MARKET INSIGHTS

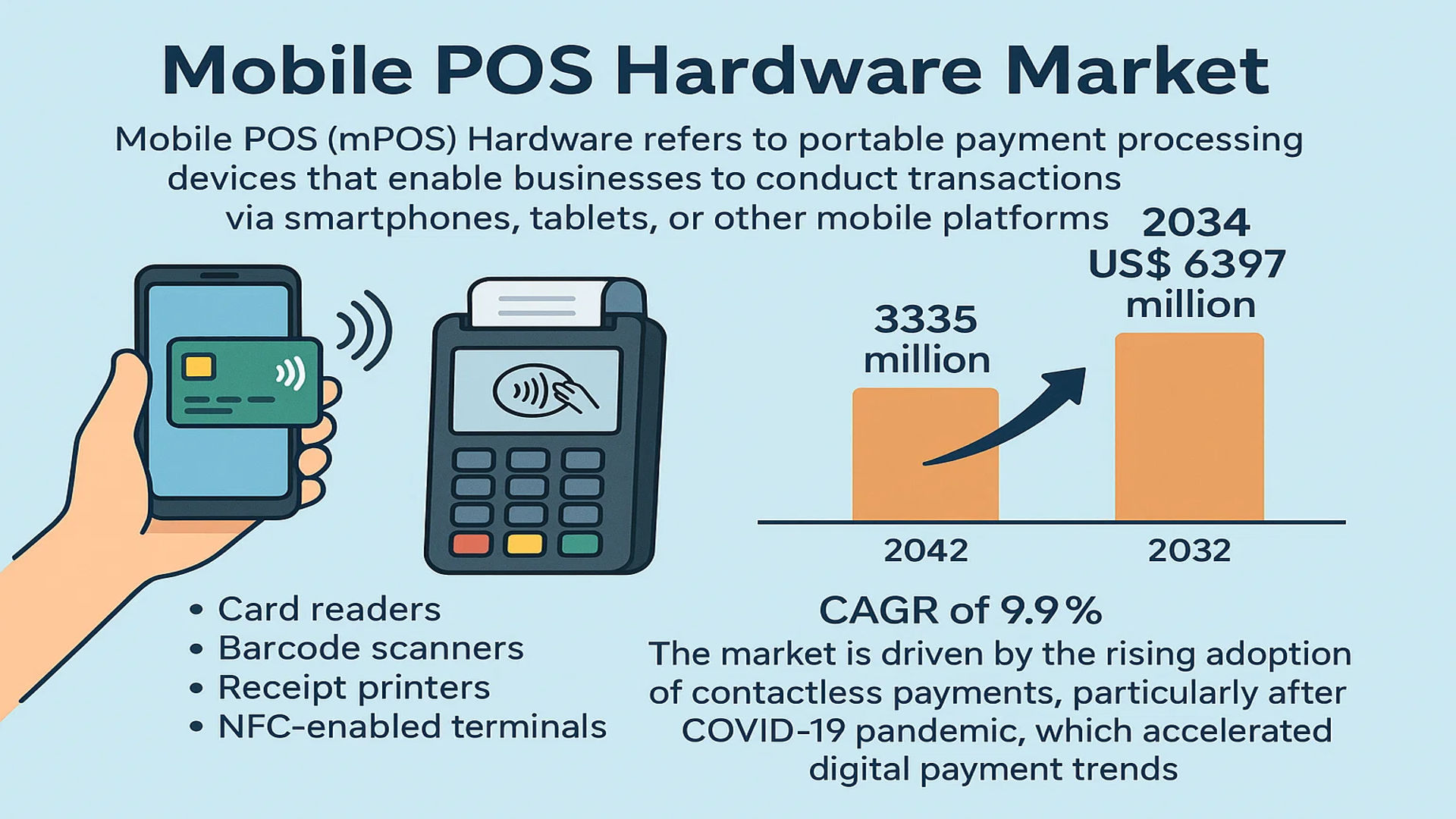

The global Mobile POS Hardware Market was valued at 3335 million in 2024 and is projected to reach US$ 6397 million by 2032, at a CAGR of 9.9% during the forecast period.

