MARKET INSIGHTS

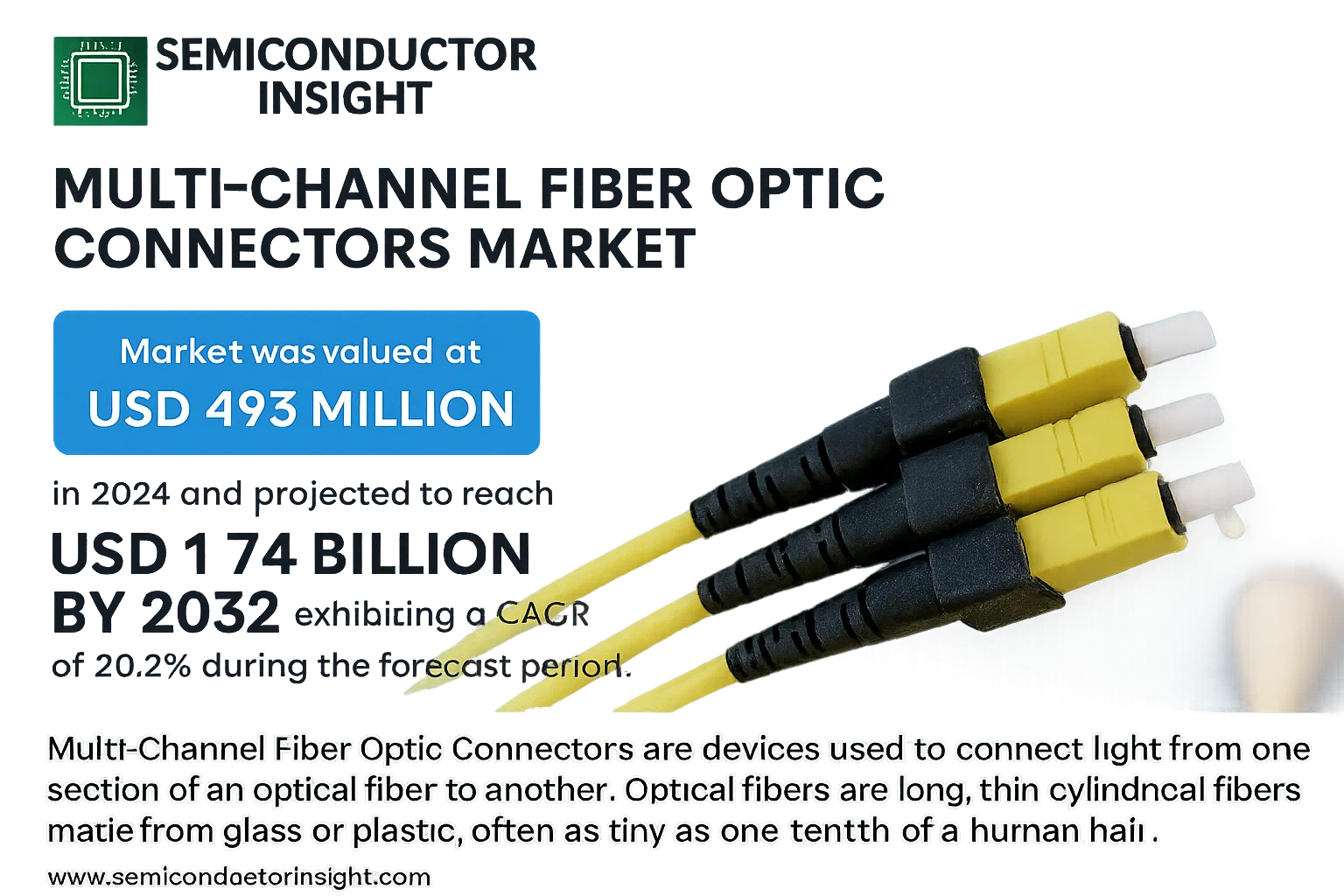

Global Multi-Channel Fiber Optic Connectors Market was valued at USD 493 million in 2024 and is projected to reach USD 1.74 billion by 2032, exhibiting a CAGR of 20.2% during the forecast period.

