MARKET INSIGHTS

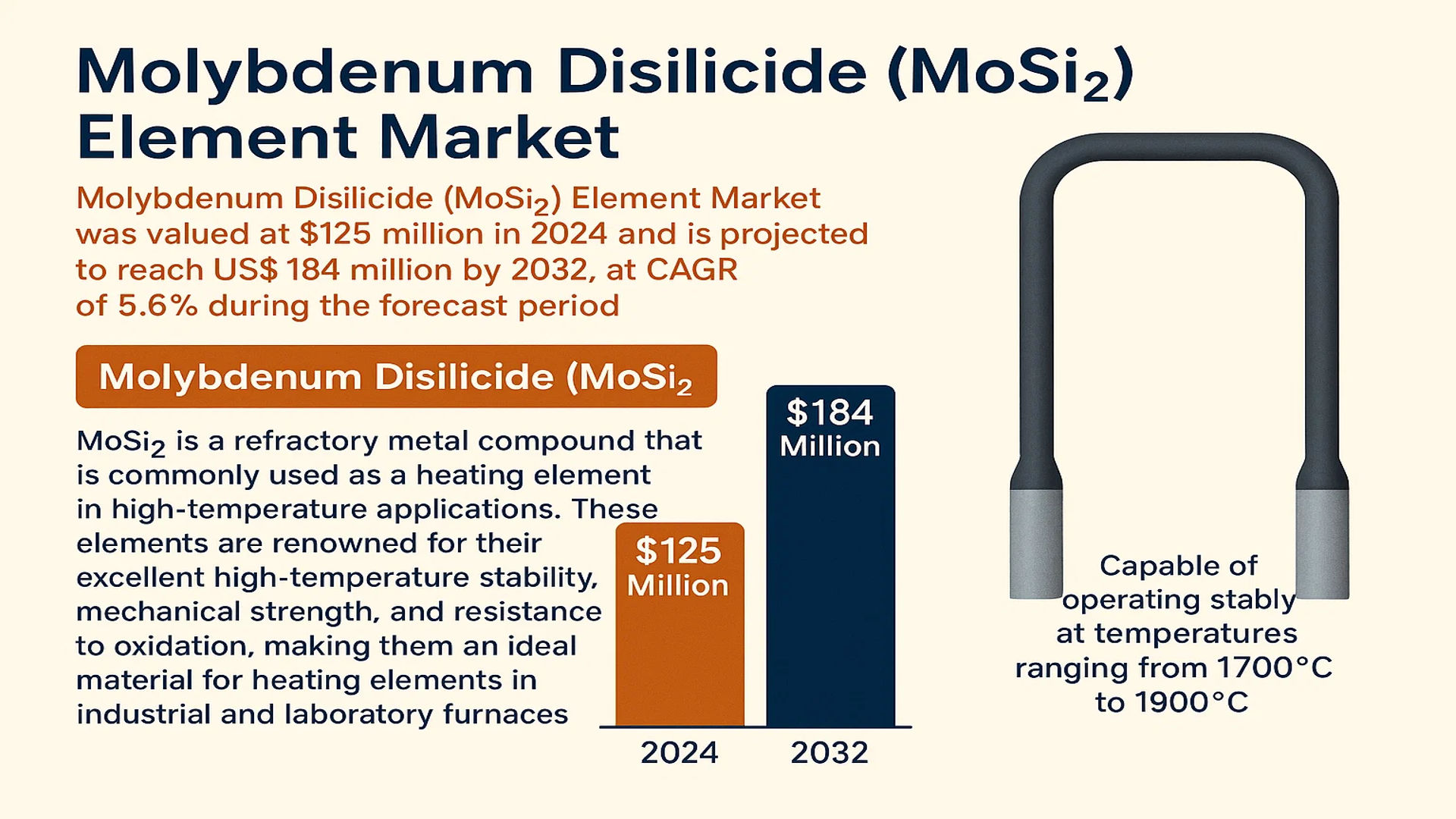

The global Molybdenum Disilicide (MoSi2) Element Market was valued at 125 million in 2024 and is projected to reach US$ 184 million by 2032, at a CAGR of 5.6% during the forecast period.

Molybdenum Disilicide (MoSi2) is a refractory metal compound that is commonly used as a heating element in high-temperature applications. These elements are renowned for their excellent high-temperature stability, mechanical strength, and resistance to oxidation, making them an ideal material for heating elements in industrial and laboratory furnaces. They are capable of operating stably at temperatures ranging from 1700°C to 1900°C.

