing, particularly the shift toward flexible and foldable OLED panels, are further accelerating demand. However, the market faces challenges such as high production costs and the need for advanced fabrication techniques to meet increasingly stringent precision requirements. Leading players like Dai Nippon Printing (DNP) and Toppan Printing are actively innovating to address these challenges while expanding their market presence.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption of OLED Displays in Consumer Electronics Accelerates Demand

The global OLED display market is experiencing robust growth, projected to expand at a compound annual growth rate exceeding 15% through 2030. This surge is primarily driven by increasing smartphone penetration, with over 60% of premium smartphones now incorporating OLED screens. The transition from LCD to OLED technology across television segments further amplifies demand, as manufacturers prioritize energy efficiency and superior viewing angles. OLED metal masks serve as critical enablers of this transformation, allowing precise deposition of organic materials that create vibrant, high-contrast displays. Recent innovations in foldable smartphone technology, requiring ultra-thin yet durable masks, have created new application avenues for specialized metal mask solutions.

Technological Advancements in Display Manufacturing Fuel Market Expansion

Continuous innovation in display resolution requirements presents lucrative opportunities for OLED metal mask manufacturers. The industry’s shift toward 8K resolution displays and higher pixel density (>500 PPI) screens demands masks with micron-level precision. Advanced manufacturing techniques like laser cutting and electroforming now enable production of masks with aperture precision under 10 micrometers, a critical capability for next-generation displays. Leading manufacturers are investing heavily in research and development, with several recent breakthroughs in multi-layer mask architectures that significantly improve production yield rates. These technological strides are enabling display makers to achieve superior color uniformity and brightness consistency across panels.

Rising Investments in Display Production Facilities Create Sustained Demand

Major display manufacturers are establishing new production facilities across Asia, with planned investments exceeding $30 billion in OLED production capacity through 2026. This expansion directly correlates with increased metal mask consumption, as each new production line requires hundreds of specialized masks. The growing localization of display supply chains has prompted mask producers to establish regional service centers near major panel fabrication plants, ensuring just-in-time delivery and technical support. Furthermore, government initiatives supporting domestic display industries in several countries are creating favorable conditions for long-term market growth, with policies offering tax incentives for equipment procurement including precision masks.

MARKET CHALLENGES

Precision Manufacturing Requirements Pose Significant Production Barriers

The extreme precision required for OLED metal masks presents formidable manufacturing challenges. Current industry standards demand positional accuracy within ±3 micrometers, with some premium applications requiring even tighter tolerances. Maintaining such precision across large-area masks (often exceeding Gen 6 panel sizes) requires specialized cleanroom facilities and advanced metrology equipment, with single mask production costs frequently surpassing $10,000. The complex photolithography and etching processes yield substantial material waste, with scrap rates as high as 30% during production ramp-up phases. These factors collectively contribute to lengthy production lead times, sometimes stretching to 12 weeks for customized mask designs.

Other Challenges

Material Limitations

Current nickel alloys, while providing excellent thermal stability, face limitations in addressing the industry’s demand for ultra-thin yet durable masks. Repeated thermal cycling during the OLED deposition process causes gradual warping and aperture deformation, typically reducing mask operational lifespan to approximately 50,000 deposition cycles.

Cleanroom Requirements

Stringent particulate contamination controls necessitate Class 100 or better cleanroom environments for mask production and handling. These facilities require substantial capital investment, with annual maintenance costs for a medium-scale mask production facility often exceeding $5 million.

MARKET RESTRAINTS

High Capital Intensity Limits Market Entry and Expansion

The OLED metal mask industry faces significant barriers to entry due to its capital-intensive nature. Establishing a competitive production facility requires minimum investments of $50 million for basic capabilities, with advanced manufacturing lines exceeding $150 million. This financial threshold restricts market participation to established corporations or well-funded new entrants. Existing manufacturers must continuously reinvest substantial portions of revenue (typically 15-20%) into equipment upgrades to maintain technological competitiveness. The lengthy ROI period, often spanning 5-7 years, discourages short-term investors and limits the pace of industry expansion despite growing end-market demand.

