MARKET INSIGHTS

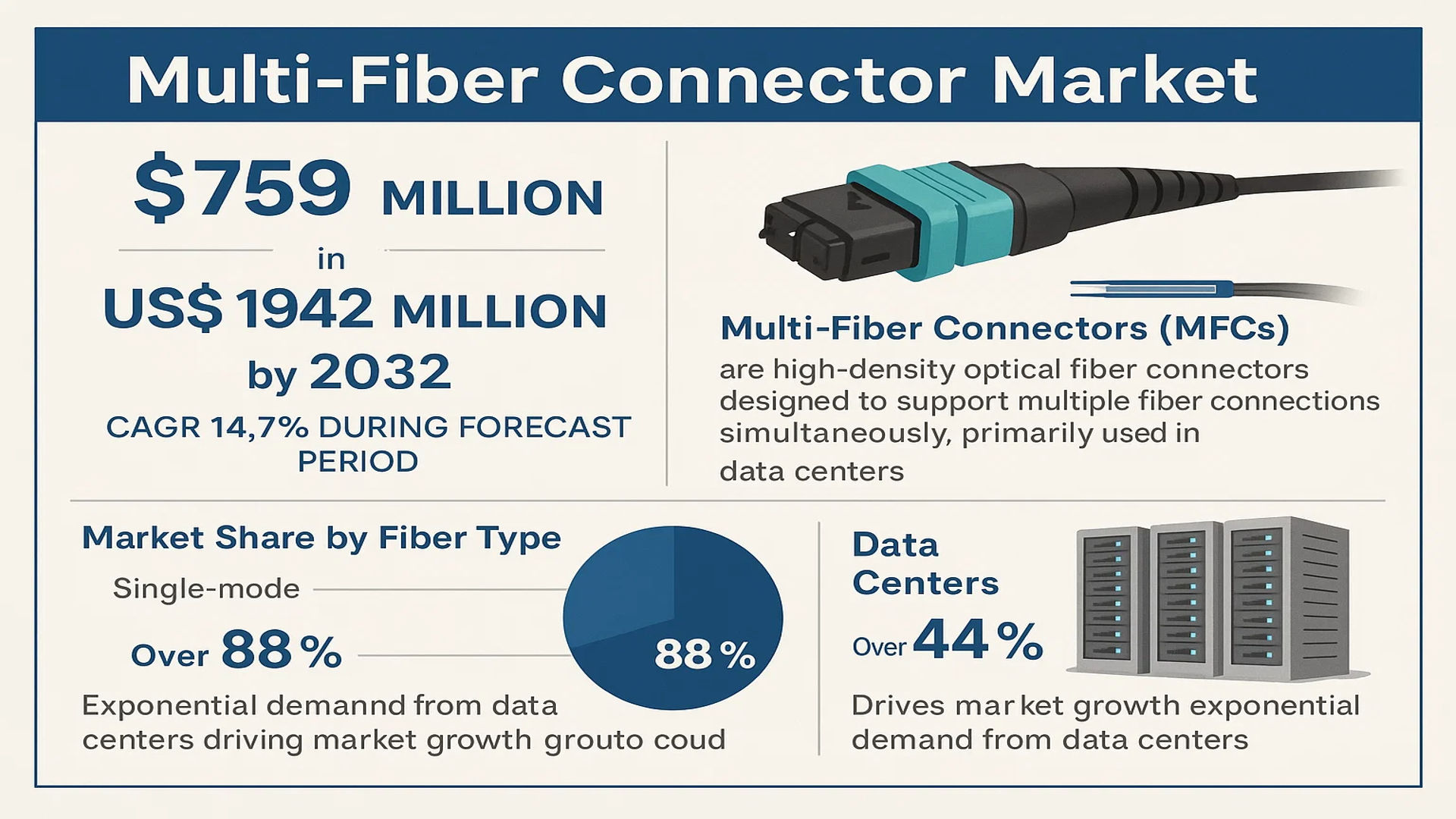

The global Multi-Fiber Connector Market was valued at 759 million in 2024 and is projected to reach US$ 1942 million by 2032, at a CAGR of 14.7% during the forecast period.

Multi-Fiber Connectors (MFCs) are high-density optical fiber connectors designed to support multiple fiber connections simultaneously, primarily used in data centers and telecommunications infrastructure. These connectors, including MPO (Multi-fiber Push-On) and MTP (Multi-fiber Termination Push-on) variants, enable efficient high-speed data transmission by reducing space requirements and installation time compared to single-fiber solutions. The technology supports both single-mode and multimode fiber applications, with multimode accounting for over 88% of market share due to its cost-effectiveness in short-range data transmission.