The market is experiencing steady growth due to several factors, including the robust demand from the industrial furnace sector, which holds a dominant 76% market share. Furthermore, rapid industrialization in emerging economies, particularly in the Asia-Pacific region which accounts for approximately 42% of global consumption, is a primary growth driver. Technological advancements focusing on energy efficiency and the inherent sustainability benefits of MoSi2 elements are also contributing to market expansion. Key players such as Kanthal, I Squared R, and ZIRCAR operate in this market with extensive product portfolios.

MARKET DYNAMICS

MARKET DRIVERS

Rising Industrial Furnace Demand Across Key Sectors to Propel Market Expansion

The industrial furnace sector is experiencing robust growth globally, driven by expanding manufacturing activities in metallurgy, ceramics, electronics, and glass production. Molybdenum Disilicide (MoSi2) Elements have become indispensable components in these high-temperature applications due to their exceptional thermal stability and oxidation resistance at temperatures reaching 1900°C. The global industrial furnace market, valued at approximately $11.2 billion in 2023, is projected to grow at a compound annual growth rate of 5.8% through 2030, creating substantial demand for advanced heating elements. Particularly in the Asia-Pacific region, which accounts for over 42% of MoSi2 element consumption, rapid industrialization in countries like China and India is driving furnace installations. China alone represents nearly 35% of global industrial furnace capacity, with its steel production reaching 1.018 billion metric tons in 2023, requiring extensive high-temperature processing equipment that utilizes MoSi2 heating elements.

Technological Advancements in Energy-Efficient Furnace Designs to Accelerate Adoption

Recent innovations in furnace technology focusing on energy efficiency and reduced environmental impact are significantly driving MoSi2 element adoption. Modern furnace designs incorporating MoSi2 elements demonstrate up to 30% higher energy efficiency compared to conventional heating systems, translating to substantial operational cost savings and reduced carbon emissions. The 1800°C grade MoSi2 elements, which hold approximately 57% market share, are particularly favored in these advanced applications due to their optimal balance of performance and durability. Manufacturers are increasingly integrating smart control systems with MoSi2 heating elements, enabling precise temperature management and predictive maintenance capabilities. These technological enhancements are crucial as industries face growing pressure to meet stringent environmental regulations while maintaining production efficiency.

Expansion of Semiconductor and Electronics Manufacturing to Fuel Market Growth

The global semiconductor industry’s exponential growth is creating substantial opportunities for MoSi2 heating elements, particularly in diffusion furnaces and rapid thermal processing equipment. With semiconductor manufacturing capital expenditures reaching $190 billion in 2023 and projected to exceed $240 billion by 2026, the demand for high-precision heating solutions is accelerating. MoSi2 elements provide the critical temperature stability required for semiconductor wafer processing, where temperature variations as small as 1°C can significantly impact product yield. The electronics sector’s shift toward smaller feature sizes and more complex materials necessitates heating elements capable of maintaining precise thermal profiles at extreme temperatures, making MoSi2 the material of choice for leading semiconductor equipment manufacturers.

MARKET CHALLENGES

High Production Costs and Raw Material Price Volatility to Constrain Market Penetration

Despite growing demand, the MoSi2 element market faces significant cost-related challenges that impact affordability and adoption rates, particularly in price-sensitive emerging markets. The manufacturing process involves sophisticated powder metallurgy techniques and high-temperature sintering, requiring substantial energy consumption and specialized equipment. Raw material costs, particularly molybdenum and silicon, have experienced volatility, with molybdenum prices fluctuating between $25 and $45 per kilogram over the past two years. These cost pressures are compounded by the need for strict quality control measures to ensure product reliability in extreme operating conditions. The resulting high product pricing creates adoption barriers for small and medium-sized enterprises, limiting market expansion in certain segments and regions.

Other Challenges

Technical Limitations in Certain Operating Environments

MoSi2 elements demonstrate reduced performance in environments containing certain corrosive gases or under rapid thermal cycling conditions. The protective silica layer that provides oxidation resistance can be compromised in reducing atmospheres or in the presence of volatile compounds, potentially limiting application scope. Additionally, thermal shock resistance remains a concern in applications requiring rapid temperature changes, as the brittle nature of the material can lead to cracking and reduced service life under extreme cycling conditions.