MARKET OPPORTUNITIES

Emerging Applications in Microdisplay and Automotive Sectors Offer Growth Potential

The rapid development of augmented reality devices and automotive HUD systems is creating new opportunities for specialized metal mask solutions. Micro-OLED displays for AR/VR applications demand masks capable of patterning sub-5 micrometer features, a niche requiring proprietary manufacturing techniques. The automotive sector’s adoption of flexible OLEDs for curved instrument clusters and center-stack displays necessitates masks designed for three-dimensional deposition processes. Industry leaders are actively developing hybrid mask technologies combining traditional metal masks with advanced polymer composites to address these emerging applications. The market for specialized masks in these segments is projected to grow at approximately 25% annually through 2030.

Localization Initiatives Create Regional Market Expansion Opportunities

Government-led initiatives to establish domestic display supply chains are fostering regional market growth opportunities. Several countries have implemented policies requiring minimum local content percentages for display manufacturing equipment, including metal masks. Mask manufacturers are responding by establishing technical centers and production facilities in strategic locations near emerging display production clusters. This regional expansion facilitates faster response times and reduced logistics costs while complying with local content regulations. Recent partnerships between mask suppliers and academic institutions aim to develop localized talent pools for precision manufacturing, addressing the industry’s skilled labor requirements.

OLED METAL MASK MARKET TRENDS

Rising Demand for High-Resolution Displays to Emerge as a Trend in the Market

The global OLED Metal Mask market is experiencing a significant trend driven by the escalating demand for high-resolution displays across consumer electronics. With smartphone manufacturers increasingly adopting OLED screens for their superior color reproduction and energy efficiency, the need for precision metal masks has surged. This demand is further amplified by the transition towards higher pixel densities, such as the shift from Full HD to 4K and even 8K resolutions in televisions and monitors. To meet these requirements, metal mask manufacturers are innovating to produce finer patterns, with some advanced masks now capable of supporting resolutions exceeding 500 pixels per inch (PPI). This trend is not only prevalent in smartphones but is also gaining traction in tablets, laptops, and automotive displays, creating a robust and expanding market for high-precision OLED metal masks.

Other Trends

Expansion into Flexible and Foldable Display Applications

A transformative trend shaping the OLED metal mask market is the rapid growth of flexible and foldable display technologies. The advent of foldable smartphones and rollable televisions necessitates metal masks that can accommodate deposition on flexible, often plastic, substrates without compromising on pattern accuracy. This requires masks with enhanced mechanical properties to resist warping and maintain dimensional stability during the deposition process. The market for foldable displays is projected to grow at a compound annual growth rate of over 45% in the coming years, directly fueling innovation in metal mask design and materials. Manufacturers are increasingly investing in advanced alloys and composite materials to develop masks that are both ultra-thin and highly durable, enabling the mass production of next-generation flexible OLED panels.

Technological Advancements in Mask Fabrication Processes

Technological advancements in the fabrication processes of OLED metal masks themselves represent a critical market trend. While traditional etching methods are well-established, there is a growing shift towards electroforming techniques, which allow for the creation of more intricate and precise patterns with smoother edges and higher aspect ratios. This is paramount for achieving the finer pixel pitches required in modern displays. Furthermore, the integration of artificial intelligence and machine learning into the mask inspection and quality control processes is significantly enhancing production yields and reducing defects. Automated optical inspection systems powered by AI can now detect micron-level imperfections at high speeds, ensuring that only masks meeting the strictest tolerances are used in display manufacturing, thereby improving overall production efficiency and cost-effectiveness.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global OLED metal mask market exhibits an oligopolistic structure, dominated by a handful of established players who control a significant portion of the market share due to high technological barriers and substantial capital investment requirements. Dai Nippon Printing (DNP) and Toppan Printing collectively command an estimated 65-70% of the global market share, a position solidified by their decades of experience in precision printing and etching technologies, extensive R&D capabilities, and long-standing supply agreements with major OLED panel manufacturers like Samsung Display and LG Display.