The market growth is driven by exponential demand from data centers, which hold over 44% market share, as hyperscale facilities expand globally to support cloud computing and 5G networks. However, supply chain disruptions from geopolitical conflicts impacted production in 2022. Asia-Pacific dominates the market with 42% share, led by China’s rapid digital infrastructure development. Key players like US Conec, Senko, and Amphenol are investing in next-generation connectors to support 400G and 800G Ethernet standards, with recent innovations including reduced-height MPO connectors for high-density applications.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth of Data Centers Driving Multi-Fiber Connector Demand

The global data center infrastructure market has witnessed unprecedented growth, with investments projected to surpass $400 billion by 2025. This surge is directly fueling demand for high-density fiber optic connectivity solutions, particularly multi-fiber push-on (MPO) connectors. Data centers increasingly require these compact, high-performance connectors to support hyperscale cloud computing and 5G backhaul networks. Each new hyperscale data center typically requires between 50,000 to 100,000 fiber connections, making multi-fiber connectors essential components for efficient rack-to-rack and switch-to-switch connectivity.

5G Network Rollouts Accelerating Deployment

The global transition to 5G technology represents another significant growth driver for multi-fiber connectors. As service providers worldwide invest over $300 billion annually in 5G infrastructure, the need for high-bandwidth fiber optic connectivity between cell towers and central offices has intensified. Modern 5G fronthaul and backhaul networks increasingly rely on MPO connectors due to their ability to handle multiple fiber connections in compact form factors. This trend is especially prominent in Asia-Pacific, where countries like China and South Korea are aggressively expanding 5G networks.

Furthermore, technological advancements in connector design have improved performance characteristics. Recent innovations include reduced insertion loss (now commonly below 0.5 dB) and enhanced durability (exceeding 500 mating cycles), making these connectors even more attractive for critical infrastructure applications.

MARKET RESTRAINTS

Installation Complexity and High Precision Requirements Limit Adoption

While multi-fiber connectors offer significant space savings, their deployment comes with technical challenges that restrain market growth. Proper installation requires highly precise alignment of multiple fibers (typically 12 or 24 per connector), necessitating specialized tools and trained technicians. Each MPO connection typically requires 30-40% more installation time compared to standard single-fiber connectors. Moreover, improper handling can lead to fiber damage or contamination, resulting in signal degradation – a critical concern when loss budgets are often less than 3 dB for modern optical networks.

Supply Chain Disruptions Impacting Component Availability

The global semiconductor shortage has extended to fiber optic components, affecting the production of precision ferrules and alignment sleeves crucial for multi-fiber connectors. Lead times for certain connector types have extended from 4-6 weeks to 12-16 weeks, creating bottlenecks for network deployment projects. This supply chain constraint, combined with rising prices for specialized ceramics used in connector manufacturing (up 18-22% since 2022), has created budget challenges for telecom operators and data center builders.

MARKET OPPORTUNITIES

Next-Generation Data Center Architectures Creating New Demand

The shift toward disaggregated data center designs presents significant growth opportunities for multi-fiber connector manufacturers. Modern hyperscale facilities are adopting optical fabric architectures that require 50-70% more fiber connections than traditional designs. These next-generation topologies favor MPO-based connectivity solutions for their ability to support high-density, high-bandwidth spine-and-leaf networks. Industry forecasts suggest data center operators will deploy over 5 million new MPO connectors annually by 2026 to support these architectures.

Emerging Applications in Quantum Networking and Li-Fi

Cutting-edge technologies like quantum key distribution networks and Li-Fi (light fidelity) systems are creating new application areas for multi-fiber connectors. These next-generation communication systems require ultra-low-loss, high-reliability optical connections – specifications that align well with advanced MPO connector designs. Research institutions and technology companies are increasingly specifying multi-fiber interfaces for prototype quantum networks, particularly in government-funded projects where security and bandwidth requirements exceed traditional networking capabilities.

MARKET CHALLENGES

Standardization Fragmentation Complicates Market Growth

The multi-fiber connector market faces significant challenges from competing standards and proprietary designs. While the IEC 61754-7 standard defines the primary MPO interface, numerous variants exist for different applications (SM/MM), fiber counts (8/12/24/72), and polarity schemes. This fragmentation creates compatibility issues, with network operators reporting that 15-20% of installation delays stem from connector mismatches. The situation is further complicated by emerging competing standards like SN-MT and MDC connectors, creating uncertainty for purchasers and slowing adoption rates.

Environmental Sensitivity Affects Reliability

While multi-fiber connectors deliver excellent performance in controlled environments, their reliability in harsh conditions remains a concern. Field studies show that connectors exposed to industrial settings or outdoor installations experience failure rates 3-5 times higher than in climate-controlled data centers. Particulate contamination, temperature cycling, and mechanical stress can significantly degrade performance – particularly for modern high-density designs with fiber pitches below 250μm. These reliability challenges have slowed adoption in certain industrial IoT and mobile fronthaul applications where environmental sealing remains inadequate.