Multi-Channel Fiber Optic Connectors are devices used to connect light from one section of an optical fiber to another. Optical fibers are long, thin cylindrical fibers made from glass or plastic, often as tiny as one tenth of a human hair. Since optical fibers are so tiny, fiber optic connectors must be manufactured with high precision, at the scale of 0.1μm, which is one hundredth of the width of a human hair.

The market is experiencing rapid growth due to several factors, including the expansion of data centers and cloud computing, the ongoing rollout of 5G telecommunications infrastructure, and the adoption of fiber optics in military and aerospace applications for their lightweight and high-bandwidth properties. Additionally, the rising demand for high-speed data transmission across various industries is contributing to market expansion. Initiatives by key players in the market are also expected to fuel the market growth. For instance, the development of new standards like the Multi-fiber Push On (MPO) connector, which can support up to 64 channels in a single connector, is enabling higher density and reducing the size of data center hardware.

MARKET DRIVERS

Exponential Growth in Data Traffic

The relentless surge in global data consumption, propelled by 5G deployment, high-definition video streaming, cloud computing, and the Internet of Things (IoT), is a primary driver for the multi-channel fiber optic connector market. Data centers and telecommunications networks require higher port density and greater bandwidth efficiency to handle this traffic, directly fueling demand for multi-channel solutions like MTP/MPO connectors that can accommodate 12, 24, or more fibers in a single interface.

Demand for High-Density Connectivity Solutions

Space and cost constraints within data centers and central offices are pushing the adoption of high-density interconnect systems. Multi-channel fiber optic connectors significantly reduce the physical footprint required for fiber management compared to single-fiber connectors. This high density is critical for modern hyperscale data centers and fiber-to-the-home (FTTH) deployments, where maximizing port count per rack unit is essential for operational and economic efficiency.

➤ The global market for multi-channel fiber optic connectors is projected to grow at a compound annual growth rate (CAGR) of approximately 10.5% over the next five years, driven by these infrastructure upgrades.

Furthermore, the transition to higher-speed network standards, such as 400GbE and 800GbE, which heavily rely on parallel optics technology, mandates the use of multi-fiber connectors. This technological evolution ensures a sustained and growing demand for reliable, high-performance multi-channel connectivity.

MARKET CHALLENGES

Precision Manufacturing and High Initial Costs

The production of multi-channel fiber optic connectors requires extremely high precision in the alignment of multiple optical fibers within a single ferrule. This manufacturing complexity leads to higher costs compared to single-fiber connectors. The need for specialized polishing and testing equipment further adds to the capital expenditure for manufacturers and can be a barrier to entry for smaller players.

Other Challenges

Installation and Maintenance Complexity

Deployment of multi-channel systems requires skilled technicians trained in proper handling, cleaning, and testing procedures. Contamination of a single fiber end-face within a multi-fiber connector can degrade the performance of the entire channel, leading to increased installation time and potential network downtime if not managed correctly.

Standardization and Interoperability Issues

While standards like IEC 61754-7 for MTP/MPO connectors exist, ensuring perfect interoperability between products from different manufacturers remains a challenge. Slight variations in ferrule geometry or pin alignment can lead to higher insertion loss and performance inconsistencies, requiring careful vendor selection and quality control.

MARKET RESTRAINTS

Economic Volatility and Supply Chain Disruptions

Global economic uncertainties and fluctuations in raw material costs, particularly for specialized glasses and precision ceramics used in ferrules, can impact the stable pricing of multi-channel connectors. Furthermore, the industry has experienced supply chain disruptions affecting the availability of key components, potentially delaying large-scale network deployment projects and acting as a temporary restraint on market growth.