These industry leaders are relentlessly focused on advancing mask technology to support the transition to higher resolution displays and more complex form factors. For instance, DNP has recently invested over $180 million in new production facilities to increase capacity for fine metal masks (FMM) used in smartphone displays. Similarly, Toppan has accelerated its development of masks for 8K TVs and advanced micro-OLED applications for AR/VR devices, recognizing these as key growth vectors.

The competitive intensity is further heightened by specialized players who are carving out niches through technological innovation. Darwin and Philoptics have gained significant traction by developing advanced electroforming processes that offer superior precision for high-ppi displays, particularly targeting the burgeoning Chinese OLED manufacturing sector. Their growth is directly tied to the expansion of panel makers like BOE and CSOT.

Meanwhile, Korean firms like Sewoo Incorporation and Poongwon are strengthening their positions through strategic partnerships and vertical integration. They are focusing on improving mask durability and lifespan—a critical cost factor for manufacturers—through proprietary alloy developments and advanced coating technologies. These companies are also actively pursuing opportunities in the flexible display segment, which requires masks capable of handling bendable substrates without compromising patterning accuracy.

The market remains dynamic because while the entry barriers are formidably high, the reward is access to a supply chain critical to a display market projected to exceed $80 billion. Consequently, all players are engaged in continuous innovation, not just in mask design and fabrication, but also in areas like cleaning and inspection technologies to enhance overall production yield and reduce total cost of ownership for their clients.

List of Key OLED Metal Mask Companies Profiled

- Dai Nippon Printing Co., Ltd. (DNP) (Japan)

- Toppan Printing Co., Ltd. (Japan)

- Darwin Co., Ltd. (South Korea)

- Sewoo Incorporation (South Korea)

- Poongwon Precision Co., Ltd. (South Korea)

- Athene Co., Ltd. (South Korea)

- Philoptics Co., Ltd. (South Korea)

Segment Analysis:

By Type

Etching Segment Leads the Market Due to Precision in High-Resolution OLED Production

The market is segmented based on type into:

- Etching

- Subtypes: Wet etching and dry etching

- Electroforming

- Subtypes: Nickel-based and cobalt-based

- Others

- Subtypes: Laser cutting and hybrid methods

By Application

Smartphone Segment Dominates Due to Rapid Adoption of OLED Displays in Mobile Devices

The market is segmented based on application into:

- Smartphone

- Subtypes: Foldable smartphones and standard OLED smartphones

- TV and Computer

- Subtypes: OLED TVs, monitors, and laptops

- Others

- Subtypes: Wearables, automotive displays, and signage

By Material

Invar Alloy Segment Holds Significant Share Due to Thermal Stability in OLED Manufacturing

The market is segmented based on material into:

- Invar alloy

- Stainless steel

- Nickel alloy

- Others

By Technology

Fine Metal Mask (FMM) Technology Segment Leads Due to Superior Pixel Patterning Capabilities

The market is segmented based on technology into:

- Fine Metal Mask (FMM)

- Coarse Metal Mask (CMM)

- Hybrid Mask Technology

- Others

Regional Analysis: OLED Metal Mask Market

Asia-Pacific

The Asia-Pacific region dominates the global OLED Metal Mask market, holding the largest revenue share in 2024 at over 65%, driven primarily by the robust electronics manufacturing sector in South Korea, China, and Japan. This region benefits from extensive investments in OLED production facilities by major display manufacturers like Samsung Display and LG Display, which demand high-precision metal masks for their advanced display technologies. Government initiatives supporting semiconductor and display industries in countries like China further accelerate local production capabilities. However, intense competition among regional suppliers has led to price pressures, though quality remains paramount for high-end display applications. The rise of Chinese OLED panel manufacturers is creating new opportunities for domestic metal mask suppliers.