MULTI-FIBER CONNECTOR MARKET TRENDS

Rapid Expansion of Data Centers Fueling Multi-Fiber Connector Adoption

The global multi-fiber connector market is experiencing substantial growth, driven primarily by the exponential rise in data center deployments. As cloud computing, artificial intelligence, and 5G networks become ubiquitous, hyperscale data centers are demanding high-density, high-bandwidth optical connectivity solutions. Multi-fiber push-on (MPO) connectors, capable of supporting up to 72 fibers in a single interface, have become the industry standard for 40G/100G/400G Ethernet applications. Recent market analysis projects that data centers will account for over 44% of multi-fiber connector consumption by 2024, with the Asia-Pacific region leading installations due to massive digital infrastructure investments in China and India.

Other Trends

Telecom Network Modernization

Telecommunication operators worldwide are upgrading their networks to support fiber-to-the-home (FTTH) and 5G backhaul requirements, creating robust demand for multi-fiber connectivity solutions. The transition from traditional single-fiber connectors to high-density MPO solutions enables space savings of up to 60% in central offices and cell tower equipment. With 5G networks requiring approximately four times more fiber than 4G deployments, telecommunications now represents the second-largest application segment after data centers. Major carriers are accelerating fiber optic deployments, with projections indicating sustained 12-15% annual growth in telecom-related multi-fiber connector demand through 2030.

Technological Innovation in Connector Design

Manufacturers are developing next-generation multi-fiber connectors with enhanced performance characteristics to meet evolving industry requirements. Recent product innovations include reduced-size MPO connectors for space-constrained applications, angled-polish connectors that minimize insertion loss, and environmentally sealed versions for harsh outdoor installations. The industry is also seeing increased adoption of single-mode multi-fiber connectors, particularly for long-haul telecom and data center interconnect applications, though multimode variants continue to dominate with 88% market share for shorter-reach applications. Emerging technologies like photonic integrated circuits (PICs) are driving new connector form factors that combine multiple optical functions into single interfaces.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Accelerate Innovation to Meet Rising Demand for High-Speed Connectivity

The global Multi-Fiber Connector (MFC) market features a dynamic competitive environment, with established players and emerging contenders vying for market share. US Conec and T&S Communications currently dominate the landscape, collectively accounting for over 20% of the global market revenue in 2024. These companies have solidified their positions through continuous product innovation and strategic partnerships with data center operators.

Sumitomo Electric and Amphenol follow closely, leveraging their extensive manufacturing capabilities and strong distribution networks across Asia-Pacific and North America. Their ability to offer customized solutions for hyperscale data centers gives them a competitive edge in this rapidly evolving market segment.

Recent industry developments show that companies are increasingly focusing on miniaturization and higher density connector designs. Senko Advanced Components made significant strides in 2023 with its new CS connector series, which offers 25% more density than conventional MPO connectors. Meanwhile, Siemon has been expanding its production capacity in Europe to meet growing demand from 5G network deployments.

The market also sees active participation from Chinese manufacturers such as Suzhou Agix Optical and China Aviation Optical, who are capitalizing on domestic demand while increasing exports to emerging markets. Their competitive pricing strategies have made them formidable players, particularly in Southeast Asia and Africa.

List of Key Multi-Fiber Connector Companies Profiled

- US Conec (U.S.)

- T&S Communications (U.S.)

- Sumitomo Electric (Japan)

- Senko Advanced Components (U.S.)

- Amphenol (U.S.)

- Siemon (U.S.)

- Belden Inc. (U.S.)

- Molex (U.S.)

- Panduit (U.S.)

- Optical Cable Corporation (U.S.)

- China Aviation Optical (China)

- Suzhou Agix Optical (China)

- Suzhou TFC Optical Comms (China)

Segment Analysis:

By Type

Multimode Segment Leads the Market Due to Wide Adoption in High-Density Data Transmission Applications

The market is segmented based on type into:

- Single-Mode

- Subtypes: SMF-28, OS2, and others

- Multimode

- Subtypes: OM1, OM2, OM3, OM4, OM5, and others

By Application

Data Centers Segment Dominates Due to Increasing Demand for High-Speed Connectivity Solutions

The market is segmented based on application into:

- Data Centers

- Telecommunications

- Aerospace & Military

- Others

By Connector Type

MPO Connectors Gain Traction for Their High-Density Fiber Deployment Capabilities

The market is segmented based on connector type into:

- MPO

- MTP

- Others

By End-User

Enterprise Networks Show Growth Potential with Rising Digital Transformation Initiatives

The market is segmented based on end-user into:

- IT & Telecom

- Healthcare

- Manufacturing

- BFSI

- Others

Regional Analysis: Multi-Fiber Connector Market

Asia-Pacific

As the largest market for multi-fiber connectors, accounting for approximately 42% of global demand, Asia-Pacific dominates due to rapid digital transformation and extensive telecommunications infrastructure development. Countries like China, Japan, and India are driving growth through massive data center expansions and government initiatives promoting 5G rollout. The region’s preference for multimode connectors (88% market share) reflects cost-effective solutions for high-density applications. While local manufacturers compete aggressively on price, global players are strengthening partnerships to capitalize on rising demand for high-speed connectivity solutions in emerging economies. China’s “Digital Silk Road” initiative further accelerates fiber optic deployment across Southeast Asia.

North America

With a strong emphasis on next-generation network infrastructure, North America represents the second-largest market for multi-fiber connectors. The U.S. leads regional adoption, particularly in data centers (44% application share) and telecommunications, supported by cloud computing growth and hyperscale data center investments. Technological advancements in MPO connectors and standardization efforts by bodies like TIA drive product innovation. However, supply chain disruptions and trade policies affecting fiber optic component imports present ongoing challenges. The market shows increasing preference for compact, high-density connectors to support AI/ML workload requirements in enterprise networks.

Europe

European demand focuses on high-performance connectors meeting strict EU RoHS and REACH compliance standards. Germany and the UK lead adoption in industrial and telecommunications sectors, with growing emphasis on sustainable manufacturing processes. The region shows particular interest in single-mode connectors for long-haul applications, though cost sensitivity in Southern Europe maintains multimode dominance. European telecom operators’ accelerated fiber-to-the-home (FTTH) deployments and data center construction in Nordic countries create sustained demand. However, energy efficiency regulations and component certification requirements add complexity to market entry for non-European suppliers.

Middle East & Africa

This emerging market demonstrates increasing demand for fiber optic infrastructure, particularly in Gulf Cooperation Council (GCC) countries undertaking smart city initiatives. The UAE and Saudi Arabia lead regional adoption, with multi-fiber connectors being deployed in aerospace, defense, and telecommunications applications. While market penetration remains lower than other regions, growing investments in subsea cable systems and data center hubs present significant opportunities. Challenges include reliance on imports and limited local technical expertise for high-density fiber installations. The market shows potential for growth with increasing digitalization and government-backed broadband expansion projects.

South America

The region exhibits moderate growth, with Brazil and Argentina driving demand through telecommunications network upgrades. Economic volatility and currency fluctuations impact procurement of high-end connector solutions, making cost-effective multimode variants preferred. Growing cloud service adoption and mobile broadband expansion create opportunities, though infrastructure development lags behind other regions. Local manufacturing remains limited, creating dependence on imports from Asia and North America. The market requires tailored solutions balancing performance with affordability to overcome budgetary constraints in both private and public sector deployments.

Report Scope

This market research report provides a comprehensive analysis of the global Multi-Fiber Connector market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Multi-Fiber Connector market was valued at USD 759 million in 2024 and is projected to reach USD 1942 million by 2032, growing at a CAGR of 14.7% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Single-Mode, Multimode), application (Data Center, Telecommunication, Aerospace & Military, Others), and end-user industry to identify high-growth segments and investment opportunities. Multimode connectors dominate with 88% market share, while Data Centers account for 44% of applications.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific leads with 42% market share, followed by North America and Europe.

- Competitive Landscape: Profiles of leading market participants including T&S Communications, US Conec, Senko, Amphenol, and Sumitomo Electric, covering their product offerings, R&D focus, manufacturing capacity, and recent developments. The top three players hold 36% market share collectively.

- Technology Trends & Innovation: Assessment of emerging technologies in fiber optic connectivity, including high-density solutions and advancements in MPO connector designs.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as 5G deployment and data center expansion, along with challenges including supply chain constraints and raw material pricing.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding the evolving ecosystem and strategic opportunities in fiber optic connectivity solutions.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Multi-Fiber Connector Market?

-> Multi-Fiber Connector Market was valued at 759 million in 2024 and is projected to reach US$ 1942 million by 2032, at a CAGR of 14.7% during the forecast period.

Which key companies operate in Global Multi-Fiber Connector Market?

-> Key players include T&S Communications, US Conec, Senko Advanced Components, Amphenol, Sumitomo Electric, Siemon, and Suzhou Agix Optical, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand from data centers, 5G network deployment, and rising adoption of high-speed connectivity solutions.

Which region dominates the market?

-> Asia-Pacific is the largest market with 42% share, driven by rapid digital infrastructure development in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of higher density connectors, adoption in hyperscale data centers, and integration with emerging 5G and IoT applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...