MLCC Market Insights

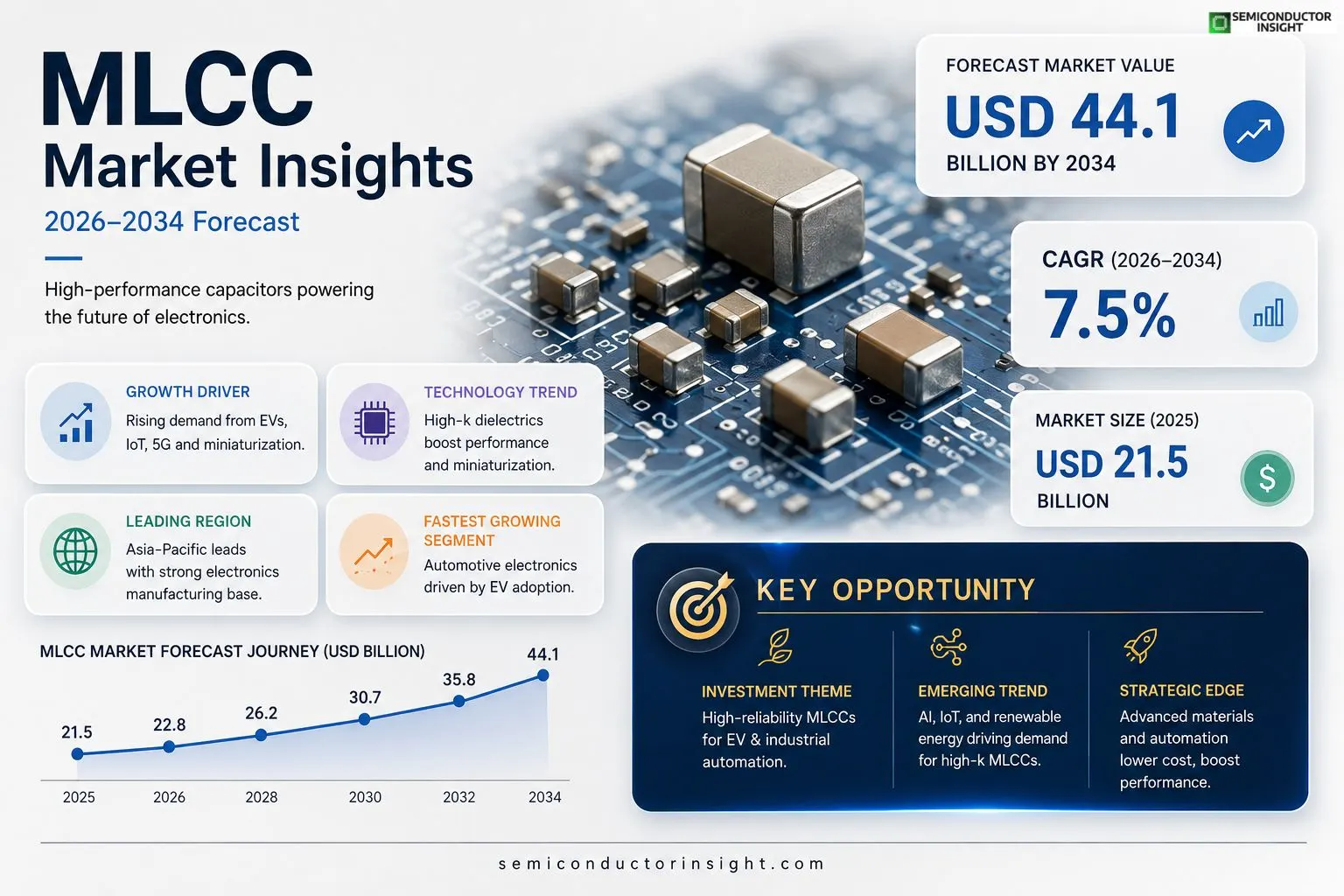

Global MLCC market size was valued at USD 21.5 billion in 2025. The market is projected to grow from USD 22.8 billion in 2026 to USD 44.1 billion by 2034, exhibiting a CAGR of 7.5% during the forecast period.

Multilayer ceramic capacitors (MLCCs) are passive electronic components consisting of alternating layers of ceramic dielectric material and metal electrodes. They deliver high capacitance within a compact footprint and provide excellent frequency stability and reliability across a wide range of applications.The market is experiencing rapid growth due to several factors, including expanding demand for electric vehicles, rising adoption of Internet‑of‑Things devices, and continued miniaturization trends in smartphones and wearables. Furthermore, advances in high‑k dielectric formulations and automated manufacturing are boosting performance while lowering costs. Initiatives by key players such as Murata Manufacturing Co., TDK Corporation, Samsung Electro‑Mechanics, and Taiyo Yuden are expected to further accelerate MLCC Market.

MARKET DRIVERS

Rising Demand in Consumer Electronics

MLCC Market expanded to roughly $18 billion in 2023, propelled by the proliferation of smartphones, wearables, and IoT devices that require ever‑smaller, high‑performance capacitors. Miniaturization trends and the shift to 5G have increased the capacitance‑per‑volume ratio, driving manufacturers to invest in advanced ceramic formulations.