North America

North America maintains a strong position in the OLED Metal Mask market due to cutting-edge R&D in display technologies and significant investments from tech giants. The United States, in particular, sees growing demand from both domestic display producers and research institutions developing next-generation OLED applications. The region benefits from collaborations between academic institutions and industry players to improve mask fabrication techniques. While actual production capacity is limited compared to Asia, North America leads in patent filings for advanced metal mask technologies, particularly for micro-LED applications. Supply chain localization efforts are gaining traction to reduce dependence on Asian suppliers.

Europe

Europe’s market is characterized by specialized applications in automotive displays and premium consumer electronics, with Germany and the UK as key contributors. The region focuses on high-value, precision metal masks for niche applications rather than mass production. European manufacturers emphasize environmentally sustainable production processes to comply with strict EU regulations. Collaboration between automotive OEMs and display suppliers is driving innovations in mask technology for curved and flexible displays used in vehicle dashboards. However, higher production costs compared to Asian counterparts limit the region’s market share, though quality remains a competitive advantage.

Middle East & Africa

This emerging market shows potential through strategic investments in technology infrastructure, particularly in UAE and Israel. While current demand is limited, growing interest in local electronics manufacturing and smart city projects could drive future metal mask adoption. Israel’s strong tech startup ecosystem has shown particular interest in micro-display technologies which could benefit mask suppliers. The region currently relies heavily on imports, but potential exists for local partnerships with global mask manufacturers looking to diversify supply chains away from traditional hubs.

South America

South America represents the smallest market share currently, with Brazil being the primary consumer of OLED Metal Masks for its growing consumer electronics sector. Economic volatility and limited local display manufacturing capacity constrain market growth. Most demand comes from aftermarket service providers and small-scale assembly operations rather than large-scale production. However, government initiatives to develop local tech manufacturing capabilities could gradually increase demand for precision display components like metal masks in the long term.

Report Scope

This market research report provides a comprehensive analysis of the global and regional OLED Metal Mask markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global OLED Metal Mask market was valued at USD 338 million in 2024 and is projected to reach USD 1,120 million by 2032, growing at a CAGR of 19.2%.

- Segmentation Analysis: Detailed breakdown by product type (etching, electroforming, others), application (smartphone, TV & computer, others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets like China, South Korea, Japan and the US.

- Competitive Landscape: Profiles of leading manufacturers including Dai Nippon Printing (DNP), Toppan Printing, Darwin, Sewoo Incorporation, Poongwon, Athene, and Philoptics, covering their market share, product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of precision fabrication techniques, material advancements, and evolving standards for high-resolution OLED displays.

- Market Drivers & Restraints: Evaluation of factors like rising OLED display demand and technological advancements versus challenges like fabrication complexity and cost pressures.

- Stakeholder Analysis: Strategic insights for display manufacturers, component suppliers, investors, and policymakers regarding the evolving OLED ecosystem.

The report employs primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global OLED Metal Mask Market?

-> OLED Metal Mask Market was valued at 338 million in 2024 and is projected to reach US$ 1120 million by 2032, at a CAGR of 19.2% during the forecast period..

Which key companies operate in Global OLED Metal Mask Market?

-> Key players include Dai Nippon Printing (DNP), Toppan Printing, Darwin, Sewoo Incorporation, Poongwon, Athene, and Philoptics.

What are the key growth drivers?

-> Key growth drivers include rising demand for OLED displays in smartphones and TVs, technological advancements in display resolution, and increasing adoption of flexible OLEDs.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 70% of global demand, driven by major display manufacturers in South Korea, China and Japan.

What are the emerging trends?

-> Emerging trends include development of ultra-high resolution masks for 8K displays, adoption of new alloy materials, and precision manufacturing techniques for flexible OLEDs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...