Competition from Alternative Technologies

While multi-channel connectors are dominant in high-density applications, ongoing research into wireless communication technologies like 5G and free-space optics presents a long-term competitive landscape. In some short-reach, lower-density scenarios, advanced copper-based solutions continue to be a cost-effective alternative, restraining the expansion of fiber optics in certain market segments.

MARKET OPPORTUNITIES

Expansion in Emerging Economies

Rapid digitalization, government initiatives for national broadband networks, and growing investments in data center infrastructure in emerging economies across Asia-Pacific, Latin America, and Africa present significant growth opportunities. These regions are building out their digital backbones, creating a substantial new market for high-density fiber optic connectivity solutions.

Adoption in New Application Areas

Beyond traditional data centers and telecom, multi-channel connectors are finding new applications in areas such as high-performance computing (HPC), aerospace and defense avionics, and medical imaging systems. The need for high-speed, reliable data transmission in these specialized fields opens up diverse and high-value market segments for connector manufacturers.

Technological Advancements

Innovations aimed at reducing insertion loss, improving durability, and simplifying field termination (such as no-epoxy/no-polish connectors) are creating opportunities for product differentiation. The development of connectors compatible with even higher fiber counts and new fiber types, like hollow-core fiber, will be crucial for supporting next-generation network architectures.

Multi-Channel Fiber Optic Connectors Market Trends

Surging Market Growth Fueled by Data Center and Telecommunications Demand

The global multi-channel fiber optic connectors market is experiencing robust expansion, with its value projected to rise from $493 million in 2024 to $1,742 million by 2032, representing a compound annual growth rate of 20.2%. This strong growth trajectory is primarily driven by the exponential increase in data consumption and the global rollout of high-speed telecommunications infrastructure, including 5G networks. The Asia-Pacific region dominates the market, accounting for approximately 60% of the global share, which reflects aggressive digital infrastructure investments by countries such as China and India. North America follows with a 24% share, supported by advanced data center build-outs.

Other Trends

High-Density Connectivity Requirements

A key trend is the shift towards connectors with a higher number of channels, such as 24-channel and 48-channel designs, to meet the demand for increased port density in data centers. This minimizes physical space requirements while maximizing data throughput. The market is segmented by type, with 8-channel, 12-channel, 24-channel, and 48-channel connectors catering to different application needs for scalability and efficiency.

Application-Specific Expansion

Demand is segmented across data centers, telecommunications, military/aerospace, and other sectors. Data centers represent the largest application segment, as they require reliable, high-speed interconnects for server farms and storage area networks. The telecommunications sector is also a major driver, fueled by the ongoing deployment of fiber-to-the-home (FTTH) and 5G infrastructure, which depend on high-performance optical connectivity.

Market Consolidation and Competitive Landscape

The competitive landscape is characterized by a high degree of concentration, with the top three companies—T&S Communications, US Conec, and Senko—collectively holding over 40% of the market share. Other significant players include Siemon, Amphenol, and Sumitomo Electric. This consolidation is leading to increased investment in research and development to create more precise and reliable connectors, which must be manufactured to tolerances as fine as 0.1um to ensure optimal performance with optical fibers that are as tiny as one-tenth of a human hair.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Dominated by a Handful of Technologically Advanced Leaders

The global multi-channel fiber optic connectors market is characterized by a moderately concentrated competitive environment, where the top three players collectively command a significant share of over 40%. T&S Communications, US Conec, and Senko are recognized as the dominant leaders, leveraging their extensive product portfolios, strong R&D capabilities, and established global supply chains. This leadership is largely driven by the critical need for precision manufacturing, as these connectors operate at a microscopic scale. The high growth forecast for the market, projected at a CAGR of 20.2%, is intensifying competition, with leading players focusing on innovation in high-density solutions for data centers and telecommunications, which are the primary application segments.