Electrification of Automotive

Electric‑vehicle (EV) adoption and advanced driver‑assistance systems (ADAS) are creating a surge in power‑density requirements. Vehicles now integrate dozens of MLCCs per module for power‑train control, thermal management, and safety‑critical functions, positioning the automotive segment as a primary growth engine.

➤ The shift to 5G and autonomous vehicles is accelerating MLCC adoption.

In parallel, regulatory standards for reliability and safety are tightening, prompting OEMs to select components with superior dielectric strength. This regulatory pressure further validates the strategic importance of MLCC Market in high‑reliability applications.

MARKET CHALLENGES

Technical Complexity and Cost

Manufacturing multilayer ceramic capacitors demands sub‑micron layer control and precise firing cycles, which inflate production costs. As customers push for thinner profiles, suppliers must balance performance with price competitiveness, a delicate trade‑off that strains profit margins.

Other Challenges

Supply Chain Volatility

Raw‑material shortages, particularly of high‑purity alumina and palladium‑free electrodes, have introduced lead times that exceed six months in some regions. Geopolitical tensions further exacerbate uncertainty, compounding inventory‑management difficulties for manufacturers.

MARKET RESTRAINTS

Environmental Regulations

Globally enforced RoHS and REACH directives restrict the use of hazardous substances in capacitor production. Compliance requires costly material substitutions and additional testing, which can suppress new product launches in tightly regulated markets.Additionally, mature segments such as traditional mobile‑phone capacitors face saturation, leading to incremental price erosion and limited upside for volume‑driven manufacturers.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy

Grid‑integration hardware, solar‑inverter modules, and energy‑storage systems are demanding high‑voltage MLCCs capable of withstanding rapid charge‑discharge cycles. The rise of renewable‑energy infrastructure offers a fresh growth avenue for suppliers that can certify long‑life performance.Moreover, the expansion of AI edge devices requires capacitors with low loss and high reliability at small form factors. This niche creates opportunities for premium‑priced, application‑specific MLCCs that cater to AI‑driven analytics and real‑time processing.

MLCC Market Trends

Rising Demand from Electric Vehicles

The growth of electric‑vehicle (EV) platforms is creating a sustained increase in component procurement, and multilayer ceramic capacitors are a core element in power‑train control modules, battery‑management systems, and on‑board chargers. Engineers favor MLCCs because they combine a compact footprint with high voltage tolerance and reliable temperature performance, which aligns with the tight packaging constraints of modern EV designs. As manufacturers introduce higher‑capacity battery packs and advanced driver‑assistance features, the need for stable, high‑frequency filtering rises, reinforcing the role of MLCCs as a strategic supply‑chain item for the automotive sector.

Other Trends

IoT Device Expansion

Broad adoption of Internet‑of‑Things (IoT) products is amplifying demand for small, low‑power passive components. MLCCs provide the necessary capacitance density to support wireless connectivity, sensor integration, and extended battery life in devices ranging from smart home hubs to industrial telemetry units. The trend toward edge computing pushes makers to embed more functionality within a single module, prompting designers to rely on MLCCs for both decoupling and timing applications. This pressure drives suppliers to optimize lead‑time and cost structures while maintaining the high reliability standards required for remotely deployed devices.

Advances in High‑k Dielectric Materials

Material science breakthroughs in high‑k dielectric formulations are delivering notable performance gains without enlarging the component size. By increasing the dielectric constant, manufacturers achieve greater capacitance per unit area, which directly supports the miniaturization agenda in smartphones, wearables, and compact medical instruments. Coupled with automation upgrades in firing and assembly processes, these advances lower production expenses and improve product consistency. The combined effect is a more competitive offering that meets the accelerating pace of electronic innovation, ensuring that MLCCs remain a preferred solution across diverse high‑volume markets.

COMPETITIVE LANDSCAPEKey Industry Players

MLCC Market Competitive Landscape Overview

The multilayer ceramic capacitor (MLCC) segment is dominated by a few global powerhouses that control the majority of high‑volume capacity. Murata Manufacturing Co. leads the market with a broad portfolio ranging from standard 0603 parts to advanced high‑k micro‑MLCCs for automotive and 5G infrastructure. TDK Corporation follows closely, leveraging its extensive dielectric research and large-scale automation to capture both consumer‑electronics and industrial shares. Samsung Electro‑Mechanics has rapidly expanded its capacity in South Korea and China, focusing on miniaturized MLCCs for smartphones and wearables, while Taiyo Yuden remains a specialist in high‑reliability components for medical and aerospace applications. These incumbents benefit from deep supply‑chain integration, sizable R&D budgets, and strategic partnerships with OEMs, reinforcing a tiered market structure where large manufacturers serve mass‑market demand and niche players target performance‑critical segments.Beyond the top tier, several niche and regional firms contribute significant innovation and competitive pressure. Kyocera and AVX (a Kyocera subsidiary) excel in high‑voltage and high‑temperature MLCCs, catering to automotive power‑train and industrial motor markets. Vishay’s capacitance portfolio emphasizes automotive safety standards, while Yageo and KEMET (now part of Yageo) focus on cost‑effective solutions for emerging IoT devices. Chinese manufacturers such as Jiangsu Changjiang and Shanghai Jiao Tong’s Tianhua specialize in ultra‑low‑profile designs for portable electronics, narrowing the price gap with Western rivals. These players sustain market dynamism by addressing specialized applications, offering alternative supply sources, and driving incremental improvements in dielectric materials and manufacturing yields.

