MARKET INSIGHTS

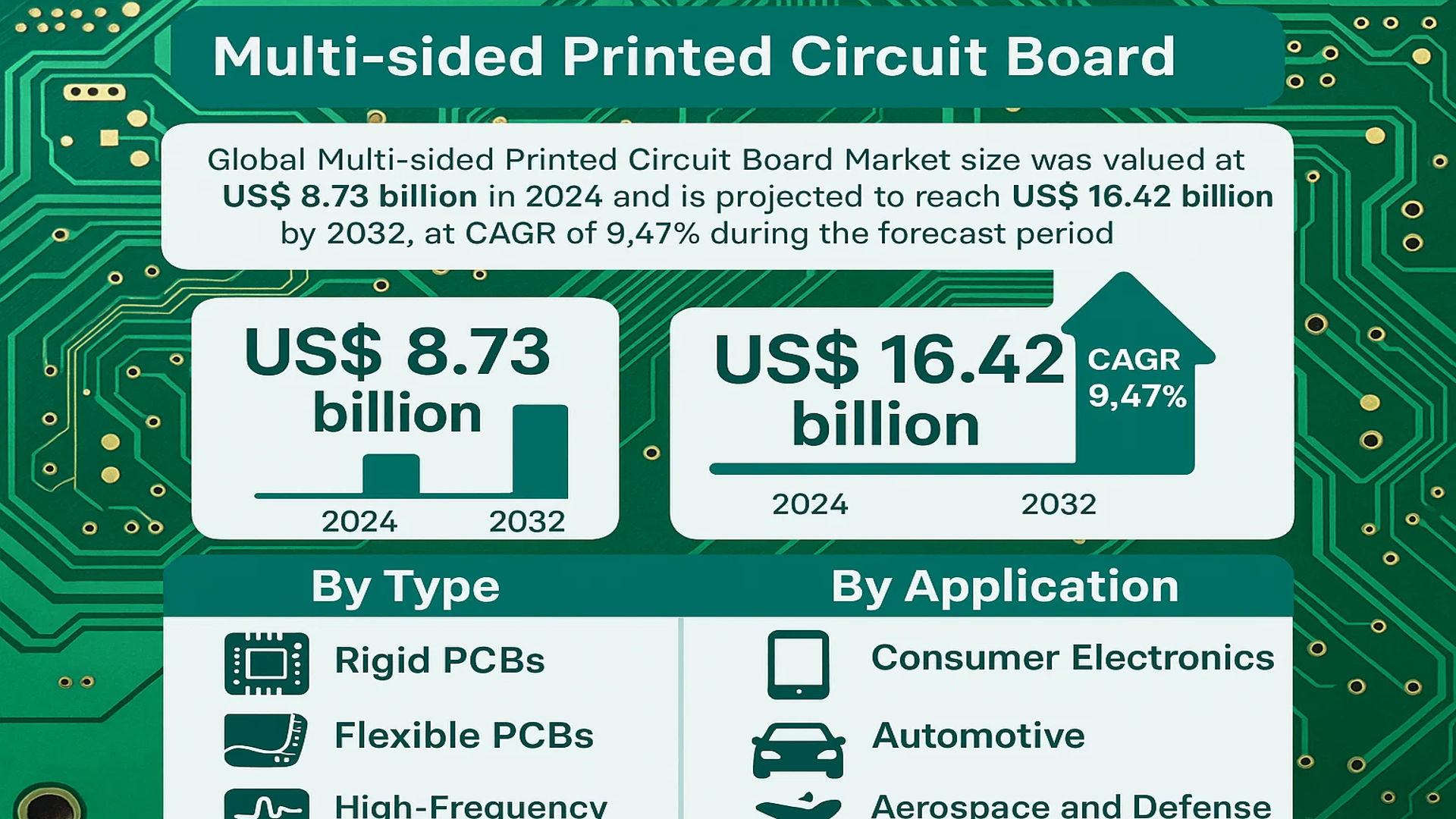

The global Multi-sided Printed Circuit Board Market size was valued at US$ 8.73 billion in 2024 and is projected to reach US$ 16.42 billion by 2032, at a CAGR of 9.47% during the forecast period 2025–2032.

Multi-sided PCBs are advanced circuit boards with multiple conductive layers separated by insulating materials, enabling complex circuit designs in compact spaces. Unlike standard double-sided boards, these multilayer PCBs typically range from 4 to 12 layers (with some specialized applications requiring up to 50 layers), offering superior electrical performance and design flexibility. The technology facilitates high-density interconnects (HDI) crucial for modern electronics.