Supply Chain Vulnerabilities and Geopolitical Factors

The concentration of molybdenum production in specific geographic regions creates supply chain vulnerabilities and potential price instability. China controls approximately 52% of global molybdenum production, while North and South America account for most of the remainder. This geographic concentration, combined with evolving trade policies and transportation challenges, introduces uncertainty in raw material availability and pricing, affecting manufacturing planning and cost structures throughout the value chain.

MARKET RESTRAINTS

Competition from Alternative Heating Technologies to Limit Market Share Growth

The MoSi2 element market faces increasing competition from emerging heating technologies, particularly silicon carbide (SiC) and graphite-based elements, which offer competitive performance in certain applications. Silicon carbide elements, while generally operating at lower maximum temperatures (approximately 1600°C), provide advantages in thermal shock resistance and cost-effectiveness for specific temperature ranges. The global silicon carbide heating elements market, valued at approximately $480 million in 2023, continues to capture applications where extreme temperature capability is not the primary requirement. Additionally, advancements in graphite element technology have improved their oxidation resistance and mechanical properties, creating alternative solutions for high-temperature applications. These competitive pressures require MoSi2 manufacturers to continuously innovate and demonstrate superior value propositions to maintain market position.

Technical Complexity and Specialized Installation Requirements to Hinder Adoption

The installation and operation of MoSi2 heating elements require specialized knowledge and careful handling due to their brittle nature and specific electrical characteristics. Proper installation necessitates trained technicians who understand the unique requirements of these elements, including appropriate support systems, electrical connections, and power control configurations. The global shortage of skilled furnace technicians and engineers, particularly in rapidly industrializing regions, creates implementation challenges and can lead to suboptimal performance when installation is performed by inadequately trained personnel. This technical complexity adds to the total cost of ownership and can delay adoption decisions, particularly in facilities with limited technical resources or experience with advanced heating technologies.

MARKET OPPORTUNITIES

Growing Renewable Energy and Energy Storage Applications to Create New Market Frontiers

The rapidly expanding renewable energy and energy storage sectors present significant growth opportunities for MoSi2 heating elements, particularly in materials processing for battery production and solar cell manufacturing. The global lithium-ion battery market, projected to reach $180 billion by 2030, requires sophisticated thermal processing equipment for electrode material production and cell assembly. MoSi2 elements are increasingly adopted in calcination and sintering furnaces for battery material processing, where precise temperature control at extreme temperatures is essential for product quality and performance. Similarly, the solar industry’s shift toward higher efficiency photovoltaic technologies necessitates advanced thermal processing equipment utilizing MoSi2 heating elements for silicon wafer and cell production. These emerging applications represent substantial untapped market potential beyond traditional industrial furnace segments.

Advancements in Additive Manufacturing and High-Temperature Materials to Drive Innovation

The additive manufacturing industry’s progression toward high-temperature material processing creates new application opportunities for MoSi2 heating elements. As metal 3D printing expands into refractory metals and advanced ceramics, the requirement for heating elements capable of maintaining precise temperatures exceeding 1700°C becomes increasingly critical. The global additive manufacturing market, valued at approximately $18.3 billion in 2023, is experiencing particularly strong growth in industrial and healthcare applications requiring high-temperature processing capabilities. Additionally, research and development in ultra-high temperature ceramics and composite materials are driving demand for advanced heating solutions in laboratory and pilot-scale furnaces, creating specialized market segments where MoSi2 elements demonstrate distinct performance advantages.

Strategic Partnerships and Vertical Integration to Enhance Market Position

Leading manufacturers are pursuing strategic partnerships and vertical integration strategies to strengthen their market position and capture additional value throughout the supply chain. Recent industry movements include collaborations between MoSi2 element producers and furnace manufacturers to develop integrated heating solutions optimized for specific applications. Several key players have announced backward integration initiatives to secure raw material supplies and reduce cost structures, while others are expanding their service offerings to include installation, maintenance, and refurbishment services. These strategic developments enable manufacturers to differentiate their offerings, improve customer retention, and capture higher-margin service revenue streams. The trend toward comprehensive solution providers rather than component suppliers represents a significant opportunity for established players with technical expertise and application knowledge.

MOLYBDENUM DISILICIDE (MOSI2) ELEMENT MARKET TRENDS

Advancements in High-Temperature Industrial Furnace Technology to Emerge as a Trend in the Market

Advancements in high-temperature industrial furnace technology, particularly the integration of sophisticated heating systems, have revolutionized thermal processing and significantly increased the demand for Molybdenum Disilicide (MoSi2) elements. Recent innovations focus on enhancing the energy efficiency and operational lifespan of these elements, with manufacturers developing new protective coatings that reduce oxidation and extend service life by up to 25%. Moreover, the integration of smart control systems and IoT-enabled monitoring has significantly improved temperature uniformity and reduced energy consumption in furnace operations, making MoSi2 elements more attractive for modern industrial applications requiring precise thermal management.