Mobile POS (mPOS) Hardware refers to portable payment processing devices that enable businesses to conduct transactions via smartphones, tablets, or other mobile platforms. These solutions include card readers, barcode scanners, receipt printers, and NFC-enabled terminals, offering flexibility for in-store, on-the-go, or curbside payments. The hardware is typically integrated with software solutions to manage inventory, customer data, and analytics in real time.

The market is driven by the rising adoption of contactless payments, particularly after the COVID-19 pandemic, which accelerated digital payment trends. Additionally, the growing preference for cloud-based POS systems among SMEs, due to lower upfront costs and scalability, is fueling demand. Key players such as Verifone, Ingenico (Worldline), and Square dominate the market with advanced security features like EMV compliance and biometric authentication, ensuring secure transactions in retail, hospitality, and other sectors.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Adoption of Contactless Payments to Fuel Market Expansion

The global mobile POS hardware market is experiencing robust growth, primarily driven by the accelerated adoption of contactless payment technologies. Following the COVID-19 pandemic, businesses and consumers increasingly prioritize hygiene and convenience, leading to a surge in demand for tap-to-pay solutions. NFC-enabled mobile POS devices now account for over 70% of newly deployed mPOS units globally, reflecting the rapid shift away from traditional card swiping and cash transactions. This trend is further strengthened by the growing consumer preference for digital wallets and wearables such as Apple Pay and Google Pay.

Retailers across various sectors, from quick-service restaurants to boutique stores, are upgrading their payment infrastructure to accommodate this shift. The hospitality industry has been particularly proactive, with over 60% of hotels and resorts now implementing mobile POS solutions that support contactless check-ins and payments. This fundamental change in payment behavior, combined with technological advancements in secure authentication methods, continues to drive substantial investments in next-generation mPOS hardware.

Small Business Digitization Creates Widespread Demand for mPOS Solutions

Small and medium enterprises (SMEs) represent the fastest-growing segment adopting mobile POS hardware, driven by the need for affordable yet sophisticated payment solutions. Traditional POS systems often prove cost-prohibitive for small businesses, with setup costs averaging 3-4 times higher than modern mPOS alternatives. Mobile POS hardware offers these businesses a compelling combination of lower upfront costs, greater flexibility, and access to advanced features previously available only to larger enterprises.

Food trucks, pop-up stores, and independent retailers particularly benefit from these portable systems. The hardware’s modular design allows seamless integration with inventory management, CRM systems, and accounting software – capabilities demonstrated by leading solutions like Square and Toast. Furthermore, the ability to process payments anywhere with cellular or Wi-Fi connectivity has revolutionized operations for mobile businesses, contributing significantly to the market’s expansion.

➤ For instance, a leading mPOS provider recently introduced a compact device that combines payment processing, barcode scanning, and receipt printing in a single handheld unit, reducing hardware costs by 40% for small retailers.

MARKET CHALLENGES

Persistent Security Vulnerabilities Threaten Market Confidence

While mobile POS hardware offers numerous advantages, security concerns remain a significant challenge hindering broader adoption. The portable nature of these devices increases their susceptibility to theft and tampering, with attempted fraud incidents rising approximately 15% annually. EMV compliance has become standard, but many businesses, particularly smaller operators, struggle with implementing comprehensive security protocols across all transaction points.

The rise of sophisticated cyberattacks targeting payment systems has forced manufacturers to allocate substantial resources to security enhancements. Each new generation of mPOS hardware must incorporate advanced encryption, tokenization, and increasingly robust authentication methods. These necessary improvements frequently result in higher production costs that either reduce profit margins or get passed on to end-users, potentially slowing market growth in price-sensitive segments.