List of Key MLCC Companies Profiled

- Murata Manufacturing Co.

- TDK Corporation

- Samsung Electro‑Mechanics

- Taiyo Yuden

- Kyocera

- AVX

- Vishay Intertechnology

- Yageo Corporation

- KEMET Corporation

- Jiangsu Changjiang Electronics

- Shanghai Tianhua Electronics

- Panasonic Industrial Devices

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

X7R is the dominant sub‑segment because:

|

| By Application |

|

Automotive electronics lead the application landscape because:

|

| By End User |

|

Smartphone manufacturers dominate end‑user demand because:

|

| By Technology |

|

High‑k dielectric formulations have become the technology of choice because:

|

| By Performance Requirement |

|

High reliability and long life are prioritized because:

|

Regional Analysis: North America

North America

The automotive industry is a major consumer of MLCCs, utilized in various electronic control units (ECUs), infotainment systems, and power management circuits. The shift towards electric vehicles (EVs) is creating significant demand for high-performance, reliable MLCCs capable of withstanding harsh operating conditions. The increasing complexity of automotive electronics, coupled with stringent safety regulations, is driving innovation in MLCC technology.

The consumer electronics sector remains a dominant force in MLCC Market. Smartphones, laptops, tablets, and other portable devices rely heavily on MLCCs for power supply, filtering, and signal conditioning. The constant demand for smaller, more powerful, and energy-efficient devices is driving the adoption of advanced MLCC technologies with higher capacitance and lower losses. The trend towards foldable displays and flexible electronics will further boost MLCC demand in this segment.

The industrial sector utilizes MLCCs in a wide range of applications, including power supplies, motor drives, and programmable logic controllers (PLCs). The increasing adoption of Industry 4.0 and IoT (Internet of Things) solutions is driving demand for MLCCs that can operate reliably in harsh environments and withstand high temperatures and vibrations. The need for energy-efficient industrial equipment is also stimulating the adoption of MLCCs with low equivalent series resistance (ESR).

The expansion of 5G networks is creating significant demand for MLCCs in base stations, network switches, and other telecommunications equipment. The stringent performance requirements of 5G applications necessitate the use of high-reliability, high-frequency MLCCs. The increasing bandwidth demands and the need for low latency are driving innovation in MLCC materials and packaging.

Europe

The European MLCC market exhibits steady growth, driven by the automotive, industrial, and consumer electronics sectors. Stringent environmental regulations and a focus on sustainable manufacturing practices are influencing the selection of MLCC materials and processes within the region. The European Union’s push for digitalization and smart manufacturing initiatives are further boosting demand for MLCCs. The market is characterized by a strong emphasis on quality and compliance with European standards.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing MLCC market globally. China is the dominant player, driven by its massive electronics manufacturing base and growing domestic demand. Other key markets in the region include Japan, South Korea, and Taiwan, which are centers of technological innovation and manufacturing excellence. The rapid expansion of the 5G infrastructure and the increasing adoption of electric vehicles are fueling significant growth in the Asia-Pacific MLCC market. Competition is intense, with numerous domestic and international players vying for market share.

South America

South America presents a moderate growth opportunity for MLCC Market, primarily driven by the expanding consumer electronics and industrial sectors in Brazil and Argentina. The increasing adoption of smartphones, tablets, and other electronic devices is boosting demand for MLCCs. The growing automotive industry in the region is also contributing to MLCC demand. However, economic uncertainties and currency fluctuations can pose challenges to market growth.

Middle East & Africa

The Middle East and Africa represent a relatively smaller but growing market for MLCCs. The increasing investment in infrastructure development, particularly in the telecommunications and automotive sectors, is driving demand. The expansion of the consumer electronics market in countries like Saudi Arabia and South Africa is also contributing to market growth. The region’s growing focus on renewable energy is also creating opportunities for MLCCs in power conversion and energy storage applications.

Report Scope

This market research report provides a comprehensive analysis of the MLCC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MLCC Market?

-> MLCC Market was valued at USD 21.5 billion in 2025 and is expected to reach USD 44.1 billion by 2034.

Which key companies operate in MLCC Market?

-> Key players include Murata Manufacturing Co., TDK Corporation, Samsung Electro‑Mechanics, and Taiyo Yuden, among others.

What are the key growth drivers?

-> Key growth drivers include expanding demand for electric vehicles, rising adoption of Internet‑of‑Things devices, continued miniaturization in smartphones and wearables, and advances in high‑k dielectric formulations and automated manufacturing.

Which region dominates the market?

-> The provided reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include high‑k dielectric materials, increased automation in production, integration of MLCCs in EV and IoT applications, and ongoing device miniaturization driving innovative package designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...