Other Trends

Sustainability and Energy Efficiency Initiatives

The growing emphasis on sustainability and energy efficiency in industrial processes has significantly heightened the demand for high-performance heating elements, driving market growth in thermal processing applications. MoSi2 elements offer superior thermal efficiency compared to alternative materials, with energy savings of approximately 15-20% in high-temperature furnace operations. This efficiency is particularly valuable in energy-intensive industries such as glass manufacturing and metallurgy, where reducing carbon footprint while maintaining operational excellence has become a priority. Furthermore, global environmental regulations pushing for lower energy consumption in industrial heating are accelerating the adoption of these advanced heating solutions across various sectors.

Expansion in Semiconductor and Electronics Manufacturing

The rapid expansion of semiconductor and electronics manufacturing is driving increased utilization of MoSi2 elements in specialized high-temperature processes. The global semiconductor industry’s growth, projected to reach $1 trillion by 2030, requires advanced thermal processing equipment for wafer fabrication, diffusion processes, and CVD applications. MoSi2 heating elements provide the precise temperature control and stability needed for these sensitive manufacturing processes, with temperature uniformity within ±2°C at operating temperatures exceeding 1700°C. This exceptional performance characteristic makes them indispensable in the production of advanced semiconductors, where even minor temperature variations can affect yield and product quality. The trend toward smaller semiconductor nodes and more complex chip architectures further reinforces the need for reliable high-temperature heating solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on High-Temperature Innovation to Secure Market Position

The competitive landscape of the global Molybdenum Disilicide (MoSi2) Element market is fragmented, characterized by a mix of large multinational corporations and specialized regional manufacturers. Kanthal, a part of the Sandvik Group, is a dominant global leader, renowned for its extensive portfolio of high-temperature heating elements and its strong technological expertise in materials science. Their global distribution network and longstanding reputation for reliability in industrial heating applications have secured them a significant market share, particularly in Europe and North America.

I Squared R Element Co., Inc. and ZIRCAR Ceramics, Inc. are also major players, holding considerable market presence. The strength of these companies stems from their deep specialization in refractory materials and custom-engineered solutions for extreme temperature environments. Their growth is further propelled by continuous investment in research and development, allowing them to offer products that meet the evolving demands of sectors like metallurgy and advanced ceramics.

Furthermore, these established players are actively pursuing growth through strategic expansions into emerging markets, particularly in the Asia-Pacific region, which consumes over 40% of global output. New product launches featuring enhanced energy efficiency and longer operational lifespans are key strategies being employed to capture a larger portion of the market during the forecast period.

Meanwhile, several Chinese manufacturers, including Henan Songshan and Yantai Torch, are strengthening their positions by leveraging cost-effective production and deep integration within the region’s vast industrial furnace supply chain. Their aggressive pricing strategies and focus on the domestic market make them formidable competitors, especially in the price-sensitive segments of the industry.

List of Key Molybdenum Disilicide (MoSi2) Element Companies Profiled

- Kanthal (Sweden)

- I Squared R Element Co., Inc. (U.S.)

- Henan Songshan (China)

- ZIRCAR Ceramics, Inc. (U.S.)

- Yantai Torch (China)

- MHI (Japan)

- SCHUPP (Germany)

- Zhengzhou Chida (China)

- Shanghai Caixing (China)

- SILCARB (India)

- American Elements (U.S.)

- Stanford Advanced Materials (U.S.)

Segment Analysis:

By Type

Straight Elements Dominate the Market Due to Their Superior Structural Integrity and Widespread Industrial Adoption

The market is segmented based on type into:

- Straight

- U-shaped

- W-shaped

- L-shaped

- Others

By Application

Industrial Furnace Segment Leads Due to High Demand in Metallurgy and Ceramics Processing

The market is segmented based on application into:

- Industrial Furnace

- Lab Furnace

By Temperature Grade

1800°C Grade Segment Holds the Largest Market Share Owing to its Optimal Balance of Performance and Cost-Efficiency

The market is segmented based on temperature grade into:

- 1700°C Grade

- 1800°C Grade

- 1900°C Grade

By End-User Industry

Metallurgy and Steel Production Segment is the Primary Consumer Driven by High-Temperature Processing Requirements

The market is segmented based on end-user industry into:

- Metallurgy and Steel Production

- Ceramics and Glass Manufacturing

- Electronics and Semiconductor

- Research and Academia

- Others

Regional Analysis: Molybdenum Disilicide (MoSi2) Element Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global MoSi2 element market, accounting for approximately 42% of total consumption. This dominance is driven by the massive manufacturing base and rapid industrialization in countries like China, Japan, and South Korea. China, in particular, is a powerhouse, with its extensive steel production, semiconductor fabrication, and advanced ceramics industries requiring vast quantities of high-temperature heating elements. The widespread adoption of 1800°C grade elements, which hold the largest market share, is particularly notable here, fueled by the need for robust and efficient industrial furnace operations. While cost-competitiveness remains a key purchasing driver, there is a growing, albeit gradual, shift towards more energy-efficient solutions as environmental concerns gain traction alongside relentless industrial expansion.

Europe

Europe represents a mature and technologically advanced market for MoSi2 elements, characterized by stringent environmental and efficiency standards under regulations like the EU’s Industrial Emissions Directive. The demand is primarily driven by the region’s well-established metallurgy, glass, and specialty ceramics sectors, which require high-performance heating solutions for precision manufacturing processes. Innovation is a key differentiator, with a strong focus on enhancing the energy efficiency and lifespan of these elements to reduce the carbon footprint of industrial operations. While the market growth is steady, it is more measured compared to APAC, being driven by furnace refurbishment and technological upgrades rather than greenfield expansion.

North America

The North American market is defined by a high emphasis on reliability and technological superiority. The well-developed aerospace, energy, and research sectors create consistent demand for high-grade MoSi2 elements, particularly for applications in laboratory furnaces and specialized industrial processes. The market is supported by a strong regulatory framework that emphasizes workplace safety and operational efficiency. Investments in modernizing industrial infrastructure, including advanced furnace technologies, further sustain demand. However, the market’s growth potential is somewhat tempered by the offshoring of heavy manufacturing, making the region more reliant on high-value, specialized applications rather than volume consumption.

South America

The market in South America is emerging and presents a landscape of untapped potential mixed with significant challenges. Industrial development, particularly in the mining and metals sectors in countries like Brazil and Chile, drives the need for industrial furnace components. However, economic volatility and inconsistent investment in industrial infrastructure often lead to cyclical demand. Price sensitivity is a major factor, often prioritizing lower-cost alternatives over premium, high-efficiency MoSi2 elements. While the long-term outlook is positive, hinging on regional economic stabilization and industrial growth, the market currently remains a minor contributor on the global stage.

Middle East & Africa

This region represents the smallest but gradually evolving market for MoSi2 elements. Development is primarily concentrated in nations with growing industrial bases, such as those in the GCC focusing on downstream petrochemicals and metals processing. The demand is nascent and is primarily for durable components capable of withstanding harsh operating environments. Progress is frequently hindered by limited local manufacturing capabilities, reliance on imports, and a lack of stringent regulations driving the adoption of advanced heating technologies. Nonetheless, long-term infrastructure development plans suggest a slowly growing market opportunity for suppliers willing to navigate its unique challenges.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Molybdenum Disilicide (MoSi2) Element markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, temperature grade, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of advanced materials, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Molybdenum Disilicide (MoSi2) Element Market?

-> Molybdenum Disilicide (MoSi2) Element Market was valued at 125 million in 2024 and is projected to reach US$ 184 million by 2032, at a CAGR of 5.6% during the forecast period.

Which key companies operate in Global Molybdenum Disilicide (MoSi2) Element Market?

-> Key players include Kanthal, I Squared R, Henan Songshan, ZIRCAR Ceramics, Yantai Torch, MHI, SCHUPP, Zhengzhou Chida, Shanghai Caixing, SILCARB, JX Advanced Metals, Dengfeng Jinyu, Zhengzhou Mingxin, Zhengzhou Chiheng, American Elements, and Stanford Advanced Materials, among others.

What are the key growth drivers?

-> Key growth drivers include high-temperature resistance and durability, growing industrial furnace demand, technological advancements in furnace applications, rapid industrialization in emerging economies, and increasing focus on sustainability and energy efficiency.

Which region dominates the market?

-> Asia-Pacific is the dominant region, holding approximately 42% of the global market share, driven by extensive manufacturing and industrial activities in countries like China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of higher temperature grade elements (1900°C), integration with smart furnace control systems, and increased R&D into more energy-efficient and longer-lasting heating elements.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...