The market growth is primarily driven by increasing demand from 5G infrastructure, automotive electronics, and AI hardware. The global PCB industry, valued at USD 81 billion in 2022 according to semiconductor research data, continues its upward trajectory with China dominating production. Recent advancements in substrate materials and miniaturization techniques are further expanding application possibilities, particularly in wearable devices and IoT components. Key players like TTM Technologies and Unimicron are investing heavily in high-layer-count PCBs to meet emerging technological demands.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 5G and IoT Technologies Accelerating PCB Demand

The rapid global rollout of 5G networks is creating unprecedented demand for multi-sided PCBs, particularly in telecommunications infrastructure and connected devices. With 5G requiring significantly more base stations than previous generations – estimated at 3-4 times denser deployment than 4G – the need for high-frequency, high-density circuit boards has surged. These advanced PCBs must handle higher data transfer rates while maintaining signal integrity, pushing manufacturers to develop boards with more layers and superior materials. The Internet of Things (IoT) ecosystem, projected to exceed 29 billion connected devices by 2027, further fuels this demand as smart devices require compact, reliable PCBs for functionality.

Automotive Electronics Evolution Driving PCB Innovation

Modern vehicles are undergoing a technological transformation, evolving into essentially computers on wheels. The average automobile now contains over 1,400 semiconductor chips, many mounted on multi-layer PCBs. Electric vehicles (EVs) in particular require advanced PCB configurations, with the power electronics system alone containing numerous high-current boards. Advanced driver-assistance systems (ADAS), in-vehicle infotainment, and upcoming autonomous driving technologies all rely on sophisticated multi-sided PCBs capable of operating in harsh environments. The automotive PCB market segment is growing at approximately 6-8% annually, outpacing many other application areas.

➤ Leading PCB manufacturers are investing heavily in automotive-grade solutions, with some dedicating up to 30% of their R&D budgets to meet stringent automotive qualification standards.

The transition to electric powertrains represents a paradigm shift for PCB manufacturers. EV power electronics demand boards that can handle high voltages and temperatures while maintaining reliability over the vehicle’s lifetime. This has spurred innovation in materials and manufacturing processes across the industry.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Material Shortages Impeding Growth

The PCB industry faces significant challenges from global supply chain disruptions and material shortages. Copper foil, a critical PCB component, has experienced fluctuating prices and inconsistent availability, with prices rising over 35% in some regions during recent supply crunches. The specialty resin systems used in high-frequency applications often have limited suppliers, creating bottlenecks. Many manufacturers report lead times for certain base materials extending to 6-9 months, compared to traditional 8-12 week delivery windows.

Other Constraints

Concentration of Production

Over 60% of global PCB manufacturing capacity is concentrated in Asia, primarily China, creating geopolitical and logistical risks. Recent trade tensions and pandemic-related shutdowns have demonstrated the vulnerability of this concentrated supply chain model.

Environmental Regulations

Stricter environmental regulations regarding chemical usage in PCB production are increasing compliance costs. The industry must navigate complex regulations like RoHS and REACH while maintaining product performance, adding to development timelines and expenses.

MARKET CHALLENGES

Technical Complexities in High-Density Interconnect Fabrication

As electronic devices become more sophisticated, PCB manufacturers face increasing challenges in producing reliable high-density interconnect (HDI) boards. The industry is transitioning to finer trace widths and spacings, with leading-edge products now requiring features below 25 micrometers. This precision manufacturing demands expensive equipment upgrades and highly controlled production environments. Yield rates for complex multi-layer boards often lag behind simpler designs, with some advanced PCBs experiencing initial yields below 60% before process optimization.

Additional Manufacturing Hurdles

Thermal Management

Managing heat dissipation in densely packed, multi-layer boards remains a persistent challenge. Power densities continue to increase while device form factors shrink, requiring innovative thermal solutions that often add cost and complexity to designs.

Signal Integrity

Maintaining signal integrity at high frequencies is becoming increasingly difficult. With 5G and millimeter-wave applications pushing into the GHz range, PCB materials and layout techniques must evolve to prevent signal degradation and crosstalk.

MARKET OPPORTUNITIES

Emerging Applications in AI Infrastructure Creating New Demand

The explosive growth of artificial intelligence applications is driving demand for specialized PCBs in data centers and edge computing devices. AI servers require boards capable of handling high-power GPU clusters and high-speed interconnects, with some designs incorporating 20+ layers. The AI hardware market is projected to grow at over 30% CAGR through 2030, representing a significant opportunity for PCB manufacturers capable of meeting these technical requirements. Cloud service providers are working closely with PCB suppliers to develop customized solutions for their AI infrastructure needs.

Advanced Packaging Technologies Opening New Frontiers

The convergence of PCB and semiconductor packaging technologies is creating opportunities for innovation. Technologies like embedded die packaging and chip-first fan-out approaches are blurring the lines between PCBs and packages. Manufacturers investing in these hybrid approaches can capture value in both markets. The global advanced packaging market is expected to surpass $65 billion by 2027, with PCB-like substrates playing an increasingly important role. This trend is particularly significant for high-performance computing, automotive, and medical electronics applications where miniaturization and performance are paramount.