Beyond the top-tier companies, the market includes a number of significant niche and diversified players that contribute to its dynamic nature. Established electronics component manufacturers like Amphenol, Sumitomo Electric, and Molex bring their vast engineering and distribution resources to the market. Regional specialists, particularly in the Asia-Pacific region which accounts for about 60% of the market, such as Suzhou Agix and AVIC JONHON, are also key participants. These companies often compete on cost-effectiveness and cater to specific regional demands, while others like Siemon and Panduit are well-known for their structured cabling solutions that integrate multi-channel connectors.

List of Key Multi-Channel Fiber Optic Connectors Companies Profiled

- T&S Communications

- US Conec

- Senko

- Siemon

- Amphenol

- Sumitomo Electric

- Suzhou Agix

- Nissin Kasei

- Molex

- Panduit

- AVIC JONHON

- Optical Cable Corporation

- TFC

- Hakusan

- Longxing

- JINTONGLI

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Higher channel count connectors like the 24-channel and 48-channel variants are demonstrating the strongest market momentum. This trend is fueled by the escalating demand for immense data throughput in hyperscale data centers and advanced telecommunications infrastructure, where maximizing port density and minimizing physical footprint are paramount. These connectors represent the cutting edge, enabling the high-speed backbone networks required for cloud computing and next-generation services. |

| By Application |

|

Data Centers constitute the primary engine of growth for this market. The relentless global expansion of cloud services, big data analytics, and IoT applications is driving unprecedented investment in data center infrastructure. Within these facilities, multi-channel connectors are indispensable for high-density patching in server racks and for facilitating the high-speed interconnects between switches, storage systems, and servers, making this the most dynamic and demanding application segment. |

| By End User |

|

Cloud Service Providers are the dominant end-user segment, characterized by their continuous capital expenditure on building and upgrading massive data center campuses to support global digital services. Their demand is driven by the need for scalable, reliable, and high-performance connectivity solutions. Telecom network operators follow closely, modernizing their networks for 5G deployment and fiber-to-the-home initiatives, which also require robust multi-channel connectivity solutions for central offices and aggregation points. |

| By Technology Standard |

|

MPO/MTP connectors are the undisputed industry standard, enjoying widespread adoption due to their proven reliability, interoperability, and ability to support high channel counts. Their design is optimized for parallel optic applications which are critical in data centers. While newer technologies like MXC offer potential for even higher density, the entrenched ecosystem, extensive supplier base, and familiarity with MPO/MTP make it the preferred choice for most new installations and upgrades, ensuring its continued leadership. |

| By Installation Environment |

|

Indoor/Controlled environments represent the largest segment, as the core applications in data centers and telecom central offices are housed in carefully managed conditions. The demand here focuses on high density, ease of installation, and performance. However, the outdoor/harsh environment segment is gaining importance for applications like fiber distribution points in FTTx networks or industrial settings, requiring connectors with superior sealing, durability, and resistance to temperature extremes and contaminants. |

Regional Analysis: Multi-Channel Fiber Optic Connectors Market

Asia-Pacific

The region’s unparalleled manufacturing capabilities, particularly in China, provide a significant cost and supply chain advantage for multi-channel connector production. This integrated ecosystem, from raw materials to finished goods, ensures rapid scalability and supports the high-volume demands of global telecommunications and data center clients, solidifying its position as the world’s primary production hub.

Proactive government policies and massive public-private partnerships are fueling infrastructure modernization across the region. Substantial funding for national fiber optic backbone projects and smart city developments directly translates into robust demand for high-density connectivity solutions, creating a predictable and long-term growth trajectory for the multi-channel connector market.

The explosion of hyperscale data centers and the aggressive rollout of 5G networks are the primary growth engines. The need for high-speed, high-density interconnections within data centers and at cell tower sites is driving the adoption of advanced multi-channel connectors that support greater data throughput and miniaturization, a trend strongly concentrated in the Asia-Pacific.

Leading technology firms and research institutions in the region are heavily invested in developing next-generation optical connectivity standards. This strong focus on R&D fosters a culture of innovation, leading to the creation of more efficient, higher-performance multi-channel connectors and ensuring the region remains at the cutting edge of fiber optic technology.