Other Challenges

Device Fragmentation Issues

The Android-based nature of most smart POS systems creates compatibility challenges, as businesses must ensure their chosen hardware works seamlessly across different OS versions and device configurations. This fragmentation increases support costs for manufacturers and may lead to inconsistent user experiences.

Battery Life Limitations

Many mobile POS devices struggle with battery performance, especially those incorporating advanced features like high-resolution displays and constant connectivity. Field reports indicate that nearly 30% of service interruptions stem from power management issues, creating operational headaches for businesses with high transaction volumes.

MARKET RESTRAINTS

Regulatory Complexity Slows Global Market Penetration

The mobile POS hardware market faces considerable restraints from varying regional payment regulations and certification requirements. Each major market maintains distinct standards for payment processing devices, forcing manufacturers to develop multiple hardware variants and undergo extensive compliance testing. In the European Union alone, mPOS devices must meet PSD2 requirements, while in North America, PCI DSS compliance remains mandatory.

Emerging markets often present even greater challenges, with some countries imposing local data residency rules or proprietary technical standards. These regulatory hurdles significantly increase time-to-market and development costs, particularly for companies targeting global distribution. The certification process for a new mPOS device can take 6-9 months in some regions, delaying revenue generation and potentially causing businesses to miss crucial market opportunities.

MARKET OPPORTUNITIES

Emerging Markets Present Significant Untapped Potential

While developed markets show strong mPOS adoption, emerging economies represent the most substantial growth opportunity for mobile POS hardware providers. Countries across Southeast Asia, Latin America, and Africa are experiencing rapid mobile payment adoption, often leapfrogging traditional banking infrastructure altogether. In these regions, smartphone penetration has surpassed 70%, creating ideal conditions for mPOS deployment among small merchants and mobile businesses.

Manufacturers are responding with devices specifically designed for emerging market conditions – ruggedized hardware, extended battery life, and support for alternative payment methods including QR codes and mobile money. These tailored solutions address local needs while maintaining global security standards, positioning providers for significant growth as financial inclusion initiatives continue expanding access to digital payments.

The ongoing shift toward unified commerce solutions also creates opportunities for mPOS providers to expand into adjacent services. Integration with e-commerce platforms, buy-online-pickup-in-store (BOPIS) systems, and omnichannel retail management tools allows hardware vendors to transition into comprehensive commerce enablement partners. This evolution from single-purpose devices to multifunctional business platforms represents a strategic avenue for sustained market expansion.

MOBILE POS HARDWARE MARKET TRENDS

Rapid Adoption of Contactless Payments Propels Market Growth

The global Mobile POS (mPOS) hardware market is experiencing robust growth, driven primarily by the accelerated adoption of contactless payment solutions. In 2024, the market was valued at $3.3 billion and is projected to reach $6.4 billion by 2032, reflecting a 9.9% CAGR during the forecast period. The shift towards NFC-enabled tap-and-go transactions has been a game-changer, especially in retail and hospitality sectors. Businesses are increasingly integrating mobile POS systems with digital wallets like Apple Pay and Google Pay, enhancing convenience and transaction speed for consumers. The post-pandemic emphasis on hygienic payment methods has further cemented this trend, with many enterprises now prioritizing hardware that supports seamless contactless interactions.

Other Trends

Cloud-Based Solutions Reshape Business Operations

Another critical trend shaping the mPOS hardware market is the growing preference for cloud-based systems. These solutions are particularly attractive to small and medium-sized enterprises (SMEs) due to their cost-effectiveness, scalability, and remote management capabilities. Cloud-based POS systems eliminate the need for expensive on-premise infrastructure, allowing businesses to access real-time sales and inventory data from anywhere. This flexibility has proven invaluable for businesses with multiple locations or those operating in dynamic environments, such as food trucks, pop-up stores, and event vendors. The ability to integrate with CRM and accounting software has also streamlined back-end operations, making cloud-based mPOS systems a cornerstone of modern retail agility.