➤ Several leading PCB manufacturers have established dedicated business units for advanced packaging solutions, recognizing it as a strategic growth area with higher margins than traditional PCB products.

MULTI-SIDED PRINTED CIRCUIT BOARD MARKET TRENDS

Advancements in High-Density Interconnect (HDI) Technology Driving Market Growth

The multi-sided printed circuit board (PCB) market is experiencing strong demand due to rapid advancements in High-Density Interconnect (HDI) technology. As electronic devices become smaller yet more powerful, PCBs with higher layer counts (ranging from 4 to over 20 layers) are essential for enabling complex circuit routing in constrained spaces. The global HDI PCB market is projected to grow at a CAGR exceeding 10% through 2030, with multi-layer variants accounting for over 65% of this segment. Recent innovations like embedded passives and through-silicon vias (TSVs) are further enhancing board performance while reducing form factor, particularly crucial for applications like 5G infrastructure and AI hardware accelerators.

Other Trends

Electric Vehicle Revolution Accelerates Demand

The automotive sector’s electrification is creating unprecedented demand for sophisticated PCBs. Modern electric vehicles contain approximately 50% more PCB content than conventional vehicles, with battery management systems, autonomous driving modules, and infotainment clusters all requiring multi-layer solutions. Tier 1 suppliers report that automotive now represents over 25% of advanced PCB orders, up from just 12% five years ago. This vertical’s growth is particularly driving adoption of heavy copper and thermally enhanced multi-layer boards capable of handling high currents and harsh operating environments.

Geopolitical Shifts Reshaping Supply Chains

While Asia continues to dominate PCB production with over 75% market share, geopolitical tensions are prompting strategic supply chain diversification. North American and European manufacturers are investing in localized production capabilities, with recent policies like the U.S. CHIPS Act allocating significant funding for domestic semiconductor infrastructure. This transition towards regionalized supply networks presents both challenges in short-term capacity constraints and opportunities for technological leapfrogging through advanced manufacturing techniques like additive PCB fabrication.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand Production Capacities to Meet Rising Global Demand

The multi-sided printed circuit board (PCB) market exhibits moderate consolidation, dominated by established manufacturers with extensive technical expertise and global supply chains. Zhen Ding Technology Holding Limited and TTM Technologies collectively command over 25% of global market share in 2024, leveraging their vertically integrated manufacturing capabilities across Asia and North America.

Unimicron and AT&S maintain strong positions through continuous innovation in high-density interconnect (HDI) technologies, particularly for 5G infrastructure and automotive applications. Both companies have announced capacity expansions in 2024, with Unimicron investing $500 million in new Southeast Asian facilities to meet growing IT and telecom sector demand.

Japanese manufacturers NOK Corporation and Sumitomo Corporation differentiate through advanced flexible PCB solutions for consumer electronics and medical devices. These firms benefit from long-standing relationships with OEMs and material science expertise.

Emerging players like Career Technology are gaining traction through targeted investments in automation and sustainable manufacturing processes, reducing lead times by 30% compared to industry averages.

List of Key Multi-sided PCB Manufacturers

- Zhen Ding Technology Holding Limited (Taiwan)

- TTM Technologies (U.S.)

- Unimicron Technology Corporation (Taiwan)

- AT&S Austria Technologie & Systemtechnik AG (Austria)

- NOK Corporation (Japan)

- Sumitomo Corporation (Japan)

- Würth Elektronik GmbH & Co. KG (Germany)

- Career Technology (Taiwan)

- Fujikura Ltd. (Japan)

- Nitto Denko Corporation (Japan)

- Jabil Circuit (U.S.)

- Murrietta Circuits (U.S.)

- Advanced Circuits (U.S.)

Segment Analysis:

By Type

Rigid PCBs Dominate the Market Due to Widespread Adoption in High-End Electronic Applications

The market is segmented based on type into:

- Rigid PCBs

- Subtypes: Standard multilayer, HDI, IC substrates

- Flexible PCBs

- Subtypes: Single-sided flex, double-sided flex, multilayer flex, rigid-flex

- High-Frequency PCBs

- Others

By Application

Consumer Electronics Segment Leads Market Growth Fueled by Smart Device Proliferation

The market is segmented based on application into:

- Consumer Electronics

- Automotive

- Aerospace and Defense

- Industrial Electronics

- IT and Telecom

- Others

By Layer Count

4-8 Layer PCBs Hold Significant Market Share Balancing Complexity and Cost-Effectiveness

The market is segmented based on layer count into:

- 4-8 Layer PCBs

- 8-16 Layer PCBs

- 16+ Layer PCBs

- Others

By End User

OEMs Represent the Largest Segment Driving PCB Innovation and Production

The market is segmented based on end user into:

- Original Equipment Manufacturers (OEMs)

- Electronic Manufacturing Services (EMS)

- Fabrication Houses

- Others

Regional Analysis: Multi-sided Printed Circuit Board Market

North America

The North American multi-sided PCB market is characterized by high-tech manufacturing standards and significant demand from defense, aerospace, and telecommunications sectors. The U.S. dominates regional consumption, accounting for nearly 65% of the market share due to its robust electronics manufacturing industry and government investments in 5G infrastructure. Key challenges include rising material costs and labor shortages, which have prompted manufacturers to explore automation solutions. Major players like TTM Technologies and Advanced Circuits are leading innovation in high-layer-count PCBs for advanced applications, supported by R&D investments totaling over $2 billion annually across the semiconductor ecosystem.

Europe

European PCB manufacturers face stricter environmental regulations under RoHS and WEEE directives, pushing the adoption of halogen-free and lead-free laminate materials. Germany remains the production hub, with specialized suppliers like Würth Elektronik focusing on automotive-grade PCBs for electric vehicles – a sector projected to grow at 15% CAGR through 2030. However, energy price volatility and component shortages are causing supply chain bottlenecks. The region shows strong potential in medical electronics, where multi-layer flex-rigid PCBs are increasingly required for portable diagnostic equipment.

Asia-Pacific

Accounting for over 60% of global PCB production, the APAC region benefits from established supply chains and lower production costs. China’s PCB output surpassed $35 billion in 2023, driven by domestic smartphone manufacturers and EV producers. While Japan and South Korea specialize in high-end substrates for semiconductor packaging, Southeast Asian nations are emerging as alternative manufacturing bases amid geopolitical tensions. The proliferation of IoT devices and 5G base stations across India and China continues to fuel demand for cost-effective 6-8 layer PCBs, though overcapacity concerns loom in standard product segments.

South America

PCB adoption in South America remains constrained by limited local manufacturing capabilities and reliance on imports, particularly from China. Brazil represents the largest market, with growth centered around automotive electronics and industrial automation applications. However, currency fluctuations and inconsistent infrastructure investment have deterred major PCB manufacturers from establishing local production facilities. The market shows gradual improvement as regional trade agreements facilitate component sourcing, with Argentina demonstrating particular promise in medical device assembly requiring specialized PCBs.

Middle East & Africa

This emerging market is witnessing strategic investments in electronics manufacturing, particularly in Israel’s military/aerospace sector and the UAE’s telecom infrastructure projects. While PCB consumption remains modest compared to other regions, growth rates exceed 8% annually due to smart city initiatives and oil/gas industry automation. Local production is virtually nonexistent beyond simple 2-4 layer boards, creating opportunities for Asian and European suppliers. South Africa serves as a regional hub for PCB distribution, though political instability in parts of Africa continues to hinder broader market development.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Multi-sided Printed Circuit Board (PCB) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Multi-sided PCB market was valued at US$ 8.73 billion in 2024 and is projected to grow significantly by US$ 16.42 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (rigid, flexible), technology, application (industrial electronics, consumer electronics, automotive, aerospace & defense, IT & telecom), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with China currently holding the largest market share.

- Competitive Landscape: Profiles of 16 leading market participants including Advanced Circuits, AT&S, TTM Technologies, and Unimicron, covering their product portfolios, manufacturing capacities, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging PCB technologies, integration with AI/5G applications, advanced fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of growth drivers (5G rollout, EV adoption, IoT expansion) along with challenges (supply chain constraints, material costs, geopolitical factors).

- Stakeholder Analysis: Strategic insights for PCB manufacturers, OEMs, component suppliers, investors, and policymakers regarding market opportunities.

The research employs both primary and secondary methodologies, including interviews with industry experts, analysis of financial reports, and validation through multiple data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Multi-sided PCB Market?

-> Multi-sided Printed Circuit Board Market size was valued at US$ 8.73 billion in 2024 and is projected to reach US$ 16.42 billion by 2032, at a CAGR of 9.47% during the forecast period 2025–2032.

Which key companies operate in Global Multi-sided PCB Market?

-> Key players include TTM Technologies, Unimicron, AT&S, Zhen Ding Technology, Nippon Mektron, and Tripod Technology, with Chinese manufacturers holding dominant market share.

What are the key growth drivers?

-> Primary growth drivers include 5G infrastructure deployment, electric vehicle production, AI hardware requirements, and IoT device proliferation across industries.

Which region dominates the market?

-> Asia-Pacific accounts for over 60% of global PCB production, with China as the manufacturing hub, followed by Taiwan, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include high-density interconnect (HDI) PCBs, flexible circuits for wearables, automotive ADAS systems, and sustainable manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...