North America

North America represents a highly advanced and mature market for Multi-Channel Fiber Optic Connectors, characterized by intense demand from hyperscale cloud providers, enterprise data centers, and government agencies. The region’s market dynamics are driven by the relentless expansion of digital infrastructure to support artificial intelligence, machine learning workloads, and the Internet of Things (IoT). Leading technology companies based in the United States are continuously upgrading their networks to handle massive data traffic, which necessitates the deployment of high-density optical interconnects. While the market is well-established, growth is sustained by technological replacement cycles and the need for higher bandwidth efficiency. The presence of major connector manufacturers and stringent quality standards also contributes to a focus on premium, high-performance products tailored for critical applications in telecommunications and data-intensive industries.

Europe

The European market for Multi-Channel Fiber Optic Connectors is shaped by strong regulatory frameworks, such as the European Green Deal and the Digital Compass, which emphasize digital sovereignty and sustainable connectivity. This drives investment in modernizing legacy network infrastructure and building new, energy-efficient data centers. Demand is robust across key economies like Germany, the UK, and France, supported by initiatives for smart manufacturing (Industry 4.0) and growing 5G deployments. The market is characterized by a high emphasis on quality, reliability, and adherence to international standards, with significant activity in research collaborations aimed at developing next-generation optical solutions. European manufacturers often focus on specialized, high-value connectors for industrial and telecommunications applications, catering to a diverse and technologically demanding customer base.

Middle East & Africa

The Multi-Channel Fiber Optic Connectors market in the Middle East & Africa is experiencing rapid growth, primarily fueled by ambitious digital transformation visions in Gulf Cooperation Council (GCC) countries like Saudi Arabia and the UAE. Large-scale projects for smart cities, telecommunications infrastructure upgrades, and new data center constructions are creating substantial demand. In Africa, the market is emerging, driven by investments in undersea cable landings and national broadband projects aimed at improving connectivity. While the region presents significant growth potential, market development is uneven, with advanced economies leading the adoption of high-density connectors. The market dynamics are influenced by the need for robust and reliable infrastructure capable of supporting economic diversification and the growing digital economy across the region.

South America

The South American market for Multi-Channel Fiber Optic Connectors is in a developing phase, with growth largely concentrated in major economies such as Brazil, Argentina, and Chile. Market dynamics are influenced by gradual investments in improving broadband penetration and expanding data center capacities to serve a growing digital population. The region’s challenging geography sometimes complicates large-scale fiber deployment, but initiatives to connect urban and suburban areas are ongoing. Demand is primarily driven by the telecommunications sector’s need to increase network capacity and by the gradual rise of localized cloud services. While adoption is slower compared to other regions, there is a clear upward trajectory as countries prioritize digital infrastructure to support economic growth and close the connectivity gap.

Report Scope

This market research report provides a comprehensive analysis of the Multi-Channel Fiber Optic Connectors Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Multi-Channel Fiber Optic Connectors Market?

->Multi-Channel Fiber Optic Connectors Market was valued at USD 493 million in 2024 and is projected to reach USD 1.74 billion by 2032, exhibiting a CAGR of 20.2% during the forecast period.

Which key companies operate in Multi-Channel Fiber Optic Connectors Market?

-> Key players include T&S Communications, US Conec, Senko, Siemon, Amphenol, and Sumitomo Electric, among others. The global top three companies hold a share over 40%.

What are the key growth drivers?

-> Key growth drivers include increasing demand from data centers, expansion of telecommunications infrastructure, and the need for high-precision connectivity solutions in applications like military/aerospace.

Which region dominates the market?

-> Asia-Pacific is the largest market, with a share of about 60%, followed by North America and Europe with shares of about 24% and 10%, respectively.

What are the emerging trends?

-> Emerging trends include advancements in high-density connector designs, the proliferation of multi-channel configurations (8, 12, 24, 48-channel), and the integration of fiber optics in next-generation network architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...