Expansion into Emerging Markets Fuels Demand

The mPOS market is witnessing significant expansion in regions like Asia Pacific, Latin America, and Africa, where mobile penetration is high but traditional banking infrastructure remains limited. In these markets, mobile POS hardware serves as a bridge, enabling small businesses to participate in digital commerce without heavy upfront investments. Additionally, governments and fintech firms in these regions are driving adoption through initiatives aimed at financial inclusion. The flexibility of mPOS solutions aligns perfectly with the needs of informal retail sectors and micro-enterprises, making them instrumental in fostering economic growth. With mobile payment volumes skyrocketing in developing economies, this trend is expected to sustain long-term market momentum.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Acquisitions Shape the mPOS Hardware Market

The global Mobile POS (mPOS) hardware market is characterized by intense competition among established players and emerging innovators. Verifone and Ingenico (Worldline) currently dominate the market, holding approximately 30% combined revenue share in 2024. Their leadership stems from comprehensive product portfolios and strong partnerships with financial institutions worldwide. Both companies have recently focused on enhancing their contactless payment capabilities and cloud-based solutions to meet evolving merchant needs.

PAX Technology has emerged as a key challenger, particularly in the Asia-Pacific region, where its affordable Android-based devices have gained significant traction. The company’s growth reflects the broader industry shift toward smart POS systems, which accounted for 68% of global mPOS hardware sales in 2024. Meanwhile, Square continues to revolutionize the market with its vertically integrated ecosystem, particularly appealing to micro-merchants and mobile businesses through its simple pricing model and sleek hardware designs.

The competitive landscape is further energized by regional specialists like Newland NPT in China and BBPOS in global mobile payment peripherals. These companies are gaining market share by offering localized solutions and competitive pricing. Industry consolidation is accelerating as major players acquire innovative startups to expand their technological capabilities – a trend exemplified by Worldline’s acquisition of Ingenico in 2022.

Looking forward, differentiation through value-added services will be crucial. Companies are increasingly bundling hardware with software solutions like inventory management, customer analytics, and loyalty programs. Security remains a key battleground, with leaders investing heavily in PCI-certified devices and tokenization technologies to address rising cybersecurity concerns in digital payments.

List of Key Mobile POS Hardware Companies Profiled

- Verifone (U.S.)

- Ingenico (Worldline) (France)

- PAX Technology (China)

- Newland NPT (China)

- New POS Technology (China)

- Shenzhen Xinguodu Technology (China)

- Wuhan Tianyu Information (China)

- BBPOS (China/Hong Kong)

- Centerm (China)

- MoreFun Electronic Technology (China)

- Posiflex Technology (Taiwan)

- NCR Voyix (U.S.)

- Beijing Shenzhou Anfu Technology (China)

- Datecs (Bulgaria)

- SZZT (China)

- ADVANTECH-AURES (France)

- Miura Systems (U.K.)

- PayCore (Turkey)

- Bitel (South Korea)

- Square (U.S.)

- Touch Dynamic (U.S.)

Segment Analysis:

By Type

Smart POS Segment Dominates with Advanced Features and Cloud Integration

The market is segmented based on type into:

- Smart POS

- Subtypes: NFC-enabled, Biometric-enabled, and Hybrid models

- Non-smart POS

- Subtypes: Basic card readers and Chip & PIN terminals

By Application

Retail Industry Leads Mobile POS Adoption for Enhanced Customer Experience

The market is segmented based on application into:

- Retail

- Restaurant

- Hospitality

- Entertainment

- Other

By Connectivity

Wireless Connectivity Solutions Gain Traction for Mobility Advantages

The market is segmented based on connectivity into:

- Wi-Fi

- Bluetooth

- 4G/5G

- Wired

By Component

Integrated Hardware-Software Solutions Becoming Industry Standard

The market is segmented based on component into:

- Card Readers

- Scanners

- Printers

- Software Solutions

Regional Analysis: Mobile POS Hardware Market

Asia-Pacific

The Asia-Pacific region dominates the global Mobile POS Hardware market, driven by rapid digital transformation, increasing smartphone penetration, and the rise of cashless economies. Countries like China, India, and Japan are at the forefront, with China alone accounting for over 35% of regional mPOS adoption. The growing number of SMEs and mobile-first payment solutions has accelerated demand for portable, cost-effective POS hardware. Governments are also supporting cashless initiatives—for instance, India’s Unified Payments Interface (UPI) recorded nearly 10 billion transactions in March 2024, reflecting the shift toward digital payments. Despite this momentum, fragmented regulatory frameworks and cybersecurity concerns pose challenges. However, localized innovations, such as low-cost NFC-enabled devices and vernacular software integration, are helping bridge accessibility gaps.

North America

North America is a mature yet high-growth market, with the U.S. contributing over 70% of regional revenue. The adoption of Mobile POS Hardware is fueled by the dominance of contactless payments, cloud-based SaaS integrations, and demand from omnichannel retail sectors. Leading providers such as Square and NCR Voyix have pioneered advanced EMV-compliant solutions tailored for businesses ranging from pop-up stores to large franchises. The U.S. mobile payment transaction value is projected to exceed $1.2 trillion by 2026, reflecting strong consumer preference for tap-and-go transactions. However, stricter data privacy laws and higher hardware costs compared to emerging markets may temper growth among small vendors.

Europe

Europe’s Mobile POS Hardware market thrives on regulatory support for digital payments, including PSD2 compliance mandates and GDPR-driven security standards. The U.K., Germany, and France collectively represent 60% of regional adoption, with hospitality and retail sectors leading deployments. NFC technology is widely embraced, with over 80% of POS terminals in Western Europe being contactless-ready. However, saturation in mature economies and slower adoption in Eastern Europe due to legacy banking infrastructure limit broader growth. Local players like Ingenico (Worldline) focus on eco-friendly, modular hardware to align with the EU’s sustainability goals, while fintech partnerships drive innovation in cross-border payment solutions.

South America

South America exhibits strong potential, with Brazil and Argentina spearheading Mobile POS Hardware adoption amid rising e-commerce and government-led financial inclusion programs. Over 50% of Brazilian SMEs now use mPOS devices, leveraging solutions like Mercado Pago’s portable card readers. However, currency volatility and uneven internet connectivity in rural areas hinder scalability. The region also faces unique challenges, such as high fraud rates, prompting vendors to prioritize biometric authentication and offline transaction capabilities. Despite these hurdles, fintech investments and localized payment methods (e.g., Pix in Brazil) are accelerating market penetration.

Middle East & Africa

The MEA market is nascent but growing rapidly, with the UAE, Saudi Arabia, and South Africa accounting for the majority of deployments. Mobile POS adoption is driven by tourism-heavy economies and initiatives like Saudi Vision 2030, which promotes cashless transactions. In Africa, mobile money platforms (e.g., M-Pesa) complement mPOS growth, particularly in Kenya and Nigeria. Yet, low banking penetration and reliance on informal retail sectors slow widespread adoption. Vendors are addressing this by offering rugged, solar-powered devices and pay-as-you-go pricing models tailored to microbusinesses. Long-term growth is anticipated as 4G/5G infrastructure expands and regulatory frameworks evolve.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Mobile POS Hardware markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, contactless payment solutions, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for hardware manufacturers, payment processors, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Mobile POS Hardware Market?

-> Mobile POS Hardware Market was valued at 3335 million in 2024 and is projected to reach US$ 6397 million by 2032, at a CAGR of 9.9% during the forecast period.by 2032.

Which key companies operate in Global Mobile POS Hardware Market?

-> Key players include Verifone, Ingenico (Worldline), PAX Technology, Newland NPT, Square, NCR Voyix, and BBPOS, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of contactless payments, SME digital transformation, cloud-based POS solutions, and mobile payment penetration in emerging economies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America currently holds the largest market share.

What are the emerging trends?

-> Emerging trends include biometric authentication, AI-powered analytics, integrated business management features, and sustainable hardware solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...